Chande Kroll Trend Strategy (SPX, 1H) | PINEINDICATORSThe "Chande Kroll Stop Strategy" is designed to optimize trading on the SPX using a 1-hour timeframe. This strategy effectively combines the Chande Kroll Stop indicator with a Simple Moving Average (SMA) to create a robust method for identifying long entry and exit points. This detailed description will explain the components, rationale, and usage to ensure compliance with TradingView's guidelines and help traders understand the strategy's utility and application.

Objective

The primary goal of this strategy is to identify potential long trading opportunities in the SPX by leveraging volatility-adjusted stop levels and trend-following principles. It aims to capture upward price movements while managing risk through dynamically calculated stops.

Chande Kroll Stop Parameters:

Calculation Mode: Offers "Linear" and "Exponential" options for position size calculation. The default mode is "Exponential."

Risk Multiplier: An adjustable multiplier for risk management and position sizing, defaulting to 5.

ATR Period: Defines the period for calculating the Average True Range (ATR), with a default of 10.

ATR Multiplier: A multiplier applied to the ATR to set stop levels, defaulting to 3.

Stop Length: Period used to determine the highest high and lowest low for stop calculation, defaulting to 21.

SMA Length: Period for the Simple Moving Average, defaulting to 21.

Calculation Details:

ATR Calculation: ATR is calculated over the specified period to measure market volatility.

Chande Kroll Stop Calculation:

High Stop: The highest high over the stop length minus the ATR multiplied by the ATR multiplier.

Low Stop: The lowest low over the stop length plus the ATR multiplied by the ATR multiplier.

SMA Calculation: The 21-period SMA of the closing price is used as a trend filter.

Entry and Exit Conditions:

Long Entry: A long position is initiated when the closing price crosses over the low stop and is above the 21-period SMA. This condition ensures that the market is trending upward and that the entry is made in the direction of the prevailing trend.

Exit Long: The long position is exited when the closing price falls below the high stop, indicating potential downward movement and protecting against significant drawdowns.

Position Sizing:

The quantity of shares to trade is calculated based on the selected calculation mode (linear or exponential) and the risk multiplier. This ensures position size is adjusted dynamically based on current market conditions and user-defined risk tolerance.

Exponential Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000 * strategy.equity / strategy.initial_capital.

Linear Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000.

Execution:

When the long entry condition is met, the strategy triggers a buy signal, and a long position is entered with the calculated quantity. An alert is generated to notify the trader.

When the exit condition is met, the strategy closes the position and triggers a sell signal, accompanied by an alert.

Plotting:

Buy Signals: Indicated with an upward triangle below the bar.

Sell Signals: Indicated with a downward triangle above the bar.

Application

This strategy is particularly effective for trading the SPX on a 1-hour timeframe, capitalizing on price movements by adjusting stop levels dynamically based on market volatility and trend direction.

Default Setup

Initial Capital: $1,000

Risk Multiplier: 5

ATR Period: 10

ATR Multiplier: 3

Stop Length: 21

SMA Length: 21

Commission: 0.01

Slippage: 3 Ticks

Backtesting Results

Backtesting indicates that the "Chande Kroll Stop Strategy" performs optimally on the SPX when applied to the 1-hour timeframe. The strategy's dynamic adjustment of stop levels helps manage risk effectively while capturing significant upward price movements. Backtesting was conducted with a realistic initial capital of $1,000, and commissions and slippage were included to ensure the results are not misleading.

Risk Management

The strategy incorporates risk management through dynamically calculated stop levels based on the ATR and a user-defined risk multiplier. This approach ensures that position sizes are adjusted according to market volatility, helping to mitigate potential losses. Trades are sized to risk a sustainable amount of equity, adhering to the guideline of risking no more than 5-10% per trade.

Usage Notes

Customization: Users can adjust the ATR period, ATR multiplier, stop length, and SMA length to better suit their trading style and risk tolerance.

Alerts: The strategy includes alerts for buy and sell signals to keep traders informed of potential entry and exit points.

Pyramiding: Although possible, the strategy yields the best results without pyramiding.

Justification of Components

The Chande Kroll Stop indicator and the 21-period SMA are combined to provide a robust framework for identifying long trading opportunities in trending markets. Here is why they work well together:

Chande Kroll Stop Indicator: This indicator provides dynamic stop levels that adapt to market volatility, allowing traders to set logical stop-loss levels that account for current price movements. It is particularly useful in volatile markets where fixed stops can be easily hit by random price fluctuations. By using the ATR, the stop levels adjust based on recent market activity, ensuring they remain relevant in varying market conditions.

21-Period SMA: The 21-period SMA acts as a trend filter to ensure trades are taken in the direction of the prevailing market trend. By requiring the closing price to be above the SMA for long entries, the strategy aligns itself with the broader market trend, reducing the risk of entering trades against the overall market direction. This helps to avoid false signals and ensures that the trades are in line with the dominant market movement.

Combining these two components creates a balanced approach that captures trending price movements while protecting against significant drawdowns through adaptive stop levels. The Chande Kroll Stop ensures that the stops are placed at levels that reflect current volatility, while the SMA filter ensures that trades are only taken when the market is trending in the desired direction.

Concepts Underlying Calculations

ATR (Average True Range): Used to measure market volatility, which informs the stop levels.

SMA (Simple Moving Average): Used to filter trades, ensuring positions are taken in the direction of the trend.

Chande Kroll Stop: Combines high and low price levels with ATR to create dynamic stop levels that adapt to market conditions.

Risk Disclaimer

Trading involves substantial risk, and most day traders incur losses. The "Chande Kroll Stop Strategy" is provided for informational and educational purposes only. Past performance is not indicative of future results. Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and risk tolerance.

SPX (S&P 500 Index)

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

Balance of Power Heikin Ashi Investing Strategy Balance of Power Heikin Ashi Investing Strategy

This is a swing strategy designed for investment help.

Its made around the Balace of Power indicator, but has been adapted on using the Monthly Heikin Ashi candle from the SPY asset in order to be used with correlation for US Stock/ETF/Index Markets.

The BOP acts as an oscilallator showing the power of a bull trend when its positive and a bearish trend when its in negative. At the same time we can spot reversals, based on the percentiles ( 99/1)

The rules for entry :

For long : The 99 percentile is ascending, and we are either in a positive value (>0), or we crossed the bottom place ( -0.35)

For short : the 99 and 1 percentile are descending, and we are either in a negative value(<0), or we crossed down the top place ( 0.6)

If you have any questions please let me know !

Stock Gaps SPY Correlation StrategyThis is daytrade stock strategy, designed to take the best out of the daily gaps that are forming between the close of previous day and opening of present day.

At the same time its logic has been adapted for SPY chart, in order to use correlation with the other stocks/assets/ etf which are linked with SP500 movement.

Lastly it has been added 2 new confirmation logics, based on the USI: advance/decline chart and percentage above vwap among all US stocks.

The rules for entry are simple :

We are at the opening daily candle, we have a long/short gap based on where the opening is happening and at the same time we are checking to see that the current different between the current difference between low and previous high (or viceversa) is higher than an established parameter(minimal deviation )

For exit, we exit based on time/clock parameter, in this case by default I selected 1h and half before close of the US session.

For testing purposes I have used 10% of the available capital, with a 0.0035$ comission per each share bought ( IBKR comissions)

If there are any questions, please let me know either here or in private !

VWAP Push StrategyThis strategy is unfortunately not finished yet.

A pretty simple strategy. If price broke through VWAP and had three consecutive candles following the breakthroughs trend, the high of the third candle will be drawn. If this happened after a crossover of the vwap and price breaks through the high of the third candle, strategy will go long. Short will be the same after crossing under the vwap. A long or short will be closed after crossing the vwap in the opposite direction, so the vwap is kind of a trailing stop.

Unfortunately, I could not manage to stop the script from entering multiple times into one drawn high or low. Of course, if a high was crossed the script should wait for a new formed high before entering a new long. If someone would find a solution to this, it would be great, because I think it is a nice strategy .

Should work great scalping 5min charts (when scripting, I used the SPX for reference).

[Pt] TICK Supertrend Strategy, 5 minBackground:

It is well known that the indices such as SPY and QQQ follow/represent market sentiment. The TICK index literally represents the market sentiment as it compares the number of stocks that are rising and falling on the NYSE. By default, the TICK index is a short term indicator. Therefore it isn't reliable for swing trading or long term strategies. However, it is perfect for scalping.

Although TICK is well known, many does not know how to use it effectively. As part of the background mechanism of this script, I’ve divided TICK into 5 major zones based on the close of each candle: Overbought (neutral with bearish bias), Bullish, Neutral, Bearish, and Oversold (neutral with bullish bias). Along with the use of Heikin Ashi technique, RSI, moving averages and candle analysis, this strategy aims to provide accurate representation of market sentiment and profitable entry and exit points. *** At the time of publication, this strategy has proved to be consistently profitable. HOWEVER, this DOES NOT guarantee future profitability. So use at your own risk! ***

What is it showing?

This strategy is an intraday scalping strategy that uses TICK data to predict market directions for optimal entry and exit points. It is displayed similarly to the famous Supertrend indicator, which is one of the most common ATR based trailing stop indicators, so visually it is easy to read. This strategy is suitable for trading indices such as SPX , SPY , SPX500USD , QQQ , DJI and any other tickers that have high positive correlation with TICK.

Script is proprietary, but as mentioned it incorporates the following elements with additional candlestick analysis, pattern recognition, stop-loss and profit taking strategy:

- NYSE TICK data

- Heikin Ashi candle technique

- ATR

- RSI

- Moving Averages

Bullish trend is determined by a confluence of said indicators and analyses, and is displayed as a green line under the price action. The distance is defined by an adjustable value that is based on a percentage of the previous daily ATR value. When a long order is in play, that line also acts as the stop-loss level. Bearish trend is the opposite and is displayed in red, by default.

What's unique?

Detecting a ranging market structure and avoiding overtrading in a choppy market has always proven to be difficult, even for the most professional traders. This strategy has built-in “choppiness” and volatility filtering scripts that attempts to help reduce the number of false entries. These elements are what makes this strategy unique and different from other indictors mashup strategies.

In addition, this strategy takes previous trades into account and “learn” from past trades when determining the optimal stop-loss level to maximize profitability. This allows this strategy to better adapts to changing and evolving market conditions.

Strategy statistics

All parameters are designed for 5min time frame.

At the time of publication, this strategy has proved to be consistently profitable through limited back testing data.

Initial capital = $10000

Pyramiding = 1

Slippage = 3 ticks to account for spread

Default leverage shown = 9x

Quantity per trade = 100% of account

Back testing period at time of publication = Apr 11, 2022 - July 22, 2022

Trading Session = 1000 - 1530 Mon-Fri

Timeframe = 5 min

Gain = 1338.48%

Total trades = 253

% Profitable = 45.85%

Profit Factor = 2.506

Max Drawdown = 19.36%

Extras

This release includes default AutoView alerts for trading SPX500USD on Oanda. It includes both long and short order entry alerts, and trailing stop-loss alerts.

Please DM for free trial.

Swing Trading SPX CorrelationThis is a long timeframe script designed to benefit from the correlation with the Percentage of stocks Above 200 moving average from SPX

At the same time with this percentage we are creating a weighted moving average to smooth its accuracy.

The rules are simple :

If the moving average is increasing its a long signal/short exit

If the moving average is decreased its a short signal/long exit.

Curently the strategy has been adapted for long only entries.

If you have any questions let me know !

Infiten Slope StrategyThis model is an index fund trading model, which uses moving averages and price percentage oscillators to minimize downside exposure.

Improved Bollinger Swing Strategy Stock NasdaqThis is an improved bollinger band strategy adapted to Nasdaq Index/Stocks.

The new update include a multiple logic calculation BB adapted for long and short, together with a risk management using movement in %.

Rules for entry

For long we have a crossover between the close and the lower band from the bb

For long we have a crossover between the close and the upper band from the bb

Rules for exit

We exit when we either find a reverse condition, or if we hit the take profit/stop loss levels.

If you have any questions, let me know !

Stock trending strategy This is a long only strategy designed maily for stock markets and futures. In general it works best with 1h, however it can be optimized with other timeframes as well.

Components:

VWAP

MACD histogram

EMA 9

Rules for entry

Long :

For VWAP: close is above the vwap daily

EMA: close is above the moving average

MACD histogram is above 0

Short:

For VWAP: close is belowthe vwap daily

EMA: close is below the moving average

MACD histogram is below 0

Rules for exit

This strategy does not have any risk management inside. Instead it exits whenver it receives an opposite signal form the original one used for entry.

If you have any questions let me know !

Ichimoku with MACD/ CMF/ TSIThis is a very powerful trend strategy designed for markets such as stocks market , stock index and crypto.

For time frames I found out that 1h seems to do the trick.

Components:

Ichimoku full pack

MACD histogram

CMF oscillator

TSI oscillator

Rules for entry

Long :

For Ichimoku:Tenkan part of cloud is bigger than kijun, Chikou is above 0 , close of a candle is above the Senkou

MACD histogram is above 0

CMF oscillator is positive and bigger than 0.1

TSI oscillator is above 0

Short:

For Ichimoku:Tenkan part of cloud is smaller than kijun, Chikou is below 0 , close of a candle is belowthe Senkou

MACD histogram is below 0

CMF oscillator is negative and below -0.1

TSI oscillator is below 0

Rules for exit

This strategy does not have any risk management inside. Instead it exits whenver it receives an opposite signal form the original one used for entry.

If you have any questions let me know !

XPloRR S&P500 Stock Market Crash Detection Strategy v2XPloRR S&P500 Stock Market Crash Detection Strategy v2

Long-Term Trailing-Stop strategy detecting S&P500 Stock Market Crashes/Corrections and showing Volatility as warning signal for upcoming crashes

Detecting or avoiding stock market crashes seems to be the 'Holy Grail' of strategies.

Since none of the strategies that I tested can beat the long term Buy&Hold strategy, the purpose was to detect a stock market crash on the S&P500 and step out in time to minimize losses and beat the Buy&Hold strategy. So beat the Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

With the default parameters the strategy generates 10262% profit (starting at 01/01/1962 until release date), with 10 closed trades, 100% profitable, while the Buy&Hold strategy only generates 3633% profit, so this strategy beats the Buy&Hold strategy by 2.82 times !

Also the strategy detects all major S&P500 stock market crashes and corrections since 1962 depending on the Trailing Stop Smoothness parameter, and steps out in time to cut losses and steps in again after the bottom has been reached. The 5 major crashes/corrections of 1987, 1990, 2001, 2008 and 2010 were successfully detected with the default parameters.

The script was first released on November 03 2019 and detected the Corona Crash on March 04 2020 with a Volatility crash-alert and a Sell crash-alert.

I have also created an Alerter Study Script based on the engine of this script, which generates Buy, Sell and Volatility signals.

If you are interested in this Alerter version script, please drop me a mail.

The script shows a lot of graphical information:

the Close value is shown in light-green. When the Close value is temporarily lower than the Buy value, the Close value is shown in light-red. This way it is possible to evaluate the virtual losses during the current trade.

the Trailing Stop value is shown in dark-green. When the Sell value is lower than the Buy value, the last color of the trade will be red (best viewed when zoomed)

the EMA and SMA values for both Buy and Sell signals are shown as colored graphs

the Buy signals are labeled in blue and the Sell signals are labeled in purple

the Volatility is shown below in green and red. The Alert Threshold (red) is default set to 2 (see Volatility Threshold parameter below)

How to use this Strategy?

Select the SPX (S&P500) graph and add this script to the graph.

Look in the strategy tester overview to optimize the values Percent Profitable and Net Profit (using the strategy settings icon, you can increase/decrease the parameters), then keep using these parameters for future Buy/Sell signals on the S&P500.

More trades don't necessarily generate more overall profit. It is important to detect only the major crashes and avoid closing trades on the smaller corrections. Bearing the smaller corrections generates a higher profit.

Watch out for the Volatility Alerts generated at the bottom (red). The Threshold can by changed by the Volatility Threshold parameter (default=2% ATR). In almost all crashes/corrections there is an alert ahead of the crash.

Although the signal doesn't predict the exact timing of the crash/correction, it is a clear warning signal that bearish times are ahead!

The correction in December 2018 was not a major crash but there was already a red Volatility warning alert. If the Volatility Alert repeats the next weeks/months, chances are higher that a bigger crash or correction is near. As can be seen in the graphic, the deeper the crash is, the higher and wider the red Volatility signal goes. So keep an eye on the red flag!

Here are the parameters:

Fast MA Buy: buy trigger when Fast MA Buy crosses over the Slow MA Buy value (use values between 10-20)

Slow MA Buy: buy trigger when Fast MA Buy crosses over the Slow MA Buy value (use values between 21-50)

Minimum Buy Strength: minimum upward trend value of the Fast MA Buy value (directional coefficient)(use values between 10-100)

Fast MA Sell: sell trigger when Fast MA Sell crosses under the Slow MA Sell value (use values between 10-20)

Slow MA Sell: sell trigger when Fast MA Sell crosses under the Slow MA Sell value (use values between 21-50)

Minimum Sell Strength: minimum downward trend value of the Fast MA Sell value (directional coefficient)(use values between 10-100)

Trailing Stop ATR: trailing stop % distance from the smoothed Close value (use values between 2-20)

Trailing Stop Smoothness: MA value for smoothing out the Trailing Stop close value

Buy On Start Date: force Buy on start date even without Buy signal (default: true)

Sell On End Date: force Sell on end date even without Sell signal (default: true)

Volatility EMA Period: MA value of the Volatility value (default 15)

Volatility Threshold: Threshold value to change volatility graph to red (default 2)

Volatility Graph Scaler: Scaling of the volatility graph (default 5)

Important : optimizing and using these parameters is no guarantee for future winning trades!

SPY - SPX - S&P --- DAILY MODELThis model is optimized for SPY on a daily time-frame.

Even though it is still profitable (Profit factor > 1) on other time-frames, such as 1h or weekly, I strongly advise you to NOT consider these signals.

You might also get positive returns on other assets, and time-frames, and I also strongly advise you to NOT consider them for your trades. For example:

AAPL-1h

GOOGL-D-W

TSLA-D-W

PYPL-D

INTC-W

MSFT-D-W

FDN-D-W

And so on …

This model is an optimization (parameters tuning) of a meta-model (generic model) for the SPY. It is mainly based on a conjunction of price & volume personal indicators for both entry and exit signals.

The relative portability of the model to other assets and time-frames, coupled with a "Development set -> Validation set" approach, confers it a stronger reliability, and a better warranty of not being « over-optimized ». The meta-model has also served for other model buildings, about 100 as of today.

Be advised that this model applied to real data will get much lower profit factors. During high-volatility periods (such as current times), the model might also be less accurate, as "News streams", more than "prices and volumes", make the market.

As always, this model is for an educational purpose only, and should never be considered as a single decision tool. So, study it, and make sure your decisions are still your own choice.

TradersAI - Test 3**** This is a TEST script only! Do NOT use on real money accounts! *****

***** Intended to be used in testing by invited_only members *****

***** If you want to participate in our testing using your paper trading account(s), send me a private message *****

TradersAI Test Script 1This is a script to test trading flows from an invite only script to one's trading view chart and then possibly to one of the connected brokers.

**** Do NOT use on real funds - this randomly triggers trades. Do NOT use on real money accounts. ******

TradersAI_UTBotCREDITS to @HPotter for the orginal code.

CREDITS to @Yo_adriiiiaan for recently publishing the UT Bot study based on the original code -

I just added some simple code to turn it into a strategy. Now, anyone can simply add the strategy to their chart to see the backtesting results!

While @Yo_adriiiiaan mentions it works best on a 4-hour timeframe or above, I am happy to share that this seems to be working on a 15-minute chart on e-mini S&P 500 Index (using the KeyValue setting at 10)! You can play around with the different settings, and may be you might discover even better settings.

Hope this helps. Btw, if any of you play with different settings and discover great settings for a specific instrument, please share them with the community here - it will be rewarded back multiple times!

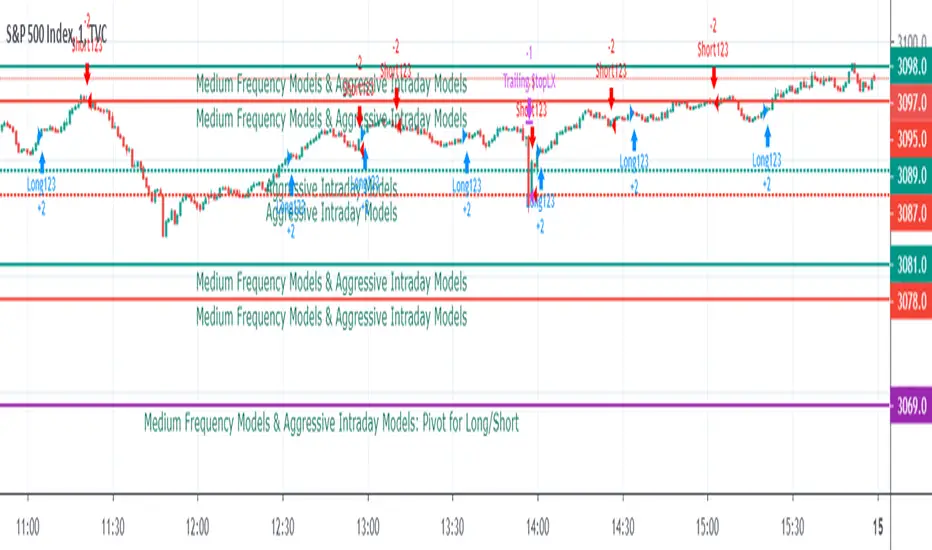

A.I.Driven TradersAI Model Trades for 20190612The entry and exit levels here are NOT derived from any specific indicator but are coming from our A.I. driven proprietary models.

This is an attempt at exploring the trading community here at TradingView and sharing our daily trading plans published at our site with the community here in the form a Pine Script - just starting and learning this platform. Please help point out any obvious errors or gotchas committed in the scripts. Thanks and have a great trading day!

**** The Trading Plan Published for today ****

>>>> Medium-Frequency Models: <<<<< For today, Wednesday 06/12, our medium-frequency models indicate using the 2895 as a pivot point - opening a long on a break above 2895, and opening a short on a break below 2895 (wait for a close on at least a five minute chart to determine the break), both sides with a 9-point trailing stop.

Note: For the trades to trigger, the breaks should occur during the regular session hours starting at 9:30am ET. By design, these models do NOT open any new positions after 3:45pm. Only one open position at any given time.

>>>>> Aggressive Intraday Models: <<<<< For today, Wednesday 06/12, our aggressive intraday models indicate going long on a break above 2892 or 2875 with an 6-point trailing stop, and going short on a break below 2887 or 2878 with an 8-point trailing stop.

Note: For the trades to trigger, the breaks should occur during regular session hours starting at 9:30am ET. Due to the intraday nature of these aggressive models, they indicate closing any open trades at 3:55pm and remaining flat into the session close. No opening of new positions after 3:45pm. Only one open position at any given time.

EMINI OPTIONS HighAccuracy Signal SystemThe SPX Options signal system is based on the Market Internals which ultimately drills down to its underlying stocks and their Movement

So a signal system is created which takes the key market Internals rather than just price alone.

In trading OPTIONS, your Direction earns you money along with Option Writing.

PARAMETERS TAKEN INTO ACCOUNT

1. Key Sector Stocks

2. NYSE TICK INDEX

3. UPVOL and DVOL

4. VIX Bands With Applied Gaussian Methodology

"PRICE OF SPX IS NOT TAKEN IN TO ACCOUNT IN THIS SIGNAL SYSTEM"

Understanding the signal system

1. Do not combine this signal system with any other indicators.

2. Greater than 75% success rate for 15 points in SPX .

Recommended time frames: 1 hour are highly recommended time frames.

But a risky trader can trade with 15 Mins because Market Internals support lower time frames. But trade cautiously and read the disclaimer carefully.

The signal system does not carry any recommendations and the signals are generated mathematically using the underlying MARKET INTERNALS LOGIC

PPSignal System Algorithm Introduction

System Algorithm based on historical price probabilities and volumes. We recommend use financial stock, bond, crypts, indices, futures and Forex market (GBPUSD, EURUSD, USDJPY, USDCAD, AUDUSD, USOIL, XAUUSD, SOYUSD, DXY, SPY, SP1!, bitcoin) with defined trends above 50 or 100 and 200 simple moving averages idem if you want trade downtrend financial assets.

Use projections and retracements Fibonacci, MACD and RSI or Stoch oscillator and figures charters Head and shoulder, triangles and double bottom, double top, etc.

This system will notify you of the probability of success. The profit will be defined for yourself and according to your investor profile.

There are stocks and other assets with high returns but the system does not know exactly. Check in the Strategy tester section and then net profit.

We have other tools that support to PPsignal system, we will publish them shortly.

Define system parameters

As it is a system that is based on past data we recommend using the most historical data weekly (W) but you an use day historical data or 3 o 2 hs.

Candle color: you can choose if you want a trend color for candles or not, in the chart propieties menu detach the border option.

PPsignal it's a very simple system with which you will have a great support when it is a good time for enter in the marker and out.

we await your comments.

Eng. Oscar Alejandro Peruchena

Quants Mathematical and Market Analyst

Bollinger + RSI, Double Strategy Long-Only (by ChartArt) v1.2This strategy uses the RSI indicator together with the Bollinger Bands to go long when the price is below the lower Bollinger Band (and to close the long trade when this value is above the upper Bollinger band).

This simple strategy only places a long, when both the RSI and the Bollinger Bands indicators are at the same time in a oversold condition.

In this new version 1.2 the strategy was simplified even more than before by going long-only, which made the strategy more successful in backtesting than the previous version (that older version also opened short trades).

This strategy does not repaint and was updated to PineScript version 3.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

P.S. For advanced users: If you want also be able to short with the same strategy approach, then please use my older version 1.1:

S&P 500 Long Only Investment Strategy, Achernar (by ChartArt)Here is my strategy with the working title "Achernar", which works best with the published default setting on the 'CBOE' 'S&P 500' daily chart. The strategy is intended for investments in long-term time-frames (the current average of the trades is a holding period of over 1000 days). The setting allows to use the 'CBOE' as price source (default) or the Tradingview TVC index, which uses a 'CFD' of the 'S&P 500' as price source. Please beware that there is a typo: This strategy does not go short, it closes the long trades and goes into cash instead, therefore this is a long only strategy.

If you don't want to lose all your money due to some random strategy you found on the Internet, here is a warning:

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

P.S. The published script does not show the other trade entries on the screenshot above. Here is how the strategy looks like on the chart:

SPY Master v1.0This is a simple swing trading algorithm that uses a fast RSI-EMA to trigger buy/cover signals and a slow RSI-EMA to trigger sell/short signals for SPY, an xchange-traded fund for the S&P 500.

The idea behind this strategy follows the premise that most profitable momentum trades usually occur during periods when price is trending up or down. Periods of flat price actions are usually where most unprofitable trades occur. Because we cannot predict exactly when trending periods will occur, the algorithm basically bets money on all trade opportunities during all market conditions. Despite an accuracy rate of only 40%, the algorithm's asymmetric risk/reward profile allows the average winner to be 2x the average loser. The end result is a positive (profitable) net payout.

TRADING RULES:

Buy/Cover = EMA3(RSI2) cross> 50

Sell/Short = EMA5(RSI2) cross< 50

BACKTEST SETTINGS:

- Period = March 2011 - Present

- Initial capital = $10,000

- Dividends excluded

- Trading costs excluded

PERFORMANCE COMPARISON:

There are 657 trades, which means 1,314 orders. Assuming each order costs $2 (what I pay for at Interactive Brokers), total trading costs should be $2,628.

-SPY (buy & hold) = 132.73 ---> 193.22 = +45.57% (dividends excluded)

-SPY Master v1.0 = $12,649 - $2,628 = $10,021 = +100.21%

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.