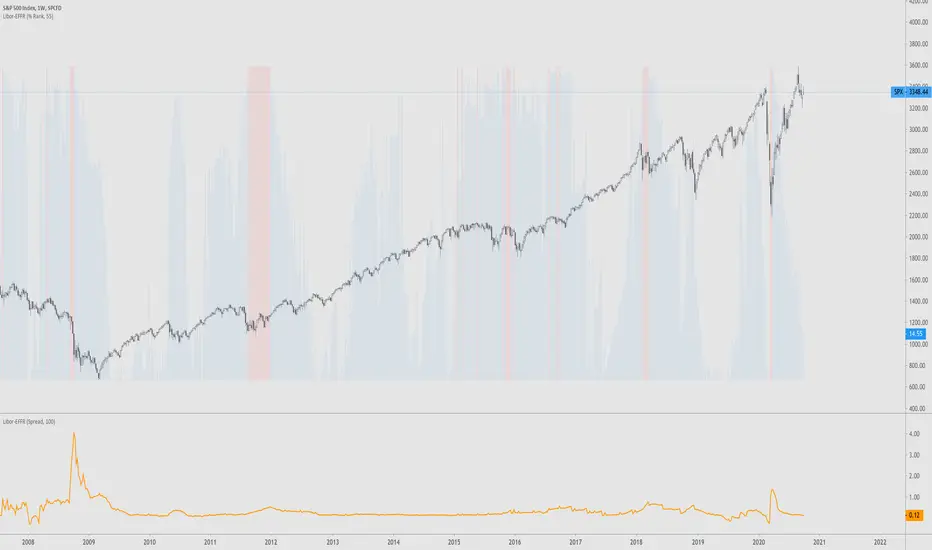

Libor-EFFRThis is the 3-month Libor minus effective federal funds rate. Traders watch certain spreads for a wider spread to indicate a bad economy.

This is a conceptual indicator that tries to make sense of how important a FRA-OIS spread can be, in this case the Libor-EFFR. It may be completely wrong in calculation and understanding :)

en.wikipedia.org

www.investopedia.com

Libor was derived from the TED Spread less 3-month treasury bills due to Quandl missing updated Libor data.

fred.stlouisfed.org

fred.stlouisfed.org

For the OIS, EFFR is used because it has long historical data and is one of (maybe) the rates used for spread. SOFR was not available at the time but it appears that is what is more common nowadays.

A possible derivative of this indicator would be taking Libor and putting it against something else.