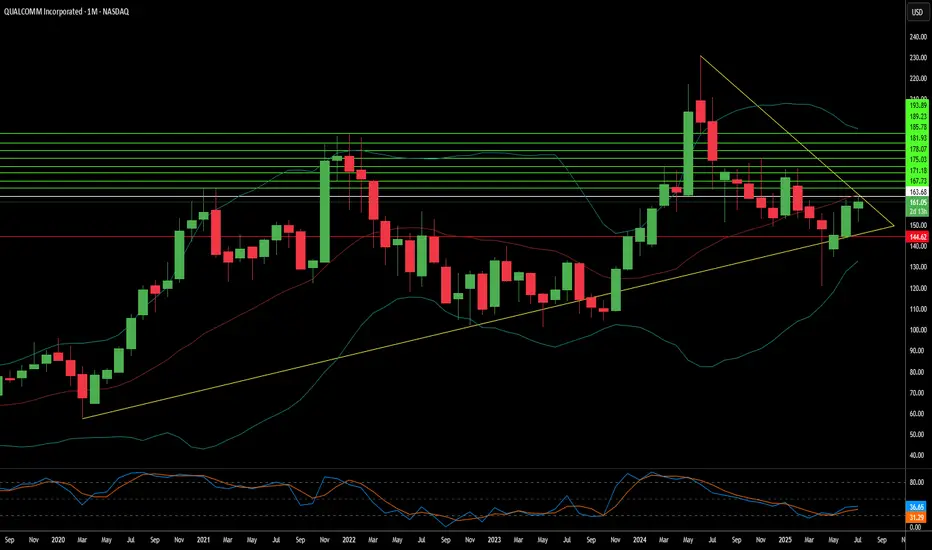

Qualcomm: Beyond the Smartphone Storm?Qualcomm (NASDAQ:QCOM) navigates a dynamic landscape, demonstrating resilience despite smartphone market headwinds and geopolitical complexities. Bernstein SocGen Group recently reaffirmed its "Outperform" rating, setting a \$185.00 price target. This confidence stems from Qualcomm's robust financials, including a 16% revenue growth over the last year and strong liquidity. While concerns persist regarding potential Section 232 tariffs and Apple's diminishing contribution, the company's strategic diversification into high-growth "adjacency" markets like automotive and IoT promises significant value. Qualcomm currently trades at a substantial discount compared to the S&P 500 and the Philadelphia Semiconductor Index (SOX), signaling an attractive entry point for discerning investors.

Qualcomm's technological prowess underpins its long-term growth narrative, extending far beyond its core wireless chipmaking. The company aggressively pushes **on-device AI**, leveraging its Qualcomm AI Engine to enable power-efficient, private, and low-latency AI applications across various devices. Its Snapdragon platforms power advanced features in smartphones, PCs, and the burgeoning **automotive sector** with the Snapdragon Digital Chassis. Further expanding its reach, Qualcomm's recent acquisition of Alphawave IP Group PLC targets the data center market, enhancing its AI capabilities and high-speed connectivity solutions. These strategic moves position Qualcomm at the forefront of the **high-tech revolution**, capitalizing on the pervasive demand for intelligent and connected experiences.

The company's extensive **patent portfolio**, encompassing over 160,000 patents, forms a critical competitive moat. Qualcomm's lucrative Standard Essential Patent (SEP) licensing program generates substantial revenue and solidifies its influence across global wireless standards, from 3G to 5G and beyond. This intellectual property leadership, combined with a calculated pivot away from its historical reliance on a single major customer like Apple, empowers Qualcomm to pursue new revenue streams. By aiming for a 50/50 split between mobile and non-mobile revenues by 2029, Qualcomm strategically mitigates market risks and secures its position as a diversified technology powerhouse. This assertive expansion, alongside its commitment to dividends, underscores a confident long-term outlook for the semiconductor giant.

5g

Crown Castle Inc. (CCI) 1WTechnical Analysis

- The weekly chart of Crown Castle Inc. (CCI) shows a potential reversal after a prolonged downtrend.

- A breakout above the descending trendline and consolidation above $110.85 (0.786 Fibonacci) could signal the start of an upward movement.

- Key Resistance Levels: $132.06 – $146.95 – $161.85 – $180.28 – $210.07.

- Key Support Zone: $83.83 - $90.

- CCI and RSI indicators confirm improving sentiment.

A sustained breakout above $110-112 could lead to mid-term growth.

Fundamental Analysis

Crown Castle is one of the largest telecommunications infrastructure operators in the US.

- Stable revenues due to long-term contracts with telecom providers.

- Dividend yield of ~6%, making it attractive for long-term investors.

- 5G expansion and IoT growth create long-term opportunities.

Risks: High debt burden, interest rate impact, and competition with American Tower.

CCI has growth potential if it breaks above the $110-112 zone. However, macroeconomic risks remain relevant.

GSAT - Split and Move to NASDAQ Monday at CloseI closed all my options except some short dated cheap OTM calls and puts in lots of 15 to hold as standard options post split, more as a lotto and protection for shares. I exercised all the 0.5c calls, the profit wasn't that high and it brought my average price down quite a bit.

I have no idea how its going to move post split. Sized for sideways or down. If it does drop farther I'll add after it stabilizes. Long play for me.

Mobix Labs is gearing up for a bull market!We're back with a new stonk after doing about a 7x on SEALSQ! I don't have much time to write an in depth analysis so please do your own research on this company.

Mobix Labs looks to be settling in their growth market, defense contracts signed and a possible acquisition. Earnings are TOMORROW Dec 19th, so of course this is risky - bad earnings could dump the stock significantly. If however, earnings are good and the investor call brings some good news, this one could fly. Technical breakout target is $10 and I like the nice retest on the bull market support band. $2.16 is the first resistance to break and to retest for a first move towards $3.5.

Let's see, remember these are low caps and risky!

MOBX resistance / support flip, target: +100% nextMobix Labs had volatile pa after earnings, an overreaction as revenue was up over 400% beating estimates. They're still at an operating loss, which is normal for a startup.

Story is simple, they did multiple acquisitions this year:

RaGE Systems:

Revenue for 2024: Not specified.

Acquisition Cost: Approximately $2 million in cash, $10 million in Mobix Labs stock, and possible earn-out payments up to $8 million over eight fiscal quarters.

Description: Provides radio frequency joint design and manufacturing services.

J-Mark Connectors Inc.:

Revenue for 2024: Not specified.

Acquisition Cost: Financial terms remain undisclosed.

Description: Specializes in custom interconnect solutions for industries like aerospace, military, and defense.

Spacecraft Components Corp.:

Revenue for 2024: Not specified, but 2023 unaudited revenues were $18.1 million with forecasted growth for the next two years.

Acquisition Cost: Between $18 million and $24 million, with consideration to be paid in a combination of cash and equity, subject to earnout provisions.

Description: Manufactures mission-critical electronics for the aerospace, defense, and transportation sectors.

Now especially Spacecraft Components Corp. is notably as they do 18.1 million in revenue and are worth roughly 22 million. Mobix Labs reported about 3 million in revenue yesterday.

This means they will do 7x the revenue after the acquisition is completed in Q1 2025. Next to that they secured the following contracts in 2024 that are not part of the current revenue:

In 2024, Mobix Labs, Inc. secured the following contracts:

M-1 Abrams Tank Army Contract: for filtered connectors.

Sole Source Supply Contract: with Gulfstream Aerospace Corp. for custom filtered connectors used in their business-jet aircraft.

GE HealthCare and PerkinElmer Contract: for the sale of proprietary electromagnetic filtering products used in pharmaceutical diagnostics and digital imaging solutions.

Tomahawk Missile System Contract: for filtered connector parts.

Javelin Missile System Contract: for guidance system components.

A 15-month Contract: to supply critical components for aerospace and defense applications, though specific details about the customer or components were not specified.

EMI Interconnect Solutions: announced new filtered ARINC connectors and secured aerospace customers.

These contracts span various sectors, focusing mainly on military, defense, aerospace, and medical applications.

---

Looks to me this company is undervalued and has a lot of growth ahead in 2025... I added on the dip and any buy under $2 should be good long term.

Short term pa looks like a support resistance flip and a next target of $3.52 - I also like that this stock isn't popular whatsoever, similar to LAES (SEALSQ) when I found it.

A patient hold for me, DYOR, happy holidays!

Taiwan Semiconductor Manufacturing Company (TSM) AnalysisCompany Overview:

TSMC NYSE:TSM is the world's leading semiconductor foundry, driving innovation in advanced chip manufacturing for critical technologies like AI, 5G, and emerging tech markets.

Key Growth Catalysts:

Strategic U.S. Expansion 🇺🇸

Arizona Fab: TSMC’s first 12-inch wafer fab begins 4 nm chip production this month, solidifying its North American presence.

$40 Billion Investment: Demonstrates TSMC's long-term confidence in U.S. chip demand and geopolitical supply chain security.

Production of 3 nm chips by 2028 highlights TSMC’s roadmap for next-gen leadership.

Rising Global Chip Demand 📈

Surging demand from AI, 5G, and cloud computing is driving industry-wide growth.

Key Clients: Apple, Nvidia, and AMD rely heavily on TSMC’s advanced node production capabilities.

Technological Leadership 🚀

4 nm Mass Production (Q1 2025): Positions TSMC at the forefront of advanced node production.

Continued R&D investments strengthen TSMC’s competitive edge in next-gen chip technologies.

Investment Outlook:

Bullish Stance: We are bullish on TSM above $172.00-$174.00, underpinned by its global dominance, strategic U.S. investments, and demand for advanced nodes.

Upside Target: Our price target is $255.00-$260.00, reflecting robust revenue growth, margin expansion, and rising semiconductor demand in AI and 5G markets.

🔹 Taiwan Semiconductor—Powering the Future of Tech! #TSM #Semiconductors #AI #5G

GSAT Update and Plan OverviewI've been long for awhile with my entire position in stock and options paid for with profit from calls and puts worked. I'll will be adding stock and options on dips in a ratio that will match post spilt as to not end up holding non-standard options. The ratio has not been announced yet and I will be actively adjusting positions as needed. I intend to accumulate over the coming years. Good luck if you play. No where but up long term.

I don't have a specific target, but I'm focused on GSAT's FCC spectrum, the Qualcomm partnership, and their terrestrial network. They're developing a new cell modem to utilize Band 53 (n53) in standard handsets, coupled with their Apple deal. The more devices sold, the greater the benefit for GSAT, particularly as climate emergency applications gain attention. This creates a self-sustaining cycle of demand for devices and satellite connectivity.

Investor Day on December 12 could act as a catalyst, especially given recent positive developments like expanded licensing, the Qualcomm partnership, and progress with Apple. Price action may see accumulation leading up to the event as investors position for updates. Post-event, the trajectory will likely depend on the depth of announcements and forward guidance. Given the past month's price consolidation, a breakout above key resistance levels is possible if news aligns with expectations

Is Apple's $1.5B Satellite Deal the Future?In the rapidly evolving world of satellite communications, a transformative partnership has emerged between tech giant Apple and satellite operator Globalstar. This landmark $1.5 billion agreement has the potential to reshape the way we connect in remote and underserved regions, inspiring questions about the future of global connectivity.

At the heart of this deal lies Globalstar's commitment to develop and operate a state-of-the-art mobile satellite services (MSS) network. Backed by Apple's substantial infrastructure prepayment of up to $1.1 billion and a $400 million equity investment, Globalstar is poised to enhance the reliability and coverage of emergency satellite communications for iPhone users worldwide. This strategic alliance not only demonstrates Apple's long-term vision for satellite-based connectivity but also positions Globalstar as a dominant player in an industry that is expected to witness a surge in activity in the coming decade.

As the satellite communications sector braces for the launch of an estimated 50,000 satellites into low-Earth orbit, this Globalstar-Apple partnership stands out as a game-changer. By dedicating up to 85% of its network capacity to Apple, Globalstar is solidifying its role as a critical infrastructure provider, catering to the growing demand for seamless connectivity in remote and underserved regions. This move, coupled with Globalstar's plans to expand its satellite constellation and ground infrastructure, suggests a future where satellite-based services become increasingly integrated into our everyday lives.

The financial implications of this deal are equally compelling. Globalstar projects that its annual revenue will more than double in the year following the launch of the expanded satellite services, marking a significant improvement from its recent financial performance. Furthermore, the company's ability to retire its outstanding senior notes and secure favorable adjustments to its funding agreement highlights the transformative nature of this partnership, positioning Globalstar for long-term growth and stability in the evolving satellite communications landscape.

Vertiv Holdings (VRT) AnalysisCompany Overview: Vertiv Holdings NYSE:VRT is strategically positioned to capitalize on the increasing demand for data center infrastructure, with a particular focus on edge computing and the expanding 5G networks. As companies across various sectors accelerate their digital transformation, Vertiv's role in providing critical infrastructure solutions, including liquid cooling technology, is crucial for the operation and efficiency of modern data centers.

Key Catalysts:

Edge Computing & 5G Growth: The rise of edge computing and 5G networks increases the need for efficient, reliable data center infrastructure, a core competency for Vertiv.

Critical Infrastructure Expertise: Vertiv's leadership in liquid cooling and other essential data center technologies will be increasingly in demand as data centers evolve and expand.

Energy Consumption in Data Centers: With U.S. data centers projected to account for a growing share of electricity consumption, Vertiv’s infrastructure solutions—designed to enhance energy efficiency and optimize operations—are expected to become even more vital.

Digital Transformation: The ongoing shift toward cloud services, AI, and machine learning will fuel greater data center demand, benefitting Vertiv’s business model.

Investment Outlook: Bullish Outlook: We are bullish on VRT above $89.00-$91.00, driven by its market-leading solutions in data center infrastructure and strong growth potential. Upside Potential: Our target range for VRT is $140.00-$145.00, reflecting the company’s strategic position in critical growth sectors like 5G, edge computing, and data centers.

🚀 VRT—Leading Data Center Infrastructure into the Digital Future. #DataCenters #EdgeComputing #5G

HNT HELIUM / DCA / TP & REFILLAfter a nice DCA on this token and a good profit taking, I am starting to re-accumulate as the correction progresses.

Patience always pays off in the end. HNT should go much higher later on, this is just a very successful first bullish move.

Helium is an incredible project in any case, with real use cases, I really like this project (like ANKR & FLUX).

Cisco's Next Chapter Overcoming Challenges Seizing OpportunitiesCisco Systems Inc., a global leader in networking and IT solutions, is undergoing a significant restructuring to navigate the challenging economic landscape and pivot towards higher-growth segments. The company recently announced a major layoff affecting 7% of its global workforce, signaling a shift in strategy.

Financial Performance:

Despite a 10% year-over-year revenue decline to $13.6 billion in its fiscal fourth quarter, Cisco exceeded analyst expectations. Earnings per share (EPS) dipped by 44% to $0.54, but the figures were better than projected, offering some relief to investors.

Strategic Shift:

Cisco’s acquisition of Splunk in March has strengthened its position in the cybersecurity market. The company is focusing on software and security solutions, aiming for higher recurring revenue and reduced reliance on traditional hardware. Cisco's investments in AI and automation are key to its future growth.

Market Reaction:

The market reacted positively to Cisco’s earnings announcement and restructuring plan, with the stock surging in after-hours trading. Investors are optimistic about Cisco's ability to address current challenges and position itself for future success.

5G Ecosystem Role:

Cisco is playing a crucial role in the 5G ecosystem. The company’s strategy includes:

[

Core Network Transformation: Solutions for building and operating 5G core networks.

RAN Solutions: Collaborations with vendors to provide orchestration and automation platforms.

Edge Computing: Investments to enable low-latency applications.

Security: Robust solutions to protect against cyber threats.

Challenges and Opportunities:

The 5G market offers significant opportunities but also poses challenges such as intense competition, complex deployments, and proving ROI to service providers. Cisco's focus on end-to-end solutions, partnerships, and R&D investments is critical to staying ahead.

Conclusion:

Cisco's future hinges on a balancing act between cost-cutting and innovation. The company's ability to adapt to industry shifts, including the rise of 5G and AI, while managing economic and supply chain challenges, will be crucial for long-term success.

Deutsche Telekom - The sleeping giant.Chart painting from the early 21st century, artist Maxi Scalibusa. No investment advice or a recommendation to buy or sell any securities. This is entertainment. Start 16.25 EUR

AGi: 692 Satoshi | $0.054 Articicial Intelprobably one of the outliers in the crypto space with a sensational upside reverting back to ALL TIME HIGHS and beyond

Ericsson: Bullish Bat with MACD Bullish DivergenceWe have a Bullish Bat Visible on the Weekly and Monthly with Weekly MACD Bullish Divergence near the bottom of a Decades Long Range. If we bounce from here to the range top a Partial-Decline will be Confirmed that could likely result in a Breakout to $28.

Ericsson also has a great P/E Ratio to back it up and as a result i have gotten the Jan 19 (413d) 8 C call options that are currently trading at well below a dollar.

Verizon (VZ) bullish scenario:The technical figure Triangle can be found in the daily chart in the US company Verizon Communications Inc. (VZ). Verizon Communications Inc., commonly known as Verizon, is an American multinational telecommunications conglomerate and a corporate component of the Dow Jones Industrial Average. Verizon's mobile network is the largest wireless carrier in the United States, with 120.9 million subscribers as of the end of Q4 2020. The Triangle broke through the resistance line on 23/12/2022. If the price holds above this level, you can have a possible bullish price movement with a forecast for the next 29 days towards 40.32 USD. Your stop-loss order, according to experts, should be placed at 36.58 USD if you decide to enter this position.

Verizon is expected to post earnings of $1.21 per share for the current quarter, representing a year-over-year change of -7.6%.

For the current fiscal year, the consensus earnings estimate of $5.18 points to a change of -3.9% from the prior year. Over the last 30 days, this estimate has changed -0.1%.

For the next fiscal year, the consensus earnings estimate of $5.05 indicates a change of -2.6% from what Verizon is expected to report a year ago. Over the past month, the estimate has changed -1%.

Risk Disclosure: Trading Foreign Exchange (Forex) and Contracts of Difference (CFD's) carries a high level of risk. By registering and signing up, any client affirms their understanding of their own personal accountability for all transactions performed within their account and recognizes the risks associated with trading on such markets and on such sites. Furthermore, one understands that the company carries zero influence over transactions, markets, and trading signals, therefore, cannot be held liable nor guarantee any profits or losses.

INSG LAUNCHING INTO ORIONS BELT FROM GIZA LOLWhat if ...?

THE GREAT PYRAMID & THE GOLDEN RATIO

THIS IS THE KINGS CHAMBER

AT&T - Future Growth and DividendsAT&T (NYSE:T) shares recently fell by approximately 10% after the firm released its second-quarter earnings. Despite better-than-expected earnings per share and revenue, excitement was muted by cash flow issues. Following the current drop, AT&T's stock yields around 7.3 percent. Furthermore, AT&T is dirt cheap again, trading at approximately 7.4 times forward EPS expectations. The market may be overreacting because the most recent earnings report was strong, and the cash flow decrease is most likely a one-time occurrence.

AT&T Financials

Furthermore, the corporation has set a clear strategy for future growth over the next several years. Furthermore, AT&T is recession-proof and may profit from a management shuffle. AT&T's downside looks to be limited, and the stock is appealing in this environment. Multiple growth and other factors might cause AT&T's stock price to rise significantly from here while also paying a sizable dividend.

AT&T announced non-GAAP earnings per share of $0.65, above average projections by $0.03. Revenue of $29.6 billion was also $130 million more than expected. During the quarter, the business added over 800,000 postpaid phone net adds and over 300,000 AT&T Fiber net adds. While AT&T raised its mobile service revenue forecast to 4.5-5 percent, it lowered its free cash flow forecast to the $14 billion range. The headline statistics for AT&T are impressive, but the cash flow drop is depressing. Cashflows are being impacted by heavy expenditures in 5G and working capital requirements. However, inflation is most likely a role, and when the economy recovers, AT&T's cash flow problems may be resolved rapidly.

AT&T's figures were pretty strong. Revenues from standalone companies were $29.7 billion, up 2% from $26 billion in the same period last year. Adjusted EBITDA increased by $175 million, or 1.7 percent, year on year. In the most recent quarter, standalone adjusted EPS climbed by 1 cent to 65 cents. Perhaps most critically, AT&T's core Wireless Service expanded by 4.6 percent year on year and is expected to rise similarly in 2022 and 2023. In addition, we observe certain FCF remarks implying that the decline in FCF is a transient event. While AT&T's performance have remained excellent, and the company has demonstrated persistence in exceeding consensus analyst predictions in recent quarters, this has not prevented the stock from underperforming its competitors.

AT&T's stock has underperformed the market, falling nearly 32% in the previous five years. AT&T's nearest competition, Verizon (VZ), is up marginally over the same time period. T-Mobile US (TMUS) is also higher, while Comcast (CMCSA) has destroyed the competition over the previous five years. If we extend the picture further, we see that AT&T's is down by around one-third during the last 10 years.

How much longer will shareholders have to wait for a genuine management revamp? For many years, AT&T's management has done nothing useful with the corporation. For decades, AT&T's stock has been worse than dead money, and it currently trades at the same price it did in 1996. AT&T has become extremely inefficient and has devolved into a bureaucracy that must be changed fast. AT&T requires new management to restore order and return the firm to growth and profitability. AT&T's previous regime, which we don't want. We'd like an expert. We are looking for someone who will offer a unique perspective and creativity to AT&T. We need someone to turn AT&T around and bring the firm back on track. A management revamp would likely be welcomed by the market.

High Dividend Yield

Furthermore, with its extremely low forward P/E multiple of 7.4, AT&T might experience a slight multiple expansion, resulting in a much higher stock price as time goes on. Even a P/E multiple of nine times, as Verizon has, would result in an increase of around 18% for AT&T. If the company's P/E multiple rises to 10, its share price will grow by around 30%. also, because of the dividend and the potential for numerous expansions. We recommend owning AT&T

HNTUSDTShort to the demand zone.

- bearish trend ( 20 EMA below 50 EMA)

- 10 indicators is showing the second day only bearish fields

- low volume

Alpha opportunity from modem and processor chips monopolySummary

3 years into Covid and the risk of recession starts to outplay the chip shortage story of semiconductor industry. With its unmovable monopoly status in its own specialties, we think there is alpha for Qualcomm against its semiconductor peers . Dominance in modem chips and smartphone processors, the company recently declared another victory as Samsung KRX:005930 gave up the plan of using the self-developed processor Exynos2300 and continue with the latest snapdragon SM8550 for the coming new galaxy S23. Just a few days earlier, another source has also shown that Apple NASDAQ:AAPL might not be able to develop their own 5G modem chip on time, which means until 2023 100% of apple products will continue to rely on Qualcomm for connectivity modem chips (instead of the previous forecast at 20%). Although the smartphone market is expected to go into a bear market for 1-2 years, Qualcomm business should still be able to maintain growth by expanding market share within . Another trend worth note taking is the rapid adoption of electric vehicles that has speeded up the development of smart-automobiles, which as a result dramatically increased the chips consumption for the automobile industry. Qualcomm infrastructure and experience in internet-of-things (IOT) application is going to give them a natural edge to make a monopoly again in car chips , which can be the growth story in the coming 2-3 years.

Albeit claiming monopoly in modem and high-end mobile processor chips, there are plenty of challengers from Taiwan and China especially on the lower-end chips. Among the challengers, Mediatek from Taiwan is rapidly gaining market shares by producing chips for mid-to-low tier smartphones such as Oppo, Vivo and most models of Xiaomi. The price barrier from lower-end chip makers make it hard for Qualcomm to entering the broader IOT market especially for devices that do not require high efficiency and computational power.

Trading discussion

Given the mid to long term positive outlook of Qualcomm, we can trade QCOM from both a short term rebound angle, as well as long term investing perspective . The company is currently trading at PE of 13.5, which is lower than its semiconductor peers. Low PE stocks are more defensive against valuation squeeze under the current increasing interest rate environment. Here are QCOM’s peers current PE for reference:

NASDAQ:AVGO : 23.9

NASDAQ:NVDA : 40.7

NASDAQ:AMD : 28.7

NYSE:TSM : 17.4

Technically speaking, QCOM is still under a bearish trend with the 20 days moving average running below the 50 days, and both pointing downward. The 50 days moving average is still the biggest upside resistance for QCOM with two previous breakout attempts on Apr-28 and May-31 both failed. Currently QCOM is flirting around the 50 days moving average again and we shall closely monitor if the breakout will be successful or not.

Here are some technical levels one should pay attentions to:

Downside support

118.23: Jun-23 dropped to a 52-weeks low

96.17: Jan-17 2020 pre-covid high, which was broken on Jul-30 2020

Upside resistance

136.39: Jul-8 attempt of breaking 50 days moving average

151.2: Apr-28 attempt of breaking 50 days moving average (also the current 250 days level)

Note that short term traders and long term investors can see and use the above levels quite differently. For short term traders, the upside resistance can serve as entry when breakout for trend following, and breaking downside support to exit. On the contrary, long term investors might make use of the downside support as entry to accumulate long positions at lower cost to save up more cost buffer to ride a longer cycle.

BRQS cheapest EV and 5G playBRQS Borqs is a global provider of 5G wireless solutions, Internet of Things and innovative clean energy. It operates in the U.S., India and China.

Borqs and its recently acquired subsidiary, HHE, will jointly develop EV chargers and generators which will be integrated with HHE Smart Load Panel in its solar energy + battery solution.

BRQS Market Cap 35.463Mil

52 Week Range 0.20 - 1.60

The minimum upside potential is 2-3X from here in my opinion.

HNTUSDT 4HThere are endless things beyond what we can see.. 🧿

Chart based on Volume Profile and VWAP :

Entry prices : Green

Sell : Red

Follow me on Tradingview if you don't want to miss my next analysis.

Going so far then I'm going so far.. ⏱

GILT launched next generation SkyEdge IV SatellitesThe latest GILAT Quarterly Report is really significant: looks like a turning point to profitability >>> Dramatic surge in Revenue with Significant Growth potential due to successful launch of the next generation SkyEdge IV Satellites, covering North America, Europe and Asia >>> bringing hyper-fast Next Generation Internet using 5G.

ERIC 5G METAVERSEERIC is gapped up this morning, got filled yesterday during the downturn at a ridiculously low bid, & was up well before market close. As you can see the daily chart is what's used, it was easy to see the turning point on volume looking for swing trade type positions. ERIC is expected to give earnings today & is expected be positive. ERIC has huge upside potential as a Metaverse 5G play. Its low price and huge infrastructure make it perfect to capture the developing metaverse market. Ericsson may not be a "leading" metaverse brand like Facebook, but it's going to grow in the background as it provides the actual bandwidth for the metaverse. This is called the picks & shovels method. Watch this space for MACRO & supply chain plays. Please like & share this post if you want more content like this. *NFA, DYOR Please check the ERIC prospectus before investing real funds*