Keltner Channel with Forecast It is recommended to use the 15-minute chart along with Heikin Ashi candles. The two blue lines represent the 15-minute Keltner Channel, while the green lines represent the 1-hour Keltner Channel. This setup provides a clearer view of both short-term and longer-term market trends, helping traders make more informed decisions based on the combined insights from the 15-minute and 1-hour timeframes.

The entire code aims to display market dynamics on the chart based on two indicators: the Keltner Channel and volume. This allows traders to identify potential reversal points (when the price touches the Keltner bands) and areas where there is increased market activity (changes in volume). With this information, traders can make more informed decisions about opening or closing positions.

The code generates forecasts based on the touches of the bands, and the yellow line acts as an additional volume indicator, suggesting important market changes.

VOL

MBAND 200 4H BTC/USDT - By MGS-TradingMBAND 200 4H BTC/USDT with RSI and Volume by MGS-Trading: A Neural Network-Inspired Indicator

Introduction:

The MBAND 200 4H BTC/USDT with RSI and Volume represents a groundbreaking achievement in the integration of artificial intelligence (AI) into cryptocurrency market analysis. Developed by MGS-Trading, this indicator is the culmination of extensive research and development efforts aimed at leveraging AI's power to enhance trading strategies. By synthesizing neural network concepts with traditional technical analysis, the MBAND indicator offers a dynamic, multi-dimensional view of the market, providing traders with unparalleled insights and actionable signals.

Innovative Approach:

Our journey to create the MBAND indicator began with a simple question: How can we mimic the decision-making prowess of a neural network in a trading indicator? The answer lay in the weighted aggregation of Exponential Moving Averages (EMAs) from multiple timeframes, each serving as a unique input akin to a neuron in a neural network. These weights are not arbitrary; they were painstakingly optimized through backtesting across various market conditions to ensure they reflect the significance of each timeframe’s contribution to overall market dynamics.

Core Features:

Neural Network-Inspired Weights: The heart of the MBAND indicator lies in its AI-inspired weighting system, which treats each timeframe’s EMA as an input node in a neural network. This allows the indicator to process complex market data in a nuanced and sophisticated manner, leading to more refined and informed trading signals.

Multi-Timeframe EMA Analysis: By analyzing EMAs from 15 minutes to 3 days, the MBAND indicator captures a comprehensive snapshot of market trends, enabling traders to make informed decisions based on a broad spectrum of data.

RSI and Volume Integration: The inclusion of the Relative Strength Index (RSI) and volume data adds layers of confirmation to the signals generated by the EMA bands. This multi-indicator approach helps in identifying high-probability setups, reinforcing the neural network’s concept of leveraging multiple data points for decision-making.

Usage Guidelines:

Signal Interpretation: The MBAND bands provide a visual representation of the market’s momentum and direction. A price moving above the upper band signals strength and potential continuation of an uptrend, while a move below the lower band suggests weakness and a possible downtrend.

Overbought/Oversold Conditions: The RSI component identifies when the asset is potentially overbought (>70) or oversold (<30). Traders should watch for these conditions near the MBAND levels for potential reversal opportunities.

Volume Confirmation: An increase in volume accompanying a price move towards or beyond an MBAND level serves as confirmation of the strength behind the move. This can indicate whether a breakout is likely to sustain or if a reversal has substantial backing.

Strategic Entry and Exit Points: Combine the MBAND readings with RSI and volume indicators to pinpoint strategic entry and exit points. For example, consider entering a long position when the price is near the lower MBAND, RSI indicates oversold conditions, and there is a notable volume increase.

About MGS-Trading:

At MGS-Trading, we are passionate about harnessing the transformative power of AI to revolutionize cryptocurrency trading. Our indicators and tools are designed to provide traders with advanced analytics and insights, drawing on the latest AI techniques and methodologies. The MBAND 200 4H BTC/USDT with RSI and Volume indicator is a prime example of our commitment to innovation, offering traders a sophisticated, AI-enhanced tool for navigating the complexities of the cryptocurrency markets.

Disclaimer:

The MBAND indicator is provided for informational purposes only and does not constitute investment advice. Trading cryptocurrencies involves significant risk and can result in the loss of your investment. We recommend conducting your own research and consulting with a qualified financial advisor before making any trading decisions.

Keltner Channel Volatility FilterOVERVIEW

The Keltner Channel Volatility Filter indicator is a technical indicator that gauges the amount of volatility currently present in the market. The purpose of this indicator is to filter out with-trend signals during ranging/non-trending/consolidating conditions.

CONCEPTS

This indicator assists traders in capitalizing on the assumption that trends are more likely to start during periods of high volatility compared to periods of low volatility . This is because high volatility indicates that there are bigger players currently in the market, which is necessary to begin a sustained trending move.

So, to determine whether the current volatility in the market is low, the KCVF will grey out all bars whose average price is within the Keltner Channels.

If the average price breaks out of the Keltner Channels , it is reasonable to assume we are in a high-volatility period. Thus, this is the ideal time to enter a trending trade due to the assumption that trends are more likely to start during these high-volatility periods.

HOW DO I READ THIS INDICATOR

When the candles are greyed out, don't take any trend trades since the current volatility is less than the usual volatility experienced in the market.

When the candles aren't greyed out, take all valid with-trend trades since the current volatility is greater than the usual volatility experienced in the market.

RISK managment TOOL not a netive english speakr - soory for spelling problems.

this tool purpse is to help you dtermine postion sizing

it take a trend meeter of your chose and mesure it with the high and low of lookback number (defult is 100 )

you can chose your trend meeter from 'close','VOL', 'MA short' , 'MA long' , 'MACD', 'VOL MA', 'ATR', 'MFI', 'TSI'

with that you can see if you are "overbought" or "oversold " with the highest and lowest of a lookback period

and size acording to that .

the MA box - MAshort and MA long is the same box for the MACD ma for calcs and for the TSI

for long - if in lower band buy +++ if midelle buy +++ if high buy +

for short - if in highr band short +++ if midelle short ++ if low short ++

hope it will help you

for source - comment email and tip.

כלי ניהול הסיכונים הזה נועד להראות לכם את היחס של המתנד הנבחר ביחס לגבוהה והנמוך בבחירת טווח הזמן הנבחר ( דיפולט הוא 100 ימים אחורה ) ובכך לעזור לכם בהחלטת גודל הפוזציה

הכלי נועד לעזור בוויזאולציה של הטרנד לעומת האיתות שאתם מקבלים ביחס לגבוהה או הנמוך של 100 ימים אחורה

אם אתם מתכננים עסקת לונג העדיפות לקנות כאשר הסמן נמצא ברצועה התחתונה ובמקום זה תוכלו להגדיל את הפוזציה ל +++

כאשר הסמן נמצא ברצועה האמצעית אפשר לקנות ++

וכאשר הסמן נמצא למעלה עדיף לשקול את הפוזציה או לקנות +

ההפך לשורט.

לקבלת הקוד אפשר להשאיר מייל בתגובה + טיפ.

תודה ל @daviddtech tnx to

Volume Highlighter in main by RSUThis indicator is displayed in the main picture, which saves the space of a picture indicator.

Volume is highlighted to allow you to focus more on the above-average volume , and if it is greater than 4 times standard deviation it is marked as a huge volume in yellow. There will be support and resistance at this level.

There is a switch to show the turnover.

vx_termsUSAGE

--------

This script helps train your intuition for changes in the VX term structure. I recommend using it on the VIX chart, so you can compare changes in the terms to changes in VIX. It's also nice for calendar spread traders who want to get a feel for the same changes.

1. Select a day, month, and year using the inputs

2. Observe the data table.

3. Open the input again and increment or decrement the day (and month, year as necessary).

4. Click "Ok".

5. Click to deselect the indicator, which allows the chart to load new data.

6. The data table will be reloaded with the next/previous day's data.

The data table has the following columns:

- contract: the VX contracts, in sequence. refer to the CBOE for month codes (F for January, etc.)

- close: the closing price of the contract.

- ma:mb: the spread (difference) between this row and the next row.

- ma:mb chg: the spread's change from prior close.

For example, given the following values for the first two columns:

VXQ2021, 16.5, -3.1, -0.2

VXU2021, 19.6, ..., ...

The front month (Q = august) closed at 16.5, $3.1 below the s\September contract. The negative spread enlarged by $0.20 from $2.90 on the previous trading day.

BUGS, ODDITIES, AND LIMITATIONS:

-------------------------------------------

- The first column will be greyed out after expiration day, which is the 3rd Tuesday of that month. Unfortunately, I can't load the next month's contract due to some limitations with TV.

- The active date is highlighted with a yellow background. When a non-trading date is selected, the highlight will disappear. However, the data table will sometimes fill with the nearest trading date, prematurely. No worries, just know that the data is probably for the previous Friday.

- The script is clunky and slow, but this is the best I can do with TV. Hopefully they add more continuous contracts or allow true dynamic symbol loading.

SPECIAL THANKS:

---------------------

Thanks to HeWhoMustNotBeNamed for helping me get through some messiness. Very helpful guy.

www.tradingview.com

0_dteUSAGE

This script guages the probability of an underlying moving a certain amount on expiration day, to aid the popular "0 dte" strategy. The script counts how many next-day moves exceeded a given magnitude in the past, under similar conditions. The inputs are:

mark_mode:

- "open": measures the magnitude as "open to close"--a true 0 dte.

- "previous close": for lazy people who don't want to wake up early. measures magnitude from the previous day's close.

move_mode:

- "percent": measures moves that exceed a given percentage.

- "absolute": measures moves that exceed a point value.

move-dir: measure only up moves, down moves, or both.

vol_model: the model for realized volatility. (may add more later).

min_vol: only measure moves when realized vol is above this value.

max_vol: only measure moves when realized vol is below this value.

precision: number of digits printed in the output table.

EXAMPLE:

- mark_mode: "previous close"

- move_mode: "percent"

- move_dir: "up"

- move_mag: 0.07

- vol_model: hv30

- min_vol: 0.2

- max_vol: 0.5

These settings will count the number of trading days that closed 7% higher than the previous day's close, when the previous day's realized volatility (annualized) was between 20% and 50%. The outputs are:

- current vol: green plot. Today's realized vol. Shown for convenience.

- max and min vol: red plots. Also shown for convenience.

- count: the number of days that exceeded the chosen magnitude, when the previous day's realized volatility was within the chosen bounds.

- total: the total number of days where realized volatility was within the chosen bounds

- probability: count / total. the percentage of days that exceeded the move when volatility was within the bounds.

- move: plotted as a purple line. purple "X" labels are plotted above

- bars where the move exceeded the magnitude threshold and volatility was in-bounds. a "hit".

CONCLUSION

This script is based on the idea that realized volatility has some bearing on future volatility. By seeing what happened in the past when volatility was close to its current value, we may be able to assess the probability that our short put will be in the money, tomorrow, and our account devastated.

NOTE: Unlike many of my other scripts, all percentages--both inputs and outputs--are given in fractional form. E.g., 0.01 means 1%.

pricing_tableThis script helps you evaluate the fair value of an option. It poses the question "if I bought or sold an option under these circumstances in the past, would it have expired in the money, or worthless? What would be its expected value, at expiration, if I opened a position at N standard deviations, given the volatility forecast, with M days to expiration at the close of every previous trading day?"

The default (and only) "hv" volatility forecast is based on the assumption that today's volatility will hold for the next M days.

To use this script, only one step is mandatory. You must first select days to expiration. The script will not do anything until this value is changed from the default (-1). These should be CALENDAR days. The script will convert to these to business days for forecasting and valuation, as trading in most contracts occurs over ~250 business days per year.

Adjust any other variables as desired:

model: the volatility forecasting model

window: the number of periods for a lagged model (e.g. hv)

filter: a filter to remove forecasts from the sample

filter type: "none" (do not use the filter), "less than" (keep forecasts when filter < volatility), "greater than" (keep forecasts when filter > volatility)

filter value: a whole number percentage. see example below

discount rate: to discount the expected value to present value

precision: number of decimals in output

trim outliers: omit upper N % of (generally itm) contracts

The theoretical values are based on history. For example, suppose days to expiration is 30. On every bar, the 30 days ago N deviation forecast value is compared to the present price. If the price is above the forecast value, the contract has expired in the money; otherwise, it has expired worthless. The theoretical value is the average of every such sample. The itm probabilities are calculated the same way.

The default (and only) volatility model is a 20 period EWMA derived historical (realized) volatility. Feel free to extend the script by adding your own.

The filter parameters can be used to remove some forecasts from the sample.

Example A:

filter:

filter type: none

filter value:

Default: the filter is not used; all forecasts are included in the the sample.

Example B:

filter: model

filter type: less than

filter value: 50

If the model is "hv", this will remove all forecasts when the historical volatility is greater than fifty.

Example C:

filter: rank

filter type: greater than

filter value: 75

If the model volatility is in the top 25% of the previous year's range, the forecast will be included in the sample apart from "model" there are some common volatility indexes to choose from, such as Nasdaq (VXN), crude oil (OVX), emerging markets (VXFXI), S&P; (VIX) etc.

Refer to the middle-right table to see the current forecast value, its rank among the last 252 days, and the number of business days until

expiration.

NOTE: This script is meant for the daily chart only.

vertical_pricer

USAGE

1. Select the type of contract (call or put), the long strike, and the width.

2. Select the volatility model

3. The standard deviation is shown, enter it into the input.

The tool gives a theoretical price of a vertical spread, based on a

historical sample. The test assumes that a spread of equal width was sold on

every prior trading day at the given standard deviation, based on the

volatility model and duration of the contract. For example, if the 20 dte

110 strike is presently two standard deviations based on the 30 period

historical volatility, then the theoretical value is the average price all

2SD (at 20 dte) calls upon expiration, limited by the width of the spread and

normalized according to the present value of the underlying.

Other statistics include:

- The number of spreads in the sample, and percentage expired itm

- The median value at expiration

- The Nth percentile value of spreads at expiration

- The number of spreads that expired at max loss

Check the script comments and release notes for further updates, since Tradingview doesn't allow me to edit this description.

Relative Volume Screener AlertsThis script will screen 12 different stocks and current chart (13 in total) for entry points from my relative volume indicator.

1. Enter in any ticker ID's from charts you wish to scan in the settings.

2. Go to desired timeframe.

3. Click add alert button at top toolbar.

4. Select RVOL Screener Alerts indicator, input alert notification settings and/or change alert name and click create.

The script will then scan the stocks and alert you of any entry points from the timeframe you set the alerts.

A new alert needs to be created for each timeframe you wish to screen.

You can find my relative volume indicator here:

Volume PanelDisplays volume data in panel on bottom right of screen. Shows current bar, change from last bar and average of last 20 bars. This number can be changed in settings if you wish to have the average calculated on a different amount of bars.

Volume Pump WaveThis indicator displays volume as a pump wave. Can be useful for chart analysis and easy detection of anomalies/trends.

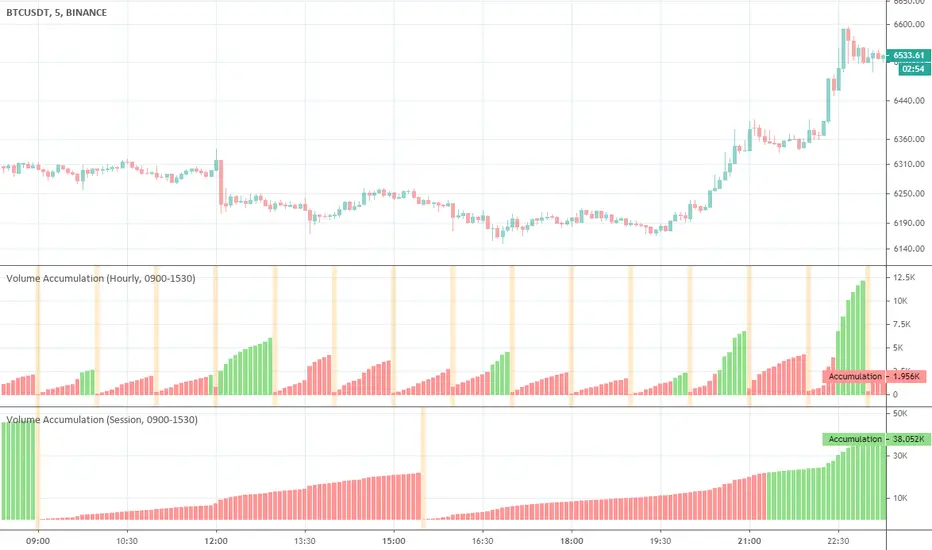

Volume AccumulationA simple tool that accumulates the trading volume of an instrument for a specified period of time.

Available modes:

Minutely

Hourly

Session

Daily

Monthly

Quarterly

Yearly

Bitcoin Real VolumeBitcoin’s Real Volume

An accurate read on the change in Bitcoin’s volume profile over time.

Based on 2019 reports by Bitwise and Alameda Research.

Please see the script code notes for assumptions and details on data selection.

Follow me for more information on this script.

Realized VolatilityRealized / Historical Volatility

Calculates historical, i.e. realized volatility of any underlying. If frequency is not the daily, but for example 6h, 30min, weeks or months, it scales the initial setting to be suitable for the different time frame.

Examples with default settings (30 day volatility, 365 days per year):

A) Frequency = Daily:

Returns 30 day historical volatility, under the assumption that there are 365 trading days in a year.

B) Frequency = 6h:

Still returns 30 day historical volatility, under the assumption that there are 365 trading days in a year. However, since 6h granularity fits 4 times in 24 hours, it rescales the look back period to rather 30*4 = 120 units to still reflect 30 day historical volatility.

SMA True Range(%)In this Indicator, we have the "True Range" in percentage and the "SMA True Range" in percentage.

we have a good difference from "SMA True Range" to "True Range".

I believe that the "SMA True Range" better shows the volatility, making your stop and target better placed.

Historical Volatility RankSame formulation of IVR but based on Historical Volatility instead.

Serves the same purpose as IV rank.

DepthHouse Better VolumeDepthHouse Better Volume takes the standard volume bars and gives it an extreme overhaul.

The brighter colored bars signal strong buying or selling pressure in the market based on the volume.

The small lines within the columns represent the duration of this increased buying and selling volume.

This calculation is based on negative and positive volume flow. These variables are based on the moving average length, type, and percent change.

All of which are user defined.

DepthHouse Better Volume also changes how each bar color is calculated. The traditional calculation is dependent on the open and close of the candle. Whereas this volume indicator calculates the displayed color based on the position of the bar relevant to the last.

The user has the option to turn this feature on or off.

Try this indicator for FREE! Just leave a comment, or feel free to send me a PM

Volume weighted Balance of PowerIt's a simple indication.

I multiplied the output of bop with volume, make it more smoother.

Dollar normalized volumeAn indicator that multiply the closing price with the current volume. (close X volume)

This will show the relative interest in the underlying asset regardless of the price change over time. For the case of FXCM, when the price fell from $16 to $1, its volume spiked 16x at the same time given the fact that 16x more shares can now be purchased with the same amount of dollar.

Enjoy! and remember to give a thumbs up.