BABA LONG IDEAGood range to fill some long positions on BABA. This is. Weekly and Monthly range to hold. Would expect some sort of reaction in this price range, and easy stop loss to place. Great risk to reward.

Enjoy!

BABA

Alibaba Investment Opportunity (Upcoming)Limit Orders placed for $100 and $86. Super oversold IMO. Super solid fundamentals + Price Evaluation = Steal!

BABA keep going lower???In the past few weeks, BABA keep going lower and lower and lost 65% of its value in the last 58 weeks!

Any sign of recovery?

I'm not able to see any ..!

These green lines are a possible support zone!

You can see the most important support (green lines) and resistance (red lines) to watch in the coming days in these charts!

Best,

Moshkelgosha

DISCLAIMER

I’m not a certified financial planner/advisor, a certified financial analyst, an economist, a CPA, an accountant, or a lawyer. I’m not a finance professional through formal education. The contents on this site are for informational purposes only and do not constitute financial, accounting, or legal advice. I can’t promise that the information shared on my posts is appropriate for you or anyone else. By using this site, you agree to hold me harmless from any ramifications, financial or otherwise, that occur to you as a result of acting on information found on this site.

BABA UPTREND SOONAlibaba dipped so much this year, I think we will see a very big uptrend this upcoming year.

if you have any feedback about the chart pls feel free to tell me:)

MY IDEA ONLY NOT A FINANCIAL ADVICE!!!

Love Yall :)

ali baba is clearing inventory before taking off ali baba is clearing inventory before taking off

sign Ma 200 diverging from sinus wave

BABA heading straight to the "Trend Line" or NOT !!!I do not know if any of this is going to happen, just something for you to consider !!!

Based on 21 Wall Street analysts offering 12 month price targets for Alibaba in the last 3 months. The average price target is $216.10 with a high forecast of $275.00 and a low forecast of $170.00. The average price target represents a 61.55% change from the last price of $133.77.

$BABA Alibaba building this potentially bullish Inverse H&S..Alibaba has been basing in the form of a bottoming reverse head & Shoulders formation. if this plays out as per the textbook we have a target in the region of $216. Keep a close eye and watch for a close above the neckline to confirm the pattern.

AliBaba Poised to loose more ground. BABAWe are still zigzaging on this one. Momentum in the negative, crashing through resistances. I suppose it's only fair given the stellar impulse we have seen earlier.

We are not in the business of getting every prediction right, no one ever does and that is not the aim of the game. The Fibonacci targets are highlighted in purple with invalidation in red. Fibonacci goals, it is prudent to suggest, are nothing more than mere fractally evident and therefore statistically likely levels that the market will go to. Having said that, the market will always do what it wants and always has a mind of its own. Therefore, none of this is financial advice, so do your own research and rely only on your own analysis. Trading is a true one man sport. Good luck out there and stay safe!

ALIBABA BOUNCE FROM TREND LINE Alibaba oversold - RSI is low, historically this has preceded growth.

P/E and P/B are low compared to other industry players and historically. Stochastic RSI was also down so tomorrow may be good for a buy.

Debt to equity ratio decreasing. despite a bit of increased dept from a few Quarters ago.

Let's see what the next few days bring, likely will open a buy position. I will update with TP levels.

Hope you enjoy the idea. Let me know what you think below, anything to add or that I miss?

Good day to you

Hottest topic right now, On daily we still have room to go down!- Probabilities since 2015 we go down by 66% Vs. 34% up.

-If this is an ABC, then C has passed equality of A @ 166

-Weekly demand area 129-147

- Fundamental analysis in running the show here, and it will

take the price back up again not tech.

- Watch smaller time frames for any possible bounce.

baba neutral as highlited in the chart we are currently at a sreogn support formed in 2017 . If this broken future downside expected till 100 ish level .

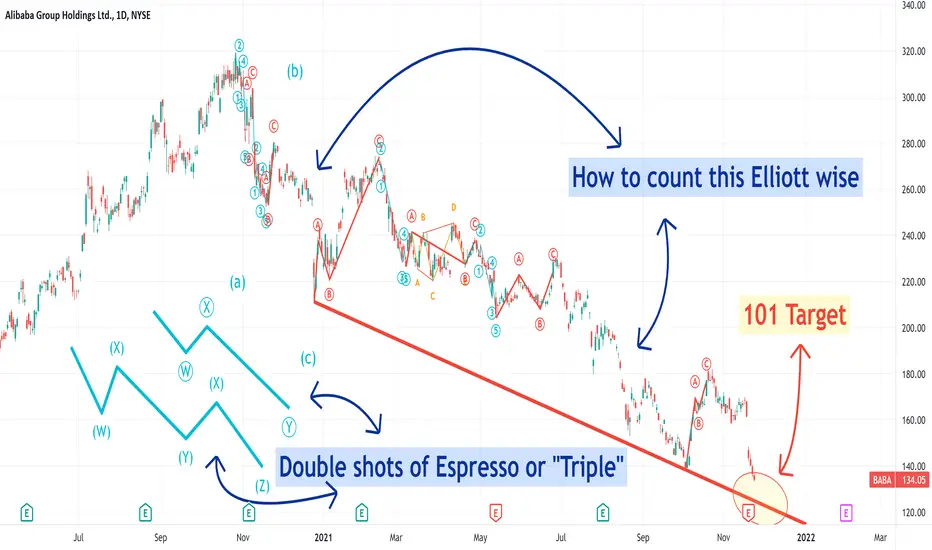

BABA's Elliott wave count, one probable count out of many !!!

Double and Triple ZigZag Rules:

Double (DZ) and Triple (TZ) Zigzags are similar to Zigzags, and are typically two or three Zigzag patterns strung together with a joining Wave called an x Wave, and are corrective in nature. Doubles are not common, and Triples are rare. Zigzags, Double Zigzags and Triple Zigzags are also known as Zigzag family patterns, or 'Sharp' patterns. Double Zigzags are labeled w-x-y, while Triple Zigzags are labeled w-x-y-xx-z. Both these patterns are included in the list of rules and guidelines below. Only a Double Zigzag is illustrated below.

Wave W must be a Zigzag.

Wave C of W cannot be a failure.

Wave X can be any corrective pattern except an ET.

Wave X must be smaller than Wave W by price.

Wave X must retrace at least 20% of W by price.

The gross price movement of Wave X must be less then 3 times the price movement of Wave W.

Wave X must be no more than 5 times Wave W by time.

Wave Y must be a Zigzag

Wave Y must be greater than or equal to Wave X by price.

Back to back and double failures are not allowed.

Wave Y must be greater than 90% of Wave W by price, and Wave Y must be less than 5 times Wave W by price.

Wave Y must be no more than a factor of 5 times either Wave X or W in price or time.

Wave C of Y cannot be a failure.

Wave XX can be any corrective pattern except an ET.

Wave XX must be smaller than Wave Y by price.

Wave XX must retrace at least 20% of Y.

The gross price movement of Wave XX must be less than 3 times the gross movement of Wave W.

Wave Z must be a Zigzag

Wave Z must be greater than or equal to Wave XX by price.

Wave Z must be less than 5 times Wave Y by price, and must also be less than 5 times Wave W by price.

Wave Z must be no more than a 5 times either Waves XX, Y, X or W in both price and time.

Double and Triple ZigZag Guidelines:

The largest Wave in Wave W is usually less than Wave W by price.

Wave X is usually a Zigzag family pattern.

Wave X is usually less than 70% of Wave W by price.

Wave X will usually retrace at least 30% of Wave W.

Wave X is most likely to be a 38.2% retracement of Wave W.

Wave X is next most likely to be a 50% retracement of Wave W.

Wave X is next most likely to be a 61.8% retracement of Wave W.

The largest Wave in Wave X is usually less than 140% of Wave W by price.

The time taken by Wave X is usually between 61.8% and 161.8% of Wave 1.

Wave Y is next most likely to be equal to 61.8% or 161.8% of W by price.

Expect the time taken by Wave Y to be between 61.8% of Wave W and 161.8% of shortest of Wave W and X.

Wave XX is usually a Zigzag family pattern.

Wave XX is usually less than 70% of Wave Y by price.

Wave XX will usually retrace at least 30% of Wave Y.

Wave XX is most likely to be a 38.2% retracement of Wave Y.

Wave XX is next most likely to be a 50% retracement of Wave Y.

Wave XX is next most likely to be a 61.8% retracement of Wave Y.

The largest Wave within Wave XX is usually less than 140% of Wave Y by price.

Wave Z is most likely to be about equal to Wave Y by price.

Wave Z is next most likely to be about equal to 61.8% or 161.8% of Wave Y.

The largest Wave in Wave Z is usually less than Wave Y by price.

BABA's Elliott wave count, # 2 probable count out of many !ZigZag Rules:

A ZigZag is a three wave structure labeled A-B-C, generally moving counter to the larger trend. It is the most common three wave Elliott pattern. Zigzags are corrective in nature.

Wave A must be an Impulse or a Leading Diagonal.

Wave B can only be a corrective pattern.

Wave B must be shorter than Wave A by price. All internal points are considered.

Wave B must be at least 20% of A by price.

Although there is no minimum time constraint for Wave B, it must not exceed 10 times the time taken by Wave A.

Wave C must be an Impulse or an Ending Diagonal.

If Wave A is a Leading Diagonal, then Wave C must not be an Ending Diagonal.

Wave C must be longer than 90% of Wave B by price.

Wave C must be less than 5 times Wave B by price.

It is not allowable to have both Wave 5 of A a failure (Wave 5 is shorter then Wave 4) and Wave 5 of C a failure.

Wave C must be no more than 10 times either Wave A or B in price or time.

ZigZag Guidelines:

It is unusual for a Wave within Wave A to have a greater gross price movement than Wave A.

Wave B should end nowhere near beginning of Wave A

Wave B should retrace at least 30% of Wave A.

Wave B is most likely to retrace Wave A by about 38.2%.

Wave B is next most likely to retrace Wave A by about 50%.

Wave B is next most likely to retrace Wave A by about 61.8%.

The largest Wave in B is usually less than the gross price movement of Wave A.

The time taken by Wave B is usually between 61.8% and 161.8% of the time taken by Wave A.

Wave C is most likely to have a similar price length to Wave A.

The next most likely price lengths for Wave C are 61.8% and 161% of Wave A

The next most likely price length for Wave C is 61.8% of Wave A beyond the end of Wave A.

If Wave C is much longer than 161.8% of A, then the pattern is more probably the beginning of an Impulse than a Zigzag.

If Wave C is complete, and has a greater slope than Wave A, expect the Zigzag to extend to an Impulse.

Although Wave C should always be greater in price to Wave B, in rare cases Wave C can be up to 10% shorter than Wave B.

The largest Wave within C by price is usually less than the gross price movement of Wave A.

The time taken by Wave C is usually between 61.8% of Wave A and 161.8% of the shortest Wave of A and B.

BABAAlibaba is in the correction phase. After having broken the support line, we are correcting Fibo. In search of 61.80% and we still have 78.6% that is at 84 dollars. Now just expect a very visible figure or strong reversal pattern!

DISCLAIMER: Please note that my studies portray my personal opinion only and should be considered for educational purposes only. They should not be considered as a recommendation to buy or sell an asset!

I am not responsible for any damages to your capital. Your capital is at risk in the equity market.

#BABA Alibaba peaking its head under the previous weekly lowAlibaba has peaked its head under the 2018 weekly swing low which is concerning. However on the positive, there does seem to be some degree of bullish divergence with the RSI not making a new low.. so there is potential for a bounce, but bulls will really want the weekly candle to close back above $130 to have some sort of comfort.

BABA has more downside leftPeople who are referring to Charlie Munger , Ray Dalio and other Gurus taking positions in Baba, prove again and again that we are retail herds.

You know their positions for last quarter after 13F filings does anyone know their short positions and Option Strategies.

TV Media / Youtube Videos and other blogs keep spreading the narrative about Baba is available at great valuation and the herd follows the Fundamentals and Shmundamentals.

Its happened in the past and it will keep happening but the way the herd will be played will be different.

Looking at the Technical , there are 2 areas where the price can bounce, around $110 and then around mid 80s. Till then I don't see Bulling Divergences, Not much Volume , and no strong Bulling Patterns.

At Smaller Time Frames like the 1 Hr, there is a bullish pattern forming, but it will not last due to strong Downward trend on the Daily.

There is a chance of another downtrend around Feb earnings season. Then Sideways Consolidation till Aug-Sept 2022.

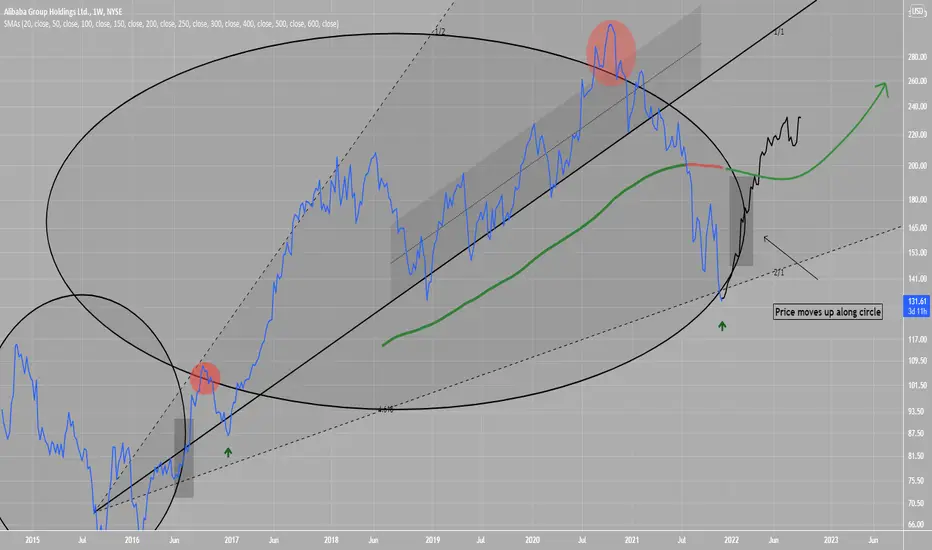

BABA Amazing Long OpportunityBABA has retraced from its all time high a lot

This is ok, as it has provided a lovely buy opportunity (buy the dip)

I expect price to move up along the 4.618 circle, and make a recovery

Attaching my thoughts about how price tends to move up along the circle.

Baba good point for longI see here a good potential for 30-40% gain with a perfect risk ratio.

$BABA

✅ On W chart we come to the strong support line on 130$

✅ Oversold (-60% from ATH)

✅ risk ratio ~3.5

BABA - STOCKS - 18. OCT. 2021Welcome to our Weekly V2-Trade Setup ( BABA ) !

-

4 HOUR

Alibaba group undervalued currently.

DAILY

Most investors panic selling.

WEEKLY

Overall great technical setup!

-

STOCK SETUP

BUY BABA

ENTRY LEVEL @ 168.02

SL @ 151.47

TP @ Open

Max Risk: 0.5% - 1%!

(Remember to add a few pips to all levels - different Brokers!)

Leave us a comment or like to keep our content for free and alive.

Have a great week everyone!

ALAN

BABA break of the downwards channel130 is a level we hav not seen for 3 years. Might head to 150 before testing 130 another time before a breakout.

BABA - time for a shiftShift has come - from this moment on, BABA will start it's rise (my prognosis).

The reason for this assumption is the very positive PE ratio, which was not hurt by the price fall.

BABA seems very healthy financially, as if it was buying out own stocks during the fall.

So my guess is that those who will still the opportunity to get the stocks for 130$, will catch the last train upwards.

I personally doubt that it will really reach the 130$ already, but since there is there are still 2 days till the weekend, it may have enough time to bounce.