DMI + HMA - No Risk ManagementDMI (Directional Movement Index) and HMA (Hull Moving Average)

The DMI and HMA make a great combination, The DMI will gauge the market direction, while the HMA will add confirmation to the trend strength.

What is the DMI?

The DMI is an indicator that was developed by J. Welles Wilder in 1978. The Indicator was designed to identify in which direction the price is moving. This is done by comparing previous highs and lows and drawing 2 lines.

1. A Positive movement line

2. A Negative movement line

A third line can be added, which would be known as the ADX line or Average Directional Index. This can also be used to gauge the strength in which direction the market is moving.

When the Positive movement line (DI+) is above the Negative movement line (DI-) there is more upward pressure. Ofcourse visa versa, when the DI- is above the DI+ that would indicate more downwards pressure.

Want to know more about HMA? Check out one of our other published scripts

What is this strategy doing?

We are first waiting for the DMI to cross in our favoured direction, after that, we wait for the HMA to signal the entry. Without both conditions being true, no trade will be made.

Long Entries

1. DI+ crosses above DI-

2. HMA line 1 is above HMA line 2

Short Entries

1. DI- Crosses above DI+

2. HMA line 1 is below HMA lilne 2

Its as simple as that.

Conclusion

While this strategy does have its downsides, that can be reduced by adding some risk manegment into the script. In general the trade profitability is above average, And the max drawdown is at a minimum.

The settings have been optimised to suite BTCUSDT PERP markets. Though with small adjustments it can be used on many assets!

Tuned

Hull Crossover Strategy no TP or SLWhat is it?

A simple yet effective strategy ran on the 30m chart.

This is a basic idea that can be expanded on using different indicator to either add signals or filter out certain bad signals!

The strategy consists of 1 fast moving average and 1 slow moving average.

Both of these moving averages are the Hull Moving Average

What is the Hull Moving Average?

The Hull Moving Average ( HMA ) is a directional trend indicator.

It captures the current market conditions and uses recent price action to determine if conditions are bullish or bearish relative to historical data.

The Hull is different from traditional trend indicators like the EMA and the SMA .

It is designed to reduce the lag often associated with other MAs by providing a faster signal on a smoother visual plane.

How it works?

When the fast HMA crosses over the slow HMA , we initiate a long signal, and

when the fast HMA crosses under the slow HMA , we initiate a short signal.

Conclusion

The power of simplicity is what makes this such a great core to use to build onto making something even better!

The results were optimised to suit the most common market conditions seen today.

******** Not financial advice! ********

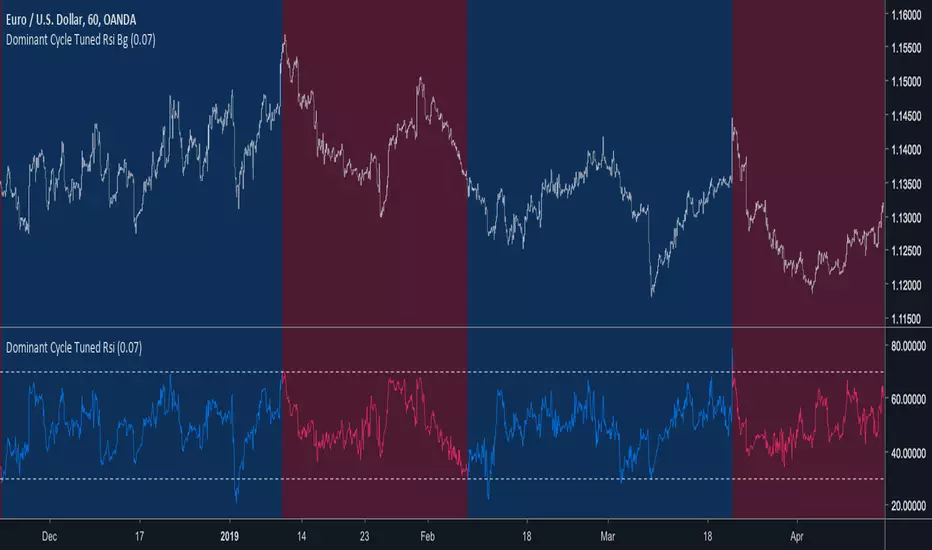

Dominant Cycle Tuned RsiIntroduction

Adaptive technical indicators are importants in a non stationary market, the ability to adapt to a situation can boost the efficiency of your strategy. A lot of methods have been proposed to make technical indicators "smarters" , from the use of variable smoothing constant for exponential smoothing to artificial intelligence.

The dominant cycle tuned rsi depend on the dominant cycle period of the market, such method allow the rsi to return accurate peaks and valleys levels. This indicator is an estimation of the cycle finder tuned rsi proposed by Lars von Thienen published in Decoding the Hidden Market Rhythm/Fine-tuning technical indicators using the dominant market vibration/2010 using the cycle measurement method described by John F.Ehlers in Cybernetic Analysis for Stocks and Futures .

The following section is for information purpose only, it can be technical so you can skip directly to the The Indicator section.

Frequency Estimation and Maximum Entropy Spectral Analysis

“Looks like rain,” said Tom precipitously.

Tom would have been a great weather forecaster, but market patterns are more complex than weather ones. The ability to measure dominant cycles in a complex signal is hard, also a method able to estimate it really fast add even more challenge to the task. First lets talk about the term dominant cycle , signals can be decomposed in a sum of various sine waves of different frequencies and amplitudes, the dominant cycle is considered to be the frequency of the sine wave with the highest amplitude. In general the highest frequencies are those who form the trend (often called fundamentals) , so detrending is used to eliminate those frequencies in order to keep only mid/mid - highs ones.

A lot of methods have been introduced but not that many target market price, Lars von Thienen proposed a method relying on the following processing chain :

Lars von Thienen Method = Input -> Filtering and Detrending -> Discrete Fourier Transform of the result -> Selection using Bartels statistical test -> Output

Thienen said that his method is better than the one proposed by Elhers. The method from Elhers called MESA was originally developed to interpret seismographic information. This method in short involve the estimation of the phase using low amount of information which divided by 360 return the frequency. At first sight there are no relations with the Maximum entropy spectral estimation proposed by Burg J.P. (1967). Maximum Entropy Spectral Analysis. Proceedings of 37th Meeting, Society of Exploration Geophysics, Oklahoma City.

You may also notice that these methods are plotted in the time domain where more classic method such as : power spectrum, spectrogram or FFT are not. The method from Elhers is the one used to tune our rsi.

The Indicator

Our indicator use the dominant cycle frequency to calculate the period of the rsi thus producing an adaptive rsi . When our adaptive rsi cross under 70, price might start a downtrend, else when our adaptive rsi crossover 30, price might start an uptrend. The alpha parameter is a parameter set to be always lower than 1 and greater than 0. Lower values of alpha minimize the number of detected peaks/valleys while higher ones increase the number of those. 0.07 for alpha seems like a great parameter but it can sometimes need to be changed.

The adaptive indicator can also detect small top/bottoms of small periods

Of course the indicator is subject to failures

At the end it is totally dependent of the dominant cycle estimation, which is still a rough method subject to uncertainty.

Conclusion

Tuning your indicator is a great way to make it adapt to the market, but its also a complex way to do so and i'm not that convinced about the complexity/result ratio. The version using chart background will be published separately.

Feel free to tune your indicators with the estimator from elhers and see if it provide a great enhancement :)

Thanks for reading !

References

for the calculation of the dominant cycle estimator originally from www.davenewberg.com

Decoding the Hidden Market Rhythm (2010) Lars von Thienen

Ehlers , J. F. 2004 . Cybernetic Analysis for Stocks and Futures: Cutting-Edge DSP Technology to Improve Your Trading . Wiley