RunRox - Backtesting System (SM)RunRox - Backtesting System (SM) is designed for flexible and comprehensive testing of trading strategies, closely integrated with our RunRox - Signals Master indicator. This combination enhances your ability to refine strategies efficiently, providing you with insights to adapt and optimize your trading tactics seamlessly.

The Backtesting System (SM) excels in pinpointing the optimal settings for the RunRox - Signals Master indicator, efficiently highlighting the most effective configurations.

Capabilities of the Backtesting System (SM)

Optimal Settings Determination: Identifies the best configurations for the Signals Master indicator to enhance its effectiveness.

Timeframe-Specific Strategy Testing: Allows strategies to be tested over specific historical time periods to assess their viability.

Customizable Initial Conditions: Enables setting of initial deposit, risk per trade, and commission rates to mirror real-world trading conditions.

Flexible Money Management: Provides options to set take profits and stop losses, optimizing potential returns and risk management.

Intuitive Dashboard: Features a user-friendly dashboard that visually displays all pertinent information, making it easy to analyze and adjust strategies.

Trading Flexibility Across Three Modes:

Dual-Direction Trading: Engage in both buying and selling with this mode. Our dashboard optimizes and identifies the best settings for trading in two directions, streamlining the process to maximize effectiveness for both buy and sell orders.

Buy-Only Mode: Tailored for traders focusing exclusively on purchasing assets. In this mode, our backtester pinpoints the most advantageous sensitivity, speed reaction, and filter settings specifically for buying. Optimal settings in this mode may differ from those used in dual-direction trading, providing a customized approach to single-direction strategies.

Sell-Only Mode: Perfect for strategies primarily based on selling. This setting allows you to discover the ideal configurations for asset sales, which can be particularly useful if you are looking for optimal exit points in long-term transactions or under specific market conditions.

Here's an example of how profits can differ on the same asset when trading using two distinct strategies: exclusively buying or trading in both directions.

Above in the image, you can see how one-directional trading influences the results of backtests on historical data. While this does not guarantee future outcomes, it provides insight into how the strategy's performance can vary with different trading directions.

As you can also see from the image, one-directional trading has affected the optimal combination of settings for Sensitivity, Speed Reaction, and Filters.

Stop Loss and Take Profit

Our backtesting system, as you might have gathered, includes flexible settings for take profits and stop losses. Here are the main features:

Multiple Take Profits: Ability to set from 1 to 4 take profit levels.

Fixed Percentage: Option to assign a fixed percentage for each take profit.

Trade Proportion Fixation: Ability to set a fixed size from the trade for securing profits.

Stop Loss Installation: Option to establish a stop loss.

Break-Even Stop Loss: Ability to move the stop loss to a break-even point upon reaching a specified take profit level.

These settings offer extensive flexibility and can be customized according to your preferences and trading style. They are suitable for both novice and professional traders looking to test their trading strategies on historical data.

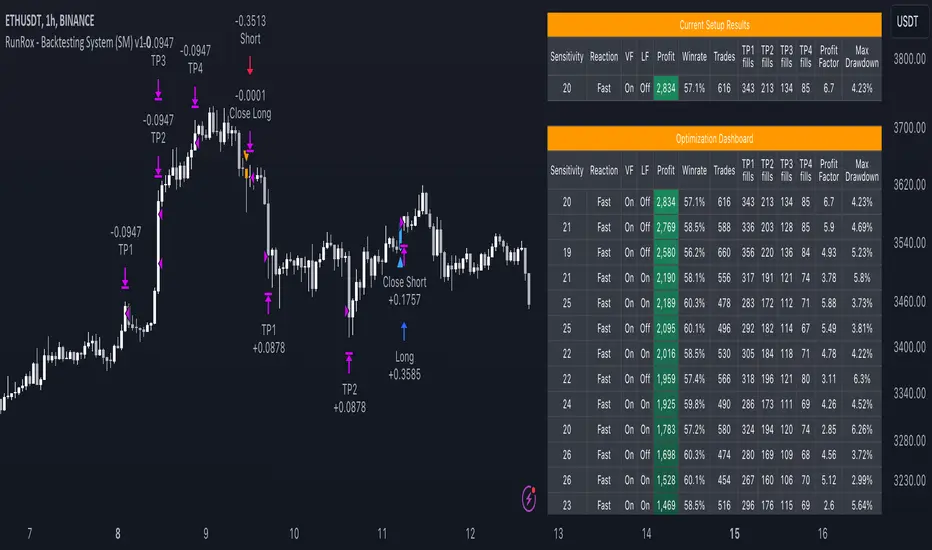

As illustrated in the image above, we have implemented money management by setting fixed take profits and stop losses. Utilizing money management has improved indicators such as profit, maximum drawdown, and profit factor, turning even historically unprofitable strategies into profitable ones. Although this does not guarantee future results, it serves as a valuable tool for understanding the effectiveness of money management.

Additionally, as you can see, the optimal settings for Signals Master have been adjusted, highlighting the best configurations for the most favorable outcomes.

Disclaimer:

Historical data is not indicative of future results. All indicators and strategies provided by RunRox are intended for integration with traders' strategies and should be used as tools for analysis rather than standalone solutions. Traders should use their own discretion and understand that all trading involves risk.

Backtestingsystem

LuxAlgo - Backtester (PAC)The PAC Backtester is an innovative strategy script that allows users to create a wide variety of strategies derived from price action-related concepts for a data-driven approach to discretionary trading strategies.

Thanks to our 'Step' and 'Match' algorithm, users can create custom and complex strategy entries and exits from features such as market structure, order blocks, imbalances, as well as any external indicators, allowing users to create entries from a sequence of conditions and/or multiple matching conditions.

We included a complete alert system that will send a notification for each action taken by the strategy and we also allow users to set custom messages for each action taken by a strategy.

🔶 Features

🔹 Step & Match Algorithm

More complex entry rules can be created by using multiple conditions together, this is done thanks to the Step dropdown setting on the right of each condition.

The Step setting is directly related to the Step & Match algorithm and works in two ways:

When two or more conditions have the same step number, both conditions are evaluated. Used to test matching conditions.

When two or more conditions have different step numbers, each condition will be evaluated in order, testing for the first step and switching to the next step once the previous one is true. When the final step is true the strategy will open a market order. Used to create a sequence of conditions.

This operation is complementary, as you can create a sequence of conditions with one step consisting of two or more matching conditions as long as they have the same step number.

🔹 Fully Customizable Price Action Concepts As Entries

We allow the users to use market structures, order blocks, imbalances, and external sources together to set their custom entry and exit conditions.

Market structures are commonly used to determine trend direction by indicating when prices break prior swing points. Their occurrence can be used as entry conditions.

Order blocks highlight areas where institutional market participants open positions, one can use order blocks to determine confirmation entries or potential targets as we can expect there is a large amount of liquidity at these order blocks. Price entering, being within, or mitigating an order block can be used as an entry condition.

Market imbalances highlight areas where there is a disparity between supply and demand. Price entering, being within, or mitigating an imbalance can be used as an entry condition.

This system also allows the use of external sources to create entry and exit conditions, such as moving averages, bands, trailing stops...etc.

🔹 Complete Alert System

Users can get alerted for any action executed by a strategy, from opening positions to closing them.

The message field in the Alert Messages setting section allows for the strategy to send a custom alert message depending on the action taken by the strategy, if no messages are set the strategy will send default messages.

🔶 Usage

Users can create complete price action strategies from this script, let's see an example using the following entry conditions:

Long: Mitigated bearish order block occurring during the New York session after a mitigated bearish imbalance.

Short: Mitigated bullish order block occurring during the New York session after a mitigated bullish imbalance.

Take Profit: 2 points away from the entry price.

Stop Loss: 1 point away from the entry price.

We can also use features from Price Action Concepts™ to construct custom exit conditions, leading to the following strategy conditions:

Long: Bullish CHoCH and price mitigates bearish FVG.

Short: Bearish CHoCH and price mitigates bullish FVG.

Exit Long: Price mitigates bearish order block.

Exit Short: Price mitigates bullish order block.

Users can achieve a wide variety of results by using external indicators as an input source for entries and exits, combining the best from price action and technical indicators. We might for example be interested in exiting a position when the RSI oscillator is overbought or oversold.

🔶 Strategy Properties (Important)

This script backtest is done on daily EURGBP, using the following backtesting properties:

Balance (default): 10 000 (default base currency)

Order Size: 10% of the equity

Comission: 3.4 pips (average spread for EURGBP)

Slippage: 1 tick

Stop Loss: 0.01 points away from entry price

We use these properties to ensure a realistic preview of the backtesting system, do note that default properties can be different for various reasons described below:

Order Size: 1 contract by default, this is to allow the strategy to run properly on most instruments such as futures.

Comission: Comission can vary depending on the market and instrument, there is no default value that might return realistic results.

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from strategies built are realistic.

🔶 How to access

You can see the Author's Instructions below to learn how to get access.

LuxAlgo - Backtester (S&O)The S&O Backtester is an innovative strategy script that encompasses features + optimization methods from our Signals & Overlays™ toolkit and combines them into one easy-to-use script for backtesting the most detailed trading strategies possible.

Our Signals & Overlays™ toolkit is notorious for its signal optimization methods such as the 'Optimal Sensitivity' displayed in its dashboard which provides optimization backtesting of the Sensitivity parameter for the Confirmation & Contrarian Signals.

This strategy script allows even more detailed & precise backtests than anything available previously in the Signals & Overlays™ toolkit; including External Source inputs allowing users to use any indicator including our other paid toolkits for take profit & stop loss customization to develop strategies, along with 10+ pre-built filters directly Signals & Overlays™' features.

🔶 Features

Full Sensitivity optimization within the dashboard to find the Best Win rates or Best Profits.

Counter Trade Mode to reverse signals in undesirable market conditions (may introduce higher drawdowns)

Built-in filters for Confirmation Signals w/ Indicator Overlays from Signals & Overlays™.

Built-in Confirmation exit points are available within the settings & on by default.

External Source Input to filter signals or set custom Take Profits & Stop Losses.

Optimization Matrix dashboard option showing all possible permutations of Sensitivity.

Option to Maximize for Winrate or Best Profit.

🔶 Settings

Sensitivity signal optimizations for the Confirmation Signals algorithm

Buy & Sell conditions filters with Indicator Overlays & External Source

Take Profit exit signals option

External Source for Take Profit & Stop Loss

Sensitivity ranges

Backtest window default at 2,000 bars

External source

Dashboard locations

🔶 Usage

Backtests are not necessarily indicative of future results, although a trader may want to use a strategy script to have a deeper understanding of how their strategy responds to varying market conditions, or to use as a tool for identifying possible flaws in a strategy that could potentially be indicative of good or bad performance in the future.

A strategy script can also be useful in terms of it's ability to generate more complete & configurable alerts, giving users the option to integrate with external processes.

In the chart below we are using default settings and built-in optimization parameters to generate the highest win rate.

Results like the above will vary & finding a strategy with a high win rate does not necessarily mean it will persist into the future, however, some indications of a well-optimized strategy are:

A high number of closed trades (100+) with a consistently green equity curve

An equity curve that outperforms buy & hold

A low % max drawdown compared to the Net Profit %.

Profit factor around 1.5 or above

In the chart below we are using the Trend Catcher feature from Signals & Overlays™ as a filter for standard Confirmation Signals + exits on a higher timeframe.

By filtering bullish signals only when the Trend Catcher is bullish, as well as bearish signals for when the Trend Catcher is bearish, we have a highly profitable strategy created directly from our flagship features.

While the Signals & Overlays features being used as built-in filters can generate interesting backtests, the provided External Sources can allow for even more creativity when creating strategies. This feature allows you to use many indicators from TradingView as filters or to trigger take-profit/stop-loss events, even if they aren't from LuxAlgo.

The chart below shows the HyperWave Oscillator from our Oscillator Matrix™ being used for take-profit exit conditions, exiting a long position on a profit when crossing 80, and exiting a short position when crossing 20.

🔶 Counter Trade Mode

Our thesis has always firmly remained to use Confirmation Signals within Signals & Overlays™ as a supportive tool to find trends & use as extra confirmation within strategies.

We included the counter-trade mode as a logical way to use the Confirmation signals as direct entries for longs & shorts within more contrarian trading strategies. Many traders can relate to using a trend-following indicator and having the market not respect its conditions for entries.

This mode directly benefits a trader who is aware that market conditions are generally not-so-perfect trends all the time. Acknowledging this, allows the user to use this to their advantage by introducing countertrend following conditions as direct entries, which tend to perform very well in ranging markets.

The big downfall of using counter-trade mode is the potential for very large max-drawdowns during trending market conditions. We suggest for making a strategy to consider introducing stop-loss conditions that can efficiently minimize max-drawdowns during the process of backtesting your creations.

Sensitivity Optimization

Within the Signals & Overlays™ toolkit, we allow users to adjust the Confirmation Signals with a Sensitivity parameter.

We believe the Sensitivity paramter is the most realistic way to generate the most actionable Confirmation Signals that can navigate various market conditions, and the Confirmation Signals algorithm was designed specifically with this in mind.

This script takes this parameter and backtests it internally to generate the most profitable value to display on the dashboard located in the top right of the chart, as well as an optimization table if users enable it to visualize it's backtesting.

In the image below, we can see the optimization table showing permutations of settings within the user-selected Sensitivity range.

The suggested best setting is given at the current time for the backtesting window that's customizable within the indicator. Optimized settings for technical indicators are not indicative of future results and the best settings are highly likely / guaranteed to change over time.

Optimizing signal settings has become a popular activity amongst technical analysts, however, the real-time beneficial applications of optimizing settings are limited & best described as complicated (even with forward testing).

🔶 Strategy Properties (Important)

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from strategies built are realistic.

🔶 How to access

You can see the Author's Instructions below to learn how to get access on our website.