Jurik RSXAdopted to Pine from www.prorealcode.com .

I haven't yet understood the details of the algorithm but it matches the original Jurik's RSX one to one.

Jurik's RSX is a "noise free" version of RSI, with no added lag. To learn more about this indicator see www.jurikres.com .

Good luck!

Zerolag

Kalman SmootherA derivation of the Kalman Filter.

Lower Gain values create smoother results.The ratio Smoothing/Lag is similar to any Low Lagging Filters.

The Gain parameter can be decimal numbers.

Kalman Smoothing With Gain = 20

For any questions/suggestions feel free to contact me

[ALERTS] MA Cross ElevenThis script is a crossing of eleven different MA, with alerts and SL and TP.

The simplest is what works best.

SMA --> Simple

EMA --> Exponential

WMA --> Weighted

VWMA --> Volume Weighted

SMMA --> Smoothed

DEMA --> Double Exponential

TEMA --> Triple Exponential

HMA --> Hull

TMA --> Triangular

SSMA --> SuperSmoother filter

ZEMA --> Zero Lag Exponential

Using "once per bar close" repaint is 0%, but if you like risk can choose "once per bar", better profit.

Thanks to JustUncleL and his amazing sripts.

Adaptive Least SquaresAn adaptive filtering technique allowing permanent re-evaluation of the filter parameters according to price volatility. The construction of this filter is based on the formula of moving ordinary least squares or lsma , the period parameter is estimated by dividing the true range with its highest. The filter will react faster during high volatility periods and slower during low volatility ones.

High smooth parameter will create smoother results, values inferior to 3 are recommended.

You can easily replace the parameter estimation method as long as the one used fluctuate in a range of , for example you can use the efficiency ratio

ER = abs(change(close,length))/sum(abs(change(close)),length)

Or the Fractal Dimension Index , in fact any values will work as long as they are rescaled (stoch(value,value,value,length)/100)

For any suggestions/questions feel free to send me a message :)

zerolag PredictiveSystemsExplanation;

www.stockspotter.com

Açıklama yukarıdaki pdf dosyasında ingilizce olarak mevcuttur.

MA Study: Different Types and More [NeoButane]A study of moving averages that utilizes different tricks I've learned to optimize them. Included is Bollinger Bands, Guppy (GMMA) and Super Guppy.

The method used to make it MtF should be more precise and smoother than regular MtF methods that use the security function. For intraday timeframes, each number represents each hour, with 24 equal to 1 day. For daily, 3 is 3 day, for weekly, 4 is the 4 weekly, etc. If you're on a higher timeframe than the one selected, the length will not change.

Log-space is used to make calculations work on many cryptos. The rules for color changing Guppy is changed to make it not as choppy on MAs other than EMA. Note that length does not affect SWMA and VWAP and source does not affect VWAP.

A short summary of each moving average can be found here: medium.com

List of included MAs:

ALMA: Arnaud Legoux

Double EMA

EMA: Exponential

Hull MA

KAMA: Kaufman Adaptive

Linear Regression Curve

LSMA: Least Squares

SMA: Simple

SMMA/RMA: Smoothed/Running

SWMA: Symm. Weighted

TMA: Triangular

Triple EMA

VWMA: Volume Weighted

WMA: Weighted

ZLEMA: Zero Lag

VWAP: Vol Weighted Average

Welles Wilder MA

Quadratic RegressionA quadratic regression is the process of finding the equation that best fits a set of data.This form of regression is mainly used for smoothing data shaped like a parabola.

Because we can use short/midterm/longterm periods we can say that we use a Quadratic Least Squares Moving Average or a Moving Quadratic Regression.

Like the Linear Regression (LSMA) a Quadratic regression attempt to minimize the sum of squares (sum of the squared difference between a set of data and an estimator), this is why

those kinds of filters have low lag .

Here the difference between a Least Squared Moving Average ( green ) and a Quadratic Regression ( red ) of both period 500

Here it look like the Quadratic Regression have a best fit than the LSMA

Double Exponential SmoothingSingle Exponential Smoothing ( ema ) does not excel in following the data when there is a trend. This situation can be improved by the introduction of a second equation with a second constant gamma .

The gamma constant cant be lower than 0 and cant be greater than 1, higher values of gamma create less lag while preserving smoothness.Higher values of length must be followed by higher values of gamma in order to keep the lag low.

The first smoothing part consist of a classic ema but we add s-s1 to the previous smoothed value, this will help decrease lag.The second smoothing part then updates the trend, which is expressed as the difference between the last two values.

Finite Impulse Response (FIR) FilterFinite Impulse Response (FIR) Filter indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 20:7 (26-31): Zero-Lag Data Smoothers).

NOTE: Ehlers' favorite FIR filter had 1, 2, 3, 3, 2, 1, 0 coefficients.

Ahrens Moving AverageAhrens Moving Average indicator script.

This indicator was originally developed by Richard D. Ahrens (Stocks & Commodities V.31:11 (26-30): Build A Better Moving Average).

Infinite Impulse Response (IIR) FilterInfinite Impulse Response (IIR) Filter indicator script.

This indicator was originally developed by John Ehlers (Stocks & Commodities V. 20:7 (26-31): Zero-Lag Data Smoothers).

Zero Lag Exponential Moving AverageZero Lag Exponential Moving Average indicator script based on the original version by John Ehlers and Ric Way

Forex MA Racer - SMA Performance /w ZeroLag EMA TriggerThis strategy uses 5 Simple Moving Averages and 2 ZeroLag Exponential Moving Averages, to determine possible entries and exits.

- Pretuned for Forex on 15m period

- Uses SMA(10/20/50/100/200) and EMA(9/21) by default

- Be cautios in sideward markets!

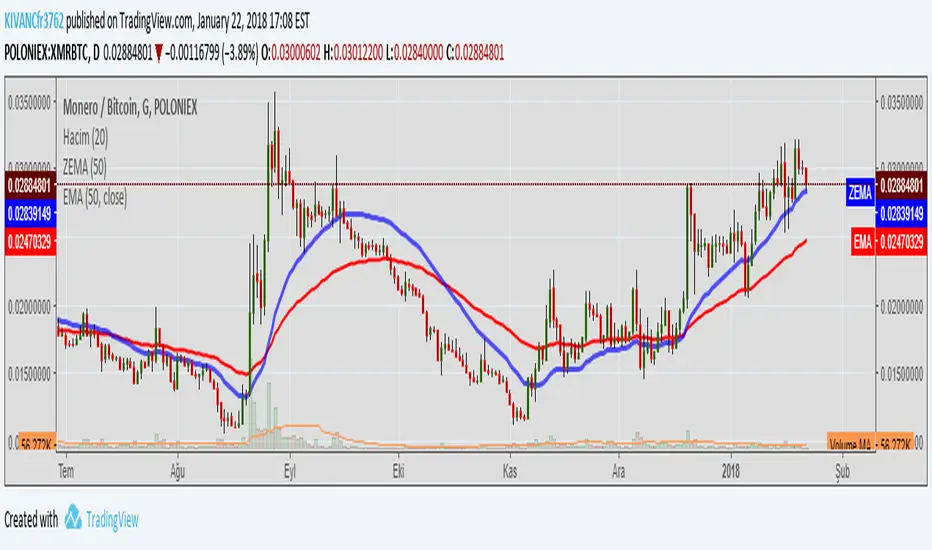

Zero Lag EMA v2 by KIVANÇ fr3762A different version of ZERO LAG EMA indicator by John Ehlers and Ric Way...

In this cover, Zero Lag EMA is calculated without using the PREV function.

The main purpose is that to provide BUY/SELL signals earlier than classical EMA's.

You can see the difference of conventional and Zero Lag EMA in the chart.

The red line is classical EMA and the blue colored line is ZEMA ( Zero Lag Ema ).

Turkish Explanation:

Ehlers ve Way'in ZERO LAG ,ndikatörünün Prev (previous value) kullanılmadan yorumlanarak hesaplanmış hali.

Amaç klasik Üssel Ortalamaya göre daha hızlı tepki verip, Al/Sat sinyallerini daha erken alabilmek.

Grafikte kırmızı renkle görülen normal Üssel HO ve mavi renkli olan Zero Lag (gecikmesiz) Üssel HO