Dealar VIX Implied Range + Retracement LevelsThis Implied range Is derived by the VIX(1 sd annual +/- Implied move.)

This Indicator plots the daily Implied range, A lot of quantitative trading firms/ MM firms hedge their delta & gamma exposure around the Implied range(prop calc). I have added retracement levels as well, so you have more pivot levels.

Enjoy!

UVXY

vix_roll_yieldShows the roll yield of the VX futures, which is the ratio of a continuously weighted average of the front two months to the VIX. The VX (VIX futures) contract expires on the third Tuesday of each month. On the next trading day, the front month will have full weighting, and the second month will have no weight. On the expiration day, the back month will have full weighting and the front month will have no weight. In between, the weight gradually shifts.

This weighted average is similar to the SPVIXSTR index that UVXY and several other funds track. When the average is below the VIX, the indicator is negative, and the front month contract will tend to gain value relatively more rapidly than the back month as it converges upward to the VIX spot price. Because funds whose NAV is tied up in VX contracts continuously roll from the (typically cheaper) front month to the back, in situations where the front month is more expensive than usual--or even more expensive than the back month--these products may have a "tailwind". In this case, they are selling expensive front month contracts to purchase cheap back month contracts.

Ordinarily, VIX funds have a "headwind." The roll yield is positive, the front month is cheap, and the back month is expensive. Day by day the funds sell cheap front month contracts and buy expensive back month contracts, which, in turn and over time, become the front month and converge with the VIX, losing value rapidly. This is a brief explanation about the decay of these products.

(JS)S&P 500 Volatility Oscillator For Options 2.0I am going to start taking requests to open source my indicators and they will also be updated to Version 4 of Pinescript.

I added some features to the original code such the ability to smooth the oscillator and select the look back periods for the historical volatility.

Link to original:

Original post:

"The idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX ). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX ) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility . (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M ) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX , SPY , even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Feb 17, 2019

Release Notes: Cosmetic update for a much cleaner look:

-Replaced the "HIGH IV" with a simlple "H"

-Now the white line is constantly showing you the relationship between VIX and VIX3M - when VIX is greater than VIX3M the background still goes red

-However, now when VIX drops below Historical Volatility, the background is bright green

-When both above are true - it's dark green

-The Average True Range on the bottom is now a series of crosses"

Historical Volatility RankSame formulation of IVR but based on Historical Volatility instead.

Serves the same purpose as IV rank.

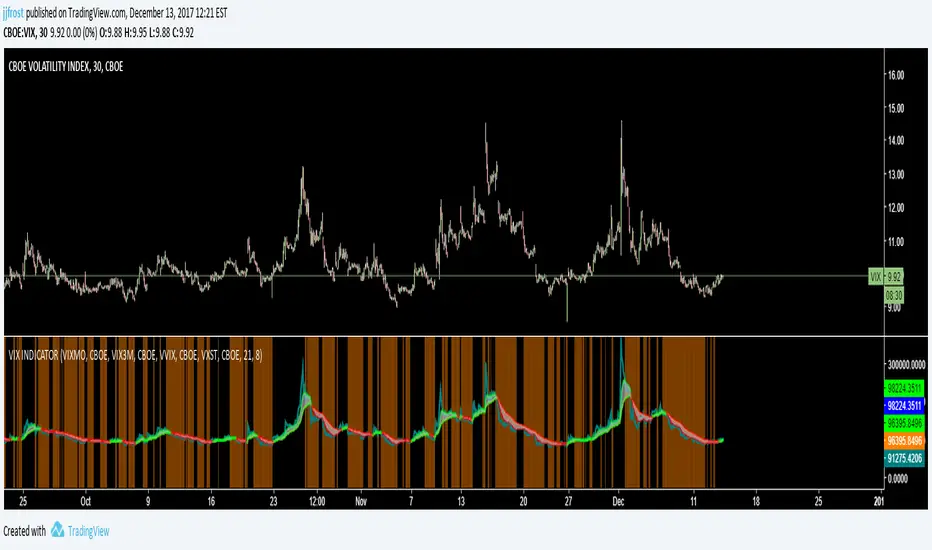

VIX INDICATORWorks best as an intraday indicator

Background black & line green = Long VIX

Background black & red line = No trade

Background orange & line green = Consider selling

Background orange & line red = Short VIX

VIX Term Roll OscillatorMy implementtion of VIX term roll Oscillator according to the articles below

seekingalpha.com

vixcontango.wordpress.com

Hope it helps!

Daniel

VIX Contango OscillatorVIX Contango Oscillator as outlined in the following blog post

vixcontango.wordpress.com

By Daniel Xu

UVXY Contango Rate - my quick and dirty indicatorFeel the force ... read the source.

Give you an idea of the contango headwind / backwardation tailwind that UVXY is experiencing.

Works on Daily time frame only unless you buy the VIX feed.