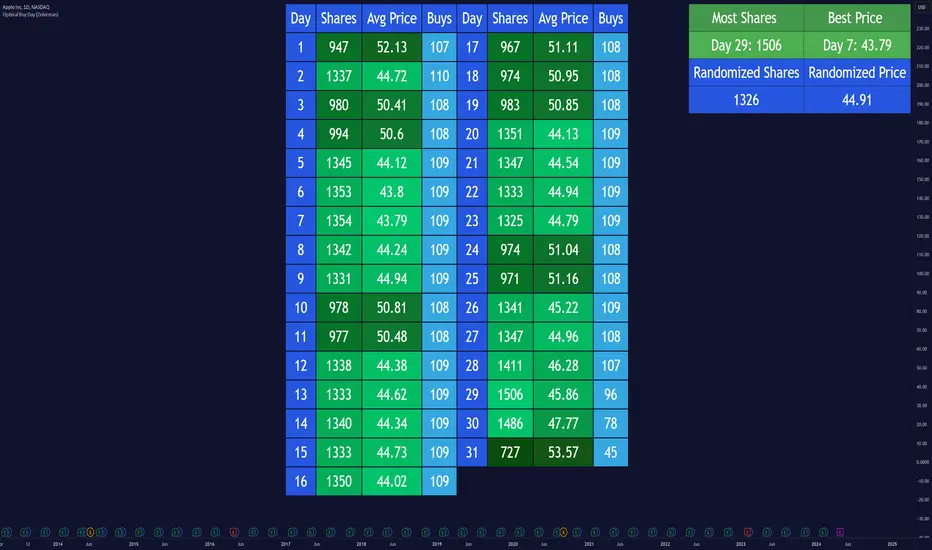

Optimal Buy Day (Zeiierman)█ Overview

The Optimal Buy Day (Zeiierman) indicator identifies optimal buying days based on historical price data, starting from a user-defined year. It simulates investing a fixed initial capital and making regular monthly contributions. The unique aspect of this indicator involves comparing systematic investment on specific days of the month against a randomized buying day each month, aiming to analyze which method might yield more shares or a better average price over time. By visualizing the potential outcomes of systematic versus randomized buying, traders can better understand the impact of market timing and how regular investments might accumulate over time.

These statistics are pivotal for traders and investors using the script to analyze historical performance and strategize future investments. By understanding which days offered more shares for their money or lower average prices, investors can tailor their buying strategies to potentially enhance returns.

█ Key Statistics

⚪ Shares

Definition: Represents the total number of shares acquired on a particular day of the month across the entire simulation period.

How It Works: The script calculates how many shares can be bought each day, given the available capital or monthly contribution. This calculation takes into account the day's opening price and accumulates the total shares bought on that day over the simulation period.

Interpretation: A higher number of shares indicates that the day consistently offered better buying opportunities, allowing the investor to acquire more shares for the same amount of money. This metric is crucial for understanding which days historically provided more value.

⚪ AVG Price

Definition: The average price paid per share on a particular day of the month, averaged over the simulation period.

How It Works: Each time shares are bought, the script calculates the average price per share, factoring in the new shares purchased at the current price. This average evolves over time as more shares are bought at varying prices.

Interpretation: The average price gives insight into the cost efficiency of buying shares on specific days. A lower average price suggests that buying on that day has historically led to better pricing, making it a potentially more attractive investment strategy.

⚪ Buys

Definition: The total number of transactions or buys executed on a particular day of the month throughout the simulation.

How It Works: This metric increments each time shares are bought on a specific day, providing a count of all buying actions taken.

Interpretation: The number of buys indicates the frequency of investment opportunities. A higher count could mean more consistent opportunities for investment, but it's important to consider this in conjunction with the average price and the total shares acquired to assess overall strategy effectiveness.

⚪ Most Shares

Definition: Identifies the day of the month on which the highest number of shares were bought, highlighting the specific day and the total shares acquired.

How It Works: After simulating purchases across all days of the month, the script identifies which day resulted in the highest total number of shares bought.

Interpretation: This metric points out the most opportune day for volume buying. It suggests that historically, this day provided conditions that allowed for maximizing the quantity of shares purchased, potentially due to lower prices or other factors.

⚪ Best Price

Definition: Highlights the day of the month that offered the lowest average price per share, indicating both the day and the price.

How It Works: The script calculates the average price per share for each day and identifies the day with the lowest average.

Interpretation: This metric is key for investors looking to minimize costs. The best price day suggests that historically, buying on this day led to acquiring shares at a more favorable average price, potentially maximizing long-term investment returns.

⚪ Randomized Shares

Definition: This metric represents the total number of shares acquired on a randomly selected day of the month, simulated across the entire period.

How It Works: At the beginning of each month within the simulation, the script selects a random day when the market is open and calculates how many shares can be purchased with the available capital or monthly contribution at that day's opening price. This process is repeated each month, and the total number of shares acquired through these random purchases is tallied.

Interpretation: Randomized shares offer a comparison point to systematic buying strategies. By comparing the total shares acquired through random selection against those bought on the best or worst days, investors can gauge the impact of timing and market fluctuations on their investment strategy. A higher total in randomized shares might indicate that over the long term, the specific days chosen for investment might matter less than consistent market participation. Conversely, if systematic strategies yield significantly more shares, it suggests that timing could indeed play a crucial role in maximizing investment returns.

⚪ Randomized Price

Definition: The average price paid per share for the shares acquired on the randomly selected days throughout the simulation period.

How It Works: Each time shares are bought on a randomly chosen day, the script calculates the average price paid for all shares bought through this randomized strategy. This average price is updated as the simulation progresses, reflecting the cost efficiency of random buying decisions.

Interpretation: The randomized price metric helps investors understand the cost implications of a non-systematic, random investment approach. Comparing this average price to those achieved through more deliberate, systematic strategies can reveal whether consistent investment timing strategies outperform random investment actions in terms of cost efficiency. A lower randomized price suggests that random buying might not necessarily result in higher costs, while a higher average price indicates that systematic strategies might provide better control over investment costs.

█ How to Use

Traders can use this tool to analyze historical data and simulate different investment strategies. By inputting their initial capital, regular contribution amount, and start year, they can visually assess which days might have been more advantageous for buying, based on historical price actions. This can inform future investment decisions, especially for those employing dollar-cost averaging strategies or looking to optimize entry points.

█ Settings

StartYear: This setting allows the user to specify the starting year for the investment simulation. Changing this value will either extend or shorten the period over which the simulation is run. If a user increases the value, the simulation begins later and covers a shorter historical period; decreasing the value starts the simulation earlier, encompassing a longer time frame.

Capital: Determines the initial amount of capital with which the simulation begins. Increasing this value simulates starting with more capital, which can affect the number of shares that can be initially bought. Decreasing this value simulates starting with less capital.

Contribution: Sets the monthly financial contribution added to the investment within the simulation. A higher contribution increases the investment each month and could lead to more shares being purchased over time. Lowering the contribution decreases the monthly investment amount.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

EDGE

Probabilities Module - The Quant Science This module can be integrate in your code strategy or indicator and will help you to calculate the percentage probability on specific event inside your strategy. The main goal is improve and simplify the workflow if you are trying to build a quantitative strategy or indicator based on statistics or reinforcement model.

Logic

The script made a simulation inside your code based on a single event. For single event mean a trading logic composed by three different objects: entry, take profit, stop loss.

The script scrape in the past through a look back function and return the positive percentage probability about the positive event inside the data sample. In this way you are able to understand and calculate how many time (in percentage term) the conditions inside the single event are positive, helping to create your statistical edge.

You can adjust the look back period in you user interface.

How can set up the module for your use case

At the top of the script you can find:

1. entry_condition : replace the default condition with your specific entry condition.

2. TPcondition_exit : replace the default condition with your specific take profit condition.

3. SLcondition_exit : replace the default condition with your specific stop loss condition.

SuperJump Edge CCI RSIThis indicator for detecting inflection points of CCI and RSI.

Low time frames have high variability, which can lead to more unreliable signals.

But you can filter it appropriately by entering the levels of oversold and overbought.

Because CCI is highly volatile, RSI signals are more reliable.

You can also use it for other panes for example RSI or CCI pane.

Repainting is not used because I implemented the filter by myself.

[TTI] Edge Arrows––––History & Credit

This indicator has been done from deep analysis of the common market conditions prior to having a massive winner. We have analysed over 400 stocks, thought by Mark Minervini in his Master Trader Program and found that in 95% of the cases the EDGE arrow occurs during the buy points!!

–––––What it does

The indicator mixes unique analysis of the RSIs, Moving averages and Bollinger Bands to print out a high probability reversal arrows. It works both on the upside and the downside.

–––––How to use it

Use the indicator as an confirmation signal for the direction of trading. When the arrow EdgeUp points there is high probabiliy of move to the long side and when the arrow EdgeDown prints there is a high probability for reversal trend/

EXAMPLES

Oscillator EdgesAnother simple script to be added on top of other indicators. Simply provides a symbol of varying color depending on the value of the oscillator. Allows up to 4 different colors in each direction. Includes alerts conditions. Demonstration is the indicator being applied to the RSI (purple) included in Market Cipher B.

To use, simply add it to your indicator, and choose and oscillator of your choice in the Input Settings. Alternatively, you can just keep it on 'close' and use the built in RSI. Or, you can use the RSI formula on top of something else (if that's your thing).

The names are silly, so I hope this is okay with all of you.

Let me know what you think, and if there are any problems, questions, or concerns!

vertical_pricer

USAGE

1. Select the type of contract (call or put), the long strike, and the width.

2. Select the volatility model

3. The standard deviation is shown, enter it into the input.

The tool gives a theoretical price of a vertical spread, based on a

historical sample. The test assumes that a spread of equal width was sold on

every prior trading day at the given standard deviation, based on the

volatility model and duration of the contract. For example, if the 20 dte

110 strike is presently two standard deviations based on the 30 period

historical volatility, then the theoretical value is the average price all

2SD (at 20 dte) calls upon expiration, limited by the width of the spread and

normalized according to the present value of the underlying.

Other statistics include:

- The number of spreads in the sample, and percentage expired itm

- The median value at expiration

- The Nth percentile value of spreads at expiration

- The number of spreads that expired at max loss

Check the script comments and release notes for further updates, since Tradingview doesn't allow me to edit this description.

strangle_pricerUsage:

1. Set the put and call strike inputs to values of your choosing.

2. Select "days to expiration".

3. Set the put and call standard deviations using the output table.

The indicator is meant help price a strangle using historical data and a volatility model. By default, the model is an ewma-method historical volatility. After selecting strikes and standard their corresponding standard deviation, theoretical values and probabilities will be shown in the table. The script is initialized with -1 for several inputs, and won't show any data until these are adjusted.

The theoretical values shown assume a strangle was bought or sold on every historical bar, and averaging their value at expiration.

For example, if you choose the $50 call and $40 put when the underlying is at $45 and there are 30 days until expiration, suppose the volatility is N and

these strikes correspond to M standard deviations. Input those and the resulting theoretial values shown will be based on opening a 30 dte call and put at M standard deviations with respect to the volatility at each bar.

- Past volatility forecasts are plotted in blue, and hidden by default.

- The current volatility forecast is drawn as a blue line.

- The put and call strikes are drawn as red lines.

This indicator is only meant for the daily chart!

Since I won't be able to edit this description later, also check the release notes and script comments for important changes.

GODXBTTRADING SCRIPT "GODXBT"

ALL IN ONE !!!

This script helps you to understand the market situation

Script includes

. Support & resistance tool

. 3 EMA's ( exponential moving average ) ( you can change ema values )

. Smooth Guppy : helps to understand support and resistance also helps to understand trend direction ( Red is bearish trend & Blue is bullish trend )

. And Buy & Sell signals to take entry and exit

how to trade :

Buy/Long when " BUY " signal appears

Sell/Short when " SELL " signal appears

take profits near support and resistance lines / close position on the break of it

* Customized Switches to on/off Guppy , S/R levels

* When guppy is blue longs are profitable and when red shorts are profitable

*DM for access

Edge-Preserving FilterIntroduction

Edge-preserving smoothing is often used in image processing in order to preserve edge information while filtering the remaining signal. I introduce two concepts in this indicator, edge preservation and an adaptive cumulative average allowing for fast edge-signal transition with period increase over time. This filter have nothing to do with classic filters for image processing, those filters use kernels convolution and are most of the time in a spatial domain.

Edge Detection Method

We want to minimize smoothing when an edge is detected, so our first goal is to detect an edge. An edge will be considered as being a peak or a valley, if you recall there is one of my indicator who aim to detect peaks and valley (reference at the bottom of the post) , since this estimation return binary outputs we will use it to tell our filter when to stop filtering.

Filtering Increase By Using Multi Steps Cumulative Average

The edge detection is a binary output, using a exponential smoothing could be possible and certainly more efficient but i wanted instead to try using a cumulative average approach because it smooth more and is a bit more original to use an adaptive architecture using something else than exponential averaging. A cumulative average is defined as the sum of the price and the previous value of the cumulative average and then this result is divided by n with n = number of data points. You could say that a cumulative average is a moving average with a linear increasing period.

So lets call CMA our cumulative average and n our divisor. When an edge is detected CMA = close price and n = 1 , else n is equal to previous n+1 and the CMA act as a normal cumulative average by summing its previous values with the price and dividing the sum by n until a new edge is detected, so there is a "no filtering state" and a "filtering state" with linear period increase transition, this is why its multi-steps.

The Filter

The filter have two parameters, a length parameter and a smooth parameter, length refer to the edge detection sensitivity, small values will detect short terms edges while higher values will detect more long terms edges. Smooth is directly related to the edge detection method, high values of smooth can avoid the detection of some edges.

smooth = 200

smooth = 50

smooth = 3

Conclusion

Preserving the price edges can be useful when it come to allow for reactivity during important price points, such filter can help with moving average crossover methods or can be used as a source for other indicators making those directly dependent of the edge detection.

Rsi with a period of 200 and our filter as source, will cross triggers line when an edge is detected

Feel free to share suggestions ! Thanks for reading !

References

Peak/Valley estimator used for the detection of edges in price.

Session P EdgesThis is an attempt to chart the primary balance ranges, however,

I have been having difficulty getting the lows to work in the graph, any assistance would be welcome

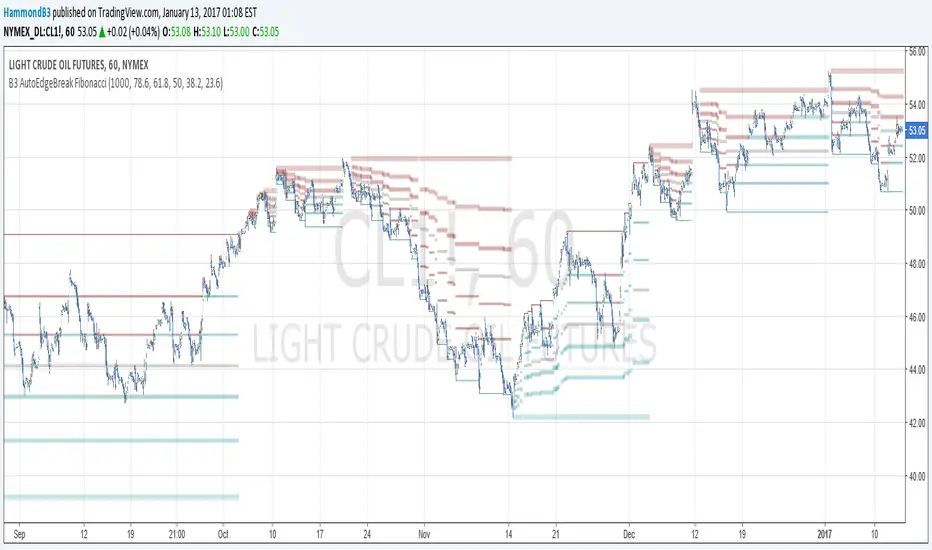

B3 AutoEdgeBreak FibonacciHere is the lazy person's Fibonacci retracement drawing machine. Keep the bars in range pretty big, but you can play around and see what it does. If too small, it gets in your way, and If oversized, your retracements will not properly work upward and downward according to action. So, if you notice that it's always retracing the same direction, then lower the first input.

Now on top of the coding being tricky because of massive history in T-view, trading the Fibs is not an easy task either. Experienced Fib traders will probably love my script, and those that are not good at Fibs will love the historical look of it, but feel helpless in real-time. It took me years to learn a reaction pattern to the Fib lines, and the one key piece of my memory: if a price-line test comes and fails in relation to your trade, get out!!! <- Not real advice, just experience talking.

I expect to be upgrading this particular script in the future. Enjoy!

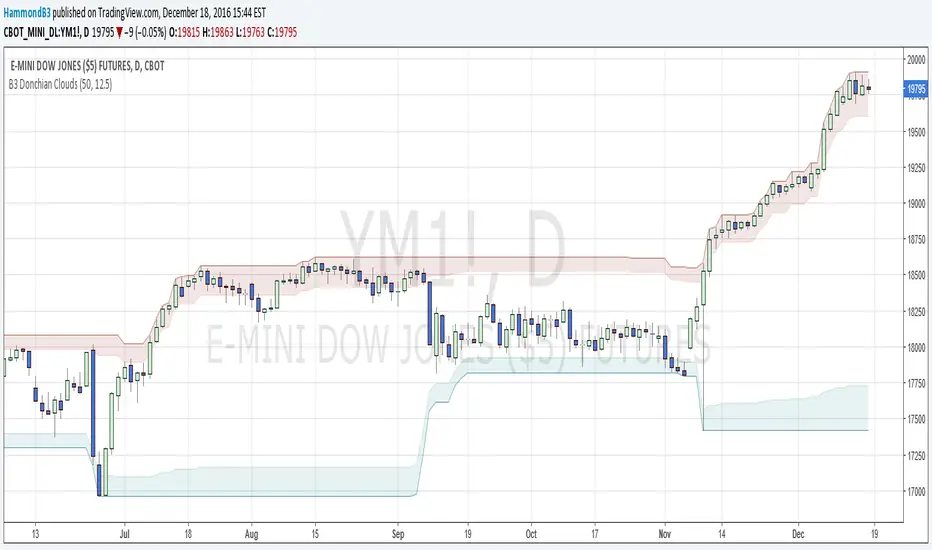

B3 Donchian CloudsThis is the Donchian Channel expressed with a percentage cloud. Default 12.5% of the range will be filled at each edge, this helps to show reversal possibilities as price returns to the area between the clouds. This offers a usage to essentially fade the turtle trader system. That system is loosely based on the playing of the breakouts of the the channel... as you can see the that last turtle trade long in YM1! was and is off the charts awesome. I will look for the fall out of the cloud to short the market.