SWARMS can be a double digit crypto again.Low risk entry level --- if we assume the bull still has legs.

AI

AI Chip Stocks NVDA and AMD Showing 5 Wave RiseNASDAQ:NVDA and NASDAQ:AMD are both showing 5 wave rise in weekly chart after a correction in WXY. I haven't checked but other AI related stocks also might be doing something similar.

Once the 5 waves are over, we can expect some correction but the 5-wave rise post a correction typically signals fresh uptrend so it might be worth keeping an eye on these stocks. Waiting till retracement/correction of this rise is complete.

$TEM - New ATH's Inbound! 50% UpsideNASDAQ:TEM - New ATH's Inbound! 🚀

Bull Flag Breakout = $84.17 🎯

74.20 Cup&Handle Breakout = $110 🎯

WCB forming 📈

TradeCityPro | ICP Approaches Key Resistance with Rising Volume👋 Welcome to TradeCity Pro

In this analysis, I want to review the ICP coin for you. The Internet Computer project operates in the fields of artificial intelligence and DePIN.

⭐ The coin of this project, with the symbol ICP, has a market cap of 3.25 billion dollars and ranks 32nd on CoinMarketCap.

📅 Daily Timeframe

As you can see in the daily timeframe, there is a descending trendline visible on the chart, which has been tested multiple times. The price has broken above it and is now sitting just below the 6.205 resistance level.

🔍 In recent candles, the volume has increased significantly, which raises the likelihood of a breakout above 6.205.

🔔 If the 6.205 level is broken, ICP's bullish trend could begin. In that case, the price could move toward the 7.423 and 9.887 levels.

📊 Entering a position with the breakout of 6.205 is supported by volume confirmation, and we will get RSI momentum confirmation if it enters the overbought zone.

📉 For the bearish scenario to play out, the price must first get rejected from 6.205, and then we’ll look for confirmation of a trend reversal with a break below 4.468.

🛒 You can also use this same 6.205 trigger for a spot buy, but keep in mind that Bitcoin dominance is still in an uptrend, so in my opinion, it’s not yet the right time to buy altcoins.

✔️ The best trigger for buying any altcoin is to wait for confirmation of a trend reversal in Bitcoin dominance. Once that’s confirmed, you can start buying the altcoins you’ve selected.

📝 Final Thoughts

This analysis reflects our opinions and is not financial advice.

Share your thoughts in the comments, and don’t forget to share this analysis with your friends! ❤️

Are The Markets Running Out Of Steam? SPY just cant seemed to hold above the 600 psychological level.

Are big players unloading into this positive market strength?

Are we due for a larger pullback?

There's a lot of mixed price action and we just cant seem to make a true breakout.

Some names are underperforming and other names are outperforming.

We remain tactically bullish while trimming keys positions into strength.

Being nimble in this market us key as were seeing large intra day swings.

Short term there is some risk of lower price so we have hedged in some individual names while still remaining bullish.

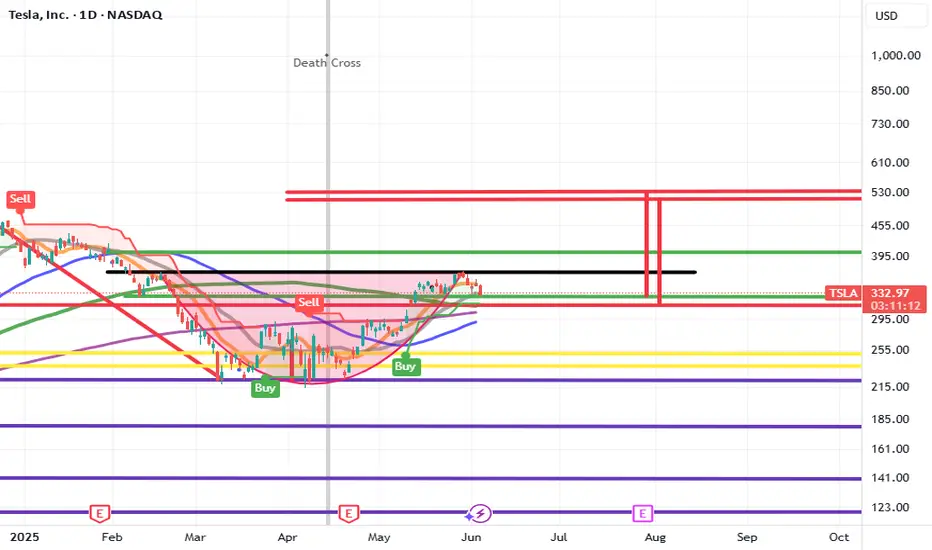

CUP AND HANDLE $TSLA TO $515 MINIMUMThe cup and handle is a bullish chart pattern commonly used by traders to spot potential buying opportunities. It features a rounded "cup" formation followed by a slight downward drift forming the "handle." This pattern typically signals a continuation of an upward trend once the handle completes its consolidation phase.

ROBOTAXI BOOM

BUY NOW NASDAQ:TSLL NASDAQ:TSLA

Bullish Intraday Patterns Everywhere!SPX had a wonderful intraday hourly chart confirmed breakout. This pattern is bullish and likely will continue higher.

The bulls tomorrow would love to confirm the daily chart breakout and will try to push for that.

SPY/SPX is holding more relative strength than the Q's & IWM which is displaying broad participation.

There are many bullish charts showing accumulation, golden crosses and bullish MA crossovers.

The DXY appears to be wanting to break down to around $97.00 which should yield more upside.

We secured profits today on SPY 594 calls & NVDA 144 calls.

We still remain net long and see the S&P 500 over $6000

Apple, XYZ, AI - are bullish setups were continuing to manage.

Technical Analysis: Worldcoin (WLD/USDT) + TRADE PLANTechnical Analysis: Worldcoin (WLD/USDT)

Chart Overview

Pattern: A falling wedge formation is clearly visible, typically a bullish reversal pattern.

Potential Breakout: The price has broken above the upper wedge resistance line, indicating a potential bullish breakout.

Key Levels:

Resistance Zones:

$1.26 (SMA50)

$1.55–$1.65 (major supply zone)

$1.80–$1.90 (final resistance target)

Support Zones:

$1.18 (local support)

$1.00–$1.10 (strong green demand zone)

$0.90 (final downside support)

Indicators & Oscillators

Volume

Volume shows moderate rising interest during breakout—confirmation would be stronger with larger volume spikes.

VMC Cipher B

Momentum waves and money flow are turning bullish.

Green dots at the bottom suggest bullish divergence and likely upward momentum.

RSI (14)

Currently at 52.77, crossing above 50—a bullish signal.

Not yet overbought, so there's room to move upward.

Money Flow Index (MFI)

Reading at 63, indicating strong inflows and increased buying pressure.

Stochastic RSI

Bullish crossover, currently at 66.78/75.27, heading upward—supports the breakout scenario.

Trading Plan

Scenario A: Bullish Breakout Confirmation

Trigger: Close above $1.20–$1.22 with rising volume and continued RSI/MFI strength.

Buy Zone (Spot 1): $1.18–$1.22

Buy Zone (Spot 2): On pullback to wedge breakout line ($1.15–$1.17)

Targets:

TP1: $1.26 (SMA50)

TP2: $1.55–$1.60 (supply zone)

TP3: $1.80 (long-term resistance)

Stop Loss: Below $1.10 (to invalidate breakout)

Risk-Reward Ratio: Minimum 1:2 for TP1, up to 1:4–1:5 for TP3

Scenario B: Failed Breakout / Bearish Rejection

Trigger: Rejection at $1.20–$1.26 and fall below $1.15 with increasing sell volume.

Short Entry (only for experienced traders): Under $1.15

Targets:

TP1: $1.05 (mid-demand zone)

TP2: $0.95–$1.00 (major demand zone)

Stop Loss: Above $1.22

Note: Prefer to stay out if volume is low—wait for clearer structure.

Risk Management & Strategy Notes

Use position sizing: No more than 3–5% of capital per trade.

Be patient—wait for candle close confirmations.

If the price consolidates near $1.20 and volume increases, a strong upward move is likely.

Avoid emotional trading—react to price action, not assumptions.

Worldcoin (WLD/USDT) is showing strong bullish potential with a confirmed breakout from a falling wedge. Indicators support upward momentum, and the structure favors a move toward the $1.50–$1.80 range. Monitor volume and key support levels to manage risk and confirm trend continuation.

Is C3.ai the Quiet Giant of Enterprise AI?C3.ai (AI), an enterprise artificial intelligence software provider, has operated somewhat under the radar despite its foundational role in delivering advanced AI solutions to large organizations. While the broader AI market has seen significant attention on hardware innovators, C3.ai has steadily scaled its platform usage and secured marquee contracts. The company's core strength lies in its sophisticated, patented C3 Agentic AI platform, developed through a multi-billion-dollar investment, which effectively tackles critical business challenges such as AI hallucinations, data security, and multi-format data integration.

A pivotal development underscoring C3.ai's growing influence is the expanded contract with the U.S. Air Force Rapid Sustainment Office (RSO). This agreement significantly increased its ceiling to $450 million through 2029, supporting the widespread deployment of C3.ai's PANDA predictive maintenance platform across the Air Force fleet. This substantial commitment not only provides a robust, long-term revenue stream but also serves as a powerful validation of C3.ai's technology at an unprecedented scale, potentially representing the largest production AI deployment within the U.S. Department of Defense.

Financially, C3.ai demonstrates compelling momentum. The company recently reported record Q4 earnings, with revenue reaching $108.7 million, a 26% year-over-year increase, driven by strong growth in both subscription and engineering services. Strategic alliances with industry giants like Baker Hughes, Microsoft Azure, and Amazon Web Services continue to accelerate new deal flow and expand market access, shortening sales cycles and enhancing overall reach. While profitability remains a near-term focus, C3.ai's solid liquidity and projected revenue growth of 15%-25% for fiscal 2026, coupled with an average analyst price target suggesting significant upside, position it for a compelling ascent in the enterprise AI landscape.

$AI is setting up for a 30% move!C3.AI - NYSE:AI Trade Setup

Inverse H&S Breakout that is now retesting.

A bounce here would confirm the breakout and lead to a MM up to $32.59 for a 30% move!

NVIDIA: 4H Golden Cross starting new Channel Up Leg.NVIDIA is bullish on its 1D technical outlook (RSI = 65.736, MACD = 5.860, ADX = 49.646) as it has established and maintained a Channel Up since its April bottom. The completion of a 4H Golden Cross has validated the start of the pattern's new bullish wave. The previous one topped at +30.58%. With the price already rebounding, we are bullish, aiming for a new HH (TP = 169.00).

See how our prior idea has worked out:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

TradeCityPro | FET: Bullish Weakness Near Key Support Zone👋 Welcome to TradeCity Pro!

In this analysis, I’ll be reviewing the FET coin — one of the popular projects in the AI space.

✔️ This project’s token currently holds a market cap of $1.75 billion and ranks 48th on CoinMarketCap.

⏳ 4-Hour Timeframe

On the 4-hour chart, we can see an uptrend in place. However, in its latest leg up to 0.923, the trend has weakened significantly and lost momentum.

💥 After getting rejected at 0.923, the price saw a deep correction down to 0.718 and failed to form a higher low — a clear sign of weakness in the bullish trend.

🔍 The 0.718 level is a crucial support, and breaking below it could trigger a long-term short position targeting 0.639.

✨ A confirmation for this short setup would be an RSI drop into the oversold zone along with increased selling volume. For now, sell volume is low and offers no confirmation yet.

🔔 On the long side, if the 0.764 level is broken, we can consider that 0.718 has held as support, allowing for a potential long entry.

🧩 In my view, even if this trigger activates and the price moves higher, it’s likely to form a lower high or retest the 0.923 level without breaking it. A breakout beyond 0.923 seems unlikely for now.

📈 For the long setup, RSI confirmation would come with a break above 42.05. As market volume is still declining, we’ll need to wait for increased buy volume to strengthen the bullish case.

📝 Final Thoughts

This analysis reflects our opinions and is not financial advice.

Share your thoughts in the comments, and don’t forget to share this analysis with your friends! ❤️

NVIDIA 1D — When “Head & Shoulders” Aren’t Just for the GymOn the daily chart, NVDA has broken out of the descending channel and reclaimed the 50-day moving average (MA50), triggering a classic inverted head and shoulders formation. Price is now holding above the key $113–$114.50 zone, confirming a structural shift. As volume picks up, buyers are eyeing the next levels of resistance.

Near-term upside targets: – $119.80 (0.5 Fibonacci) – $127.62 (0.382) – $137.28 (0.236) — primary resistance zone – Extended target — $152.91 (1.0 Fibonacci projection)

Technical setup: — Breakout from channel + above MA50

— Inverted head and shoulders pattern completed

— $114.50–$118.00 now acts as buyer support

— EMA and MA convergence supports trend reversal

— Increasing volume on rallies supports bullish momentum

Fundamentals: NVIDIA remains the AI and semiconductor sector leader. Growing demand for high-performance GPUs in AI and data centers positions NVDA as a core tech play. Expectations of strong earnings and continued institutional accumulation support the bullish narrative.

The confirmed breakout and inverted H&S setup mark a clear structural reversal. As long as price stays above $114.50, the path toward $127–$137 remains the primary target zone, with $152.91 in sight if momentum continues.

SPY, SPX, IWM, Natural Gas, NVDA, XYZ, AI - Analysis- Markets sold off into the NVDA rally this morning.

- Small afternoon rally turned indices back green

- Major pre market high levels up ahead likely allow us to push higher in coming days.

- NVDA should retest its premarket high levels.

- Profits secured on AI calls!

- Structurally indices are still bullish and remain above key levels.

- Yields see nasty reversal lower and look to be going down.

- Natural Gas trying to lure investors with a bottoming tail - but i think its false hope.

DR COPPER vs GOLD as a Safe HavenAn enlightening ratio provides additional proof that 2026 is set to be a remarkable year of economic growth, propelling us into the upcoming peak of the #AI cycle.

A key indicator of the AI peak is the initial public offering (IPO) of Open AI on the stock market. This is a definitive signal to capitalise and harvest as much economic energy as possible during the euphoric frenzy, and establish Open AI as a new Tech Titan for the next decade.

$TEM - GET READY! 30%+ UpsideNASDAQ:TEM - GET READY!

✅ Inverse H&S Breakout

✅ Falling Wedge Breakout

🎯 Targets: $77.43 & $90.63 Before August!

AI C3ai Options Ahead of EarningsIf you haven`t bought AI before the previous earnings:

Now analyzing the options chain and the chart patterns of AI C3ai prior to the earnings report this week,

I would consider purchasing the 23.5usd strike price Calls with

an expiration date of 2025-5-30,

for a premium of approximately $1.31.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

BOXCATUSDT Hourly Technical AnalysisBOXCATUSDT Hourly Technical Analysis

Boxcat, one of the newly listed coins, has moved sideways after the initial listing drop. Currently, it is pricing above the 0.0729 support level. In case of a possible reversal, Boxcat coin may present a high profit potential. With indicators also showing a positive outlook, we expect a possible upward movement in the near future. If a rise occurs and the price reaches the 0.10525 resistance level, there could be a profit potential of around 44%.

Resistances: 0.10525 - 0.11718

Support: 0.07290

THIS IS NOT INVESTMENT ADVICE.

The information, comments, and recommendations provided here do not constitute investment advice. Investment advisory services are provided under a contract between the investor and authorized institutions such as brokerage firms, portfolio management companies, and non-deposit banks. The content on this page reflects personal opinions only. These views may not be suitable for your financial situation or your risk and return preferences. Therefore, no investment decisions should be made based solely on the information and commentary provided here.

We’d greatly appreciate it if you follow and like us to avoid missing our analyses with positive or risky technical indicators.

MASA Ascending Triangle (1D) + Key LevelsBITGET:MASAUSDT is currently forming an ascending triangle on the daily chart, with horizontal resistance around $0.040 and rising support.

This structure typically leans bullish and suggests accumulation under resistance.

Structure & Zones

• Resistance: ~$0.040 (triangle top, within flipped demand → supply zone)

• Support: Rising diagonal since early May

• Demand: ~$0.013

• Main Supply: $0.06-$0.09 (High Volume Node, with $0.075 as a key S/R)

Breakout Target

A breakout with strong volume could trigger a measured move toward ~$0.060, aligning with the lower boundary of the High Volume Node (HVN) and the previous price cluster.

Context

The grey $0.06-$0.09 HVN has acted as a pivotal area — both as support and resistance — and could become the next key level if price breaks out.

Triggers

• A clean daily close above $0.040 with volume would be a strong bullish signal

• A breakdown below the ascending support would invalidate the pattern and likely lead to a retest of ~$0.013

DOGE can be worth many DOLLAR'SGrok, the AI supercomputer interface on Elon Musk’s X platform, predicts that Dogecoin might hit $10 between 2029 and 2040.

While I remain hopeful, I believe that a more realistic target could be around 3-5 dollars by the end of this decade. This could potentially trigger a significant blowoff top, leading to an extended bear market for cryptocurrencies.

When you examine this chart, it’s hard not to appreciate its beauty, comparable to Bitcoin, as it showcases a well-defined uptrend and follows cyclical rises and falls. This has resulted in Dogecoin creating numerous millionaires. The pressing question is whether those investors who currently hold 250,000 coins will become the next wave of millionaires in just a few years?

C3.AI has bottomed and is targeting $39.00C3.ai (AI) has been trading within a Channel Down pattern since the June 16 2023 High and right now is testing its 1D MA50 (blue trend-line) as Support, following a bottom (Lower Lows) rebound on April 08 2025.

This is technically the start of its new Bullish Leg, even though based on May - August 2024, it may be delayed. On the long-term though, our Target will be the 0.786 Fibonacci retracement level at $39.00.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

#FETUSDT #4h (Bitget Futures) Falling wedge breakout and retestFetch just regained 100EMA support and looks good for bullish continuation from here.

⚡️⚡️ #FET/USDT ⚡️⚡️

Exchanges: Bitget Futures

Signal Type: Regular (Long)

Leverage: Isolated (4.0X)

Amount: 5.0%

Current Price:

0.7863

Entry Zone:

0.7806 - 0.7504

Take-Profit Targets:

1) 0.8561

1) 0.9244

1) 0.9926

Stop Targets:

1) 0.6897

Published By: @Zblaba

NYSE:FET BITGET:FETUSDT.P #4h #Fetch #AI fetch.ai

Risk/Reward= 1:1.2 | 1:2.1 | 1:3.0

Expected Profit= +47.3% | +83.0% | +118.7%

Possible Loss= -39.6%

Estimated Gaintime= 1-2 weeks