The Dot-AI BubbleSpeculative bubbles excite traders and investors alike.

NVDA is the absolute winner of the AI craze.

Craze is the sentiment of the market cycle peak.

After craze and euphoria, fear and denial will inevitably flood our minds.

It is nothing more than the never-ending cycle of the economy.

A simple line drawn on a chart spells the ultimate demise for speculation.

NVDA is making all-time-highs. Its performance/momentum however is showing alarming signs of weakness.

Beware. Not all is as it seems.

The very nature of a Bubble is that it defies all measurable mathematics.

NVDA wants more. It wants everything. Just like any other corporation would.

For capitalism, more equals more.

NVDA aims to swallow the entire money supply. Improbable as it may seem, physics theoretically allows that.

Divergence is one of the most misunderstood concepts in analysis. Divergence is not describing a future weakness. It describes the current weakness.

NVDA is moving so fast, that its bear market is itself growing exponentially.

If NVDA is now moving slower now than it was in 2015-2018, how fast is it trying to go?

NVDA remembers the explosiveness of that period, and is trying everything to repeat it.

Prices and investors have memory. Both however forget the well-known saying.

Past performance does not guarantee future performance.

This is the Achilles' heel of prices. They promise what they cannot deliver.

Price will reach as high as possible, for as long as there is a willing buyer to take the bait.

For capitalism, more is better, at all costs. The ultimate cost will certainly be paid.

The last buyer will be the last NVDA bear who will give-in the mania. And that will mark the end.

Tread lightly, for this is hallowed ground.

-Father Grigori

AAPL

Topping Pattern Ahead of Earnings: AAPLNASDAQ:AAPL needs to have a great earnings report on August 1st but it has a topping formation at the moment, after huge speculation from promoting something that is not yet proven to increase sales. You can't take hope to the bank. Speculation occurred as investors assumed that AI would sell more new iPhones in droves. This earnings report will reveal reality one way or another.

There is a negative divergence between the price trend and accumulation/distribution suggesting there may have been quiet rotation against the retail speculation.

AAPL Support and Resistance Levels and Options225 is a major level for AAPL it is shown that a previous support on 225 back in July became a resistance. There is also a spread in the options chain where if the price stays below 225 then 220, 215, and 200 will get sold as well. so far we are still under 225 so we remain bearish. however there is a lot of spread pinned in 220. if we go above 220 we can see 232.5 and 240 but below that we are still targeting 215, 210 and 200.

AAPL expected correction and buying areaDue to an engulfing pattern and completion of 5 wave impulsive Elliott wave pattern, I expect Apple to correct to price levels below in black from where I expect it to rally to new all time high.

AAPl: Breakout and RetestBreakout and Retest

Disclaimer: only for education purposes, no buy or sell recommendation. we are not sebi registered. always discuss first with your financial advisors

$AAPL short term range $242-214Think NASDAQ:AAPL is likely to continue the trend higher here and squeeze up to the $242 level.

Once we hit that, I do think we'll see a sharp selloff back down to the $214 level.

My plan is to enter puts once we hit the top level because I think we should see a swift pullback and there should be large gains to come from that.

I'll update as price action continues to play out.

I'm Long $PEP - new trade, Watch,imitate and make moneyI'm Long on PEP - new trade, Watch,imitate and make money

direction on the chart.

Take a look at my past trades in my signature.

AAPL short to $190-$200 rangeJust pattern recognition encouraged by expected overall markets pullback thanks to US elections.

Apple: Bullish Seasonal Growth ExpectedApple Inc. (AAPL) is trading at $230.54 and higher in the pre-market session, continuing to demonstrate strength as the price embarks on a seasonal growth trajectory that is projected to persist through the first two weeks of August. This anticipated bullish upside aligns with our in-depth analysis of market trends and seasonal patterns.

A significant factor driving this optimistic outlook is the positioning of various market participants. Large speculators, typically institutional investors and hedge funds, are currently holding long positions on Apple. This suggests a strong confidence in the stock’s potential for further gains. On the other hand, retail traders are predominantly positioned on the short side, which often indicates a contrarian opportunity for upward movement as these positions may get squeezed.

Given these dynamics, we see a compelling opportunity to buy Apple stock at the opening of today’s market. The alignment of large speculators' long positions with the seasonal trend enhances the probability of a sustained bullish run. Historical data supports this seasonal growth pattern for Apple, typically seeing a positive performance during this time of year.

Investors should consider the broader market context as well. Apple, as a leading tech giant, often sets the tone for market sentiment. Its robust fundamentals, continuous innovation, and strong consumer demand further underpin the bullish case. Additionally, any positive developments in the broader tech sector or favorable economic indicators could provide additional tailwinds for Apple's stock price.

In conclusion, with Apple trading at $230.54 and higher in the pre-market and supported by a seasonal growth pattern and strong positioning from large speculators, we are poised to capitalize on this opportunity. Entering a long position at the market opening aligns with our analysis and the anticipated bullish trajectory through mid-August. Investors should monitor the stock closely, considering both the seasonal trends and market participant behavior to make informed trading decisions.

✅ Please share your thoughts about AAPL in the comments section below and HIT LIKE if you appreciate my analysis. Don't forget to FOLLOW ME; you will help us a lot with this small contribution.

SPY WEEKLY June 15 2024I have clearly explained the long levels. I am still bullish with all the logics that I have discussed.

If you have any doubts feel free to DM me

NOTE: DO NOT SHORT THE MARKET

APPLE: Bearish Forecast & Outlook

It is essential that we apply multitimeframe technical analysis and there is no better example of why that is the case than the current APPLE chart which, if analyzed properly, clearly points in the downward direction.

❤️ Please, support our work with like & comment! ❤️

Apple is BullishApple is bullish and in an uptrend channel on the daily timeframe.

With today's close will confirm, a break out above the resistance area around 195-200 (to become the new support/demand zone) and a break out of the double-bottom pattern. Target is set to the upper levels of the channel at 250.

Tech stocks in demand 11 July 2024Most of the top holding is in Demand zone along with spy. So technically yes there is no issue with the level.

If it hits your Sl. Take it and move on.

I have shared what I added today

Matter MattersMarkets are liquid. Liquids, by definition, move.

Some of them have moved tremendously well.

These liquids got so strong that they are now considered to be gasses.

Unfortunately for them, gasses are not very dense. They are light and weak.

Apple is the prime example of this important paradigm change.

Until ~2005 Apple tried to strengthen and it magnificently did. It reached the optimal point in its cycle. It began as cold hard ice which is hard to move and turned into dense water. In the last 20 years Apple (and many others) turned into hot liquids that have the risk of evaporation into gas.

Now these hot markets are reaching the end of their cycle...

Gases reach the upper levels of the atmosphere. There they can only turn into rain, or escape into space. Either one of them is bad for markets.

The birthplace of bull markets are rivers lakes and oceans. The end of their life is up in the skies. Market Cycles are just like Water Cycles. They cannot escape the cycle.

Hot markets can only get colder. Remember, space is very very cold and can easily turn growing gasses into falling rain. Investors are now beginning to fear.

And so, they fly to safety. One of these safe havens is Gold, which has performed incredibly these past few months. Inside the equity market however, there are stocks that begin to exhibit incredible signs of resilience (coldness) like BRK.A

Has Berkshire reached the "island of stability"?

If we plot a volume-weighted candle chart, we realize that Berkshire Hathaway has created a massive plateau. A lake in the mountains. A place for investors to swim into.

With ongoing worldwide conflict, investments like these will definitely pull buyers towards them.

Apple is not the only weak. It is a mere example of the many "bubbling" companies that face issues.

Their growth was an example of easy money loose monetary policies. With high yield rates the survival of these bull markets is not guaranteed.

On the other hand Berkshire is not the only one that shows strength.

Companies like Exxon Mobil, an energy company, cannot be easily ignored.

Now compare this massive brick of volume to the following chart:

No words need be spoken.

Matter matters. Not all H2O is identical.

A solid investment needs ample liquidity and warm water.

A long-term investor may seek heavy icebergs, which may take years to melt.

A seller or a reckless trader may look into some of the innumerable gas giants to profit on.

Tread lightly, for this is hallowed ground.

-Father Grigori

Hot Stocks to Watch for Week ending 7/12/2024In this video i break down my favorite picks for week ending 7/12/2024. Im looking to play the majority of these with options! come follow along as we have a diverse group that we analyze each and every week!

APPLE: Will Keep Falling! Here is Why:

Our strategy, polished by years of trial and error has helped us identify what seems to be a great trading opportunity and we are here to share it with you as the time is ripe for us to sell APPLE.

❤️ Please, support our work with like & comment! ❤️

TSMC: Chipmaker Prepares for WarRising tensions between China and Taiwan pose a significant challenge to the global technology supply chain. Taiwan Semiconductor Manufacturing Company (TSMC), a world leader in chip manufacturing, is at the forefront of these concerns. In response to the potential for a Chinese invasion, TSMC has developed contingency plans, including the ability to remotely disable its advanced chipmaking equipment.

This "kill switch" strategy is intended to prevent China from acquiring TSMC's cutting-edge semiconductor technology. Such an event could have a crippling effect on the global tech industry, with companies like Apple potentially facing significant disruptions.

The article delves into the geopolitical factors driving these tensions, the ramifications of a potential invasion of the global tech supply chain, and the ongoing efforts to bolster domestic chipmaking capabilities in Western countries. These efforts aim to reduce dependence on a single source and mitigate the risks associated with geopolitical instability.

While the exact timeline for a potential invasion and the effectiveness of TSMC's contingency plans remain uncertain, this situation highlights the critical need for strategic planning and technological self-sufficiency in an increasingly complex geopolitical landscape.

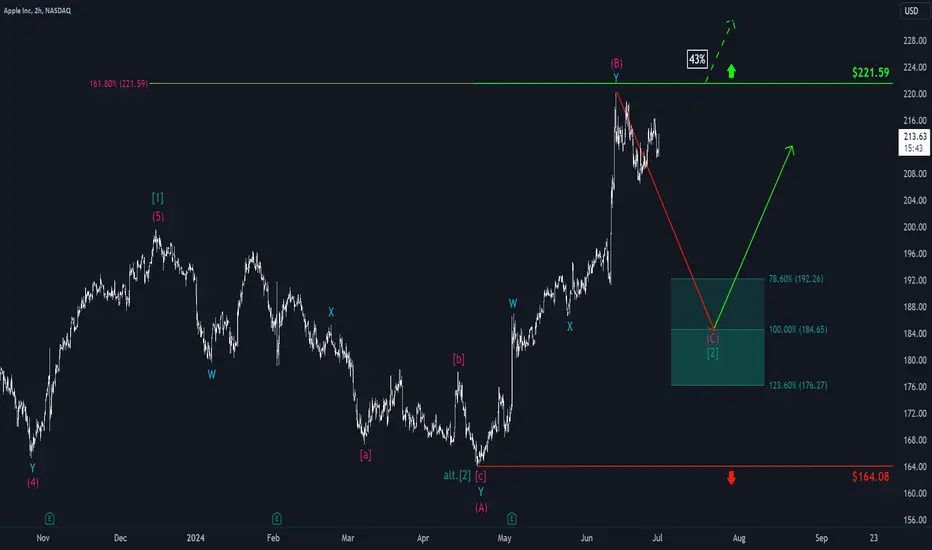

Apple: DownhillApple recently set the high of the corrective wave (B) in magenta just below the resistance at $221.59. The wave (C) should now expand down into our green Target Zone (between $192.26 and $176.27). There the superior green wave (2) should be completed. Subsequently, we expect a reversal and a rise above $221.59. However, please note our alternative scenario (43%) that will come into play on a direct break of this resistance. In this case, the green wave alt.(2) is already complete.

AAPL / Apple - Idea I.Hey guys,

Yearly Chart: Bullish Engulfing

-> Showdown Zone at 228-246 (138.2 &161.8 Fib ext.)

200 Being the First Resistance and 210 the second.

Quarterly: Candle is bullish

-> broke through the ascending triangular pattern and closed above bullishly

-> moreover 210 has been broken and 220 has been tested. -> Some profit taking would be logical but is not necessary since 228 can be seen as the first "real" target. But we will see … 3D chart will show.

-> Stochastic Ind. is OB but pointing up. -actually it is still in a very bullish condition.

Monthly: Bullish close but long shadow.

-> Stochastics has turned up after forming a double bottom

-> Target of 210 has been reached so Monthly traders might take profit as well.

-> looking for Bullish entries after a correction towards 200-190 area.

3D: trend is up with Stochastic turning down

Trendline still bullish

thanks for reading…

219/220 and why it is an issue alt 228219 area plus or minus 1 Has stop AAPL in her tracks reason is we reached major over head resistance and the question is was that the TOP of wave 3 today rally just stopped at a .618 But Cycles and spiral point toward july 5 to the 11th .so if we break above 215.4at anytime I would look for the throwover into the top of the channel that is at 228 plus or minus 1 I have taken a long position this is the second time the first made nice $ best of trades Wavetimer

$NVDA $90 , THEN $75 BY NOVEMBERHere is the 10D chart on NVDA from an example that lead to an approximate 40% decline. We are currently at the same point on the chart in modern day time. Proceed with Caution. Refer to next post.

Apple (AAPL): Bullish Breakout and What to Expect NextApple has broken out above the range between $198 and $165, currently trading around $210. This breakout is seen as very bullish, indicating that we can discard our alternative scenarios. We are confident that Wave (4) completed at $123 and we are now in the larger Wave (5).

Current Situation:

Elliott Wave Analysis: We believe that the initial super sub-wave ((i)) of the larger Wave (5) needs to correct after the strong rise since mid-April.

Correction Levels: We expect a potential pullback to the $185 to $165 range. Whether it will reach as low as $165 remains uncertain.

Confluences:

RSI: The RSI is overbought but without a bearish divergence, indicating continued bullish momentum with a "normal" pullback.

Volume: Support should hold around $175, providing a potential entry point during the correction.

Strategy:

No Immediate Orders: We are not placing any limit orders yet.

Market Report: If we decide to place a limit order, we will issue a market report to inform our group.

The outlook for Apple remains bullish. We anticipate a correction within the $185 to $165 range, with strong support around $175. We will monitor the situation closely and communicate any order placements through a market report.

June 20th Members Daily AnalysisMarkets saw some selling...QQQ finally lagged!

NVVDA almost 8% reversal range. Bearish engulfing

SOXX absolutely bludgeoned.

Oil ripping / NYSE:XOM monster profits.

AAPL PUT / PROFITS SECURED.