Chande Kroll Trend Strategy (SPX, 1H) | PINEINDICATORSThe "Chande Kroll Stop Strategy" is designed to optimize trading on the SPX using a 1-hour timeframe. This strategy effectively combines the Chande Kroll Stop indicator with a Simple Moving Average (SMA) to create a robust method for identifying long entry and exit points. This detailed description will explain the components, rationale, and usage to ensure compliance with TradingView's guidelines and help traders understand the strategy's utility and application.

Objective

The primary goal of this strategy is to identify potential long trading opportunities in the SPX by leveraging volatility-adjusted stop levels and trend-following principles. It aims to capture upward price movements while managing risk through dynamically calculated stops.

Chande Kroll Stop Parameters:

Calculation Mode: Offers "Linear" and "Exponential" options for position size calculation. The default mode is "Exponential."

Risk Multiplier: An adjustable multiplier for risk management and position sizing, defaulting to 5.

ATR Period: Defines the period for calculating the Average True Range (ATR), with a default of 10.

ATR Multiplier: A multiplier applied to the ATR to set stop levels, defaulting to 3.

Stop Length: Period used to determine the highest high and lowest low for stop calculation, defaulting to 21.

SMA Length: Period for the Simple Moving Average, defaulting to 21.

Calculation Details:

ATR Calculation: ATR is calculated over the specified period to measure market volatility.

Chande Kroll Stop Calculation:

High Stop: The highest high over the stop length minus the ATR multiplied by the ATR multiplier.

Low Stop: The lowest low over the stop length plus the ATR multiplied by the ATR multiplier.

SMA Calculation: The 21-period SMA of the closing price is used as a trend filter.

Entry and Exit Conditions:

Long Entry: A long position is initiated when the closing price crosses over the low stop and is above the 21-period SMA. This condition ensures that the market is trending upward and that the entry is made in the direction of the prevailing trend.

Exit Long: The long position is exited when the closing price falls below the high stop, indicating potential downward movement and protecting against significant drawdowns.

Position Sizing:

The quantity of shares to trade is calculated based on the selected calculation mode (linear or exponential) and the risk multiplier. This ensures position size is adjusted dynamically based on current market conditions and user-defined risk tolerance.

Exponential Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000 * strategy.equity / strategy.initial_capital.

Linear Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000.

Execution:

When the long entry condition is met, the strategy triggers a buy signal, and a long position is entered with the calculated quantity. An alert is generated to notify the trader.

When the exit condition is met, the strategy closes the position and triggers a sell signal, accompanied by an alert.

Plotting:

Buy Signals: Indicated with an upward triangle below the bar.

Sell Signals: Indicated with a downward triangle above the bar.

Application

This strategy is particularly effective for trading the SPX on a 1-hour timeframe, capitalizing on price movements by adjusting stop levels dynamically based on market volatility and trend direction.

Default Setup

Initial Capital: $1,000

Risk Multiplier: 5

ATR Period: 10

ATR Multiplier: 3

Stop Length: 21

SMA Length: 21

Commission: 0.01

Slippage: 3 Ticks

Backtesting Results

Backtesting indicates that the "Chande Kroll Stop Strategy" performs optimally on the SPX when applied to the 1-hour timeframe. The strategy's dynamic adjustment of stop levels helps manage risk effectively while capturing significant upward price movements. Backtesting was conducted with a realistic initial capital of $1,000, and commissions and slippage were included to ensure the results are not misleading.

Risk Management

The strategy incorporates risk management through dynamically calculated stop levels based on the ATR and a user-defined risk multiplier. This approach ensures that position sizes are adjusted according to market volatility, helping to mitigate potential losses. Trades are sized to risk a sustainable amount of equity, adhering to the guideline of risking no more than 5-10% per trade.

Usage Notes

Customization: Users can adjust the ATR period, ATR multiplier, stop length, and SMA length to better suit their trading style and risk tolerance.

Alerts: The strategy includes alerts for buy and sell signals to keep traders informed of potential entry and exit points.

Pyramiding: Although possible, the strategy yields the best results without pyramiding.

Justification of Components

The Chande Kroll Stop indicator and the 21-period SMA are combined to provide a robust framework for identifying long trading opportunities in trending markets. Here is why they work well together:

Chande Kroll Stop Indicator: This indicator provides dynamic stop levels that adapt to market volatility, allowing traders to set logical stop-loss levels that account for current price movements. It is particularly useful in volatile markets where fixed stops can be easily hit by random price fluctuations. By using the ATR, the stop levels adjust based on recent market activity, ensuring they remain relevant in varying market conditions.

21-Period SMA: The 21-period SMA acts as a trend filter to ensure trades are taken in the direction of the prevailing market trend. By requiring the closing price to be above the SMA for long entries, the strategy aligns itself with the broader market trend, reducing the risk of entering trades against the overall market direction. This helps to avoid false signals and ensures that the trades are in line with the dominant market movement.

Combining these two components creates a balanced approach that captures trending price movements while protecting against significant drawdowns through adaptive stop levels. The Chande Kroll Stop ensures that the stops are placed at levels that reflect current volatility, while the SMA filter ensures that trades are only taken when the market is trending in the desired direction.

Concepts Underlying Calculations

ATR (Average True Range): Used to measure market volatility, which informs the stop levels.

SMA (Simple Moving Average): Used to filter trades, ensuring positions are taken in the direction of the trend.

Chande Kroll Stop: Combines high and low price levels with ATR to create dynamic stop levels that adapt to market conditions.

Risk Disclaimer

Trading involves substantial risk, and most day traders incur losses. The "Chande Kroll Stop Strategy" is provided for informational and educational purposes only. Past performance is not indicative of future results. Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and risk tolerance.

Chande

Chande Kroll Stop + ADX filter strategyDear TV''ers,

Hereby a script where i created a simple strategy using the underappreciated chande kroll stop indicator. Short signal is when the close crosses under the orange line and a long signal is generated upon a crossover of a close candle of the blue line.

Additionally you have the option to filter using ADX the minimize getting rekt in a choppy market.

good luck trading!

[STRATEGY] Moving Average CrossoverThis is a backtester for the Moving Average Crossover indicator.

This tool allows you to backtest 4096 combinations of different MA types x customizable periods x customizable take-profits and stop-losses = almost limitless possibilities.

Study version can be found here:

Make Moving Averages Great Again!

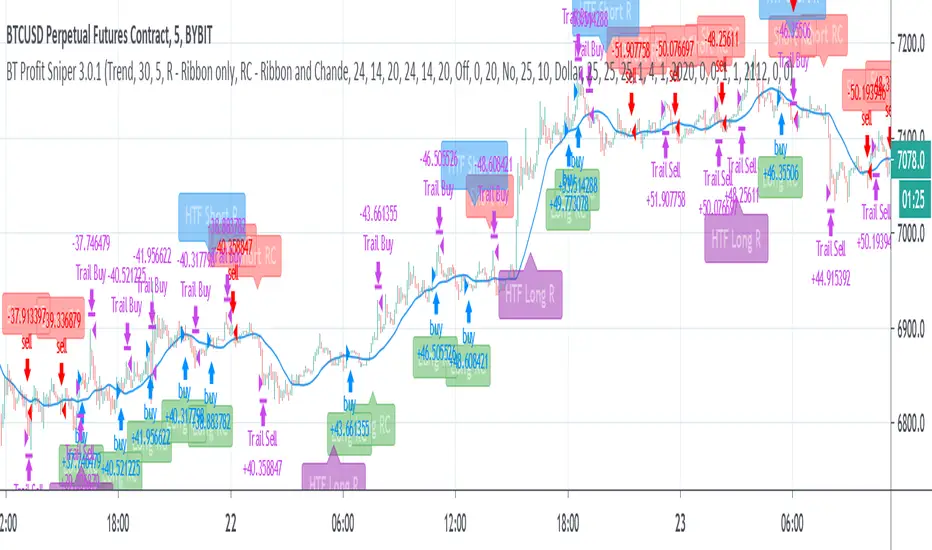

BT Profit Sniper: Insiders EditionBT Profit Sniper: Insiders Edition is an Strategy accompaniment for “Profit Sniper : Insiders Edition”, designed to evaluate the success of the long & short alerts generated to facilitate trading in BTCUSD.

The flags are derived from Bollinger Bands and Chande Momentum operating in higher & lower timeframes, as well as our own bespoke stochastic ribbons that when combined, provide insight into trend pivots as they happen.

For access, please send us a Personal Message.

QuantCat Chande Swinger StrategyQuantCat Chande Swinger

This strategy is designed to be used on the 1 minute with mainly bitcoin, and cryptocurrencies. But parameters can be adjusted to ANY pair.

After some long research about chande momentum oscillator, I decided to create a strategy using normal distribution percentage levels to snipe entries. This in turn on the 1 minute can create a nice profit over a consecutive amount of days, the end goal is to get a stronger version of this strategy running on a bot and print some money. This strategy is tightly defined, and can be loosened up to make more trades too- giving a higher sample size and better sharpe ratio.

The strategy checks to see if the Chande value is in an extreme percentile based on the last few hundred chande values- if it is it will open a position.

No stoploss or take profit implemented into the swinger yet, but this will be the next addition to really minimise loss and amplify potential profits.

Any liquid crypto pair on the low timesframes will net a good result with this strategy.

We also have a free 15M and 1H strategy available too.

You can join our discord server to get live alerts for the strategies as well as speak to our devs! Link in signature below!!!

Combo Backtest 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Chande Momentum Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors

Combo Backtest 123 Reversal & Chande Forecast Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

WARNING:

- For purpose educate only

- This script to change bars colors.

Dynamic Momentum Index (DMI) Backtest This indicator plots Dynamic Momentum Index indicator. The Dynamic Momentum

Index (DMI) was developed by Tushar Chande and Stanley Kroll. The indicator

is covered in detail in their book The New Technical Trader.

The DMI is identical to Welles Wilder`s Relative Strength Index except the

number of periods is variable rather than fixed. The variability of the time

periods used in the DMI is controlled by the recent volatility of prices.

The more volatile the prices, the more sensitive the DMI is to price changes.

In other words, the DMI will use more time periods during quiet markets, and

less during active markets. The maximum time periods the DMI can reach is 30

and the minimum is 3. This calculation method is similar to the Variable

Moving Average, also developed by Tushar Chande.

The advantage of using a variable length time period when calculating the RSI

is that it overcomes the negative effects of smoothing, which often obscure short-term moves.

The volatility index used in controlling the time periods in the DMI is based

on a calculation using a five period standard deviation and a ten period average

of the standard deviation.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Qstick Indicator Backtest A technical indicator developed by Tushar Chande to numerically identify

trends in candlestick charting. It is calculated by taking an 'n' period

moving average of the difference between the open and closing prices. A

Qstick value greater than zero means that the majority of the last 'n' days

have been up, indicating that buying pressure has been increasing.

Transaction signals come from when the Qstick indicator crosses through the

zero line. Crossing above zero is used as the entry signal because it is indicating

that buying pressure is increasing, while sell signals come from the indicator

crossing down through zero. In addition, an 'n' period moving average of the Qstick

values can be drawn to act as a signal line. Transaction signals are then generated

when the Qstick value crosses through the trigger line.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Chande Forecast Oscillator Backtest The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Chande Forecast Oscillator The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.