Prame Weekly RSI and EMA Strategy Prame Weekly RSI and EMA Strategy

weekly RSI 14 is above 55

EMA 9 weeks of weekly RSI 14 is more than EMA 21 weeks of weekly RSI 14

price EMA 9 weeks is more than price EMA 21 weeks

Bands and Channels

Minkiu Bollinger Band Strategy Convert all Indicator specific code to Strategy specific code. Don't use any code that a TradingView Strategy won't support. Especially timeframes and gaps. Define those in code so they are semantically the same as before.

High Frequency Trend Following - Single Trade ActiveHigh Frequency Trend Following - Single Trade Active Strategy

Overview

This TradingView strategy script is designed for high-frequency trading on shorter timeframes, leveraging exponential moving averages (EMAs) and the Relative Strength Index (RSI) to identify potential trade entries and exits. It ensures only one active trade at a time by closing the current position when an opposing signal is detected. This clean, visually appealing strategy is suited for day traders looking to follow short-term trends with minimal chart clutter.

How It Works

The strategy combines three main indicators:

EMA Cross: The script uses two EMAs (20-period and 50-period) to capture trend direction. A cross of the shorter EMA (20) above the longer EMA (50) indicates a bullish trend, while a cross below signals a bearish trend.

RSI Confirmation: RSI levels are used to confirm entries, filtering out trades in overbought or oversold conditions. For long entries, the RSI must be below 40, indicating a potential reversal from oversold conditions. For short entries, the RSI must be above 60, signaling a potential reversal from overbought conditions.

ATR-Based Exits: This script incorporates the Average True Range (ATR) to dynamically adjust stop loss and take profit levels based on market volatility, although exits in this version are based on opposite signals.

Best Use

This strategy is best suited for fast-moving markets and shorter timeframes, such as 5- or 15-minute charts, where it can capture frequent trend reversals. It can be applied to cryptocurrencies, forex, and other high-volatility assets.

Set Timeframe: This strategy performs best on intraday timeframes (e.g., 5-minute or 15-minute) where trend reversals are frequent.

Pair with High Volatility Assets: Ideal for assets like cryptocurrency pairs or forex where short-term trends and reversals are common.

Variables and Parameters

EMA Periods:

ema_short_length: The length of the short-term EMA (default is 20). This captures the faster-moving trend.

ema_long_length: The length of the long-term EMA (default is 50), representing the slower trend.

RSI Settings:

rsi_length: The period for the RSI (default is 14).

rsi_overbought: RSI level above which the market is considered overbought (default is 60).

rsi_oversold: RSI level below which the market is considered oversold (default is 40).

ATR Settings:

atr_length: Period for calculating ATR (default is 14).

atr_multiplier: Multiplier to adjust stop loss distance relative to ATR (default is 1.1).

take_profit_multiplier: Multiplier to adjust take profit distance relative to ATR (default is 1.5).

Interpretation

Entry Signals:

Long Entry: When the 20 EMA crosses above the 50 EMA (indicating an uptrend) and the RSI is below the rsi_oversold threshold (default 40), the script opens a long position.

Short Entry: When the 20 EMA crosses below the 50 EMA (indicating a downtrend) and the RSI is above the rsi_overbought threshold (default 60), the script opens a short position.

Exit Signals:

The strategy closes a long position when a short entry signal is generated, and vice versa. This ensures only one active trade at a time.

Visuals:

EMA Lines: The 20 EMA is green, and the 50 EMA is red. Crosses between these lines indicate potential trend shifts.

Background Colors: The background color changes faintly to green when a long position is active and to red when a short position is active, providing a clear visual representation of the current trade direction.

Entry and Exit Arrows: Small green arrows indicate long entries and exits from short positions, while red arrows mark short entries and exits from long positions.

Additional Notes

Customizability: Users can adjust the EMA and RSI parameters to suit their specific asset or timeframe. For example, decreasing the EMA lengths (e.g., 10 and 30) can make the strategy more sensitive to short-term trends.

Trading Environment: This strategy is ideal for high-volatility environments, where price reversals are common and where high-frequency trading can capture small but frequent gains.

Disclaimer

This strategy is intended for educational purposes and should be backtested and adjusted according to the specific asset and market conditions. Always use risk management and trade responsibly.

Enhanced 1-Hour Strategy for Maximized ReturnsEnhanced 1-Hour Strategy for Maximized Returns

Overview

This is a trend-following and volatility-based breakout strategy designed for trading on the one-hour timeframe. It combines moving average crossovers, RSI for momentum, and Bollinger Bands as a volatility filter to confirm entries and exits. With a focus on maximizing returns, this strategy is tuned to work with leveraged trading and dynamically allocates position sizes based on available equity.

How the Strategy Works

Trend Detection: The strategy uses two moving averages—a short-term and a long-term—to detect trends.

A crossover of the short moving average above the long moving average indicates a potential upward trend.

Conversely, a crossover of the short moving average below the long moving average suggests a downward trend.

Momentum Confirmation with RSI: To avoid entering trades in low-momentum conditions, the strategy employs the Relative Strength Index (RSI).

A long (buy) trade is considered only when RSI is above a set threshold, indicating upward momentum.

A short (sell) trade is considered only when RSI is below a set threshold, indicating downward momentum.

Volatility Filter with Bollinger Bands: Bollinger Bands act as a filter to ensure the strategy enters trades only during periods of higher volatility.

For a long trade, the price must be above the lower Bollinger Band.

For a short trade, the price must be below the upper Bollinger Band.

ATR-Based Stop-Loss and Take-Profit: The strategy uses the Average True Range (ATR) to set stop-loss and take-profit levels dynamically based on market volatility.

The stop-loss level is set at a certain multiplier of the ATR below (for long trades) or above (for short trades) the entry price.

The take-profit level is set at a larger ATR multiplier, allowing the strategy to capture larger movements.

Position Sizing with Leverage: The position size is calculated as a percentage of equity, leveraging it to maximize returns as the account balance grows.

Key Variables and Adjustable Parameters

Here are the adjustable inputs in the strategy, allowing traders to tailor it to their preferences:

Moving Averages:

Short MA Length (shortMaLength): Length of the short-term moving average (default: 14).

Long MA Length (longMaLength): Length of the long-term moving average (default: 50).

These lengths can be adjusted to make the moving average crossovers more or less sensitive.

RSI Settings:

RSI Length (rsiLength): Length of the RSI calculation (default: 14).

RSI Upper Threshold (rsiUpperThreshold): Minimum RSI value required for long trades (default: 60).

RSI Lower Threshold (rsiLowerThreshold): Maximum RSI value allowed for short trades (default: 40).

Adjusting these thresholds can help control the momentum conditions required for trades.

ATR Multipliers for Stop-Loss and Take-Profit:

ATR Stop-Loss Multiplier (atrMultiplierStopLoss): Multiplier for the ATR to set the stop-loss level (default: 1.5).

ATR Take-Profit Multiplier (atrMultiplierTakeProfit): Multiplier for the ATR to set the take-profit level (default: 3.0).

Tuning these multipliers can help in balancing risk and reward, depending on market volatility.

Bollinger Bands Settings:

Deviation (dev): The standard deviation multiplier for Bollinger Bands (default: 2).

Bollinger Bands provide a volatility filter, and this multiplier affects the width of the bands.

Position Sizing and Leverage:

Leverage (leverage): The leverage applied to the position (default: 10).

Allocation Percent (allocationPercent): The percentage of equity allocated to each trade (default: 0.1 or 10%).

Adjusting these settings can increase or decrease the position size relative to your equity, helping control risk exposure.

VWAP Stdev Bands Strategy (Long Only)The VWAP Stdev Bands Strategy (Long Only) is designed to identify potential long entry points in trending markets by utilizing the Volume Weighted Average Price (VWAP) and standard deviation bands. This strategy focuses on capturing upward price movements, leveraging statistical measures to determine optimal buy conditions.

Key Features:

VWAP Calculation: The strategy calculates the VWAP, which represents the average price a security has traded at throughout the day, weighted by volume. This is an essential indicator for determining the overall market trend.

Standard Deviation Bands: Two bands are created above and below the VWAP, calculated using specified standard deviations. These bands act as dynamic support and resistance levels, providing insight into price volatility and potential reversal points.

Trading Logic:

Long Entry Condition: A long position is triggered when the price crosses below the lower standard deviation band and then closes above it, signaling a potential price reversal to the upside.

Profit Target: The strategy allows users to set a predefined profit target, closing the long position once the specified target is reached.

Time Gap Between Orders: A customizable time gap can be specified to prevent multiple orders from being placed in quick succession, allowing for a more controlled trading approach.

Visualization: The VWAP and standard deviation bands are plotted on the chart with distinct colors, enabling traders to visually assess market conditions. The strategy also provides optional plotting of the previous day's VWAP for added context.

Use Cases:

Ideal for traders looking to engage in long-only positions within trending markets.

Suitable for intraday trading strategies or longer-term approaches based on market volatility.

Customization Options:

Users can adjust the standard deviation values, profit target, and time gap to tailor the strategy to their specific trading style and market conditions.

Note: As with any trading strategy, it is important to conduct thorough backtesting and analysis before live trading. Market conditions can change, and past performance does not guarantee future results.

PTS - Bollinger Bands with Trailing StopPTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

Thought for 1m 7s

Description for the "PTS - Bollinger Bands with Trailing Stop" Strategy

PTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

How the Strategy Works

1. Initialization

Calculates Bollinger Bands and ATR based on selected parameters.

2. Entry Logic

Opens a long position when the closing price exceeds the upper Bollinger Band.

3. Exit Logic

Uses a trailing stop loss based on ATR. Exits if the closing price drops below the lower Bollinger Band.

4. Date Filtering

Executes trades only within the specified date range.

Advantages

Adaptive Risk Management: Trailing stop adjusts to market volatility. Simplicity: Clear entry and exit signals. Customizable Parameters: Tailor the strategy to different assets or conditions.

Considerations

Aggressive Position Sizing: Using 100% equity per trade is high-risk. Market Conditions: Best in trending markets; may produce false signals in sideways markets. Backtesting: Always test on historical data before live trading.

Disclaimer

This strategy is intended for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Assess your financial situation and consult a financial advisor if necessary.

Usage Instructions

1. Apply the Strategy: Add it to your TradingView chart. 2. Configure Inputs: Adjust parameters to suit your style and asset. 3. Analyze Backtest Results: Use the Strategy Tester. 4. Optimize Parameters: Experiment with input values. 5. Risk Management: Evaluate position sizing and incorporate risk controls.

Final Notes

The "PTS - Bollinger Bands with Trailing Stop" strategy provides a framework to leverage momentum breakouts while managing risk through adaptive trailing stops. Customize and test thoroughly to align with your trading objectives.

Harmony Signal Flow By ArunThis Pine Script strategy, titled "Harmony Signal Flow By Arun," uses the Relative Strength Index (RSI) indicator to generate buy and sell signals based on custom thresholds. The script incorporates stop-loss and target management and restricts new trades until the previous position closes. Here's a detailed description:

Custom RSI Metric:

The strategy calculates a 5-period RSI based on the closing price, aiming for a more responsive measure of price momentum.

RSI thresholds are defined:

Lower threshold (30): Indicates oversold conditions, triggering a potential buy.

Upper threshold (70): Indicates overbought conditions, prompting a possible sell.

Entry Conditions:

Buy Signal: The strategy initiates a buy order when the RSI crosses above the lower threshold (30), indicating a shift from oversold conditions.

Sell Signal: A sell order is triggered when the RSI crosses below the upper threshold (70), suggesting an overbought reversal.

Only one order (buy or sell) can be active at a time, ensuring that a new trade begins only when there’s no existing position.

Stop-Loss and Target Management:

For each trade, stop-loss and target conditions are applied to manage risk and secure profits.

For Buy Positions:

Stop-loss is set 100 points below the entry price.

Target is set 150 points above the entry price.

For Sell Positions:

Stop-loss is set 100 points above the entry price.

Target is 150 points below the entry price.

The strategy closes the trade when either the stop-loss or target is met, marking the trade as "closed" and allowing a new trade entry.

Trade Sequencing:

A new trade (buy or sell) is only permitted after the previous position hits either its stop-loss or target, preventing overlapping trades and ensuring clear trade sequences.

This sequential approach enhances risk management by ensuring only one active position at any time.

End-of-Day Closure:

All open positions are closed automatically at 3:25 PM (Indian market time) to avoid overnight exposure, ensuring the strategy remains strictly intraday.

The flag for trade entry is reset at the end of each day, enabling fresh trades the next day.

Chart Indicators:

The script plots buy and sell signals directly on the chart with visible labels.

It also displays the custom RSI metric with horizontal lines for the lower and upper thresholds, providing visual cues for entry and exit points.

Summary

This strategy is a momentum-based intraday trading approach that uses the RSI for identifying potential reversals and manages trades through predefined stop-loss and target levels. By enforcing trade sequencing and closing positions at the end of the trading day, it prioritizes risk management and seeks to capitalize on short-term trends while avoiding overnight market risks.

[ETH] Optimized Trend Strategy - Lorenzo SuperScalpStrategy Title: Optimized Trend Strategy - Lorenzo SuperScalp

Description:

The Optimized Trend Strategy is a comprehensive trading system tailored for Ethereum (ETH) and optimized for the 15-minute timeframe but adaptable to various timeframes. This strategy utilizes a combination of technical indicators—RSI, Bollinger Bands, and MACD—to identify and act on price trends efficiently, providing traders with actionable buy and sell signals based on market conditions.

Key Features:

Multi-Indicator Approach:

RSI (Relative Strength Index): Identifies overbought and oversold conditions to time market entries and exits.

Bollinger Bands: Acts as a dynamic support and resistance level, helping to pinpoint precise entry and exit zones.

MACD (Moving Average Convergence Divergence): Detects momentum changes through bullish and bearish crossovers.

Signal Conditions:

Buy Signal:

RSI is below 45 (indicating an oversold condition).

Price is near or below the lower Bollinger Band.

MACD bullish crossover occurs.

Sell Signal:

RSI is above 55 (indicating an overbought condition).

Price is near or above the upper Bollinger Band.

MACD bearish crossunder occurs.

Trade Execution Logic:

Long Trades: Opened when a buy signal flashes. If there’s an open short position, it is closed before opening a long.

Short Trades: Opened when a sell signal flashes. If there’s an open long position, it is closed before opening a short.

The strategy also ensures a minimum number of bars between consecutive trades to avoid rapid trading in choppy conditions.

Pyramiding Support:

Up to 3 consecutive trades in the same direction are allowed, enabling traders to scale into positions based on strong signals.

Visual Indicators:

RSI Levels: Dotted lines at 45 and 55 for quick reference to oversold and overbought levels.

Buy and Sell Signals: Visual markers on the chart indicate where trades are executed, ensuring clarity on entry and exit points.

Best Used For:

Swing Trading & Scalping: While optimized for the 15-minute timeframe, this strategy works across various timeframes, making it suitable for both short-term scalping and swing trading.

Crypto Trading: Tailored for Ethereum but effective for other cryptocurrencies due to its dynamic indicator setup.

Keltner Channel Strategy by Kevin DaveyKeltner Channel Strategy Description

The Keltner Channel Strategy is a volatility-based trading approach that uses the Keltner Channel, a technical indicator derived from the Exponential Moving Average (EMA) and Average True Range (ATR). The strategy helps identify potential breakout or mean-reversion opportunities in the market by plotting upper and lower bands around a central EMA, with the channel width determined by a multiplier of the ATR.

Components:

1. Exponential Moving Average (EMA):

The EMA smooths price data by placing greater weight on recent prices, allowing traders to track the market’s underlying trend more effectively than a simple moving average (SMA). In this strategy, a 20-period EMA is used as the midline of the Keltner Channel.

2. Average True Range (ATR):

The ATR measures market volatility over a 14-period lookback. By calculating the average of the true ranges (the greatest of the current high minus the current low, the absolute value of the current high minus the previous close, or the absolute value of the current low minus the previous close), the ATR captures how much an asset typically moves over a given period.

3. Keltner Channel:

The upper and lower boundaries are set by adding or subtracting 1.5 times the ATR from the EMA. These boundaries create a dynamic range that adjusts with market volatility.

Trading Logic:

• Long Entry Condition: The strategy enters a long position when the closing price falls below the lower Keltner Channel, indicating a potential buying opportunity at a support level.

• Short Entry Condition: The strategy enters a short position when the closing price exceeds the upper Keltner Channel, signaling a potential selling opportunity at a resistance level.

The strategy plots the upper and lower Keltner Channels and the EMA on the chart, providing a visual representation of support and resistance levels based on market volatility.

Scientific Support for Volatility-Based Strategies:

The use of volatility-based indicators like the Keltner Channel is supported by numerous studies on price momentum and volatility trading. Research has shown that breakout strategies, particularly those leveraging volatility bands such as the Keltner Channel or Bollinger Bands, can be effective in capturing trends and reversals in both trending and mean-reverting markets  .

Who is Kevin Davey?

Kevin Davey is a highly respected algorithmic trader, author, and educator, known for his systematic approach to building and optimizing trading strategies. With over 25 years of experience in the markets, Davey has earned a reputation as an expert in quantitative and rule-based trading. He is particularly well-known for winning several World Cup Trading Championships, where he consistently demonstrated high returns with low risk.

Bollinger Bands Mean Reversion by Kevin Davey Bollinger Bands Mean Reversion Strategy Description

The Bollinger Bands Mean Reversion Strategy is a popular trading approach based on the concept of volatility and market overreaction. The strategy leverages Bollinger Bands, which consist of an upper and lower band plotted around a central moving average, typically using standard deviations to measure volatility. When the price moves beyond these bands, it signals potential overbought or oversold conditions, and the strategy seeks to exploit a reversion back to the mean (the central band).

Strategy Components:

1. Bollinger Bands:

The bands are calculated using a 20-period Simple Moving Average (SMA) and a multiple (usually 2.0) of the standard deviation of the asset’s price over the same period. The upper band represents the SMA plus two standard deviations, while the lower band is the SMA minus two standard deviations. The distance between the bands increases with higher volatility and decreases with lower volatility.

2. Mean Reversion:

Mean reversion theory suggests that, over time, prices tend to move back toward their historical average. In this strategy, a buy signal is triggered when the price falls below the lower Bollinger Band, indicating a potential oversold condition. Conversely, the position is closed when the price rises back above the upper Bollinger Band, signaling an overbought condition.

Entry and Exit Logic:

Buy Condition: The strategy enters a long position when the price closes below the lower Bollinger Band, anticipating a mean reversion to the central band (SMA).

Sell Condition: The long position is exited when the price closes above the upper Bollinger Band, implying that the market is likely overbought and a reversal could occur.

This approach uses mean reversion principles, aiming to capitalize on short-term price extremes and volatility compression, often seen in sideways or non-trending markets. Scientific studies have shown that mean reversion strategies, particularly those based on volatility indicators like Bollinger Bands, can be effective in capturing small but frequent price reversals  .

Scientific Basis for Bollinger Bands:

Bollinger Bands, developed by John Bollinger, are widely regarded in both academic literature and practical trading as an essential tool for volatility analysis and mean reversion strategies. Research has shown that Bollinger Bands effectively identify relative price highs and lows, and can be used to forecast price volatility and detect potential breakouts . Studies in financial markets, such as those by Fernández-Rodríguez et al. (2003), highlight the efficacy of Bollinger Bands in detecting overbought or oversold conditions in various assets .

Who is Kevin Davey?

Kevin Davey is an award-winning algorithmic trader and highly regarded expert in developing and optimizing systematic trading strategies. With over 25 years of experience, Davey gained significant recognition after winning the prestigious World Cup Trading Championships multiple times, where he achieved triple-digit returns with minimal drawdown. His success has made him a key figure in algorithmic trading education, with a focus on disciplined and rule-based trading systems.

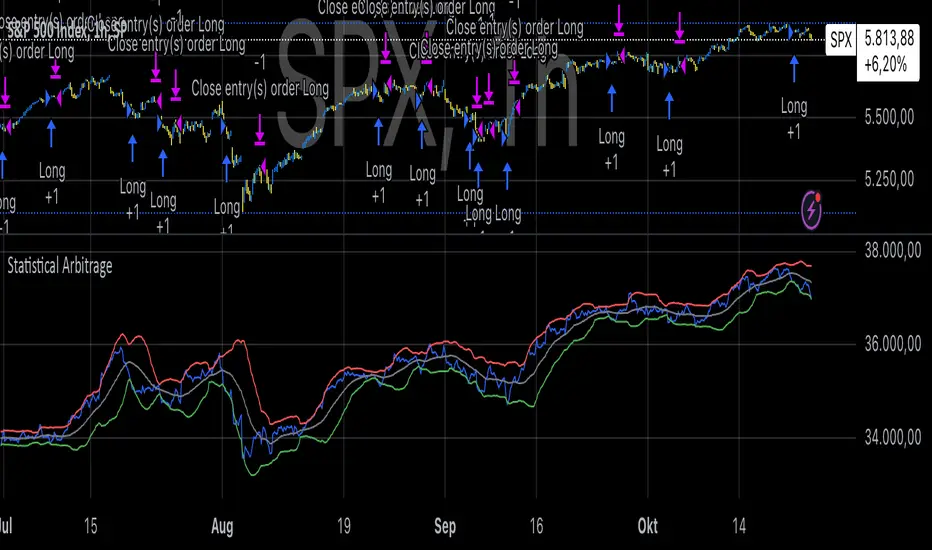

Statistical ArbitrageThe Statistical Arbitrage Strategy, also known as pairs trading, is a quantitative trading method that capitalizes on price discrepancies between two correlated assets. The strategy assumes that over time, the prices of these two assets will revert to their historical relationship. The core idea is to take advantage of mean reversion, a principle suggesting that asset prices will revert to their long-term average after deviating significantly.

Strategy Mechanics:

1. Selection of Correlated Assets:

• The strategy focuses on two historically correlated assets (e.g., equity index futures like Dow Jones Mini and S&P 500 Mini). These assets tend to move in the same direction due to similar underlying fundamentals, such as overall market conditions. By tracking their relative prices, the strategy seeks to exploit temporary mispricings.

2. Spread Calculation:

• The spread is the difference between the prices of the two assets. This spread represents the relationship between the assets and serves as the basis for determining when to enter or exit trades.

3. Mean and Standard Deviation:

• The historical average (mean) of the spread is calculated using a Simple Moving Average (SMA) over a chosen period. The strategy also computes the standard deviation (volatility) of the spread, which measures how far the spread has deviated from the mean over time. This allows the strategy to define statistically significant price deviations.

4. Entry Signal (Mean Reversion):

• A buy signal is triggered when the spread falls below the mean by a multiple (e.g., two) of the standard deviation. This indicates that one asset is temporarily undervalued relative to the other, and the strategy expects the spread to revert to its mean, generating profits as the prices converge.

5. Exit Signal:

• The strategy exits the trade when the spread reverts to the mean. At this point, the mispricing has been corrected, and the profit from the mean reversion is realized.

Academic Support:

Statistical arbitrage has been widely studied in finance and economics. Gatev, Goetzmann, and Rouwenhorst’s (2006) landmark study on pairs trading demonstrated that this strategy could generate excess returns in equity markets. Their research found that by focusing on historically correlated stocks, traders could identify pricing anomalies and profit from their eventual correction.

Additionally, Avellaneda and Lee (2010) explored statistical arbitrage in different asset classes and found that exploiting deviations in price relationships can offer a robust, market-neutral trading strategy. In these studies, the strategy’s success hinges on the stability of the relationship between the assets and the timely execution of trades when deviations occur.

Risks of Statistical Arbitrage:

1. Correlation Breakdown:

• One of the primary risks is the breakdown of correlation between the two assets. Statistical arbitrage assumes that the historical relationship between the assets will hold in the future. However, market conditions, company fundamentals, or external shocks (e.g., macroeconomic changes) can cause these assets to deviate permanently, leading to potential losses.

• For instance, if two equity indices historically move together but experience divergent economic conditions or policy changes, their prices may no longer revert to the expected mean.

2. Execution Risk:

• This strategy relies on efficient execution and tight spreads. In volatile or illiquid markets, the actual price at which trades are executed may differ significantly from expected prices, leading to slippage and reduced profits.

3. Market Risk:

• Although statistical arbitrage is designed to be market-neutral (i.e., not dependent on the overall market direction), it is not entirely risk-free. Systematic market shocks, such as financial crises or sudden shifts in market sentiment, can affect both assets simultaneously, causing the spread to widen rather than revert to the mean.

4. Model Risk:

• The assumptions underlying the strategy, particularly regarding mean reversion, may not always hold true. The model assumes that asset prices will return to their historical averages within a certain timeframe, but the timing and magnitude of mean reversion can be uncertain. Misestimating this timeframe can lead to extended drawdowns or unrealized losses.

5. Overfitting:

• Over-reliance on historical data to fine-tune the strategy parameters (e.g., the lookback period or standard deviation thresholds) may result in overfitting. This means that the strategy works well on past data but fails to perform in live markets due to changing conditions.

Conclusion:

The Statistical Arbitrage Strategy offers a systematic and quantitative approach to trading that capitalizes on temporary price inefficiencies between correlated assets. It has been proven to generate returns in academic studies and is widely used by hedge funds and institutional traders for its market-neutral characteristics. However, traders must be aware of the inherent risks, including correlation breakdown, execution risks, and the potential for prolonged deviations from the mean. Effective risk management, diversification, and constant monitoring are essential for successfully implementing this strategy in live markets.

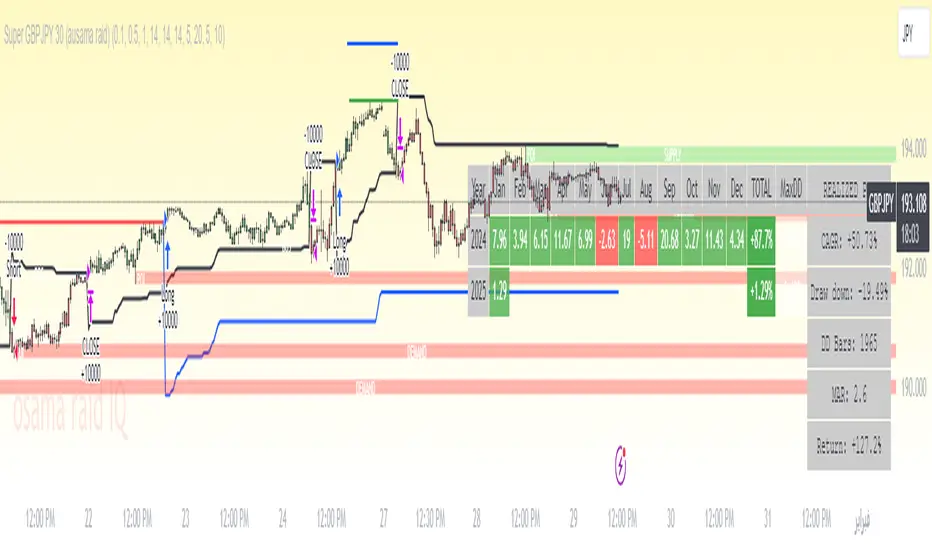

Super GBPJPY 30 (ausama raid)

### Strategy Description: Super GBPJPY 30 (ausama raid)

FX:GBPJPY

**Overview**:

The "Super GBPJPY 30" trading strategy utilizes SuperTrend indicators to identify overall trends and entry/exit signals specifically on the GBP/JPY currency pair, operating on a 30-minute timeframe. This strategy aims to enhance profit opportunities by leveraging financial leverage and advanced take-profit settings.

**Strategy Settings**:

1. **Leverage**: Users can specify an appropriate leverage (1 or higher).

2. **Enable Advanced Take Profit**: This allows users to activate or deactivate the advanced take profit level.

3. **Show Monthly Performance Table**: Displays the strategy's performance across previous months and years.

**Timeframe**:

- The strategy is designed for the **GBP/JPY currency pair** on the **30-minute timeframe**, providing a balance between timely entries and risk management.

**Entry and Exit Indicators**:

- **Overall Trend Indicator**: The overall trend is determined using the SuperTrend indicator, with specific settings for the ATR length and factor used.

- **Entry Indicator**: A second SuperTrend indicator is employed to signal entry and exit points, improving decision-making accuracy.

### How It Works:

1. **Buy Signals**: A buy order is placed when the overall trend is bullish, and the entry indicator gives a buy signal.

2. **Sell Signals**: A sell order is executed when the overall trend is bearish, and the entry indicator provides a sell signal.

3. **Trade Management**:

- Half of the position can be closed when a specific profit level is reached.

- The position will be exited if the entry indicator's trend changes.

### Chart Illustrations:

- **Indicator Lines**: The indicator lines are displayed on the chart, with trends indicated in blue (bullish) or red (bearish).

- **Candle Colors**: The candle colors change based on the entry indicator's signals, making it easier to visualize current trends.

### Performance:

- **Performance Table**: The current year's monthly performance is displayed, allowing users to view past results.

- **Profit Percentage**: The strategy offers good risk management by defining the profit percentage for each trade.

**Note**: Ensure to test the strategy on a demo account before applying it in the real market.

---

G-Channel with EMA StrategyThe G-Channel is a custom channel with an upper (a), lower (b), and average (avg) line. These lines are dynamically calculated based on the current and previous closing prices, using the length input (default 100) to smooth the values:

Upper Line (a): This is the maximum value of the current price or the previous upper value, adjusted by the difference between the upper and lower lines divided by the length.

Lower Line (b): This is the minimum value of the current price or the previous lower value, similarly adjusted by the difference between the upper and lower lines.

The average line (avg) is simply the midpoint between the upper and lower lines. The G-Channel signals trend direction:

Bullish Condition: The system looks for the condition when the price crosses over the lower line (b), indicating a potential upward trend.

Bearish Condition: When the price crosses under the upper line (a), it signals a potential downward trend.

Exponential Moving Average (EMA)

The strategy also incorporates an EMA with a default length of 200. The EMA serves as a trend filter to determine whether the market is trending upward or downward:

Price below EMA: Indicates a bearish trend.

Price above EMA: Indicates a bullish trend.

Buy/Sell Conditions

The strategy generates buy or sell signals based on the interaction between the G-Channel signals and the price relative to the EMA:

Buy Signal: The strategy triggers a buy when:

A bullish condition (recent crossover of price over the lower G-Channel line) is detected.

The price is below the EMA, indicating that despite the recent bullish signal, the market might still be undervalued or in a temporary downturn.

Sell Signal: The strategy triggers a sell when:

A bearish condition (recent crossunder of price below the upper G-Channel line) is detected.

The price is above the EMA, suggesting that the market might be overextended and poised for a downturn.

Visualization

The strategy plots:

The upper, lower, and average lines of the G-Channel, with the average line colored based on bullish (green) or bearish (red) conditions.

The EMA (orange) line to provide context on the general trend direction.

Markers for Buy and Sell signals to visually indicate the strategy's entry points.

Strategy Execution

When a buy or sell signal is detected:

Buy Entry: If the bullish condition and price < EMA condition are met, a long (buy) position is opened.

Sell Entry: If the bearish condition and price > EMA condition are met, a short (sell) position is opened.

Purpose

This strategy aims to catch price reversals at critical points (when the price moves through the G-Channel) while filtering trades using the EMA to avoid entering during unfavorable market trends.

Wolfpack Elite - Liquidation Sniper - by 9123416916### Strategy: **Wolfpack Elite - Liquidation Sniper by Md Arif**

**Overview:**

This is a technical analysis strategy designed for trading, which combines two popular technical indicators: **Relative Strength Index (RSI)** and **Moving Averages (MA)**. It identifies potential buy (long) and sell (short) signals based on oversold and overbought conditions in the market, along with crossovers between two moving averages. The strategy also incorporates a risk management system by setting **take profit** and **stop loss** levels to protect against large losses and lock in gains.

---

**Key Components:**

1. **Indicators Used:**

- **RSI (Relative Strength Index):**

- Measures the speed and change of price movements.

- Used to identify **overbought** (above 70) and **oversold** (below 30) conditions.

- **Short and Long Moving Averages:**

- The strategy uses two simple moving averages (SMA) to detect trends and potential entry points.

- Short MA (9-period) and Long MA (21-period) are used for crossovers.

2. **Entry Signals:**

- **Bullish Entry (Long Position):**

- Triggered when the RSI falls below the oversold level (30) and the **short MA** crosses above the **long MA** (bullish crossover).

- This suggests that the market might be oversold and ready to rebound.

- **Bearish Entry (Short Position):**

- Triggered when the RSI rises above the overbought level (70) and the **short MA** crosses below the **long MA** (bearish crossover).

- This suggests that the market might be overbought and due for a correction.

3. **Risk Management:**

- **Take Profit and Stop Loss:**

- The strategy calculates the take profit and stop loss levels as percentages of the entry price.

- **Take Profit:** Set at 5% above the entry price for long positions and 5% below the entry price for short positions.

- **Stop Loss:** Set at 3% below the entry price for long positions and 3% above the entry price for short positions.

4. **Position Sizing:**

- The position size is calculated as a percentage of the trader's total equity (default set to 100% of equity).

5. **Exit Conditions:**

- **For Long Positions:**

- Exit the trade if the price hits the take profit level (5% above entry) or the stop loss level (3% below entry).

- **For Short Positions:**

- Exit the trade if the price hits the take profit level (5% below entry) or the stop loss level (3% above entry).

6. **Visualization:**

- The strategy visually plots the short and long moving averages on the chart.

- It also marks **bullish crossovers** with green upward triangles and **bearish crossovers** with red downward triangles, making it easier to spot potential entry points.

---

**How the Strategy Works:**

- The strategy starts by calculating the **RSI** and **moving averages**.

- It waits for specific conditions to trigger buy or sell signals. If the RSI indicates that the market is oversold and a bullish crossover occurs, it initiates a **long trade**. Similarly, if the RSI shows an overbought condition and a bearish crossover occurs, it opens a **short trade**.

- Once a trade is open, the strategy monitors the price and automatically exits the trade if the price reaches the set take profit or stop loss level.

---

This strategy is designed for active traders who seek to capitalize on short-term price movements and want clear entry/exit points with built-in risk management.

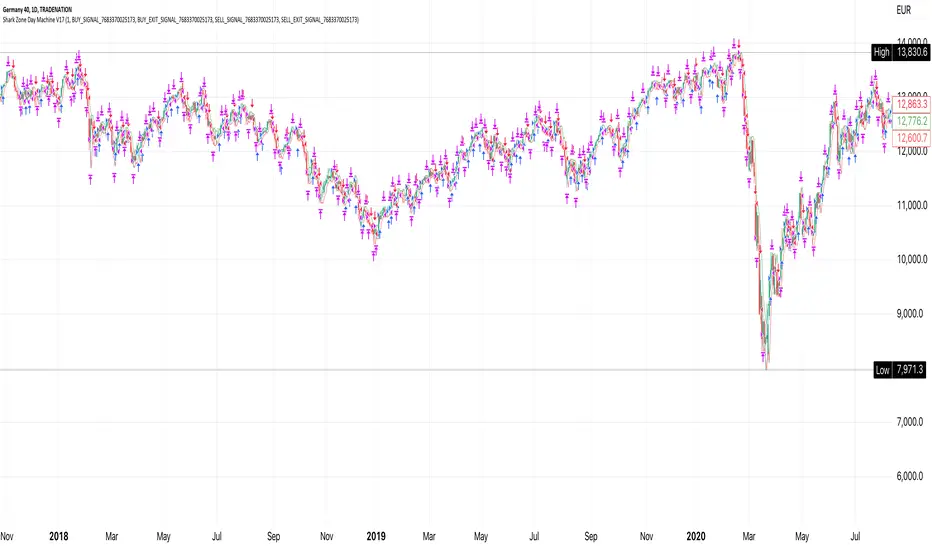

Shark Zone Day Machine V17### **Strategy Overview: Shark Zone Day Machine V14**

The "Shark Zone Day Machine V14" is a daily breakout trading strategy designed for traders who wish to capitalize on intraday price movements based on key levels from the previous day. The strategy operates on a daily timeframe, allowing traders to execute precise entries and manage their trades effectively. It includes both long and short trading capabilities, with user-friendly inputs for customization.

### **Key Features:**

1. **Daily Breakout Logic**:

- **Long Position**: The strategy opens a long position when the price breaks above the previous day's high, indicating potential upward momentum.

- **Short Position**: The strategy opens a short position when the price drops below the previous day's low, signaling possible downward pressure.

2. **Stop Loss Management**:

- The strategy uses a fixed stop loss of 50 points, which is set at the previous day's low for long trades and 50 points above the entry for short trades.

3. **Spread Adjustment**:

- Includes an adjustable spread input to account for bid-ask differences, ensuring entries and exits are accurately calculated.

4. **Activation Controls**:

- Traders can easily enable or disable long and short trading strategies independently using input toggles.

5. **Custom Alert Integration**:

- The strategy includes alert messages configured to work seamlessly with Pine Connector. These alerts can be set up to automatically send trade signals to MT4, enabling a fully automated trading experience.

### **Automated Trading Setup via Pine Connector to MT4**

To implement this strategy for automated trading between TradingView and MT4 using Pine Connector, follow these steps:

1. **Apply the Script on TradingView**:

- Load the "Shark Zone Day Machine V14" script onto your TradingView chart and adjust the input parameters as needed, including activation toggles, spread, and stop loss settings.

2. **Set Up Alerts on TradingView**:

- Click on the `Alerts` button in TradingView.

- Under "Condition," select the strategy and choose "Any alert() function call."

- For each alert, use the predefined messages:

- **Long Entry Alert**: `"BUY_SIGNAL_7683370025173"`

- **Long Exit Alert**: `"BUY_EXIT_SIGNAL_7683370025173"`

- **Short Entry Alert**: `"SELL_SIGNAL_7683370025173"`

- **Short Exit Alert**: `"SELL_EXIT_SIGNAL_7683370025173"`

- Ensure the alert actions are set to "Notify on app" and "Show pop-up" for immediate feedback.

3. **Configure Pine Connector**:

- Pine Connector should be installed and set up on your MT4 platform. Ensure the Pine Connector ID matches the alert messages from the TradingView script.

- Configure your MT4 EA to recognize these signals and execute trades accordingly. For example, a `"BUY_SIGNAL_7683370025173"` alert from TradingView will instruct MT4 to place a buy order.

4. **Test the Setup**:

- It’s essential to test the automation in a demo account first. Monitor how trades are opened and closed on MT4 when alerts are triggered from TradingView.

- Adjust the parameters on TradingView if needed for optimal performance and minimal slippage.

### **Benefits of Automated Trading with This Strategy**:

- **Consistency**: Eliminates the potential for human error by executing trades precisely as per the strategy’s logic.

- **Speed**: Rapid response to breakout conditions, ensuring you capture opportunities as soon as they arise.

- **Flexibility**: The ability to adjust stop loss, spread, and trading size allows for quick adaptation to different market conditions.

### **Important Notes**:

- Ensure your TradingView account remains active and has real-time data enabled for accurate alerts.

- Verify that Pine Connector and MT4 settings are configured correctly to prevent missed trades or incorrect lot sizes.

- Be mindful of market conditions, as breakout strategies may perform differently during high-volatility periods.

By following this guide, you'll be able to leverage the "Shark Zone Day Machine V14" strategy to its full potential, automating your trades and optimizing your trading efficiency.

Fibonacci & Bollinger Bands StrategyThis strategy combines Bollinger Bands and Fibonacci retracement/extension levels to identify potential entry and exit points in the market. Here’s a breakdown of each component and how the strategy works:

1. Bollinger Bands:

Bollinger Bands consist of a simple moving average (SMA) and two standard deviations (upper and lower bands) plotted above and below the SMA. The bands expand and contract based on market volatility.

Purpose in Strategy:

The lower band represents an area where the market might be oversold.

The upper band represents an area where the market might be overbought.

The price crossing these bands suggests overextended market conditions, which can be used to identify potential reversals.

2. Fibonacci Retracement and Extension Levels:

Fibonacci retracement levels are horizontal lines that indicate where price might find support or resistance as it retraces some of its previous movement. Common retracement levels are 61.8% and 78.6%.

Fibonacci extension levels are used to project areas where the price might extend after completing a retracement. These levels can help determine potential targets after a significant price movement.

Purpose in Strategy:

The strategy calculates the most recent swing high (fibHigh) and swing low (fibLow) over a lookback period. It then plots Fibonacci retracement and extension levels based on this range.

The Fibonacci levels are used as key support and resistance areas. The price approaching or touching these levels signals potential turning points in the market.

3. Entry Criteria:

A long position (buy) is triggered when:

The price crosses below the lower Bollinger Band, indicating an oversold condition.

The price is near or above a Fibonacci extension level (calculated based on the most recent price swing).

This suggests that the price is potentially reaching a strong support area, where a reversal is likely.

4. Exit Criteria:

The long position is closed (exit trade) when either:

The price touches or crosses the upper Bollinger Band, signaling an overbought condition.

The price reaches a Fibonacci retracement level or exceeds the recent swing high (fibHigh), indicating a potential exhaustion point or a reversal area.

5. General Strategy Logic:

The strategy takes advantage of market volatility (captured by the Bollinger Bands) and key support/resistance levels (determined by Fibonacci retracement and extension levels).

By combining these two techniques, the strategy identifies potential entry points at oversold levels with the expectation that the market will retrace or reverse upward, especially when near key Fibonacci extension levels.

Exit points are identified by potential overbought levels (Bollinger upper band) or key Fibonacci retracement levels, where the price might reverse downward.

6. Conditions to Execute the Strategy:

The Fibonacci levels are only calculated once the price has made a significant movement, establishing a recent high and low over a 50-bar period (which you can adjust). This ensures the Fibonacci levels are based on meaningful swings.

The entry and exit signals are filtered using both Bollinger Bands and Fibonacci levels to ensure that trades are not taken solely based on one indicator, thus reducing false signals.

Key Features of the Strategy:

Trend-following with reversal: It tries to catch reversals when the price hits extreme levels (Bollinger Bands) while respecting important Fibonacci levels.

Dynamic market adaptation: The strategy adapts to market conditions as it recalculates Fibonacci levels based on recent price swings and adjusts the Bollinger Bands for market volatility.

Confirmation through multiple indicators: It uses both the volatility-based signals from Bollinger Bands and the price structure from Fibonacci levels to confirm trade entries and exits.

Summary of the Strategy:

The strategy looks to buy low and sell high based on oversold/overbought signals from Bollinger Bands and Fibonacci levels that indicate key support and resistance zones.

By combining these two technical indicators, the strategy aims to reduce risk and increase accuracy by only entering trades when both indicators suggest favorable conditions.

Trade Entry Detector, Wick to Body Ratio Trade Entry Detector: Wick-to-Body Ratio Strategy with Bollinger Bands

Overview

The Trade Entry Detector is a custom strategy for TradingView that leverages the Bollinger Bands and a unique wick-to-body ratio approach to capture precise entry opportunities. This indicator is designed for traders who want to pinpoint high-probability reversal points when price interacts with Bollinger Bands, all while offering flexible entry fill options.

The strategy performs primary analysis on the daily time frame, regardless of your current chart setting, allowing you to view daily Bollinger Band levels and entry signals even on lower time frames. This approach is suitable for swing traders and short-term traders looking to align intraday moves with higher time frame signals.

How the Strategy Works

1. Bollinger Band Analysis on the Daily Time Frame

Bollinger Bands are calculated using a 20-period simple moving average (SMA) and a standard deviation multiplier (default is 2). These bands dynamically expand and contract based on market volatility, making them ideal for identifying overbought and oversold conditions:

* Upper Band: Indicates potential overbought levels.

* Lower Band: Indicates potential oversold levels.

2. Wick-to-Body Ratio Condition

This strategy places significant emphasis on candle wicks relative to the candle body. Here’s why:

* A large upper wick relative to the body signals potential selling pressure after testing the upper Bollinger Band.

* A large lower wick relative to the body indicates buying support after testing the lower Bollinger Band.

* Ratio Threshold: You can set a minimum wick-to-body ratio (default is 1.0), meaning that the wick must be at least equal in size to the body. This ensures only candles with significant reversals are considered for entry.

3. Flexible Entry Timing

To adapt to various trading styles, the indicator allows you to choose the entry fill timing:

* Daily Close: Enter at the close of the daily candle.

* Daily Open: Enter at the open of the following daily candle.

* HOD (High of Day): Set entry at the daily high, for those who want confirmation of upward momentum.

* LOD (Low of Day): Set entry at the daily low, ideal for confirming downward movement.

4. Position Sizing and Risk Management

The strategy calculates position size based on a fixed risk percentage of your account balance (default is 1%). This approach dynamically adjusts position sizes based on stop-loss distance:

* Stop Loss: Placed at the nearest swing high (for shorts) or swing low (for longs).

* Take Profit: Exits are triggered when the price reaches the opposite Bollinger Band.

5. Order Expiration

Each pending order (long or short) expires after two days if unfilled, allowing for new setups on subsequent candles if conditions are met again.

Using the Trade Entry Detector

Step-by-Step Guide

1. Set the Primary Time Frame

The core calculations run on the daily time frame, but the strategy can be applied to intraday charts (e.g., 65-minute or 15-minute) for deeper insights.

2. Adjust Bollinger Band Settings

* Length: Default is 20, which determines the period for calculating the moving average.

* Standard Deviation Multiplier: Default is 2.0, which sets the width of the bands. Adjusting this can help you capture broader or tighter volatility ranges.

3. Define the Wick-to-Body Ratio

Set the minimum ratio between wick and body (default 1.0). Higher values filter out candles with less wick-to-body contrast, focusing on stronger rejection moves.

4. Choose Entry Fill Timing

Select your preferred fill condition:

* Daily Close: Confirms the trade at the end of the daily session.

* Daily Open: Executes the entry at the open of the next day.

* HOD/LOD: Uses the daily high or low as an additional confirmation for upward or downward moves.

5. Position Sizing and Risk Management

* Set your account balance and risk percentage. The strategy automatically calculates position sizes based on the stop distance to manage risk efficiently.

* Stop Loss and Take Profit points are automatically set based on swing highs/lows and opposing Bollinger Bands, respectively.

Practical Example

Let’s say SPY (S&P 500 ETF) tests the lower Bollinger Band on the daily time frame, with a lower wick that is twice the size of the body (meeting the 1.0 ratio threshold). Here’s how the strategy might proceed:

1. Signal: The lower wick on SPY suggests buying interest at the lower Bollinger Band.

2. Entry Fill Timing: If you’ve selected "Daily Open," the entry order will be placed at the next day's open price.

3. Stop Loss: Positioned at the nearest daily swing low to minimize risk.

4. Take Profit: If SPY price moves up and reaches the upper Bollinger Band, the position is automatically closed.

Indicator Features and Benefits

* Multi-Time Frame Compatibility: Perform daily analysis while tracking signals on any intraday chart.

* Automatic Position Sizing: Tailor risk per trade based on account balance and desired risk percentage.

* Flexible Entry Options: Choose from close, open, HOD, or LOD for optimal timing.

* Effective Trend Reversal Identification: Uses wick-to-body ratio and Bollinger Band interaction to pinpoint potential reversals.

* Dynamic Visualization: Bollinger Bands are displayed on your chosen time frame, allowing seamless intraday tracking.

Summary

The Trade Entry Detector provides a unique, data-driven way to spot reversal points with customizable entry options. By combining Bollinger Bands with wick-to-body ratio conditions, it identifies potential trade setups where price has tested extremes and shown reversal signals. With its flexible entry timing, risk management features, and multi-time frame compatibility, this indicator is ideal for traders looking to blend daily market context with shorter-term execution.

Tips for Usage:

* For swing trading, consider the Daily Open or Close entry options.

* For momentum entries, HOD or LOD may offer better alignment with the direction of the wick.

* Backtest on different assets to find optimal Bollinger Band and wick-to-body settings for your market.

Use this indicator to enhance your understanding of price behavior at key levels and improve the precision of your entry points. Happy trading!

KAMA Cloud STIndicator:

Description:

The KAMA Cloud indicator is a sophisticated trading tool designed to provide traders with insights into market trends and their intensity. This indicator is built on the Kaufman Adaptive Moving Average (KAMA), which dynamically adjusts its sensitivity to filter out market noise and respond to significant price movements. The KAMA Cloud leverages multiple KAMAs to gauge trend direction and strength, offering a visual representation that is easy to interpret.

How It Works:

The KAMA Cloud uses twenty different KAMA calculations, each set to a distinct lookback period ranging from 5 to 100. These KAMAs are calculated using the average of the open, high, low, and close prices (OHLC4), ensuring a balanced view of price action. The relative positioning of these KAMAs helps determine the direction of the market trend and its momentum.

By measuring the cumulative relative distance between these KAMAs, the indicator effectively assesses the overall trend strength, akin to how the Average True Range (ATR) measures market volatility. This cumulative measure helps in identifying the trend’s robustness and potential sustainability.

The visualization component of the KAMA Cloud is particularly insightful. It plots a 'cloud' formed between the base KAMA (set at a 100-period lookback) and an adjusted KAMA that incorporates the cumulative relative distance scaled up. This cloud changes color based on the trend direction — green for upward trends and red for downward trends, providing a clear, visual representation of market conditions.

How the Strategy Works:

The KAMA Cloud ST strategy employs multiple KAMA calculations with varying lengths to capture the nuances of market trends. It measures the relative distances between these KAMAs to determine the trend's direction and strength, much like the original indicator. The strategy enhances decision-making by plotting a 'cloud' formed between the base KAMA (set to a 100-period lookback) and an adjusted KAMA that scales according to the cumulative relative distance of all KAMAs.

Key Components of the Strategy:

Multiple KAMA Layers: The strategy calculates KAMAs for periods ranging from 5 to 100 to analyze short to long-term market trends.

Dynamic Cloud: The cloud visually represents the trend’s strength and direction, updating in real-time as the market evolves.

Signal Generation: Trade signals are generated based on the orientation of the cloud relative to a smoothed version of the upper KAMA boundary. Long positions are initiated when the market trend is upward, and the current cloud value is above its smoothed average. Conversely, positions are closed when the trend reverses, indicated by the cloud falling below the smoothed average.

Suggested Usage:

Market: Stocks, not cryptocurrency

Timeframe: 1 Hour

Indicator:

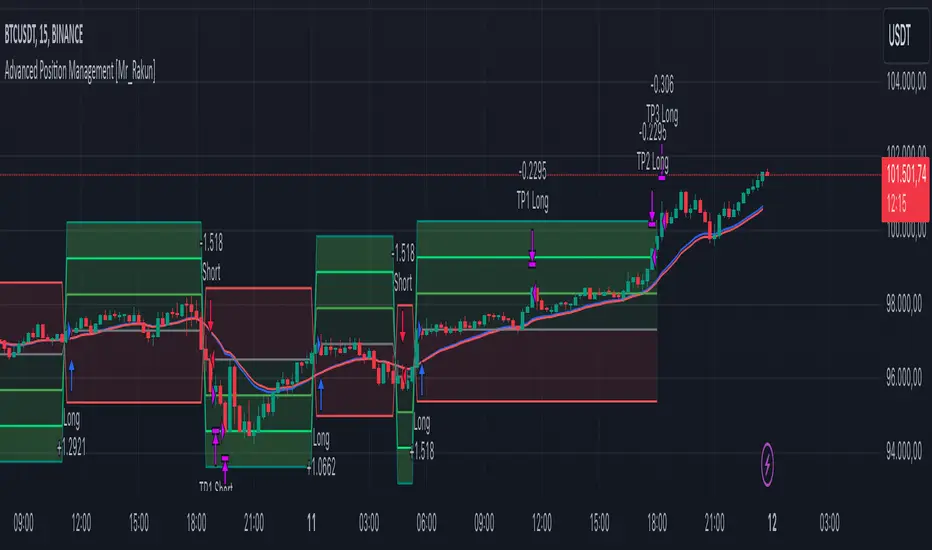

Advanced Position Management [Mr_Rakun]Advanced Position Management

This Pine Script code is for a strategy titled "Advanced Position Management," aimed at effective trade execution and management using multiple take profit levels, trailing stop loss, and dynamic position sizing.

Take Profit Levels: It defines up to three take profit (TP) levels, allowing partial position exits at different price thresholds. The take profit levels and their respective quantities are adjustable using inputs.

Stop Loss and Trailing Stop: The script implements an initial stop loss based on a percentage from the entry price. Additionally, it features a trailing stop that moves based on either a percentage or previous TP levels, dynamically adjusting to maximize gains while protecting profits.

Position Size: The position size is customizable and based on USD value, allowing the trader to manage risk more effectively.

Advantages:

Flexibility: Multiple take profit levels and a dynamic stop loss system allow traders to lock in profits while keeping the position open for further gains.

Risk Management: The initial stop loss and trailing stop help to limit losses and protect profits as the trade moves in the desired direction.

Automation: Once the strategy is deployed, it automatically handles entry, exit, and stop management, reducing the need for constant monitoring.

------ TR ------

Gelişmiş Pozisyon Yönetimi

Bu Pine Script kodu, Gelişmiş Pozisyon Yönetimi için kendi stratejilerinize kolayca entegre edeceğiniz bir risk yönetimidir. Çoklu kâr al seviyeleri, takip eden stop-loss ve dinamik pozisyon büyüklüğü kullanarak işlem yürütme ve yönetiminde etkilidir.

Gelişmiş Pozisyon Yönetimi

Kâr Alma Seviyeleri;

Kod, pozisyonların farklı fiyat seviyelerinde kısmi kapatılmasını sağlayan üç farklı kâr alma (TP) seviyesini tanımlar. Bu kâr alma seviyeleri ve ilgili miktarları, girişlerle ayarlanabilir.

Stop Loss ve Takip Eden Stop;

Koda, giriş fiyatından bir yüzdeye dayalı olarak başlangıçta stop-loss uygulanır. Ayrıca, fiyat hareketine göre kendini ayarlayan takip eden bir stop-loss sistemi bulunur. Ayrıca TP seviyelerini takip eden stop loss özelliğide vardır.

Avantajları:

Esneklik;

Çoklu kâr alma seviyeleri ve dinamik stop-loss sistemi, trader'ların kazançlarını kilitleyip aynı zamanda pozisyonu açık tutmalarına olanak tanır.

Risk Yönetimi;

Başlangıç stop-loss ve takip eden stop, zararı sınırlamaya ve kazançları korumaya yardımcı olur.

Otomasyon;

Strateji bir kez devreye alındığında, giriş, çıkış ve stop yönetimi otomatik olarak gerçekleştirilir, bu da sürekli takip ihtiyacını azaltır.

Post-Open Long Strategy with ATR-based Stop Loss and Take ProfitThe "Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit" is designed to identify buying opportunities after the German and US markets open. It combines various technical indicators to filter entry signals, focusing on breakout moments following price lateralization periods.

Key Components and Their Interaction:

Bollinger Bands (BB):

Description: Uses BB with a 14-period length and standard deviation multiplier of 1.5, creating narrower bands for lower timeframes.

Role in the Strategy: Identifies low volatility phases (lateralization). The lateralization condition is met when the price is near the simple moving average of the BB, suggesting an imminent increase in volatility.

Exponential Moving Averages (EMA):

10-period EMA: Quickly detects short-term trend direction.

200-period EMA: Filters long-term trends, ensuring entries occur in a bullish market.

Interaction: Positions are entered only if the price is above both EMAs, indicating a consolidated positive trend.

Relative Strength Index (RSI):

Description: 7-period RSI with a threshold above 30.

Role in the Strategy: Confirms the market is not oversold, supporting the validity of the buy signal.

Average Directional Index (ADX):

Description: 7-period ADX with 7-period smoothing and a threshold above 10.

Role in the Strategy: Assesses trend strength. An ADX above 10 indicates sufficient momentum to justify entry.

Average True Range (ATR) for Dynamic Stop Loss and Take Profit:

Description: 14-period ATR with multipliers of 2.0 for Stop Loss and 4.0 for Take Profit.

Role in the Strategy: Adjusts exit levels based on current volatility, enhancing risk management.

Resistance Identification and Breakout:

Description: Analyzes the highs of the last 20 candles to identify resistance levels with at least two touches.

Role in the Strategy: A breakout above this level signals a potential continuation of the bullish trend.

Time Filters and Market Conditions:

Trading Hours: Operates only during the opening of the German market (8:00 - 12:00) and US market (15:30 - 19:00).

Panic Candle: The current candle must close negative, leveraging potential emotional reactions in the market.

Avoiding Entry During Pullbacks:

Description: Checks that the two previous candles are not both bearish.

Role in the Strategy: Avoids entering during a potential pullback, improving trade success probability.

Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit

The "Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit" is designed to identify buying opportunities after the German and US markets open. It combines various technical indicators to filter entry signals, focusing on breakout moments following price lateralization periods.

Key Components and Their Interaction:

Bollinger Bands (BB):

Description: Uses BB with a 14-period length and standard deviation multiplier of 1.5, creating narrower bands for lower timeframes.

Role in the Strategy: Identifies low volatility phases (lateralization). The lateralization condition is met when the price is near the simple moving average of the BB, suggesting an imminent increase in volatility.

Exponential Moving Averages (EMA):

10-period EMA: Quickly detects short-term trend direction.

200-period EMA: Filters long-term trends, ensuring entries occur in a bullish market.

Interaction: Positions are entered only if the price is above both EMAs, indicating a consolidated positive trend.

Relative Strength Index (RSI):

Description: 7-period RSI with a threshold above 30.

Role in the Strategy: Confirms the market is not oversold, supporting the validity of the buy signal.

Average Directional Index (ADX):

Description: 7-period ADX with 7-period smoothing and a threshold above 10.

Role in the Strategy: Assesses trend strength. An ADX above 10 indicates sufficient momentum to justify entry.

Average True Range (ATR) for Dynamic Stop Loss and Take Profit:

Description: 14-period ATR with multipliers of 2.0 for Stop Loss and 4.0 for Take Profit.

Role in the Strategy: Adjusts exit levels based on current volatility, enhancing risk management.

Resistance Identification and Breakout:

Description: Analyzes the highs of the last 20 candles to identify resistance levels with at least two touches.

Role in the Strategy: A breakout above this level signals a potential continuation of the bullish trend.

Time Filters and Market Conditions:

Trading Hours: Operates only during the opening of the German market (8:00 - 12:00) and US market (15:30 - 19:00).

Panic Candle: The current candle must close negative, leveraging potential emotional reactions in the market.

Avoiding Entry During Pullbacks:

Description: Checks that the two previous candles are not both bearish.

Role in the Strategy: Avoids entering during a potential pullback, improving trade success probability.

Entry and Exit Conditions:

Long Entry:

The price breaks above the identified resistance.

The market is in a lateralization phase with low volatility.

The price is above the 10 and 200-period EMAs.

RSI is above 30, and ADX is above 10.

No short-term downtrend is detected.

The last two candles are not both bearish.

The current candle is a "panic candle" (negative close).

Order Execution: The order is executed at the close of the candle that meets all conditions.

Exit from Position:

Dynamic Stop Loss: Set at 2 times the ATR below the entry price.

Dynamic Take Profit: Set at 4 times the ATR above the entry price.

The position is automatically closed upon reaching the Stop Loss or Take Profit.

How to Use the Strategy:

Application on Volatile Instruments:

Ideal for financial instruments that show significant volatility during the target market opening hours, such as indices or major forex pairs.

Recommended Timeframes:

Intraday timeframes, such as 5 or 15 minutes, to capture significant post-open moves.

Parameter Customization:

The default parameters are optimized but can be adjusted based on individual preferences and the instrument analyzed.

Backtesting and Optimization:

Backtesting is recommended to evaluate performance and make adjustments if necessary.

Risk Management:

Ensure position sizing respects risk management rules, avoiding risking more than 1-2% of capital per trade.

Originality and Benefits of the Strategy:

Unique Combination of Indicators: Integrates various technical metrics to filter signals, reducing false positives.

Volatility Adaptability: The use of ATR for Stop Loss and Take Profit allows the strategy to adapt to real-time market conditions.

Focus on Post-Lateralization Breakout: Aims to capitalize on significant moves following consolidation periods, often associated with strong directional trends.

Important Notes:

Commissions and Slippage: Include commissions and slippage in settings for more realistic simulations.

Capital Size: Use a realistic trading capital for the average user.

Number of Trades: Ensure backtesting covers a sufficient number of trades to validate the strategy (ideally more than 100 trades).

Warning: Past results do not guarantee future performance. The strategy should be used as part of a comprehensive trading approach.

With this strategy, traders can identify and exploit specific market opportunities supported by a robust set of technical indicators and filters, potentially enhancing their trading decisions during key times of the day.

Larry Connors %b Strategy (Bollinger Band)Larry Connors’ %b Strategy is a mean-reversion trading approach that uses Bollinger Bands to identify buy and sell signals based on the %b indicator. This strategy was developed by Larry Connors, a renowned trader and author known for his systematic, data-driven trading methods, particularly those focusing on short-term mean reversion.

The %b indicator measures the position of the current price relative to the Bollinger Bands, which are volatility bands placed above and below a moving average. The strategy specifically targets times when prices are oversold within a long-term uptrend and aims to capture rebounds by buying at relatively low points and selling at relatively high points.

Strategy Rules

The basic rules of the %b Strategy are:

1. Trend Confirmation: The closing price must be above the 200-day moving average. This filter ensures that trades are made in alignment with a longer-term uptrend, thereby avoiding trades against the primary market trend.

2. Oversold Conditions: The %b indicator must be below 0.2 for three consecutive days. The %b value below 0.2 indicates that the price is near the lower Bollinger Band, suggesting an oversold condition.

3. Entry Signal: Enter a long position at the close when conditions 1 and 2 are met.

4. Exit Signal: Exit the position when the %b value closes above 0.8, signaling an overbought condition where the price is near the upper Bollinger Band.

How the Strategy Works

This strategy operates on the premise of mean reversion, which suggests that extreme price movements will revert to the mean over time. By entering positions when the %b value indicates an oversold condition (below 0.2) in a confirmed uptrend, the strategy attempts to capture short-term price rebounds. The exit rule (when %b is above 0.8) aims to lock in profits once the price reaches an overbought condition, often near the upper Bollinger Band.

Who Was Larry Connors?

Larry Connors is a well-known figure in the world of financial markets and trading. He co-authored several influential trading books, including “Short-Term Trading Strategies That Work” and “High Probability ETF Trading.” Connors is recognized for his quantitative approach, focusing on systematic, rules-based strategies that leverage historical data to validate trading edges.

His work primarily revolves around short-term trading strategies, often using technical indicators like RSI (Relative Strength Index), Bollinger Bands, and moving averages. Connors’ methodologies have been widely adopted by traders seeking structured approaches to exploit short-term inefficiencies in the market.

Risks of the Strategy

While the %b Strategy can be effective, particularly in mean-reverting markets, it is not without risks:

1. Mean Reversion Assumption: The strategy is based on the assumption that prices will revert to the mean. In trending or sharply falling markets, this reversion may not occur, leading to sustained losses.

2. False Signals in Choppy Markets: In volatile or sideways markets, the strategy may generate multiple false signals, resulting in whipsaw trades that can erode capital through frequent small losses.

3. No Stop Loss: The basic implementation of the strategy does not include a stop loss, which increases the risk of holding losing trades longer than intended, especially if the market continues to move against the position.

4. Performance During Market Crashes: During major market downturns, the strategy’s buy signals could be triggered frequently as prices decline, compounding losses without the presence of a risk management mechanism.

Scientific References and Theoretical Basis

The %b Strategy relies on the concept of mean reversion, which has been extensively studied in finance literature. Studies by Avellaneda and Lee (2010) and Bouchaud et al. (2018) have demonstrated that mean-reverting strategies can be profitable in specific market environments, particularly when combined with volatility filters like Bollinger Bands. However, the same studies caution that such strategies are highly sensitive to market conditions and often perform poorly during periods of prolonged trends.

Bollinger Bands themselves were popularized by John Bollinger and are widely used to assess price volatility and detect potential overbought and oversold conditions. The %b value is a critical part of this analysis, as it standardizes the position of price relative to the bands, making it easier to compare conditions across different securities and time frames.

Conclusion

Larry Connors’ %b Strategy is a well-known mean-reversion technique that leverages Bollinger Bands to identify buying opportunities in uptrending markets when prices are temporarily oversold. While the strategy can be effective under the right conditions, traders should be aware of its limitations and risks, particularly in trending or highly volatile markets. Incorporating risk management techniques, such as stop losses, could help mitigate some of these risks, making the strategy more robust against adverse market conditions.

Nifty scalping 3 minutesOverview:

The "Nifty Scalping 3 Minutes" strategy is a uniquely tailored trading system for Nifty Futures traders, with a clear focus on capital preservation, dynamic risk management, and high-probability trade entries. This strategy uses unique combination of standard technical indicators like Jurik Moving Average (JMA), Exponential Moving Average (EMA), and Bollinger Bands, but it truly stands out through its Price-Volume Spike Detection system—a unique mechanism designed to trigger trades only during periods of high momentum and market participation. The strategy also incorporates robust risk management, ensuring that traders minimize losses while maximizing profits. in complete back test range max drawdown is less than 1%

Scalping Approach and Requirements:

The strategy focuses on quick in and out trades, aiming to capture small, quick profits during periods of heightened market activity. For optimal performance, traders should have ₹2,00,000 or more in capital available per trade. The dynamic lot calculation and risk controls require this level of capital to function effectively.

Small, frequent trades are the focus, and the strategy is ideal for traders comfortable with high-frequency executions. Traders with insufficient capital or those not comfortable with frequent trades may find this strategy unsuitable.

Default Properties for Publication:

Initial Capital: ₹2,000,000

Lot Size: 25 contracts (adjusted dynamically based on available margin)

Stop-Loss: Risk per trade capped at 1% of equity.

Slippage and Commission: Realistic values are factored into the backtesting.

Key Feature: Price-Volume Spike Detection