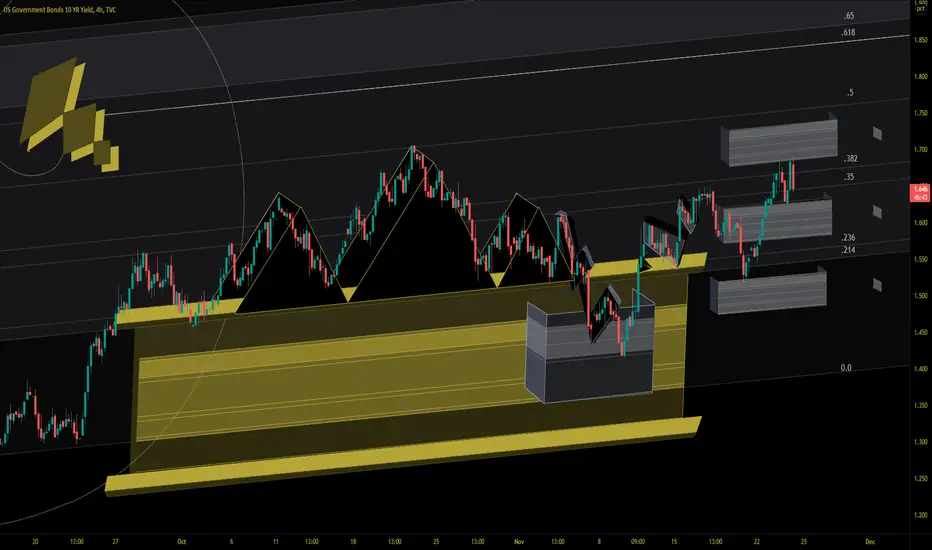

10Y Bull Breakthe H&S broke for the confirmation, but only to the first maker at the .214. A Diamond Continuation has fueled the yield to back above 1.80

10yearnote

Bond Broadening - in 3DVolatility is the name of the game as the major indexes were in a big range all week. The Nasdaq is testing it's 2 hour UBB with a Bull Flag under resistance. The Russell 2000 also has a Bull Flag after finding 2hr LBB support, setting up a potential Lower High under the 2h 50 SMA. The Bonds gave back the bull break during the FOMC meeting and are now showing a choppy head and shoulders, on the 30 minute, which does not have the nice rolling shoulders. The weekly iH&S neckline remains a point of control.

TNX - 10 YR T-Note Yield - Overblown?This thing is way ahead of where quarterly money flows suggest it should be - I think it will pull back and consolidate 1.10 - 1.150 range. Also looks to be exhibiting the same post-crisis recovery that it followed after the GFC. I'm pretty sure all of these anti-fed pumpers were out there barking about it back then as well.

Also, Bitcoin (all cryptos) still look like crud, barely hanging on minus over 30% and still tired.

Stocks looking real good in terms of quarterly money flows. This recent pull back looks like profit taking to me (maybe another 5% down and reverse but I think we are near the end of the correction. Oil also holding up and actually creeping higher, suggesting demand remains (for now); again, we know that the American consumer IN 2007 - FIFTEEN YEARS AGO - was able to support $100+ / barrel oil. Today we are tickling $86 / barrel.

Fear sells. Listen to the data.

God Bless.

#GoChiefs!

ES1! - Opex Week Preview in 3DYhe 10Y Note Yield Gained 4.8% on Friday, topping out at 1.79%. The echoes from the pundits are calling for a return to value as high beta-growth has seen continued pressure, with ARKK leading the declines. NQ1! defended it's 4h Higher low on Friday with a hammer but remains in a 4h Real-Body Bear-Flag. In contrast RTY1! (Russell 2000) and YM1! (Dow Jones Industrial Average), set lower lows before their bounces. RTY1! is in a 4h bear channel, approaching the upper-bound. Vix lost steam at 22 finding support at 19. For consolidation to continue the path is a Daily H&S neckline break, in the most recent test of the largest expansion in the History of the Federal Reverse's Balance Sheet. This looks like a middle, with major markets offering divergent clues. Opex weeks have a way of offering abrupt clarity.

Updating the US10Y Bonds.Data for Kissing/Crossing 200Weekly MA:

2017-2019? One year nothing then 11%/20%

2015-2016 : 14%

2015-9 months sideways then 12%

2015 xxxx nothing

2013-2014 Long bull move. 9% pullback.

2011- 8%

2011- 7%

2010- 17%

2005-2007 : xxx long Bull move the crash

05-6%

05- 7%

04- 8%

1999-13%/10%/13% then crash

1997- 10% the bull move.

1996-8% Choppy Market then bull move

1994-9% then big bullish market ( 1 Year choppy market)

20%

11%

7%

7%

8%

36%

14 %

----------------------------------------------------------------------

Summary: 24 signals Kissing or Crossing 200W MA.

18 signals we went down @ kissing/crossing .

Kissing/crossing happened a during pullbacks.

6 months-Year nothing happened then crash crossing

down.

75% success rate we will get a pullback/correction

kissing/crossing 200w MA.

25% we will continue a Bullish till crossing down then crash

- 2 Years after crossing then crash 2007

-2015 cross up/down = Nothing happen to SPX !!!

ZN - 10 Year Note Futures / Monthly @ 20 Yrs / The Abyss of DEBTIt is often said by Quantity Theorists echoing, Milton Friedman - "Inflation is always and everywhere a monetary phenomenon.”

Conditions... matter, they change as does the "moneyness of money" - but you can't keep the Chicago School of Economic

mind poisoning down.

That could be why I didn't play with academia, it is a toxic sandbox wed to a beach at times. Polluting the incoming tides.

Friedman could not have imagined how awry his QT has been turned on its collective head.

Gold Bugs to this day, quote this - scores of times every single day. "Were Gold Priced in DEBT

it would be $250,000+"

No one cares, least of all Central Banks who Demonetized it but made it legal to own under Nixon.

You all swap fungibles for... Silver? A Weimar home? Taco Bell?

Good luck, it's a Tier 1 asset on the Books of Central Banks for a reason and trades at a varying rate as it always has.

Q of M clearly isn't tied to it and it's not chasing away Good Money for Bad any longer... those storied days passed very

long ago.

_____________________________________________________________________________________________________________

Money loses its purchasing power parity in a number of ways - not simply through more money chasing goods and services,

this is merely one-sided - "ceteris para bis" Jedi Mind Fuck at its finest.

Causation is always assumed from the money supply increase to price rises...a very basic truth, but ONLY a precondition

and not a fate acompli.

____________________________________________________________________________________________________________

The Fundamental causes of a general price inflation are still supply-side factors - for example, rises in wages or prices of factor input costs - which we see in the PMI data - to date not fully passed onto Consumes due to Supply-Side Shocks ) or demand-side ones - high demand causing price increases in markets.

The fatal flaw is QMT assumes an exogenous money world and the wrong direction of causality.

The contraction in Broad Money with a Credit Money System aka Bank Money is destroyed as people move to acquire CASH money

or what is perceived to be a CASH Equivalent.

_____________________________________________________________________________________________________________

Simply Put: Aged Theory is flawed beyond. Supply Side Cocktails and the Ingredients of the CREDIT MONEY Elixirs are quite

different than in 1963 Uncle Milty.

______________________________________________________________________________________________________________

Speaking of Credit (DEBT MONEY if you can al it that) the BOE recently raised rates.

China, faced with new lockdowns surrounding the - Credit Squeeze (TY to Shevchenko for the prod to dig in and determine WTF) .

Turns out 6 property developers including the "Grande" have deferred wages the CCP now says must be paid by the start of the

Lunar New Year, oh and... yer gonna need to pay $21.37 Billion in Bonds or default.

Sounds bad huh? Not remotely...

Back wages amount to $174.38 Billion, can't pay 'em?

Lock 'em down, which is precisely what the CCP is setting up to avoid immense Social upheaval.

______________________________________________________________________________________________________________

Are we seeing a trend appear?

We are indeed. Debt Defaults have been propped by Governments to stave off tragic Social disruptions.

Hardly a footstep in the direction of Trust for Journey of 1,000 miles to default.

S'ok China, yer not alone, we proudly stand with you, although we've been at tit longer on this turn, so we're

just better at wallpapering over it with Currency Seniorage.

Yaun / Renminbi - only one works inside and one outside.

Hmmm...

That could not possibly happen here in the US of A, could it?

Naw.

_____________________________________________________________________________________________________________

When you destroy the Moneyness of Money with it goes all attendant prior theory as well as the very thing used to bring

Money into Circulation @ Tier One - The BOND MARKETS.

Fractional Reserve Banking merely extends it to obscene levels of Leverage and DEBT which are far beyond repayment.

Toss in the 6% Vig the FED takes for this privilege and after a hundred or so years, they end up owning everything.

They are, after all, the lender of last resort, the DTC merely the record keeper for when the payments halt and DEBT

becomes unserviceable.

What are your opportunity costs to Debt?

What do you value?

Forget Price it's no longer a metric for the sane, merely a distended and starved stomach.

_____________________________________________________________________________________________________________

Moral:

When Risks are ignored, they are mispriced...

10 Year Note - Support Bear Back-Test in 3DA Market Metaverse - Vix remains above 20 with NQ1! finding resistance at the 16400-16450 zone for the 13th time on the 2h since November 23rd. The Fixed Range Volume Profile (11/23 - 12/16) - Point of Control (POC) is 16286, 2.54% above the current price. The 10Y bond back-tested, bear, the 1.43 support break.

10 Year Note - Break UpdateBack-testing the break .214. The S&P 500 has formed a 2 hour Bull Flag. The Russell 2000 is supported by the 2 hour 8 EMA

10 Year - ih&s Confirmed - Break Target RulerWatching for a back-test of the neckline. NQ1! with support below at the 2 hour MBB.

10 Year Bond Yield - Inverse Head and Shoulders in 3DPrice is testing the neckline with mini-bull pennant below the neckline. A low volume day in the indexes as consolidation commenced after the covering rally yesterday. AAPL has led the bull rotation, with Meta finding support at $300. MSFT found supply at the 338 zone with 15!! tests of that resistance since it's loss on 11/23.

Bond Yields Downtrend in 3DAfter finding support and a fourth Lower Low under 1.35, bond yields have had a mini bounce to produce a Bear Flag. A lower interest rate environment persists, will the volatility in bonds become a staple of the new markets?

10 Year Note - Bear Flag in 3DThe one area that is transitory is the messaging around whether or not inflation is in fact transitory. The new boss the same as the old boss, low rates for the win.

10 Year Note in #D - 35 Support WickThe 10 Year Bond Yield found resistance at the 8h 50 SMA; with support at the monthly 8 EMA. The 8-hour model's H&S Pattern Target Ruler's .35 offered a support wick as the low interest rate environment continues with a sub 1.5 reading.

10 Year Bond - Golden Pocket SupportA flight to safety with, a rejection of the monthly iH&S neckline, yields retreated, finding Golden Pocket support at the lower channel.

10 Year Note - Inverse H&S 8h View - in 3DThat wraps-up the trading before the break. The 10 Year Note is top watch as we round the corner to last month of the year. Today, after a pre-market ramp, the 10 year found resistance, fueling the relief rally for NAS. NAS found support, after recovering the Daily MBB.

10 Year Bond Yield - Testing .35 Support - in 3DYields were turned away at the monthly H&S neckline (inverted view) to support a NAS and SPX Daily MBB Bounce. NAS resistance at the Daily 8 EMA.

10 Year Bond - Challenging Monthly ResistanceAnother rejection of this zone is needed to reverse the consolidation in the NAS. If this breaks watching for a back-test and the potential of a pressure valve to the upside for rates.

10 Year Note in 3D - Breaking Resistance to New HighsAfter an 11% move from the Higher Low on 11/19, the 10 Year Bond has gained and back-tested the channel .382. NASDAQ is finding resistance under the 2 hour 8 EMA. The Russell 2000 is in a downtrend with resistance at the 2h MBB.

10 Year Note - Resistance BreakOn watch for a reaction to the larger monthly iH&S neckline and the NASDAQ and Big Tech. MSFT near All Time Highs with AMZN and FB in the middle of their ranges.

US10Y - The MetaVerse of BondsTeh 10 Year Notes Rally, after a series of confirmed Bull Flags, stalled at the larger Fibonacci scaffolding .35. The Monthly view is presenting a massive iH&S, with price at the neckline. A break of this key spot zone would put broader market consolidation on watch.

10 Year Note - Bull Flag Testing Upper BoundWelcome to Opex week; as the 10Y Note catches a demand zone off the H&S neckline. Watching the bullflag boundary as a proxy for the direction of NASDAQ.

Bond Break Out - in 3DAfter setting up a short framed iH&S the 10Y is testing the H&S neckline break. This CPI number was hot and a new paradigm will follow. For now more of the same with NASDAQ's dip being scooped up in the short run. NAS Res at the 2 hour MBB.