Canada's GDP contracts, US nonfarm payrolls misses forecastThe Canadian dollar continues to lose ground against its US counterpart and is trading at two-month lows. In the European session, the Canadian dollar is trading at 1.3875, down 0.13% on the day. USD/CAD has risen for six straight days, climbing 1.9% during that time.

US nonfarm payrolls for July were softer than expected at 73 thousand, compared to the forecast of 110 thousand. The June report was revised sharply downwards to 14 thousand from an initial 147 thousand.

Canada's GDP posted a small decline of 0.1% m/m in May, matching the market estimate. This followed an identical reading in April, as the economy is essentially treading water. A drop in retail trade was a significant factor in the weak GDP reading, particularly in motor vehicles and parts.

The decline in GDP in April and May can be squarely blamed on the trade war with the US, which has put a chill in economic activity. The markets are expecting a slight improvement in June, with an estimate of a 0.1% gain.

The Bank of Canada held the benchmark rate at 2.75% on Thursday for a third consecutive meeting. The rate statement noted that US trade policy remains "unpredictable" and Governor Macklem reiterated this at his press conference, saying that "some level of uncertainty will continue" until the US and Canada reach a trade agreement.

Meanwhile, the trade war between the two sides is heating up. President Trump announced on Thursday that the US was slapping 35% tariffs on Canadian products, effective Aug. 1. The new tariff will not apply to goods covered under the US-Mexico-Canada Agreement.

Canada's Prime Minister Mark Carney said he was "disappointed" with the US decision and vowed that "Canadians will be our own best customer". These are brave words, but Carney will be under pressure to reach a deal with the US, as 75% of Canadian exports are shipped to the US and Canada can ill-afford a protracted trade war with its giant southern neighbor.

BOC

USDCAD Rebound Steadies Ahead of BOC and FOMC MeetingsAligned with the DXY holding above the 96 support and approaching the 100-resistance, the USDCAD is maintaining a rebound above the 1.3540 level.

It has maintained a hold beyond the boundaries of a contracting downtrend across 2025 and is aiming for the 1.38 resistance to confirm a steeper bullish breakout.

A sustained move above 1.38, which connects lower highs from June and July, while the RSI holds below the 50 neutral line, could extend gains toward the 1.40 level.

From the downside, should the breakout above 1.38 fail, the pair may remain trapped within the consolidation range extending from June, with initial support seen at 1.3580.

Written by Razan Hilal, CMT

EUR/CAD: Quant-Verified ReversalThe fundamental catalyst has been triggered. The anticipated strong Canadian CPI data was released as expected, confirming the primary driver for this trade thesis. Now, the focus shifts to the technical structure, where price is showing clear exhaustion at a generational resistance wall. 🧱

Our core thesis is that the confirmed fundamental strength of the CAD will now fuel the technically-indicated bearish reversal from this critical price ceiling.

The Data-Driven Case 📊

This trade is supported by a confluence of technical, fundamental, and quantitative data points.

Primary Technical Structure: The pair is being aggressively rejected from a multi-year resistance zone (1.6000 - 1.6100). This price action is supported by a clear bearish divergence on the 4H chart's Relative Strength Index (RSI), a classic signal that indicates buying momentum is fading despite higher prices.

Internal Momentum Models: Our internal trend and momentum models have flagged a definitive bearish shift. Specifically, the MACD indicator has crossed below its signal line into negative territory, confirming that short-term momentum is now bearish. This is layered with a crossover in our moving average module, where the short-term SMA has fallen below the long-term SMA, indicating the prevailing trend structure is now downward.

Quantitative Probability & Volatility Analysis: To quantify the potential outcome of this setup, we ran a Monte Carlo simulation projecting several thousand potential price paths. The simulation returned a 79.13% probability of the trade reaching our Take Profit target before hitting the Stop Loss. Furthermore, our GARCH volatility model forecasts that the expected price fluctuations are well-contained within our defined risk parameters, reinforcing the asymmetric risk-reward profile of this trade.

The Execution Plan ✅

Based on the synthesis of all data, here is the actionable trade plan:

📉 Trade: Sell (Short) EUR/CAD

👉 Entry: 1.6030

⛔️ Stop Loss: 1.6125

🎯 Take Profit: 1.5850

The data has spoken, and the setup is active. Trade with discipline.

Canada's inflation eases, Canadian dollar edges lowerThe Canadian dollar continues to have a quiet week. In the North American session, USD/CAD is trading at 1.3920, down 0.21% on the day.

Canada released the April inflation report, which indicated that headline and core inflation were moving in opposite directions. Headline CPI dropped sharply to 1.7% y/y, down from 2.3% but shy of the market estimate of 1.6%. This was the lowest annual inflation rate in seven months. The sharp drop was driven by the end of the consumer carbon tax, with gasoline prices dropping 18% lower compared to April 2024.

Core inflation accelerated in April, with two key indicators rising to an average of 3.15%, compared to 2.85% in March. This was above the market estimate of 2.9%.

The money markets have responded to the inflation data, lowering the probability of a rate cut at the June 4 meeting to 48%, down from 65% prior to the inflation release.

The Bank of Canada has been aggressive in its easing cycle, trimming rates seven straight times from June 2024 until April, when it held rates. The cash rate is currently at 2.75% but the BoC is hesitant to lower in the midst of the uncertainty over the US trade tariffs, which have led to sharp swings in the stock markets.

There are no US events on the calendar and the markets will be all ears as a host of FOMC members make public statements today. Investors will be looking for insights into the Fed's rate path. The Fed is widely expected to hold rates in June and may cut as little as twice in the second half of the year. That could change, depending on inflation, the US labor market and Trump's tariffs.

USD/CAD is testing support at 1.3936. Below, there is support at 1.3911

There is resistance at 1.3952 and 1.3977

Canadian dollar shrugs after mixed employment numbersThe Canadian dollar is steady on Friday, after a two-day slid in which the loonie declined by 1%. In the North American session, USD/CAD is trading at 1.3911, down 0.09% on the day. On the data calendar, Canada released the employment report and there are no US economic releases.

The April employment report didn't show much change and the Canadian dollar has shown little reaction. The economy added 7.4 thousand jobs, rebounding from the loss of 32.6 thousand in March and above the market estimate of 2.5 thousand. At the same time, the unemployment rate climbed to 6.9%, higher than the market estimate of 6.8% and above the March reading of 6.7%. This was the highest level since Nov. 2024.

The rise in unemployment is likely a reflection of the US tariffs. Canada's exports to the US were down in March, hurting businesses that export to the US. If the tariffs remain in place, weaker demand from the US could significantly damage Canada's economy.

The Bank of Canada released its Financial Stability Report on Thursday. The BoC said that the financial system was strong but warned that a prolonged trade war between Canada and the US could lead to banks cutting back on lending, which would hurt consumers and businesses and damage the economy. The report said that the unpredictibility of US trade policy could cause further market volatility and was a risk to financial stability.

The Federal Reserve maintained rates earlier this week and Fed Chair Powell said the Fed was in a wait-and-see-stance due to the uncertainty over the US tariffs. We'll hear from seven Fed members on Friday and Saturday, who may provide some insights on where rate policy is headed. The markets have priced in a rate hike in June at only 18%, down sharply from 58% a week ago.

USD/CAD is testing resistance at 1.3928. Above, there is resistance at 1.3935

1.3922 and 1.3915 are the next support levels

Canadian dollar in holding pattern on Election DayThe Canadian dollar is showing limited movement on Monday. In the European session, USD/CAD is trading at 1.3868, up 0.10% on the day. There are no economic releases out of the US or Canada today.

It's Election Day in Canada. Prime Minister Mark Carney, who has only been in office since March, is favored to win the election. Carney's Liberal Party was badly trailing the Conservatives but US President Trump has ignited Canadian nationalism and turned the election race upside down.

Trump has talked about annexing Canada and although most Canadians don't expect that to happen, there is strong resentment against the US tariff policy, which has hit Canada even though the two countries have a free trade agreement.

Carney is viewed as a strong leader who can stand up to Trump and the markets have priced in a Liberal majority. If the Liberals are forced to make a coalition with the smaller parties, the new government would be considered less stable and that would likely trigger some CAD weakness. If the Conservatives manage to pull out a surprise election victory, the Canadian dollar would likely get a boost.

Canada's retail sales declined 0.4% m/m in February but bounced back in March with a strong gain of 0.7%. On an annualized basis, retail sales slipped to 4.7% in February, down from a revised 5.3% in January.

The improvement in March was driven by consumers making purchases ahead of US tariffs, but consumer spending is likely to deteriorate. The Bank of Canada will be keeping a close eye and will have to consider further rate cuts if upcoming economic data is weak. The BoC maintained the cash rate at 2.75% earlier this month and meets next on June 4.

USD/CAD is testing resistance at 1.3868. Above, there is resistance at 1.3880 and 1.3910

1.3850 and 1.3838 are the next support levels

USDCAD Forecast: Key Levels in SightFollowing softer Canadian CPI data, the Bank of Canada held interest rates steady at 2.75%, sending USDCAD toward the 1.3820 support level — an area that aligns with the November 2024 lows and a key resistance zone extending back to the highs of September 2022.

The 1.3820 low aligns with the 0.272 Fibonacci retracement of the uptrend from May 2021 to January 2025. This support also coincides with RSI levels not seen since 2021.

A sustained hold and reversal from this zone may push the pair toward 1.4040, 1.4150, 1.4350, and eventually 1.4500. On the downside, a firm break below 1.3820 could open losses toward 1.3670, 1.3570,1.3430, and 1,3270.

Written by Razan Hilal, CMT

USDCAD - Bank of Canada keeps interest rates unchanged!The USDCAD pair is below the EMA200 and EMA50 on the 4-hour timeframe and is in its descending channel. The continuation of the downward movement of this pair will provide us with a buying position with a good risk-reward ratio. If the correction continues, we can sell within the specified supply zone.

On Wednesday, oil prices climbed by approximately 1%, driven by renewed optimism in the markets regarding potential trade talks between the United States and China. However, lingering concerns about the trade war’s negative effects on global energy demand limited further gains in oil prices.Initially, oil prices declined, but market sentiment shifted after Bloomberg reported—citing an anonymous source—that China was seeking greater respect from the Trump administration before agreeing to new negotiations. The same source also stated that China had requested a new outreach from the U.S. to initiate the discussions.

Giovanni Staunovo, an analyst at UBS, commented that easing trade tensions between the two nations could help reduce constraints on economic growth and energy demand, potentially exerting downward pressure on oil prices.

Meanwhile, the International Energy Agency (IEA) reported that global oil demand is expected to rise by just 730,000 barrels per day this year—well below both its previous projections and those of OPEC.

In a new report, the Fitch rating agency warned that the intensifying global trade war has significantly weakened the outlook for economic growth. According to the report, China’s economic growth will fall below 4% in both this year and the next, while the eurozone is projected to grow by less than 1%.

Fitch further estimates that global economic growth in 2025 will fall below 2%, marking the weakest performance since 2009 (excluding the COVID-19 pandemic period).

Despite the sharp decline in the U.S. growth outlook, Fitch expects the Federal Reserve to delay any interest rate cuts until Q4 of 2025. Conversely, deeper rate cuts are anticipated for the European Central Bank and emerging market economies.

In the energy sector, Fitch lowered its short-term oil price forecast due to risks stemming from weaker demand and trade disruptions but left its natural gas price forecast unchanged.

Additionally, the Bank of Canada maintained its policy rate at 2.75%. Highlights from the Bank’s monetary statement include:

• Tariffs and logistical challenges are driving price increases.

• New U.S. trade policies have heightened uncertainty, slowed growth, and sparked inflation fears.

• The Bank supports economic growth with inflation control but urges caution due to elevated domestic risks.

• Both upside risks (higher costs) and downside risks (weaker growth) to inflation are under close watch.

• Beginning in April, the removal of carbon taxes and cheaper oil are expected to temporarily lower inflation for about a year.

• The recent rise in inflation reflects renewed commodity price growth and the end of temporary sales tax relief.

• Due to high uncertainty related to U.S. trade tariffs, the Bank is refraining from issuing an economic forecast.

• The output gap in Q1 2025 was estimated between 0% and -1%.

• Annualized GDP growth for the same quarter was 1.8%, down from the January forecast of 2%.

• Two scenarios are under consideration: one involving tariff reduction via agreement, and another involving a prolonged global trade war.

• In the first scenario, Canadian and global growth temporarily decline, inflation drops to 1.5%, and later returns to the 2% target.

• In the second, the global economy slows sharply, inflation surges, and Canada enters a severe recession. Inflation surpasses 3% by mid-2026 before returning to the 2% target.

• In both scenarios, the neutral interest rate is estimated to be around the midpoint of the 2.25%–3.25% range.

BOC decision - trading the uncertaintyMarkets are narrowly leaning toward no rate cut from the Bank of Canada this Wednesday. Markets were pricing a 58% chance of a pause as of Friday last week. With traders nearly evenly split, short-term volatility in USD/CAD is possible.

While the Bank had previously signaled it would "proceed carefully" on future rate cuts, that guidance came before the heightened risks tied to the U.S. “Liberation Day” tariff announcements.

From a technical standpoint, there are early signs the pair may be forming a near-term bottom. If the BOC holds rates steady, USD/CAD could retake its 200-day moving average, opening the door for a move toward resistance near 1.4100.

USD/CAD: Rebound Above 1.4265 or Imminent Drop?📊 Market Context

The USD/CAD exchange rate has shown recent volatility with a significant surge followed by a retracement phase. The market is reacting to expectations regarding decisions from the Federal Reserve and the Bank of Canada (BoC), as well as fluctuations in oil prices, a key factor for the Canadian dollar.

🔍 Technical Analysis

The chart analysis highlights the following key levels:

Main Resistance: 1.4521 → Located in the upper zone of the chart, this level could act as a barrier to further bullish movements.

Key Supports: 1.4333 - 1.4265 - 1.4239 → These levels have previously acted as bounce points and could provide a base for price recovery.

Market Structure: The price reacted with a strong green candle after testing the lower support area, followed by a correction phase.

Bullish Momentum: If the price holds above 1.4265, it could attempt another push towards 1.4521.

📌 Potential Bullish Scenario: If the price remains above 1.4265, we could see another push towards 1.45 and beyond.

📌 Bearish Scenario: A break below 1.4239 could trigger a sharper decline towards the 1.41 - 1.40 range.

🌍 Fundamental Analysis

Federal Reserve: The Fed is assessing the impact of its monetary policies, with markets speculating on a potential rate cut by mid-year.

Bank of Canada: The BoC maintains a cautious approach, monitoring inflation and the labor market.

Oil Prices: The CAD is correlated with oil prices, so an increase in crude oil could strengthen the Canadian dollar and push USD/CAD lower.

🎯 Conclusion

Main Bias: Bullish above 1.4265, targeting 1.45.

Trend Invalidation: Below 1.4239, a potential downward correction could occur.

Canadian dollar calm ahead of BoC, US inflationThe Canadian dollar posted gains earlier but couldn't consolidate. In the European session, USD/CAD is trading at 1.4439, up 0.03% on the day.

It's decision day at the Bank of Canada, which is widely expected to lower rates by 25 basis points. This would lower the cash rate to 2.75%, its lowest level since July 2022. The BoC has been aggressive and has lowered rates at five straight meetings, chopping 200 basis points during that time.

The economy remains weak despite the sharp drop in interest rates and the central bank plans to continue lowering rates in order to boost economic growth. The BoC finds itself in a difficult position as far as rate policy. The labor market is showing weakness, with almost no job growth in February, while at the same time inflation remains sticky, above the BoC's 2% target. Throw into the mix the Trump administration's tariffs on Canada, and the situation has become fluid. The specter of a long trade war between Canada and the US would be disastrous for Canada and has complicated matters for the BoC.

In the US, inflation has been contained but remains above the Federal Reserve's target of 2%. Headline CPI for February is expected to ease to 0.3% m/m, down from 0.5% in January, and down to 2.9% y/y from 3.0%. The core rate is projected to drop to 0.3% m/m from 0.4% and to 3.2% from 3.3%.

If the CPI estimates prove to be on target, it would point to little movement in inflation and investors may feel relieved that Trump's tariffs policies have not yet raised inflation. The Federal Reserve is widely expected to hold rates at next week's meeting but it's unclear what happens after that, with the chances of a May cut at around 50/50.

USD/CAD is testing resistance at 1.4445. Above, there is resistance at 1.4511

1.4370 and 1.4304 are the next support levels

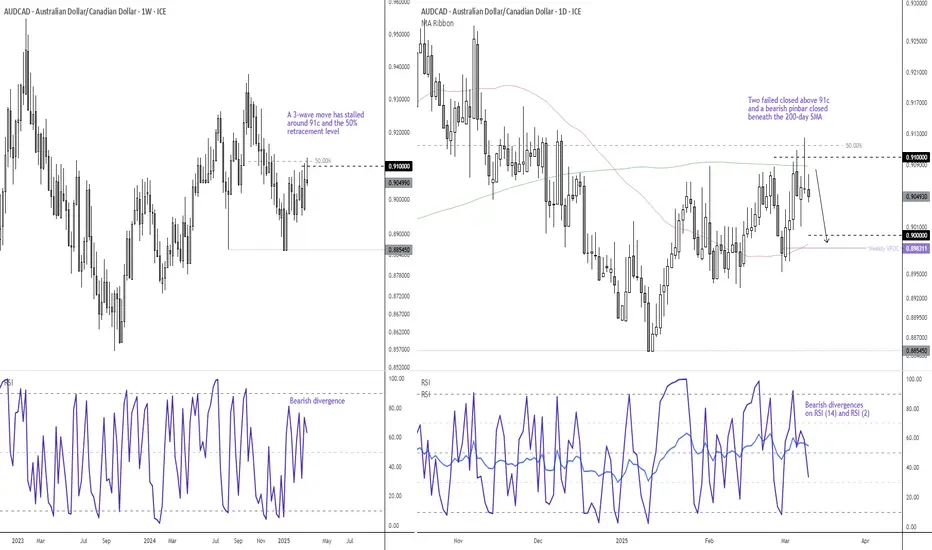

AUD/CAD stalls around 91c, pullback pending?A 3-wave move has developed from the January low, that for now appears hesitant to hold above 91c or its 50% retracement level. Twice we have seen false breaks of the 91c level on the daily chart, and Monday presented a bearish pinbar which closed below the 200-day SMA.

Bearish divergences have also formed on the weekly and daily RSI (14) and daily RSI (2). Perhaps a pullback is brewing.

Bears could fade into moves towards the 200-day SMA, in anticipation for a move down to at least 90c, just above the 50-day SMA and weekly VPOC (volume point of control).

And if the BOC refrain from promising further cuts while delivering an expected 25bp cut tomorrow, it could further strengthen the Canadian dollar and weaken AUD/CAD further.

Matt Simpson, Market Analyst at City Index and Forex.com

Canadian dollar higher as US suspends auto tariffsThe Canadian dollar is steady on Thursday after gaining around 1% over the past two days. In the European session, USD/CAD is trading at 1.4351, up 0.07% on the day. We could see some volatility from the Canadian dollar over the next two days, with the release of the Ivey PMI today and the employment report on Friday.

The Trump tariff saga took a twist on Wednesday, as the US announced it would exempt automakers in Canada and Mexico from 25% tariffs for 30 days provided they complied with existing free trade rules. Trump made clear that the trade war between the US and its two neighbors was not over.

Trump has been shooting from the hip, imposing, suspending, and re-imposing tariffs against Canada. Is this merely a heavy-handed negotiation tactic? If so, chances are good that a deal can be reached and a damaging trade war can be averted. Canada can ill afford a trade war with the US, as some 75% of Canadian exports head to its southern neighbor. A trade war would tip the weak Canadian economy into a recession.

The Bank of Canada is nervously watching as trade tensions escalate between Ottawa and Washington. The BoC has said that a trade war with the US would inflict "permanent" damage on Canada's economy and boost inflation. The BoC is in the midst of an easing cycle and a trade war would complicate plans to futher lower rates.

Canada's Ivey PMI fell sharply in January to 47.1 from 54.7, its first contraction in five months. The PMI is expected to rebound in February, with a market estimate of 50.6, which would point to stagnation. On Friday, Canada and the US release employment reports.

143.75 and 144.19 are the next resistance lines

There is support at 143.00 and 142.56

BYD - What next post-earnings and the BoC's stimulus?HKEX:1211 has had a strong year in growth prospects, reporting solid earnings growth thanks to its robust EV sales and expanding footprint in international markets. The recent earnings beat highlighted an impressive increase in revenue, driven by the demand for both their electric and hybrid vehicles. But what we can notice is that the stock has only reflected this as a c.16% rise in price YTD. However, the question now is: where does BYD go from here?

- More recently, the BoC's latest stimulus measures, including rate cuts and support for the real estate sector, could indirectly benefit BYD. With increased liquidity and consumer confidence, domestic demand for EV's could rise, especially if coupled with additional green energy incentives.

- As for the earnings release, the markets reacted well, and with this new-found optimism in the markets, with both the SEE Composite Index SSE:000001 and the Hang Seng Index TVC:HSI up 5.78% and 9.28% in the past 5 days, is this the turn-around for China as a whole?

USDCAD - Where will the Canadian dollar go?!The USDCAD pair is above the EMA200 and EMA50 on the 4-hour timeframe and is moving in a range. As long as the pair is in this range, the best thing to do is to sell at the top and buy at the bottom. A break of this range to the top or bottom will allow us to continue its rise and fall.

The Bank of Canada has announced its decision to lower the policy interest rate to 3% after six consecutive reductions. Additionally, it confirmed the end of quantitative tightening (QT) and the gradual resumption of asset purchases starting in March. These measures reflect the central bank’s effort to stabilize the economy and support sustainable growth.

The Bank of Canada emphasized three key points:

• Inflation has approached the 2% target. After a period of high volatility, inflation expectations have moderated, and price pressures—except in the housing sector—have eased.

• Lower interest rates have increased household spending power and gradually boosted economic activity, particularly in the housing sector and durable goods purchases such as automobiles.

• New U.S. trade policies remain a significant risk to Canada’s economy. Any escalation in trade tensions could negatively impact economic growth.

One of the first sectors to benefit from the rate cut is the housing market.Lower borrowing costs are expected to attract new buyers; however, the central bank anticipates a more balanced increase in housing prices over time. The recent slowdown in construction activity and declining rental prices indicate that investment appeal in this sector has somewhat diminished.

For investors and entrepreneurs, the lower interest rates present an opportunity to secure cheaper financing and expand their businesses. Sectors such as startups, technology, and export-driven manufacturing are expected to gain the most from this policy.

With inflation stabilizing around 2% and the economy recovering, the Bank of Canada sees no immediate need for further rate cuts. However, potential economic disruptions from U.S. trade policies could alter this outlook.

Reports suggest that if U.S. President Donald Trump proceeds with a proposed 25% tariff on Canadian imports, the Canadian government plans to implement financial aid measures similar to those used during the COVID-19 pandemic. However, these programs require parliamentary approval, and given that the Liberal government lacks a parliamentary majority, there is no guarantee they will pass.

All opposition parties have expressed their intent to oust the current government, meaning any economic stimulus package would require support from the New Democratic Party (NDP). The NDP has backed the Liberal government over the past three years. The Canadian Parliament is currently adjourned until March 24, allowing the Liberal Party to select a new leader to replace Justin Trudeau, with Mark Carney as a likely successor. However, an early leadership decision may occur before the scheduled date.

Tiff Macklem, Governor of the Bank of Canada, stated that household debt is not a sustainable driver of consumption growth. He expressed greater concern about declining business investment due to tariff threats, arguing that such policies could have a more significant impact on the Canadian dollar than interest rate differentials.

He also reaffirmed that the Bank of Canada believes inflation has been successfully contained. The central bank aims to ensure that any CPI increases resulting from tariffs remain temporary and that the consequences of trade policies are managed to minimize sudden economic disruptions.

USDCAD - which direction will the Canadian dollar go?The USDCAD currency pair is above the EMA200 and EMA50 in the 4-hour timeframe and is moving within the range. The correction of this currency pair towards the demand zone will provide us with the next buying position. The upward movement of this currency pair will make its selling positions attractive.

Canada has initiated efforts to mitigate the economic impacts of new U.S. tariffs. These measures include the creation of a critical minerals management unit and defense procurement activities.

Prime Minister Justin Trudeau emphasized that Canada would respond firmly and decisively if the U.S. imposes tariffs. Bloomberg reported that Canada is prepared to impose tariffs on $105 billion worth of American goods should the U.S. act first. Quebec’s Premier stated that no official announcements about retaliatory actions would be made until Trump’s plans are clearer, but no options are off the table. Ontario’s Premier added that any retaliatory measures against the U.S. must be stringent.

Donald Trump, the U.S. President-elect, campaigned on promises such as imposing heavy import tariffs, tightening immigration policies, reducing regulations, and downsizing the government.However, the economy he is set to oversee may require a different approach from the policies implemented in 2017.

Currently, the U.S. economy is growing at an above-average pace, unemployment is near full employment, and inflationary pressures remain significant. This suggests that the U.S. economy might not need fiscal stimulus measures like tax cuts. Furthermore, high asset valuations and rising bond yields could expose the economy to sharper corrections.

When Trump took office in 2017, the U.S. economy was still recovering from the 2007-2009 financial crisis. Policies such as tax cuts and import tariffs had varying impacts then. However, today, inflation remains above the Federal Reserve’s 2% target, mortgage rates are near 7%, and government bond yields are close to 5%. These rising yields may reflect market concerns about inflation control and America’s fiscal discipline.

In a recent Reuters survey, 25 out of 31 economists predicted that the Bank of Canada would cut interest rates by 0.25% at its January 29 meeting, while the remaining six expected rates to stay unchanged.

Gravelle, Deputy Governor of the Bank of Canada, stated that quantitative tightening (QT) is expected to conclude in the first half of 2025. He noted that ending QT would require settlement balances to rise to a range of CAD 50-70 billion, up from the previous estimate of CAD 20-60 billion. Treasury bond purchases are set to commence in the last quarter of this year, initially in small volumes.

Following the release of recent data, projections for real personal consumption expenditures in Q4 have risen from 3.3% to 3.7%, while real government spending growth for the same period increased from 2.9% to 3%. However, forecasts for real private domestic investment growth have been revised downward from -0.4% to -0.8%.

In its updated forecast, Wells Fargo indicated that the Federal Reserve would cut interest rates twice this year by 0.25%, once in September and again in December. Previously, three rate cuts were anticipated for the year.

USD/CAD in holding pattern ahead of US, Cdn. jobs dataThe Canadian dollar started the week with strong gains but has shown little movement since then. In the European session, USD/CAD is trading at 1.4411, up 0.12% at the time of writing. We could see stronger movement from the Canadian dollar in the North American session, with the release of Canadian and US employment reports.

Canada's economy may not be in great shape but the labor market remains strong. The economy added an impressive 50.5 thousand jobs in November and is expected to add another 24.9 thousand in December. Still, the unemployment rate has been steadily increasing and is expected to tick up to 6.9% in December from 6.8% a month earlier. A year ago, the unemployment rate stood at 5.8%. This disconnect between increased employment and a rising unemployment rate is due to a rapidly growing labor market which has been boosted by high immigration levels.

Another sign that the labor market is in solid shape is strong wage growth. Average hourly wages have exceeded inflation and this complicates the picture for the Bank of Canada as it charts its rate path for early 2025. The BoC has been aggressive, delivering back-to-back half point interest rate cuts in October and December 2024. Inflation is largely under control as headline CPI dipped to 1.9% in November from 2% in October. However, core inflation is trending around 2.6%, well above the BoC's target of 2%. The central bank is likely to take a more gradual path in its easing, which likely means that upcoming rate cuts will be in increments of 25 basis points. The BoC meets next on Jan. 29.

In the US, all eyes are on today's nonfarm payrolls report. The market estimate stands at 160 thousand for December, compared to 227 thousand in November. The US labor market has been cooling slowly and the Federal Reserve would like that trend to continue as it charts its rate cut path for the coming months. An unexpected reading could have a strong impact on the direction of the US dollar in today's North American session.

USD/CAD is testing resistance at 1.4411. Above, there is resistance at 1.4427

1.4388 and 1.4372 are the next support levels

USDCAD: political crisis and tariff crisis in Canada!The USDCAD currency pair is above the EMA200 and EMA50 in the 4-hour timeframe and is moving in its upward channel. The correction of this currency pair towards the demand zones will provide us with the next buying position.

The political crisis surrounding Justin Trudeau is deepening, with an increasing number of Liberal Party members publicly calling for the Canadian Prime Minister to step down and allow a new leader to take charge before the 2025 elections.

Chad Collins, a Member of Parliament from Ontario, stated that nearly 50 elected Liberals are part of a growing group advocating for Trudeau’s resignation. Other Liberal opponents have reported similar numbers, representing approximately one-third of the 153 Liberal MPs in the House of Commons.

The resignation of Chrystia Freeland, Trudeau’s influential Finance Minister and longtime deputy, has been a significant blow to the Prime Minister. Collins remarked that this resignation has caused irreparable harm to Trudeau.

Freeland explained that she decided to resign after being informed of a reassignment within the cabinet. She mentioned that Trudeau informed her of the decision only three days before an important speech intended to update the nation on its financial and economic status.

Criticizing Trudeau’s leadership, Collins said, “I don’t know who is advising him, but I can guess. This advice is far from effective. Ultimately, he is responsible for his decisions, and we are now witnessing consequences that many consider to be a clear demonstration of poor judgment.”

Trudeau, now 52, has been under mounting pressure to resign for months. In June, the Liberals lost a by-election in a Toronto district they had held for decades. Similarly, they lost another seat in Montreal in September. However, Freeland’s resignation, amid economic threats posed by Trump’s incoming administration, has turned discontent into a full-blown crisis for Trudeau. The Prime Minister has canceled all of his usual year-end television interviews. Collins warned that more Liberals would exit politics if Trudeau insists on staying in power.

Meanwhile, Ian de Verteuil, an equity strategist at CIBC Capital Markets, discussed Donald Trump’s tariff threats against Canada in an interview with Bloomberg. He argued that Trump’s threat to impose sweeping tariffs on Canadian imports on his first day in office could hurt American consumers and is unlikely to proceed without major revisions.

De Verteuil emphasized that Trump should be taken seriously, though not always literally. He added that Trump’s slogan, “Make America Great Again,” would be put to the test if a 25% tariff were imposed on Mexican and Canadian goods. Such tariffs could harm American consumers and are unlikely to be implemented.

He further noted that tariffs are unlikely to target fossil fuels or auto parts from Canada, given the U.S. economy’s heavy reliance on these imports. However, companies exporting consumer goods such as clothing and vehicles to the U.S. are at greater risk.

De Verteuil also highlighted that Mexican companies exporting goods to the U.S. would face more significant impacts, as Trump’s border concerns primarily focus on America’s southern neighbor. In conclusion, he stated that Canada remains a vital trade partner for the U.S., and major challenges for Canada in 2025 are highly improbable.

USD/CAD steady ahead of retail salesThe Canadian dollar is showing limited movement on Friday. In the European session, USD/CAD is trading at 1.4384, down 0.11% at the time of writing. On Thursday, the Canadian dollar fell to its lowest level since March, touching 1.4435.

Canada retail sales have risen for four consecutive months and the trend is expected to continue today, with a market estimate of 0.7% m/m.

The economy outlook remains gloomy and the Bank of Canada is expected to continue lowering rates in order to boost the weak economy. The BoC has been aggressive, cutting rates five times since June for a total of 175 basis points. The central bank slashed the benchmark rate by 50 basis points to 3.25% last week but signaled that it plans a "more gradual approach to monetary policy", which means we can expect 25-bp increments in rate cuts if there are no surprises in inflation or employment data.

The "gradual approach" sounds a lot like what we're hearing from the Federal Reserve, which surprised the markets on Wednesday when it lowered its forecast to just two rate cuts in 2025, compared to four cuts in the September projection. The US dollar soared after the rate announcement and the Canadian dollar took it on the chin with losses of around 1% on Wednesday.

The incoming Trump administration could be a major headache for Canada, as Trump has pledged to slap tariffs on Canadian products. The Canadian government has announced enhanced security measures at its border with the US, hoping these moves will encourage Trump to suspend his tariff plans. Canada's Finance Minister Chrystia Freeland resigned earlier this month after a bitter row with Prime Minister Trudeau, which has added political uncertainty that could weigh on the wobbly Canadian dollar.

USD/CAD tested resistance at 1.4404 earlier. Above, there is resistance at 1.4463

1.4341 and 1.4282 are the next support levels

USDCAD - CAD Vs tariffs!The USDCAD currency pair is above the EMA200 and EMA50 in the 4H timeframe and is moving in its upward channel. The correction of this currency pair towards the demand zone will provide us with the next buying position. You can sell up to the bottom of the ascending channel within the specified supply zone with the appropriate risk reward.

The Canadian dollar has underperformed against other currencies this year, largely due to the Bank of Canada’s consistent interest rate cuts. It is expected that the central bank will lower interest rates for the fifth time in December, though the likelihood of a 50-basis-point cut has diminished following a higher-than-expected inflation report.

The Royal Bank of Canada (RBC) and the Canadian Imperial Bank of Commerce (CIBC) still foresee the possibility of a larger rate cut. Meanwhile, per capita GDP data reveals that economic growth has declined for the sixth consecutive period. Monthly GDP figures indicate that growth in September and October was only 0.1%.

According to CIBC, domestic demand remained relatively stable during this time, comparable to the previous quarter. However, monthly data shows that the third quarter ended with gradual deceleration rather than the sharp rebound initially expected, leading to significantly lower fourth-quarter forecasts compared to the projections in October’s Monetary Policy Report (MPR).

RBC maintains its prediction of a 50-basis-point rate cut but has stated that Friday’s employment report will be closely monitored ahead of the central bank’s December 11 meeting.

“GDP numbers reinforce the notion that current interest rates are higher than necessary to maintain inflation at the 2% target. The Bank of Canada will also closely monitor next week’s labor market data, but a further 50-basis-point cut in December is likely,” an analyst remarked.

Currently, the Bank of Canada projects 2% GDP growth in the fourth quarter, but this figure is likely to be revised downward. With government forecasts suggesting population declines, the central bank may adopt a more cautious approach for 2025.

Deputy Governor Mendes of the Bank of Canada stated that inflation is gradually easing and will eventually stabilize at 2%. Lower inflation will boost consumer and business confidence, encouraging spending and investment. If the economy evolves as anticipated, further rate cuts could be possible. However, he emphasized that decisions will be made step-by-step, considering both above-target and below-target inflation. Mendes warned that additional measures to curb inflation might hurt economic growth, with potentially more negative long-term consequences than short-term benefits.

According to Axios, a senior Canadian Liberal minister involved in Sunday’s negotiations stated that Canadian officials plan to “visibly and robustly” enhance border security following a meeting between Prime Minister Justin Trudeau and President-elect Trump. Trump previously threatened to impose tariffs on Canada and other countries due to his concerns over migrants and drugs entering the U.S.

Dominic LeBlanc, Canada’s Public Safety Minister, told CBC Radio and Television that Canadian officials met with Trump and Commerce Secretary nominee Howard Lutnick to discuss tariffs and their implications for the economy. LeBlanc stressed that existing border security cooperation remains strong but noted concerns over firearm smuggling from the U.S.

LeBlanc also shared that during an informal dinner with Trudeau, Trump jokingly suggested that Canada become the 51st U.S. state. He clarified that the comment was made in jest and was not meant seriously.

Canada’s job growth sparkles but Canadian dollar fallsThe Canadian dollar can’t find its footing and is trading at nine-week low against the US dollar. In the North American session, USD/CAD is trading at 1.3792 at the time of writing, up 0.21%. The Canadian dollar has recorded eight straight losing sessions and is down 1.9% in October.

The week ended on a high note, as Canada’s employment growth jumped by 46.7 thousand, crushing the market estimate of 27 thousand and sharply higher than the August reading of 22.1 thousand. Full-time employment surged by 112 thousand, following a decline of 43.6 thousand in August, while the unemployment rate dropped from 6.6% to 6.5%.

The impressive numbers couldn’t stop the Canadian dollar’s nasty slide but it will please Bank of Canada policymakers. The central bank has shifted its primary focus from inflation to risks to the labor market, now that inflation has been largely contained. In August, CPI dropped to 2%, its lowest level since February 2021.

The BoC meets next week and has a tough decision to make. The drop in inflation raised the odds of a 50-basis point cut but Friday’s employment report was stronger than expected and supports the case for a modest 25-bps cut. The BoC has been aggressive in its rate-cutting cycle and has lowered rates three times this year in a bid to ease the pressure of elevated rates.

The Federal Reserve has been late to the rate-lowering party, delivering its first rate cut in September. Still, the oversized 50-basis point cut in September signaled that the Fed means business and isn’t afraid to slash rates with large cuts. The Fed is expected to trim rates by an additional 50 or 75 basis points before year’s end. The most likely scenario is rate cuts of 25 bps in both November and December. The Fed could, however, deliver one more 50-bps cut if employment or inflation numbers are lower than expected.

USD/CAD has pushed above resistance at 1.3758 and is testing resistance at 1.3790. The next resistance line is 1.3817

1.3731 and 1.3699 are the next support levels

AUD/USD – Australian retail sales flat, Aussie shrugsThe Australian dollar continues to have a quiet week. AUD/USD is trading at 0.6804 in the European session, up 0.09% today at the time of writing.

Consumer spending in Australia has been weak, which has chilled economic activity. Retail sales for July didn’t provide any relief with a reading of zero, shy of the market estimate of 0.3% and well off the June gain of 0.5%. Consumers continue to feel squeezed by elevated interest rates and the high cost of living. The weak economy and a cooling labor market are making consumers even more cautious about discretionary spending.

Will today’s soft data prod the Reserve Bank of Australia to consider a rate cut? The RBA is frustrated with the slow decline in inflation - Governor Bullock has said that the central bank is unlikely to cut for six months and RBA members have been discussing a possible rate hike at recent meetings. The markets are marching to a different tune and have priced in a rate cut in November with more cuts early next year.

The remaining tier-1 events ahead of the Sept. 24 policy meeting are GDP and the employment report and both releases will be important factors in the rate decision. If these numbers are weaker than supported, it would support the case for a rate cut before year’s end.

The week wraps up with the US Core PCE Price index, considered the Federal Reserve’s preferred inflation indicator. The markets are expecting a small increase in July – from 2.5% to 2.6% y/y and 0.1% to 0.2% m/m. A small move is unlikely to concern the Fed, which has shifted its focus to the weakening labor market now that the battle with inflation is largely over.

AUD/USD is testing resistance at 0.6808. Above, there is resistance at 0.6822

0.6776 and 0.6754 are providing support

Canadian dollar jumps on retail sales reboundThe Canadian dollar is showing some strength on Friday. In the North American session, USD/CAD is trading at 1.3532 at the time of writing, down 0.60% on the day. The Canadian dollar is at its highest level since early April and is poised to post its third winning week in a row.

Canada’s retail sales report was a mix. In June, retail sales fell 0.3% m/m, confirming the initial estimate and following a May reading of -0.8%. However, the initial estimate for July jumped 0.6%, which would indicate a much-needed rebound in consumer spending.

Retail sales were down 0.5% in the second quarter and 0.4% in Q1, which would mark the weakest two quarters since 2009, outside the covid pandemic. The spike in July is likely due to the Bank of Canada’s quarter-point rate cuts in June and July, bringing down the benchmark rate to 4.5%. The BoC is expected to continue to trim rates as inflation has eased and the labor market shows signs of decline.

The annual Jackson Hole meeting has begun and the highlight of the summit will be today’s speech from the host, Fed Chair Jerome Powell. The markets are all ears, although it would not be a surprise if Powell’s speech is little more than a cautious acknowledgment that inflation is moving in the right direction and that the Fed is poised to cut at the Sept. 18 meeting. The markets have fully priced in a rate cut at next month’s meeting, with the odds at 71% for a 25-basis point cut and 29% for a 50-bps cut, according to CME’s FedWatch.

There’s a strong chance that the Fed will deliver additional cuts before the end of the year, but recent employment data has been very weak and that could delay further rate cuts. The next employment report on Sept. 6 will be a key factor in determining the Fed’s rate path.

USD/CAD has pushed below support at 1.3578 and is testing support at 1.3538. Below, there is support at 1.3478

There is resistance at 1.3628 and 1.3653