Mean Reversion Cloud (Ornstein-Uhlenbeck) // AlgoFyreThe Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator detects mean-reversion opportunities by applying the Ornstein-Uhlenbeck process. It calculates a dynamic mean using an Exponential Weighted Moving Average, surrounded by volatility bands, signaling potential buy/sell points when prices deviate.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Adaptive Mean Calculation

🔸Volatility-Based Cloud

🔸Speed of Reversion (θ)

🔶 FUNCTIONALITY

🔸Dynamic Mean and Volatility Bands

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Visualization via Table and Plotshapes

🞘 Table Overview

🞘 Plotshapes Explanation

🞘 Code extract

🔶 INSTRUCTIONS

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

🞘 Understanding What to Look For on the Chart

🞘 Possible Entry Signals

🞘 Possible Take Profit Strategies

🞘 Possible Stop-Loss Levels

🞘 Additional Tips

🔸Customize settings

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) is a unique indicator that applies the Ornstein-Uhlenbeck stochastic process to identify mean-reverting behavior in asset prices. Unlike traditional moving average-based indicators, this model uses an Exponentially Weighted Moving Average (EWMA) to calculate the long-term mean, dynamically adjusting to recent price movements while still considering all historical data. It also incorporates volatility bands, providing a "cloud" that visually highlights overbought or oversold conditions. By calculating the speed of mean reversion (θ) through the autocorrelation of log returns, this indicator offers traders a more nuanced and mathematically robust tool for identifying mean-reversion opportunities. These innovations make it especially useful for markets that exhibit range-bound characteristics, offering timely buy and sell signals based on statistical deviations from the mean.

🔸Adaptive Mean Calculation Traditional MA indicators use fixed lengths, which can lead to lagging signals or over-sensitivity in volatile markets. The Mean Reversion Cloud uses an Exponentially Weighted Moving Average (EWMA), which adapts to price movements by dynamically adjusting its calculation, offering a more responsive mean.

🔸Volatility-Based Cloud Unlike simple moving averages that only plot a single line, the Mean Reversion Cloud surrounds the dynamic mean with volatility bands. These bands, based on standard deviations, provide traders with a visual cue of when prices are statistically likely to revert, highlighting potential reversal zones.

🔸Speed of Reversion (θ) The indicator goes beyond price averages by calculating the speed at which the price reverts to the mean (θ), using the autocorrelation of log returns. This gives traders an additional tool for estimating the likelihood and timing of mean reversion, making the signals more reliable in practice.

🔶 FUNCTIONALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator is designed to detect potential mean-reversion opportunities in asset prices by applying the Ornstein-Uhlenbeck stochastic process. It calculates a dynamic mean through the Exponentially Weighted Moving Average (EWMA) and plots volatility bands based on the standard deviation of the asset's price over a specified period. These bands create a "cloud" that represents expected price fluctuations, helping traders to identify overbought or oversold conditions. By calculating the speed of reversion (θ) from the autocorrelation of log returns, the indicator offers a more refined way of assessing how quickly prices may revert to the mean. Additionally, the inclusion of volatility provides a comprehensive view of market conditions, allowing for more accurate buy and sell signals.

Let's dive into the details:

🔸Dynamic Mean and Volatility Bands The dynamic mean (μ) is calculated using the EWMA, giving more weight to recent prices but considering all historical data. This process closely resembles the Ornstein-Uhlenbeck (OU) process, which models the tendency of a stochastic variable (such as price) to revert to its mean over time. Volatility bands are plotted around the mean using standard deviation, forming the "cloud" that signals overbought or oversold conditions. The cloud adapts dynamically to price fluctuations and market volatility, making it a versatile tool for mean-reversion strategies. 🞘 How it works Step one: Calculate the dynamic mean (μ) The Ornstein-Uhlenbeck process describes how a variable, such as an asset's price, tends to revert to a long-term mean while subject to random fluctuations. In this indicator, the EWMA is used to compute the dynamic mean (μ), mimicking the mean-reverting behavior of the OU process. Use the EWMA formula to compute a weighted mean that adjusts to recent price movements. Assign exponentially decreasing weights to older data while giving more emphasis to current prices. Step two: Plot volatility bands Calculate the standard deviation of the price over a user-defined period to determine market volatility. Position the upper and lower bands around the mean by adding and subtracting a multiple of the standard deviation. 🞘 How to calculate Exponential Weighted Moving Average (EWMA)

The EWMA dynamically adjusts to recent price movements:

mu_t = lambda * mu_{t-1} + (1 - lambda) * P_t

Where mu_t is the mean at time t, lambda is the decay factor, and P_t is the price at time t. The higher the decay factor, the more weight is given to recent data.

Autocorrelation (ρ) and Standard Deviation (σ)

To measure mean reversion speed and volatility: rho = correlation(log(close), log(close ), length) Where rho is the autocorrelation of log returns over a specified period.

To calculate volatility:

sigma = stdev(close, length)

Where sigma is the standard deviation of the asset's closing price over a specified length.

Upper and Lower Bands

The upper and lower bands are calculated as follows:

upper_band = mu + (threshold * sigma)

lower_band = mu - (threshold * sigma)

Where threshold is a multiplier for the standard deviation, usually set to 2. These bands represent the range within which the price is expected to fluctuate, based on current volatility and the mean.

🞘 Code extract // Calculate Returns

returns = math.log(close / close )

// Calculate Long-Term Mean (μ) using EWMA over the entire dataset

var float ewma_mu = na // Initialize ewma_mu as 'na'

ewma_mu := na(ewma_mu ) ? close : decay_factor * ewma_mu + (1 - decay_factor) * close

mu = ewma_mu

// Calculate Autocorrelation at Lag 1

rho1 = ta.correlation(returns, returns , corr_length)

// Ensure rho1 is within valid range to avoid errors

rho1 := na(rho1) or rho1 <= 0 ? 0.0001 : rho1

// Calculate Speed of Mean Reversion (θ)

theta = -math.log(rho1)

// Calculate Volatility (σ)

sigma = ta.stdev(close, corr_length)

// Calculate Upper and Lower Bands

upper_band = mu + threshold * sigma

lower_band = mu - threshold * sigma

🔸Visualization via Table and Plotshapes

The table shows key statistics such as the current value of the dynamic mean (μ), the number of times the price has crossed the upper or lower bands, and the consecutive number of bars that the price has remained in an overbought or oversold state.

Plotshapes (diamonds) are used to signal buy and sell opportunities. A green diamond below the price suggests a buy signal when the price crosses below the lower band, and a red diamond above the price indicates a sell signal when the price crosses above the upper band.

The table and plotshapes provide a comprehensive visualization, combining both statistical and actionable information to aid decision-making.

🞘 Code extract // Reset consecutive_bars when price crosses the mean

var consecutive_bars = 0

if (close < mu and close >= mu) or (close > mu and close <= mu)

consecutive_bars := 0

else if math.abs(deviation) > 0

consecutive_bars := math.min(consecutive_bars + 1, dev_length)

transparency = math.max(0, math.min(100, 100 - (consecutive_bars * 100 / dev_length)))

🔶 INSTRUCTIONS

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator can be set up by adding it to your TradingView chart and configuring parameters such as the decay factor, autocorrelation length, and volatility threshold to suit current market conditions. Look for price crossovers and deviations from the calculated mean for potential entry signals. Use the upper and lower bands as dynamic support/resistance levels for setting take profit and stop-loss orders. Combining this indicator with additional trend-following or momentum-based indicators can improve signal accuracy. Adjust settings for better mean-reversion detection and risk management.

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

Adding the Indicator to the Chart:

Go to your TradingView chart.

Click on the "Indicators" button at the top.

Search for "Mean Reversion Cloud (Ornstein-Uhlenbeck)" in the indicators list.

Click on the indicator to add it to your chart.

Configuring the Indicator:

Open the indicator settings by clicking on the gear icon next to its name on the chart.

Decay Factor: Adjust the decay factor (λ) to control the responsiveness of the mean calculation. A higher value prioritizes recent data.

Autocorrelation Length: Set the autocorrelation length (θ) for calculating the speed of mean reversion. Longer lengths consider more historical data.

Threshold: Define the number of standard deviations for the upper and lower bands to determine how far price must deviate to trigger a signal.

Chart Setup:

Select the appropriate timeframe (e.g., 1-hour, daily) based on your trading strategy.

Consider using other indicators such as RSI or MACD to confirm buy and sell signals.

🞘 Understanding What to Look For on the Chart

Indicator Behavior:

Observe how the price interacts with the dynamic mean and volatility bands. The price staying within the bands suggests mean-reverting behavior, while crossing the bands signals potential entry points.

The indicator calculates overbought/oversold conditions based on deviation from the mean, highlighted by color-coded cloud areas on the chart.

Crossovers and Deviation:

Look for crossovers between the price and the mean (μ) or the bands. A bullish crossover occurs when the price crosses below the lower band, signaling a potential buying opportunity.

A bearish crossover occurs when the price crosses above the upper band, suggesting a potential sell signal.

Deviations from the mean indicate market extremes. A large deviation indicates that the price is far from the mean, suggesting a potential reversal.

Slope and Direction:

Pay attention to the slope of the mean (μ). A rising slope suggests bullish market conditions, while a declining slope signals a bearish market.

The steepness of the slope can indicate the strength of the mean-reversion trend.

🞘 Possible Entry Signals

Bullish Entry:

Crossover Entry: Enter a long position when the price crosses below the lower band with a positive deviation from the mean.

Confirmation Entry: Use additional indicators like RSI (above 50) or increasing volume to confirm the bullish signal.

Bearish Entry:

Crossover Entry: Enter a short position when the price crosses above the upper band with a negative deviation from the mean.

Confirmation Entry: Look for RSI (below 50) or decreasing volume to confirm the bearish signal.

Deviation Confirmation:

Enter trades when the deviation from the mean is significant, indicating that the price has strayed far from its expected value and is likely to revert.

🞘 Possible Take Profit Strategies

Static Take Profit Levels:

Set predefined take profit levels based on historical volatility, using the upper and lower bands as guides.

Place take profit orders near recent support/resistance levels, ensuring you're capitalizing on the mean-reversion behavior.

Trailing Stop Loss:

Use a trailing stop based on a percentage of the price deviation from the mean to lock in profits as the trend progresses.

Adjust the trailing stop dynamically along the calculated bands to protect profits as the price returns to the mean.

Deviation-Based Exits:

Exit when the deviation from the mean starts to decrease, signaling that the price is returning to its equilibrium.

🞘 Possible Stop-Loss Levels

Initial Stop Loss:

Place an initial stop loss outside the lower band (for long positions) or above the upper band (for short positions) to protect against excessive deviations.

Use a volatility-based buffer to avoid getting stopped out during normal price fluctuations.

Dynamic Stop Loss:

Move the stop loss closer to the mean as the price converges back towards equilibrium, reducing risk.

Adjust the stop loss dynamically along the bands to account for sudden market movements.

🞘 Additional Tips

Combine with Other Indicators:

Enhance your strategy by combining the Mean Reversion Cloud with momentum indicators like MACD, RSI, or Bollinger Bands to confirm market conditions.

Backtesting and Practice:

Backtest the indicator on historical data to understand how it performs in various market environments.

Practice using the indicator on a demo account before implementing it in live trading.

Market Awareness:

Keep an eye on market news and events that might cause extreme price movements. The indicator reacts to price data and might not account for news-driven events that can cause large deviations.

🔸Customize settings 🞘 Decay Factor (λ): Defines the weight assigned to recent price data in the calculation of the mean. A value closer to 1 places more emphasis on recent prices, while lower values create a smoother, more lagging mean.

🞘 Autocorrelation Length (θ): Sets the period for calculating the speed of mean reversion and volatility. Longer lengths capture more historical data, providing smoother calculations, while shorter lengths make the indicator more responsive.

🞘 Threshold (σ): Specifies the number of standard deviations used to create the upper and lower bands. Higher thresholds widen the bands, producing fewer signals, while lower thresholds tighten the bands for more frequent signals.

🞘 Max Gradient Length (γ): Determines the maximum number of consecutive bars for calculating the deviation gradient. This setting impacts the transparency of the plotted bands based on the length of deviation from the mean.

🔶 CONCLUSION

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator offers a sophisticated approach to identifying mean-reversion opportunities by applying the Ornstein-Uhlenbeck stochastic process. This dynamic indicator calculates a responsive mean using an Exponentially Weighted Moving Average (EWMA) and plots volatility-based bands to highlight overbought and oversold conditions. By incorporating advanced statistical measures like autocorrelation and standard deviation, traders can better assess market extremes and potential reversals. The indicator’s ability to adapt to price behavior makes it a versatile tool for traders focused on both short-term price deviations and longer-term mean-reversion strategies. With its unique blend of statistical rigor and visual clarity, the Mean Reversion Cloud provides an invaluable tool for understanding and capitalizing on market inefficiencies.

Meanreversal

Reversion Zone IndexThe Reversion Zone Index (RZI) is an indicator that combines the Commodity Channel Index (CCI), Choppiness Index (CI), and Bollinger Bands Percentage (BBPct) to identify mean reversion signals in the market. It is plotted as an Exponential Moving Average (EMA) smoothed oscillator with overbought and oversold zones, and mean reversion signals are represented by red and green arrows.

The three indicators are combined to benefit from their complementary aspects and create a more comprehensive view of mean reversion conditions. Here's a brief overview of each indicator's benefits:

1. Commodity Channel Index (CCI): CCI measures the current price level relative to its average over a specified period. It helps identify overbought and oversold conditions, as well as potential trend retracements. By incorporating CCI, the RZI gains insights into momentum and potential turning points.

2. Choppiness Index (CI): CI quantifies the market's choppiness or trendiness by analyzing the range between the highest high and lowest low over a specific period. It indicates whether the market is in a trending or ranging phase. CI provides valuable information about the market state, which can be useful in mean reversion analysis.

3. Bollinger Bands Percentage (BBPct): BBPct measures the current price's position relative to the Bollinger Bands. It calculates the percentage difference between the current price and the bands, identifying potential overbought or oversold conditions. BBPct helps gauge the market's deviation from its typical behavior and highlights potential reversal opportunities.

The RZI combines the three indicators by taking an average of their values and applying further calculations. It smooths the combined oscillator using an EMA to reduce noise and enhance the visibility of the trends. Smoothing with EMA provides a more responsive representation of the overall trend and helps filter out short-term fluctuations.

The overbought and oversold zones are marked on the chart as reference levels. When the combined oscillator is above the overbought zone or below the oversold zone, it suggests a potential mean reversion signal. Red and green arrows are displayed to visually indicate these mean retracement signals.

The RZI is a valuable tool for identifying mean reversion opportunities in the market. It incorporates multiple indicators, each providing unique insights into different aspects of mean reversion, such as momentum, volatility, and price positioning. Traders can use this indicator to spot potential turning points and time their trades accordingly.

Intraday Mean Reversion Money Performance indicatorThe diagram shows Money Performance when buying stocks for 10 000 at every buy signal from the Intraday Mean Reversion indicator.

The indicator is best used in combination with Intraday Mean Reversion Main Indicator

The rules for trading are: Buy on Open price if the Intraday Mean Reversion Main indicator gives a buy signal. Sell on the daily close price.

According to my knowledge it is not possible to create a PineScript strategy based on these rules, because the indicator is used on Day to Day graph. Therefore this indicator can be used to analyze Money performance of this strategy.

The lines show the performance of the Intraday Mean Reversion Strategy, based on the different levels in the strategy (from 0.5 Standard deviation to 1.1 standard deviation)

Using this indicator it is possible to find stocks that often reverse towards mean after open.

Use this strategy on stocks with high positive performance. Do not use on stocks with negative performance.

Intraday Mean Reversion MainThe Intraday Mean Reversion Indicator works well on certain stocks. It should be used for day trading stocks but need to be applied on the Day to Day timeframe.

The logic behind the indicator is that stocks that opens substantially lower than yesterdays close, very often bounces back during the day and closes higher than the open price, thus the name Intraday Mean reversal. The stock so to speak, reverses to the mean.

The indicator has 7 levels to choose from:

0.5 * standard deviation

0.6 * standard deviation

0.7 * standard deviation

0.8 * standard deviation

0.9 * standard deviation

1.0 * standard deviation

1.1 * standard deviation

The script can easily be modified to test other levels as well, but according to my experience these levels work the best.

The info box shows the performance of one of these levels, chosen by the user.

Every Yellow bar in the graph shows a buy signal. That is: The stocks open is substantially lower (0.5 - 1.1 standard deviations) than yesterdays close. This means we have a buy signal.

The Multiplier shows which multiplier is chosen, the sum shows the profit following the strategy if ONE stock is bought on every buy signal. The Ratio shows the ratio between winning and losing trades if we followed the strategy historically.

We want to find stocks that have a high ratio and a positive sum. That is More Ups than downs. A ratio over 0.5 is good, but of course we want a margin of safety so, 0.75 is a better choice but harder to find.

If we find a stock that meets our criteria then the strategy will be to buy as early as possible on the open, and sell as close as possible on the close!

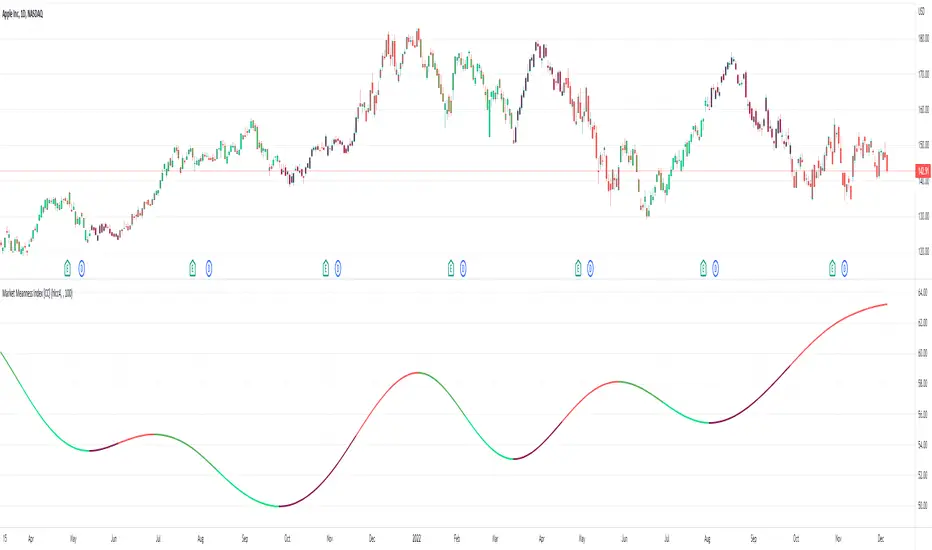

Market Meanness Index [CC]The Market Meanness Index was created by Johann Christian Lotter and I added some smoothing of my own, so feel free to try it without any smoothing to see the differences. This indicator relies on the mean reversion theory that all prices will eventually revert to the mean over a long period of time. Obviously there is more to the theory but the basic idea is if you plot a sma or other typical moving average, you will see the price moving up or below the long term moving average such as a 200 day sma but usually heads back to the average in the short term. This is a good statistical analysis used for volatility which is where this indicator comes in. Simply put, we calculate volatility based on how often a price is both above the median and above the previous price or vice versa.

A rising Market Meanness Index means that the market is becoming more volatile and that there is a high likelihood of a change in the underlying trend. A falling Market Meanness Index means that the current trend is dying and there is a high likelihood of a trend reversal. Typically I put general buy and sell signals in red or green but in this particular case, this indicator works best as a overall trend filter and you would want to place a trade when this indicator has a peak or valley. Let me know if you find a good overall buy and sell signal system of course.

I know I keep saying that I will get active again and post more indicators but life is very hectic for me. For those who have been following my updates, my twins were finally born a little over a month ago and as you can imagine, they keep me up at all hours of the day so it is hard to create new indicator scripts when I'm getting no sleep lol. I will do my best to start publishing the giant backlog of scripts I have created but in the meantime, please be patient with me. This indicator was a special request so let me know if you have any special requests of your own!

3C QFL Mean reversalWhat is QFL trading strategy?

QFL stands for Quickfingersluc, and sometimes it is referred to as the Base Strategy or Mean Reversals. Its main idea is about identifying the moment of panic selling and buying below the base level and utilizing Safety orders.

What is Base level or Support Level?

Base level or Support Level refers to the lowest price level that was reached before the moment the price started increasing again. At that level, you can notice that buyers of some cryptocurrencies make a strong reaction.

In this strategy we can also reverse the strategy and go short. But i must warn you that that is alot riskier.

QFL is meant to be used on higher TF's like 1hr, 2hr and 4hr. But this strategy also work well on lower Timeframes.

The script also simulates DCA strategy with parameters used in 3commas DCA bots for futures trading.

Experiment with parameters to find your trading setup.

Beware how large your total leveraged position is and how far can market go before you get liquidated!

Do that with the help of futures liquidation calculators you can find online!

Included:

An internal average price and profit calculating, instead of TV`s native one, which is subject to severe slippage.

A graphic interface, so levels are clearly visible and back-test analyzing made easier.

Long & Short direction of the strategy.

Table display a summary of past trades

Vertical colored lines appear when the new maximum deviation from the original price has

been reached

All the trading happens with total account capital, and all order sizes inputs are expressed in percent.

Trend Following or Mean RevertingThe strategy checks nature of the instruments. It Buys if the close is greater than yesterday's high, reverse the position if the close is lower than yesterday's low and repeat the process.

1. If it is trend following then the equity curve will be in uptrend

2. If it is mean reverting then the equity curve will be downtrend

Thanks to Rayner Teo.