Indian NIFTY Correlation Daytrade/Swing StrategyINTRODUCTION :

This is a daytrading/swing strategy designed mainly for indian market where internally has been adapted to NIFTY market and as well using for internal calculations the values of the candles from NIFTY asset.

With it we search to use with the most correlated asset from the indian market.

For this example I choosed BANKNIFTY

STRATEGY:

The strategy initially uses as candle values the data from the NIFTY asset.

With them I am dividing the work into two calculation parts such as :

-For first part logic, I am doing calculations regarding the volatility of NIFTY, where I initially take into consideration INDIAVIX to have an idea of the expected implied volatility of NIFTY asset and then I compare it with different tools such as ATR, BB and Percentile location of the volatility.

Based on all these factors I take into account the location of the volatility which is atm and if there is a possibility of a strong movement(trend) or sidemarket situation.

-Once I am done with the values of the volatility, the next process in the script logic is to start looking into the trend.

For it I am using different tools such as volume checker, support and resistence key points, pivot points, price actions patterns and different moving averages.

-Risk management part : once we are done with calculation for the entry, the next part is to have an idea where to exit. In this case I am making use of a dynamic risk management which is compressed from multiple ideas such as : we can exit if there were a big gap on the next day in our initial direction, we can also exit based of an internal daily ATR calculation value(we use initially 15min timeframe chart) and lastly if we are around some key points like support/resistence or other different chart patterns like double top, double bot and so on.

CASE EXAMPLE:

As I said before we are initially using for calculation the NIFTY chart with 15min timeframe. With it we can apply to any indian etf,stocks,future. All the assets are going to have the same time of entry and the same time of exit(we get this from NIFTY) and we plot it on the chart we are using, so its key point to look for assets which have a min 75-80% correlation with NIFTY. For this example I used BANKNIFTY chart.

So a type of entry would be this way

Lets assume NIFTY50 is on 19.000 level

INDIAVIX level is currently at 11 which can be translated : 11 / sqrt(250)

So 11 means that on a yearly base we expect the asset to move 11% upwards or downwards

and in a year we have aprox 250 days. So we divide the 11 by sqrt of 250 to get an idea of a daily expected move from the implied volatility of india VIX

11/15.87 = +-0.69%

So INDIAVIX tells us that the values for today nifty is 19000+0,69% and 19000-0.69%

After that I am looking into the daily ATR, and I see that the expected is around 0.8% and is ascending over the last 2 weeks.

Lastly I am looking at the percentile which is currently the volatility on both ATR and INDIAVIX, and I get a value of 90th percentile.

With this my biased is that we are going to expect a short trend, but i cant confirm on the volatility alone so next step is start looking into technical analysis.

I look at volume and is increasing, I look at different price actions paterns and pivots and I see a lower low and a lower high (a descending pattern).

I also see the price is below the key MA like SMA50/100/200, VWAP and so on.

With all of this I get more confirmation that the asset is in a short trend.

Internally once a certain specific % of confirmation from all the logics is achieved, it will trigger a long/short entry, so in this case lets assume we have 80% of our indicators pointing to the short, is going to enter a short.

Now for a long scenario the scene would be , indiavix is around 9,5, ATR is descending. We are around 40th percentile of the volatility.

Our asset is above multiple moving averages, vwap , etc

We have an increasing volume towards bullish side.

And so on( overall 75% of our indicators are pointing towards the long side)

Now for the exit, since we are dealing with a daytrade/swing mentality, short on average we keep the trade open for a less period of time than long ( 19 bars of 15min candles, compared to 57 bars of 15min for long) , so most of the times for short we are going to exit next day and if the trend is still in our favour we re enter the trade.

For long we can stay much more time, sometimes even weeks and we exit mainly when the % of confirmation of indicators point out a reversal/short confirmation fo a big pice action pattern.

STRATEGY RESULTS

For strategy analysis I have used BANKNIFTY NSE with deep history to get access to data from 2011 until present( giving more than 2500 trades) .

For inputs I am using 0.02% comission total ( the comission applied from ZERODHA indian exchange is close to 0.0175% total) so I used it a bit higher in order to take into account some slippages.

For capital THE REASON I USED 100% of the capital allocation is to make a proper comparison with the buy an hold from the same period

Lets assume we had an account of 1M ruppes initially in 2011, we start using 100% of it and then the new values automatically compounded with the new profits and losses so directly compare with 1M of rupees in shares on BANKNIFTY ETFs bought in 2011(buy n hold) until present day.

STRATEGY ACCESS

Strategy is free to be tested for everyone, just let me know in private that you wish to get access to it.

Indianmarkets

PIVOT STRATEGY [INDIAN MARKET TIMING]

A Back-tested Profitable Strategy for Free!!

A PIVOT INTRADAY STRATEGY for 5 minute Time-Frame , that also explains the time condition for Indian Markets

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above ema1 ,indicated by pivot highest line in green color .

2) Price crosses below ema1 ,indicated by pivot lowest line in red color .

3) Candle high crosses above pivot highest , is the Long condition .

4) Candle low crosses below pivot lowest , is the Short condition .

5) Maximum Risk per trade for the intraday trade can be changed .

6) Default_qty_size is set to 60 contracts , which can be changed under settings → properties → order size .

7) ATR is used for trailing after entry, as mentioned in the inputs below.

// ═════════════════════════//

// ————————> INPUTS <————————— //

// ═════════════════════════//

Leftbars —————> Length of pivot highs and lows

Rightbars —————> Length of pivot highs and lows

Price Cross Ema —————> Added condition

ATR LONG —————> ATR stoploss trail for Long positions

ATR SHORT —————> ATR stoploss trail for Short positions

RISK —————> Maximum Risk per trade for the day

The strategy was back-tested on RELIANCE ,the input values and the results are mentioned under "BACKTEST RESULTS" below .

// ═════════════════════════ //

// ————————> PROPERTIES<——————— //

// ═════════════════════════ //

Default_qty_size ————> 60 contracts , which can be changed under settings

↓

properties

↓

order size

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the script , Add it → click on ' { } ' → Pine editor→ making it a copy [right top corner} → Edit the line 25 .

The Indian Markets open at 9:15am and closes at 3:30pm .

The 'time_cond' specifies the time at which Entries should happen .

"Close All" function closes all the trades at 3pm, at the open of the next candle.

To change the time to close all trades , Go to Pine Editor → Edit the line 103 .

All open trades get closed at 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

NSE:RELIANCE

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 128 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better back-test results.

The strategy applied to NIFTY ( 5 min Time-Frame and contract size 60 ) gives us 60% profitability y , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.45 ,net Profit of 21,500Rs profit .

Sharpe Ratio : 0.311

Sortino Ratio : 0.727

The graph has a Linear Curve with consistent profits .

The INPUTS are as follows,

1) Leftbars ————————> 3

2) Rightbars ————————> 5

3) Price Cross Ema ——————> 150

4) ATR LONG ————————> 2.7

5) ATR SHORT ———————> 2.9

6) RISK —————————> 2500

7) Default qty size ——————> 60

NSE:RELIANCE

Save it to favorites.

Apply it to your charts Now !!

↓

FOLLOW US FOR MORE !

Thank me later ;)

Channel Cross StrategyTrend Following using Channel based Script. Long and Short Entry based on Custom filter to avoid False Signal.

Works best for BankNifty and Nifty and few Indian Stocks.

Untick Exponential gives better Result.

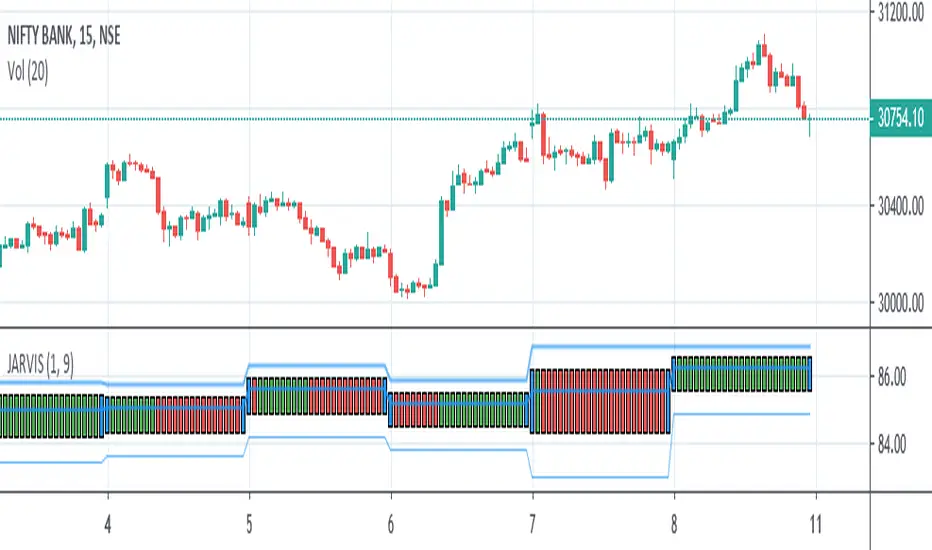

JARVISJARVIS is a technical indicator primarily designed for Nifty Bank. But, it also works on other instruments like stocks for example. You may apply it on other instruments if you find it useful.

Once the indicator is plotted, it will have bars with 3 colours

1) Blue - It's watching

2) Green - It's bullish

3) Red - It's bearish

So, it's that easy to interpret.

Following are few examples on NSE:BANKNIFTY

September 20, 2019 - Indicator turned green and remained so till end of the day. If you would have followed this, you would have made more than 2000 points.

September 25, 2019 - Indicator turned red and remained so till end of the day. If you would have followed this, you would have made more than 100 points.

September 26, 2019 and September 27, 2019 - Indicator remained blue and you see that the market was just consolidating.

Above are just a few examples of what this is capable of. Apart from Nifty Bank, it also works well on popular stocks like Reliance, TCS, SBIN etc

Recommended time frame for this is 15 mins, but, you may experiment with other time frames as well. It's all about finding the right time frame for that particular instrument, for example it works best on 2H when applied on Nifty.

Should you have any doubts, feel free to DM me.