USD/JPY breaches 150USD/JPY is almost unchanged today but hit a milestone in the Asian session as it briefly darted above the 150 line, which has psychological significance. This marked the yen's lowest level since August 1990 as the currency continues to slide. The yen hasn't recorded a winning session since October 4th and has plunged about 600 points during this period. Later today, Japan releases Core CPI for September, which is expected to rise to 3.0%, up from 2.8% in August.

The Bank of Japan holds its policy meeting next week, but it seems unlikely that it will change its ultra-loose policy. The yen is sinking and inflation is above the Bank's 2% target, but the central bank is fixated on continuing to provide massive stimulus in order to support the weak economy. Earlier today, Japan's 10-year government bonds breached the 0.25% cap which the BoJ has fiercely defended, rising as high as 0.264%. The BoJ has responded with an emergency bond-buying package in order to bring yields back below 0.25%.

With the BoJ defending its policy and ignoring the yen's descent, the ball is in the court of the Ministry of Finance (MoF). The MoF dramatically intervened in late September to prop up the yen after it fell below 145, but the move did little more than slow the yen's descent for a few days. Another intervention is possible, but it would have to be on a larger scale to have any substantial effect on the exchange rate. Finance Minister Suzuki has warned that the government would "properly respond" in the currency markets, but increasingly, the verbal bullets out of Tokyo are being viewed as blanks. With the Federal Reserve showing no signs of easing up on oversize rate hikes, the yen remains at the mercy of the US/Japan rate differential, which continues to widen. The yen's prolonged downturn looks set to continue, with the currency likely to hit new lows.

USD/JPY is testing support at 149.81. Below, there is support at 149.09

There is resistance at 150.04 and 151.32

Boj

The If, When, How of the BoJ interventionAs the Yen continues to weaken, the market consensus is that the BoJ is most likely to intervene when the price hits the round number level of 150.

Understanding the previous time the BoJ intervened (non stealth) on 22nd September 2022, there are a few learning points to note:

- The market consensus price level then was 145. However, the BoJ intervened only when the USDJPY climbed to reach 145.90. ( Noteworthy : A hard and fast number probably isn't what the BoJ is paying attention to, OR market consensus is generally wrong)

- The BoJ is deemed to have intervened (stealth) twice more since the 22nd September 2022 (13th & 18th October). But these saw lesser price volatility and were quickly and easily reversed. ( Noteworthy : Stealth intervention doesn't seem to work well)

- The BoJ intervention on 22nd September was after the BoJ policy report and the actions were announced by the BoJ. ( Noteworthy : The next BoJ policy report is soon! On the 28th October)

How to prepare and take advantage of a BoJ intervention?

- Utilise a sell stop pending order.

- Judging from the previous intervention which had more than 500pip move and almost no whipsaw; you could apply the pending order below the round number level (in this case, below 149)

- And if the price continues to climb, just shift the order up accordingly.

- However, always ensure that you have a StopLoss: approximately 45 pips and a TakeProfit: of at least 200 pips which would allow you to have a very good R:R.

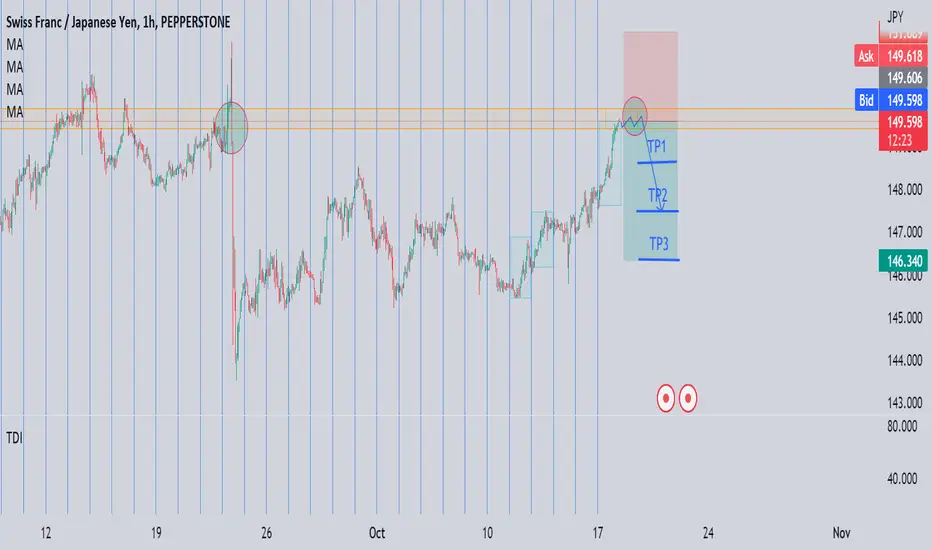

USDJPY SellDear Traders,

Many of us have been stopped by the strong uptrend of UJ.

This is a counter trend idea.

The Red area is Monthly Supply Zone since years ago. The fact that the prace is barely above in the 4H doesn't mean that it is now a demand zone.

It has to be tested multiple times in order to be categorised as support.

The pair needs breath to be corrected and the market cycles indicates overbought conditions with TDI giving us bearish divergence comparing to Price action. Maybe the big players are getting ready to close their profits.

So, I count on a nice pullback with 4 potential profit levels.

Good luck!

USD/JPY breaks above 149USD/JPY has edged higher today and is currently trading at 149.17. The yen has fallen for eight straight sessions, losing 500 points in that time.

The yen continues to set new 24-year-old lows as the dollar/yen has pushed above the 149 line. This is a higher level than when the government intervened last month, which marked the first intervention since 1998. Officials have reacted to the yen's latest slide with familiar verbal rhetoric. Bank of Japan Deputy Governor Masazumi Wakatabe has said that the yen's recent fluctuations were "clearly too rapid and too one-sided". Wakatabe added that there was no contradiction between currency intervention to prop up the yen and the BoJ's ultra-low interest rate policy, which has been the driver of the yen's poor performance this year.

Prime Minister Kishida said on Saturday that the BoJ would have to maintain policy until wages rose, and the BoJ has not shown any signs of rethinking its policy, even with the yen sliding and inflation remaining above the central bank's target of 2%. Japan's core CPI rose 2.8% in August, the fifth straight month that it has exceeded the 2% level.

The key question is whether the government again step in and intervene in the currency markets. The first intervention clearly didn't achieve its desired effect of stabilizing the yen below 145 and Japan's foreign reserves fell by a record amount in September, around 2.8 trillion yen. The game of cat-and-mouse between the government and speculators betting against the yen continues, and another currency intervention could be in the works, but it would likely have to be much larger than the first intervention in order to have a more lasting effect.

USD/JPY faces resistance at 150.04 and 151.32

There is support at 148.85 and 147.58

chfjpy Hi traders.

On Thursday 22 of September, the Price actions violated rapidly the former support.

It has not been checked and my bias has shifted to bearish, 'cause I take into account as a supply area now.

The price action has been performing bullish impulse moves without significant correction.

With positive JPY news, this scenario can be validated even more.

Thank you for your support to the messages! I hope that I help.

Good luck!

USD/JPY creeping higherUSD/JPY continues to move edge higher and is up 1.6% this week. In the European session, USD/JPY is trading at 147.67, up 0.25%.

The Japanese yen is once again on a downswing, after hugging the key 145 line. The dramatic intervention by Japan's Ministry of Finance (MoF) in September stemmed the yen's bleeding, but this move by Tokyo appears to have had a very short shelf-life, as the yen fall to new 24-year lows.

The burning question is with the yen currently lower than when the MOF stepped in, will it again intervene to prop up the Japanese currency? The first intervention clearly didn't achieve its desired effect of stabilizing the yen below 145 and Japan's foreign reserves fell by a record amount in September, around 2.8 trillion yen. The game of cat-and-mouse between the MOF and speculators betting against the yen continues, and another currency intervention could be in the works, but it would likely have to be much larger than the first intervention.

The MOF could try to send a stronger warning to the markets, but it's questionable whether unilateral action by Japan will be enough to change the yen's downtrend. The Bank of Japan has no intention of capping JGB yields and with the Fed likely to deliver another oversize rate hike in November, the US/Japan rate differential will continue to widen and likely weigh on the Japanese yen.

The US posted another hot inflation report for September. Headline inflation ticked lower to 8.2%, down from 8.3% but above the consensus of 8.1%. Core inflation rose to 6.6%, up from 6.3% and higher than the forecast of 6.5%. Inflation clearly is yet to peak despite monetary policy becoming restrictive, and the inflation data cements expectations for a 75 basis point hike at the November meeting.

USD/JPY is testing resistance at 147.50. Above, there is resistance at 148.32

There is support at 147.50 and 146.04

USD/JPY implied volatility rallies ahead of US inflation There are two tell tale signs that an important event is looming; realised volatility has died a quiet death whilst implied volatility has sprung alive. For all FX majors, 1-day implied volatility is currently higher than 1-week implied volatility, which means options traders estimate volatility over the next 24-hours to be greater than the next five days.

Today is clearly all about the US inflation report, where another hot print is expected. Core CPI is expected to rise to 6.5% and match its 40-year high set in June, whilst CPI is expected to soften to 8.1% y/y – thanks to lower energy prices which OPEC are doing their best to support.

With markets fully braced for another hot CPI – which will no doubt prompt a bullish response for the dollar if true, there is little talk of it missing expectations. And that could arguably prompt a more volatile response should it come in slightly softer. And speaking of volatility, implied vols for forex are screaming higher whilst USD/JPY trades within a miniscule range around its 24-year high.

USD/JPY remains within a strong uptrend on the 1-hour chart, and trades within a tight consolidation just off its 24-year high. There’s been little in the way of jawboning from the MOF since prices broke above the previous intervention high, and the BOJ’s Kuroda has once again given a weak yen the thumbs-up – so long as its demise is not too volatile.

A break above 147 confirms a bull-flag breakout and assumes trend continuation toward the 147..65 high – but given the historical significance of this level, it could prompt a shakeout has traders book profits or even fade the move.

Should prices move initially lower then bulls could consider dips, but if CPI is to come in softer than expected then bears would likely drive this pair much lower.

What the Forex now? Finally long yen?Today was just bizarre, to say the least. Dead cat bounce or what? Well, lets see how things pan out but be prepared to get short of the dollar if the set ups turn up on Friday and next week.

USD/JPY traders gobbled up by the BoJ?Well, that was a bummer! USD/JPY has been smashed, probably by Bank of Japan intervention.

USD/JPY closes above 145 - NFP now in focusUSD/JPY finally closed above 145 for the first time in 24 years. Given we saw the MOF (Ministry of Finance) intervene around 145.9 then the potential for the BOJ or MOF to jawbone (if not intervene) may be high. However, traders remain aware that it will take a coordinated intervention to turn this trend around, which is why prices simply drifted back to the highs when the MOF intervened in September. And until we see any sort of intervention, price action remains king. Take note that the MOF last intervened around 145.90, so maret may become twitchy the closer we get to that level.

An inverted head and shoulders pattern has formed on the USD/JPY 1-hour chart, which projects a target around 146.2. With the dollar looking strong ahead of today's NFP report, perhaps we'll see another leg higher ahead of the key Nonfarm report.

The trend remains bullish and we would consider bullish setups above the broken neckline, with the initial target being the highs around 145.35 and the daily R1 pivot.

$JPY: BOJ - Let's challenge you!BOJ - Let's challenge you!

Intervening in there currency was a perfect technical set-up as well but as I started in my previous posts, we are going to re-rest the highs as we are, and we could perhaps go further if we break above that spike high of 146 area. However, we could get a fake break to either direction that's where you should be careful. Technically we have a great technical set-up once again!

Formation: Triangle

Bears: A break below 143 half handle we could head down to 142 half areas.

Bull: A break above 146 areas we could ahead above to 146 three-quarter areas.

Fundamentally: BOJ just like BOE followed and ECB are doing in having to intervene due to higher DXY - print money despite high inflation, in order to support their sovereign bond markets. BOJ intervening is being tested highly!

Key tip: Be careful of fake break outs and follow your own trade plan

Have a great week ahead,

Trade Journal

USDJPY 3rd OCTOBER 2022The yen's recent sharp fall, which has pushed up the cost of living for households as fuel, food and drink prices rise, was partly driven by the widening gap between the US Federal Reserve's aggressive monetary tightening and the BOJ's ultra-loose monetary policy. BOJ Governor Haruhiko Kuroda echoed Suzuki's warning that a rapid yen move was undesirable, but stressed his determination to maintain ultra-low interest rates that analysts blame for accelerating the decline in the Japanese currency.

"If risks to the economy materialize, we will obviously take various monetary easing measures without hesitation as needed," he said at a meeting with business executives in Osaka, western Japan. The remarks came after the government's decision on Thursday (22/9/2022) to intervene in the currency market to stem the yen's weakness by selling the dollar and buying the yen for the first time since 1998. However, analysts doubt whether the move will stop the yen's decline from falling prolonged for a long time.

The Japanese government will allow individual foreign tourists to enter, re-enact visa waivers, and remove daily arrival limits from Tuesday 11 October. "Starting October 11, Japan will relax border requirements to match the United States' while reinstating visa-free travel and individual travel," this step is a testament to Japan's beginning to emerge from its economic downturn by loosening its tourism sector policies. It is projected that there will be an increase in the number of tourists after the policy recently made by the Japanese government.

Can I tell you about: The BoJ InterventionThe USDJPY had been climbing strongly especially as the price broke above the 140.50 resistance level to an overall high of 145.90. However, before the high of 145.90 was reached, the price had been resisted by the 145-round number resistance level.

On the 14th of September , as the USDJPY tested the 145 resistance level again, the Bank of Japan conducted a rate check, in apparent preparation for currency intervention. The signaling of the BoJ's intention to intervene in the Forex market saw the USDJPY trade lower towards the 142.50 support level.

On 22nd September , with the release of the BoJ monetary policy decision maintaining at -0.1% and failing to indicate an intervention from the BoJ, the USDJPY traded with significant volatility but eventually traded higher towards the 145.90 price level.

As the price hit the 145.90 price level, the BoJ announced that it had intervened in the foreign exchange market, to buy the yen for the first time since 1998, in an attempt to shore up the battered currency.

This saw the UDSJPY plunge to around 140.36 yen. However, as Finance Minister Shunichi Suzuki declined to disclose how much authorities had spent buying yen, whether other countries had consented to the move, and with no subsequent signs of further intervention, the Yen has almost completely retraced the reactionary plunge.

Currently trading below the 145 resistance level and the 78.60% fib level, the directional bias of the USDJPY is still heavily dependent on the strength of the USD and the overall volatility of the DXY. But it could be a while more before we see the USDJPY trade higher beyond the 146 resistance level.

Japanese yen dips, retail sales nextThe yen has reversed directions today and is in negative territory. In the North American session, USD/JPY is trading at 144.59, up 0.33%. Japan releases a data dump later today, highlighted by retail sales for August. The headline reading is expected to rise to 2.8%, following a 2.4% gain in July.

It was exactly a week ago that the yen went on a spectacular roller-coaster ride, as USD/JPY traded in a 450-point range. The yen has performed poorly this year, losing about 20% of its value against the dollar. As the yen continued to slide, the Bank of Japan and the Ministry of Finance (MoF) would warn that it was concerned, but the verbal rhetoric was not backed up with action until the MoF's dramatic currency intervention last week. The MoF stepped in after USD/JPY broke 145, and the yen climbed as much as 2.5% after the intervention. Immediately, there were questions as to whether a unilateral action could stem the yen's descent. Is 145 truly a line in the sand, or will Tokyo allow the yen to continue to fall?

The intervention gave the yen a brief shot in the arm, but it has been unable to consolidate these gains, for two reasons. First, the Federal Reserve is expected to remain hawkish at least into 2023, which has pushed US Treasury yields higher and widened the US/Japan rate differential. Second, the yen is caught in a tug-of-war between the MoF, which wants to see a stronger yen, and the BoJ, which is focused on maintaining an ultra-accommodative policy, which has kept JGB yields at low levels, even though this has hurt the yen. Governor Kuroda has said more than once that a weak yen is not necessarily bad, and has made clear that he will not change policy until it is clear that inflation is not transient (taking a page out of Jerome Powell's playbook).

These conflicting signals have invited speculation in short positions in the yen and I would not be surprised to see dollar/yen make another attempt at breaking the 145 line shortly.

144.81 is under pressure in resistance. 146.06 is next

There is support at 143.21 and 141.88

Look on USDJPY!For almost three decades now, investors have looked at the economic headwinds faced by the Bank of Japan, at its QE and QQE policies, and at the country’s awful demographics and realised that the obvious outcome is a massive sell-off in Japanese government bonds (JGBs) and a dramatically weaker yen. So ‘obvious’ has this trade been that, at some point, just about everybody in the financial market has been short either JGBs or the yen — or both.

Of course, the main reason for the failure of the Widowmaker trade has been the staunch refusal of the Bank of Japan to ‘allow’ price discovery in JGBs. Over time, its efforts have become increasingly desperate and the distortion of the country’s sovereign bond market more pronounced.

NIkkei 225 10 year ProfileBOJ intervened for the first time since 1998, to prop up it's the YEN, with some speculation they likely sold a lot of their massive reserves of long end (10-30 year) US T Bills to buy back the Yen. This hypothesis appears supported by the lack of short end yield movement at 4-5a, EST at time of BOJ intervention announcement late last week. Of note in this chart are:

- Almost a decade long volume profile aligned with vPOC at 382 retrace.

- Structure of current price action seemingly mirroring the covid structure as represented by the fractal in light blue above.

How can we profit after BoJ's intervention?Yesterday, after more than 10 years, the Bank of Japan intervened in the market.

UsdJpy pair was very volatile and has a 550 pips daily range from top to bottom. However, thinking of previous interventions, yesterday's volatility represented around 2.5% if we take into consideration the daily close when in the past we had 5% moves...

But, what do we know from previous interventions?

First of all, they never worked, in fact from the past 11 interventions, BoJ was able to maintain "the move" in only one case, and that time wasn't a BoJ intervention, but a joint intervention in the markets alongside other central banks.

Second, and most importantly, we can profit from this.

So, how can we do this:

1. As I said, we know that BoJ intervention doesn't work and the pair resumes its previous trend. In UsdJpy we have a clear up trend and in such a case we should look for buying opportunities.

Using only support and resistance we can see that under 140 we have a very good level of support. So under 140, we should look for buying opportunities. Considering the resistance provided by the intervention, we can set a take profit in that zone.

Considering a hypothetical trade, if we buy at 139.50 with a take profit at 145.50, we have a potential 500 pips profit. As a stop loss, we can use a large and comfortable stop loss of 250 pips, which still gives us a 1:2 risk to rewards ratio, or, be more aggressive and use 138 as a stop loss and, in this case, we have more than 1:3 R: R.

2. Using the ceiling given by BoJ yesterday, which is 146. So, also a hypothetical trade: sell around that zone, set a stop loss of 150-200 pips and as for target, we choose the 140 support. In this case, we count on 2 things: first, we are backed by BoJ which "said" very clearly yesterday that is not comfortable with UsdJpy above 145, second, a lot of people will sell or close their buy positions there, using the same reasoning, putting pressure on the pair.

P.S: Keep in mind that levels provided in this article are for the sake of example, not specific points where to buy or sell.

Regards and best of luck!

Mihai Iacob

USD/JPY -22/9/2022-• Japan government finally intervenes in the FX market to try and support the Yen

• Major currencies lost almost 300 pips against the Yen following the news

• On the chart above, illustrated an ascending channel the Dollar Yen is trading in, a bullish pattern indicating further gains on the cards

• Also illustrated are the major support/resistance levels in red thick line

• Current trading range is 139.300-144.730

Japanese yen steady ahead of Fed, BoJUSD/JPY continues to show limited movement this week. In the North American session, USD/JPY is trading at 144.10, up 0.27%.

The Japanese yen has depreciated by over 20% this year, and the yen's slide will be high on the agenda at the Bank of Japan's meeting on Thursday. We could see some strong rhetoric expressing deep concern about the yen, but the central bank has stayed on the sidelines during the yen's long slide and I don't expect that to change. The BoJ is committed to its ultra-accommodative policy, in order to boost Japan's weak economy. Inflation has been rising, but Governor Kuroda has said he won't tighten policy until it's clear that inflation is sustainable, which would mean solid wage growth.

There have been some rumblings about currency intervention by Tokyo, and the yen received a short boost in the arm earlier in September, after a report that the BoJ had conducted a rate check, which could have been a prelude to intervention. Japan hasn't taken such a drastic move since 2011 and would require the consent of the G-20 to do so. As part of its loose policy, the BOJ has been very firm with its yield curve control, and the yen has borne the brunt of this policy, as the US/Japan rate differential continues to widen. With the Federal Reserve poised to raise rates by 75 or even 100 basis points later today, the outlook for the yen appears grim.

The markets are anxiously awaiting the Fed's rate announcement, as well as the Fed's quarterly economic forecast. This will include projections for unemployment, inflation and interest rate levels. If Fed Chair Powell's message is 'higher for longer' with regard to rate levels, investors could respond by sending the US dollar higher.

There is resistance at 144.71 and 146.49

USD/JPY has support at 143.19, followed by 141.88

USDJPY and BOJIf the monetary expansion of the Bank of Japan continues, which will be determined in the next meeting of the central bank, on Thursday this week, there is a possibility of a rapid rise for the USDJPY currency pair more than now.

The Treasury's resolve may be tested, and if the Treasury fails to do so, USDJPY could quickly reach the 150 area.

#USDJPY | Macroanalys:Japanese yen: important weeks ahead.

In the last week, rumors about interventions by the Bank of Japan have intensified. The government also called on the financial authorities to intervene in the situation on the foreign exchange market.

We consider 3 scenarios most likely:

№ 1. Selling dollars from reserves, through RRP reduction, or selling short-term US bonds.

№ 2. Through an increase in interest rates and avoidance of negative rates while maintaining quantitative easing.

№ 3. Removing the cap on the maximum yield limit on 10-year Japanese bonds.

We consider the first option the most probable.

This point in time was chosen in a timely manner. The Fed is close to the neutral rate, tightening the monetary policy has a negative impact on the global economy and reduces consumption. All this lowers oil prices.

Thus, we believe that in the absence of risk factors*, we are close to opening long positions on the Japanese currency.

Deal of the year 2023 begins.

Risk factors:

No. 1. US rates will go above 4%.

No. 2. Oil or gas prices will continue to rise (geopolitical risk in the Middle East, possibly Iran).

Number 3. The Bank of Japan will ease the monetary policy.

USD/JPY slides after BoJ rate checkThe Japanese yen has posted sharp gains today. USD/JPY is trading at 143.09, down 1.00% on the day.

The yen has taken investors on a roller-coaster ride this week. On Tuesday, the dollar shined, posting broad gains against the majors and climbing 1.19% against the yen. The catalyst for the upswing was the US inflation report, which was higher than expected. The yen has recovered most of these losses today, after reports that the Bank of Japan had conducted a rate check, which could signal currency intervention in order to prop up the ailing yen.

The BoJ has rigidly maintained its ultra-loose monetary policy in order to stimulate Japan's fragile economy. As part of this policy, the BoJ has kept a firm hand on its yield curve control, and the price for this stance has been a freefall in the yen, which is done an astounding 30% against the dollar this year. Japanese policy makers have fired verbal warnings about the yen's depreciation causing deep concern, but the markets have learned to ignore the rhetoric, which hasn't been backed up by any action.

The yen hit 144.99 last week, a new 24-year low, and there has been speculation that 145 is a line in the sand for Japan's Ministry of Finance, which would be responsible for a currency intervention by purchasing a massive amount of yen with US dollars on the currency markets. Japanese officials haven't ruled out intervention, but there is a legal hurdle as Japan cannot intervene in the currency markets without permission from the G-20. The last time Japan intervened to prop up the yen was in 2011, in the middle of a financial crisis in Asia. Still, investors will be paying close attention to the BOJ's meeting on September 22, which comes just one day after the Fed's next meeting. Any hints of intervention could send the yen sharply higher.

If, however, Japan decides once again to stay on the sidelines, the yen has more room to fall. The Fed is likely to raise rates by 75bp at the upcoming meeting, but there is a reasonable possibility of a massive 100bp hike as well. With the yen at the mercy of the US/Japan rate differential, I expect the yen to continue to lose ground, barring some dramatic action from Tokyo.

1.4363 is the next line of resistance, followed by 144.81

USD/JPY has support at 142.56, followed by 141.88