OPEN-SOURCE SCRIPT

Hurst Spectral Analysis Oscillator

"It is a true fact that any given time history of any event (including the price history of a stock) can always be considered as reproducible to any desired degree of accuracy by the process of algebraically summing a particular series of sine waves. This is intuitively evident if you start with a number of sine waves of differing frequencies, amplitudes, and phases, and then sum them up to get a new and more complex waveform." (Spectral Analysis chapter of J M Hurst's book, Profit Magic)

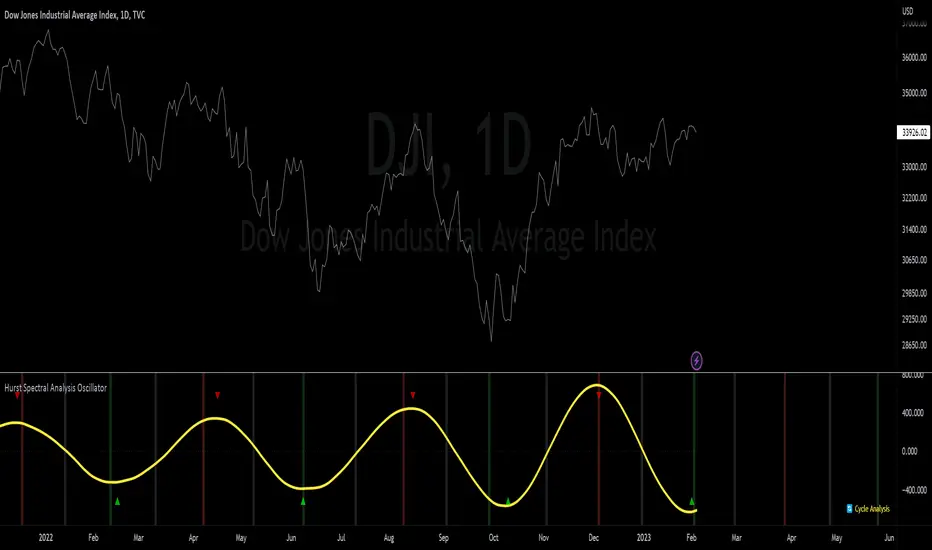

Background: A band-pass filter or bandpass filter is a device that passes frequencies within a certain range and rejects (attenuates) frequencies outside that range. Bandpass filters are widely used in wireless transmitters and receivers. Well-designed bandpass filters (having the optimum bandwidth) maximize the number of signal transmitters that can exist in a system while minimizing the interference or competition among signals. Outside of electronics and signal processing, other examples of the use of bandpass filters include atmospheric sciences, neuroscience, astronomy, economics, and finance.

About the indicator: This indicator will accept float/decimal length inputs to display a spectrum of 11 bandpass filters. The trader can select a single bandpass for analysis that includes future high/low predictions. The trader can also select which bandpasses contribute to a composite model of expected price action.

10 Statements to describe the 5 elements of Hurst's price-motion model:

Shoutouts & Credits for all the raw code, helpful information, ideas & collaboration, conversations together, introductions, indicator feedback, and genuine/selfless help:

🏆 TerryPascoe

🏅 DavidF at Sigma-L, and HPotter

👏 Saviolis, parisboy, and upslidedown

Background: A band-pass filter or bandpass filter is a device that passes frequencies within a certain range and rejects (attenuates) frequencies outside that range. Bandpass filters are widely used in wireless transmitters and receivers. Well-designed bandpass filters (having the optimum bandwidth) maximize the number of signal transmitters that can exist in a system while minimizing the interference or competition among signals. Outside of electronics and signal processing, other examples of the use of bandpass filters include atmospheric sciences, neuroscience, astronomy, economics, and finance.

About the indicator: This indicator will accept float/decimal length inputs to display a spectrum of 11 bandpass filters. The trader can select a single bandpass for analysis that includes future high/low predictions. The trader can also select which bandpasses contribute to a composite model of expected price action.

10 Statements to describe the 5 elements of Hurst's price-motion model:

- Random events account for only 2% of the price change of the overall market and of individual issues.

- National and world historical events influence the market to a negligible degree.

- Foreseeable fundamental events account for about 75% of all price motion. The effect is smooth and slow changing.

- Unforeseeable fundamental events influence price motion. They occur relatively seldom, but the effect can be large and must be guarded against.

- Approximately 23% of all price motion is cyclic in nature and semi-predictable (basis of the "cyclic model").

- Cyclicality in price motion consists of the sum of a number of (non-ideal) periodic cyclic "waves" or "fluctuations" (summation principle).

- Summed cyclicality is a common factor among all stocks (commonality principle).

- Cyclic component magnitude and duration fluctuate slowly with the passage of time. In the course of such fluctuations, the greater the magnitude, the longer the duration and vice-versa (variation principle).

- Principle of nominality: an element of commonality from which variation is expected.

- The greater the nominal duration of a cyclic component, the larger the nominal magnitude (principle of proportionality).

Shoutouts & Credits for all the raw code, helpful information, ideas & collaboration, conversations together, introductions, indicator feedback, and genuine/selfless help:

🏆 TerryPascoe

🏅 DavidF at Sigma-L, and HPotter

👏 Saviolis, parisboy, and upslidedown

Open-source script

In true TradingView spirit, the author of this script has published it open-source, so traders can understand and verify it. Cheers to the author! You may use it for free, but reuse of this code in publication is governed by House rules. You can favorite it to use it on a chart.

Made w/ ❤ by @BarefootJoey ✌💗📈

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.