OPEN-SOURCE SCRIPT

Inverse Fisher Transform on SMI (Stochastic Momentum Index)

Updated

Inverse Fisher Transform on SMI (Stochastic Momentum Index)

About John EHLERS:

From California, USA, John is a veteran trader. With 35 years trading experience he has seen it all. John has an engineering background that led to his technical approach to trading ignoring fundamental analysis (with one important exception).

John strongly believes in cycles. He’d rather exit a trade when the cycle ends or a new one starts. He uses the MESA principle to make predictions about cycles in the market and trades one hundred percent automatically.

In the show John reveals:

• What is more appropriate than trading individual stocks

• The one thing he relies upon in his approach to the market

• The detail surrounding his unique trading style

• What important thing underpins the market and gives every trader an edge

About INVERSE FISHER TRANSFORM:

The purpose of technical indicators is to help with your timing decisions to buy or

sell. Hopefully, the signals are clear and unequivocal. However, more often than

not your decision to pull the trigger is accompanied by crossing your fingers.

Even if you have placed only a few trades you know the drill.

In this article I will show you a way to make your oscillator-type indicators make

clear black-or-white indication of the time to buy or sell. I will do this by using the

Inverse Fisher Transform to alter the Probability Distribution Function (PDF) of

your indicators. In the past12 I have noted that the PDF of price and indicators do

not have a Gaussian, or Normal, probability distribution. A Gaussian PDF is the

familiar bell-shaped curve where the long “tails” mean that wide deviations from

the mean occur with relatively low probability. The Fisher Transform can be

applied to almost any normalized data set to make the resulting PDF nearly

Gaussian, with the result that the turning points are sharply peaked and easy to

identify. The Fisher Transform is defined by the equation

1)

Whereas the Fisher Transform is expansive, the Inverse Fisher Transform is

compressive. The Inverse Fisher Transform is found by solving equation 1 for x

in terms of y. The Inverse Fisher Transform is:

2)

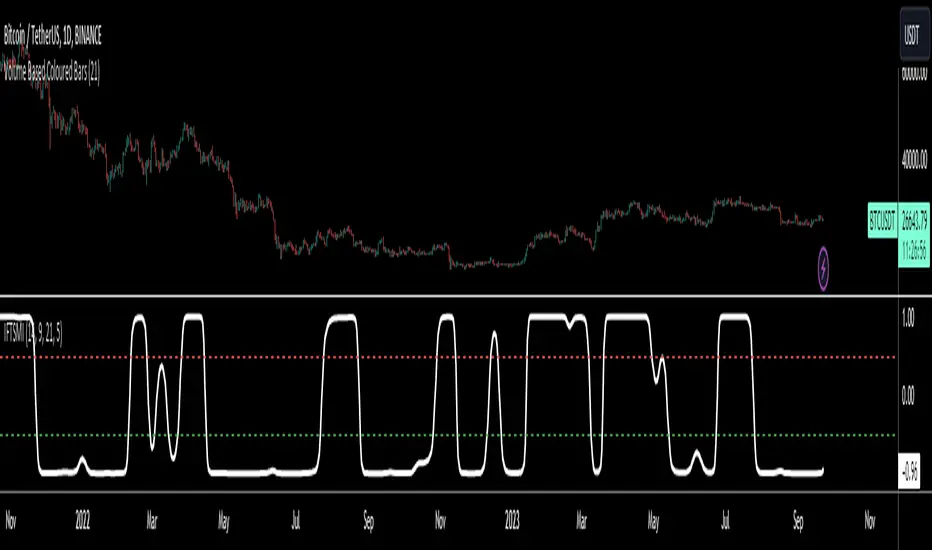

The transfer response of the Inverse Fisher Transform is shown in Figure 1. If

the input falls between –0.5 and +0.5, the output is nearly the same as the input.

For larger absolute values (say, larger than 2), the output is compressed to be no

larger than unity. The result of using the Inverse Fisher Transform is that the

output has a very high probability of being either +1 or –1. This bipolar

probability distribution makes the Inverse Fisher Transform ideal for generating

an indicator that provides clear buy and sell signals.

About John EHLERS:

From California, USA, John is a veteran trader. With 35 years trading experience he has seen it all. John has an engineering background that led to his technical approach to trading ignoring fundamental analysis (with one important exception).

John strongly believes in cycles. He’d rather exit a trade when the cycle ends or a new one starts. He uses the MESA principle to make predictions about cycles in the market and trades one hundred percent automatically.

In the show John reveals:

• What is more appropriate than trading individual stocks

• The one thing he relies upon in his approach to the market

• The detail surrounding his unique trading style

• What important thing underpins the market and gives every trader an edge

About INVERSE FISHER TRANSFORM:

The purpose of technical indicators is to help with your timing decisions to buy or

sell. Hopefully, the signals are clear and unequivocal. However, more often than

not your decision to pull the trigger is accompanied by crossing your fingers.

Even if you have placed only a few trades you know the drill.

In this article I will show you a way to make your oscillator-type indicators make

clear black-or-white indication of the time to buy or sell. I will do this by using the

Inverse Fisher Transform to alter the Probability Distribution Function (PDF) of

your indicators. In the past12 I have noted that the PDF of price and indicators do

not have a Gaussian, or Normal, probability distribution. A Gaussian PDF is the

familiar bell-shaped curve where the long “tails” mean that wide deviations from

the mean occur with relatively low probability. The Fisher Transform can be

applied to almost any normalized data set to make the resulting PDF nearly

Gaussian, with the result that the turning points are sharply peaked and easy to

identify. The Fisher Transform is defined by the equation

1)

Whereas the Fisher Transform is expansive, the Inverse Fisher Transform is

compressive. The Inverse Fisher Transform is found by solving equation 1 for x

in terms of y. The Inverse Fisher Transform is:

2)

The transfer response of the Inverse Fisher Transform is shown in Figure 1. If

the input falls between –0.5 and +0.5, the output is nearly the same as the input.

For larger absolute values (say, larger than 2), the output is compressed to be no

larger than unity. The result of using the Inverse Fisher Transform is that the

output has a very high probability of being either +1 or –1. This bipolar

probability distribution makes the Inverse Fisher Transform ideal for generating

an indicator that provides clear buy and sell signals.

Release Notes

Updated to v5 and added multiple Time frame Feature.Open-source script

In true TradingView spirit, the author of this script has published it open-source, so traders can understand and verify it. Cheers to the author! You may use it for free, but reuse of this code in publication is governed by House rules. You can favorite it to use it on a chart.

Telegram t.me/AlgoRhytm

YouTube (Turkish): youtube.com/c/kivancozbilgic

YouTube (English): youtube.com/c/AlgoWorld

YouTube (Turkish): youtube.com/c/kivancozbilgic

YouTube (English): youtube.com/c/AlgoWorld

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.