ARIMA Indicator with Optional SmoothingOverview

The ARIMA (AutoRegressive Integrated Moving Average) Indicator is a powerful tool used to forecast future price movements by combining differencing, autoregressive, and moving average components. This indicator is designed to help traders identify trends and potential reversal points by analyzing the historical price data.

Key Features

AutoRegressive Component (AR): Utilizes past values to predict future prices.

Moving Average Component (MA): Averages past price differences to smooth out noise.

Differencing: Reduces non-stationarity in the time series data.

Optional Smoothing: Applies EMA to the ARIMA output for a smoother signal.

Customizable Parameters: Allows users to adjust AR and MA orders, differencing periods, and smoothing lengths.

Concepts Underlying the Calculations

Differencing: Subtracts previous prices from current prices to remove trends and seasonality, making the data stationary.

AutoRegressive Component (AR): Predicts future prices based on a linear combination of past values.

Moving Average Component (MA): Uses past forecast errors to refine future predictions.

Exponential Moving Average (EMA): Applies more weight to recent prices, providing a smoother and more responsive signal.

How It Works

The ARIMA Indicator first calculates the differenced series to achieve stationarity. Then, it computes the simple moving average (SMA) of this differenced series. The indicator uses the AR and MA components to adjust the SMA, creating an approximation of the ARIMA model. Finally, an optional smoothing step using EMA can be applied to the ARIMA approximation to produce a smoother signal.

How Traders Can Use It

Traders can use the ARIMA Indicator to:

Identify Trends: Detect emerging trends by observing the direction of the ARIMA line.

Spot Reversals: Look for divergences between the ARIMA line and the price to identify potential reversal points.

Generate Trading Signals: Use crossovers between the ARIMA line and the price to generate buy or sell signals.

Filter Noise: Enable the optional smoothing to filter out market noise and focus on significant price movements.

Example Usage Instructions

Add the ARIMA Indicator to your chart.

Adjust the input parameters to suit your trading strategy:

Set the SMA Length (e.g., 14).

Choose the Differencing Period (e.g., 1).

Define the AR Order (p) and MA Order (q) (e.g., 1).

Configure the Smoothing Length if smoothing is desired (e.g., 5).

Enable or disable smoothing as needed.

Observe the ARIMA line (blue) and compare it to the price chart.

Use the ARIMA line to identify trends and potential reversals.

Implement trading decisions based on the ARIMA line’s behavior relative to the price.

Timeseries

TimeSeriesRecurrencePlotLibrary "TimeSeriesRecurrencePlot"

In descriptive statistics and chaos theory, a recurrence plot (RP) is a plot showing, for each moment i i in time, the times at which the state of a dynamical system returns to the previous state at `i`, i.e., when the phase space trajectory visits roughly the same area in the phase space as at time `j`.

```

A recurrence plot (RP) is a graphical representation used in the analysis of time series data and dynamical systems. It visualizes recurring states or events over time by transforming the original time series into a binary matrix, where each element represents whether two consecutive points are above or below a specified threshold. The resulting Recurrence Plot Matrix reveals patterns, structures, and correlations within the data while providing insights into underlying mechanisms of complex systems.

```

~starling7b

___

Reference:

en.wikipedia.org

github.com

github.com

github.com

github.com

juliadynamics.github.io

distance_matrix(series1, series2, max_freq, norm)

Generate distance matrix between two series.

Parameters:

series1 (float) : Source series 1.

series2 (float) : Source series 2.

max_freq (int) : Maximum frequency to inpect or the size of the generated matrix.

norm (string) : Norm of the distance metric, default=`euclidean`, options=`euclidean`, `manhattan`, `max`.

Returns: Matrix with distance values.

method normalize_distance(M)

Normalizes a matrix within its Min-Max range.

Namespace types: matrix

Parameters:

M (matrix) : Source matrix.

Returns: Normalized matrix.

method threshold(M, threshold)

Updates the matrix with the condition `M(i,j) > threshold ? 1 : 0`.

Namespace types: matrix

Parameters:

M (matrix) : Source matrix.

threshold (float)

Returns: Cross matrix.

rolling_window(a, b, sample_size)

An experimental alternative method to plot a recurrence_plot.

Parameters:

a (array) : Array with data.

b (array) : Array with data.

sample_size (int)

Returns: Recurrence_plot matrix.

TimeSeriesGrammianAngularFieldLibrary "TimeSeriesGrammianAngularField"

provides Grammian angular field and associated utility functions.

___

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

www.researchgate.net

method normalize(data, a, b)

Normalize the series to a optional range, usualy within `(-1, 1)` or `(0, 1)`.

Namespace types: array

Parameters:

data (array) : Sample data to normalize.

a (float) : Minimum target range value, `default=-1.0`.

b (float) : Minimum target range value, `default= 1.0`.

Returns: Normalized array within new range.

___

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

normalize_series(source, length, a, b)

Normalize the series to a optional range, usualy within `(-1, 1)` or `(0, 1)`.\

*Note that this may provide a different result than the array version due to rolling range*.

Parameters:

source (float) : Series to normalize.

length (int) : Number of bars to sample the range.

a (float) : Minimum target range value, `default=-1.0`.

b (float) : Minimum target range value, `default= 1.0`.

Returns: Normalized series within new range.

method polar(data)

Turns a normalized sample array into polar coordinates.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Converted array into polar coordinates.

polar_series(source)

Turns a normalized series into polar coordinates.

Parameters:

source (float) : Source series.

Returns: Converted series into polar coordinates.

method gasf(data)

Gramian Angular Summation Field *`GASF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GASF`* values.

method gasf_id(data)

Trig. identity of Gramian Angular Summation Field *`GASF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GASF`* values.

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

method gadf(data)

Gramian Angular Difference Field *`GADF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GADF`* values.

method gadf_id(data)

Trig. identity of Gramian Angular Difference Field *`GADF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GADF`* values.

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

[Max] Power lag analysis An indicator that is a parametric lag power filter.

I'm starting Time Series Analysis by Hamilton James Douglas, to try to find some fun ideas to test and upgrade my skills on that subject and share them when it produce something that can be useful.

The idea behind that indicator, it's to only get the shape of the biggest movement in percent.

To solve that problem, I iterate about the rate of change of about 15 intervals and I apply a bigger power to the intervals that get bigger.

Why ? If the price is ranging, the indicator will show only the spics, but if the price breakout of the range, each new close that are longer from the price will have a better impact on the indicator and the last ones will be neglected.

I've try to use some parametric lag indicators on top of that indicator but he result is not good enough for me, it can't be used for trade directly but it can be an approach.

If you have upgrade ideas or recommendations on that indicator, I will be please to hear them.

Have fun with the script.

Have a great day !

Max

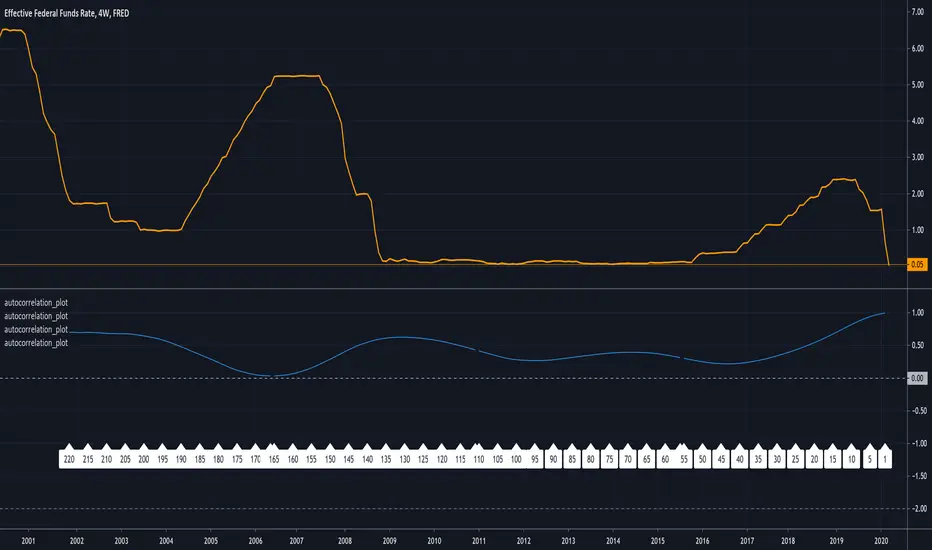

Autocorrelation PlotA tool to plot auto correlation of time series, this is useful in identifying periodicity in a time series or signal.

Due to the limits of Pine Script you'll need to add it multiple times if you want autocorrelation beyond 55 periods. I have added it 4 times here for 220 periods.

For more information on Autocorrelation see: en.wikipedia.org

Note: There are 1 bar gaps every 55 because I wanted the labels to remain every 5, but you don't have to have gaps....

TimeSync by KingThies TimeSync by Kingthies

Written in Pine v4

Applies one function that was published in the Tradingview Pinescript Manual

The Motivation behind this script - Time is 50% of your chart. Many ignore it entirely. This should help give an idea on how to read it and incorporate it in their analysis.

TimeSync by KingThies takes a simple concept and turns it into a visual tracking system of when timeframes of significant impact, all close at the same time.

By utilizing several high time-frames, we see overlaps in periods and more significant events occurring when multiple periods close at once.

The TFs included are 3D,1W,2W and 1M. When users use the timeframes above intraday, the resolution for these HTF's is shown. When using the LTFs, anything lower than 1D/is intraday, the user sees a similar concept but comprised of the 4H, 6H,8H and 10H charts.

Users can adjust the settings to show the HTFs in sync AND also factor in if the event was on a business quarter or new year, which adds more significance to the occurrence.

By seeing when these periods end in sync, we can assume more volatility is present in a given market, presenting various opportunities for traders to take advantage of a given situation.

Apologies in advance for any questions that come up - I will do my best to reply or respond here on Tradingview.com.

Additional Resources for this topic can be found in my account signature, located at the bottom of this post.