We will wait before taking action on Chinese Stocks. Today we will take a look at BABA. When do we think maybe a good moment to start adding Chinese stocks into our portfolio?

Of course, we will look at the answer from a technical perspective, and this is the conclusion we make:

a) We must see contact with the support level first (Is there buying pressure?)

b) If we see bullish pressure, that is the first sign those big investors may be adding again.

c) Ok, that's the first filter; the second filter is the breakout of the descending trendline. That would mean a change in behavior or sentiment. Now the price can stabilize and avoid the previous decreasing angle in price.

d) Cool, can I buy it now? You can buy whenever you want; however, we will not do that; we want to see our 3rd filter. Corrective Pattern after the contact on the support level + breakout of the descending trendline. It's pretty standard after we observer a breakout of a key level (in this case, the descending trendline), a lot of FOMO comes to the market. "Chinese Stocks are booming! I will not miss this..." And most of the time, those traders or investors get trapped on a correction.

e) So if all the previous filters happen, we will develop long setups on BABA.

f) Patience is key when looking for quality setups; you can't ask the market for opportunities; you need to wait until the market provides one.

Thanks for reading!

China

OMX 4% downsideShort term trend for OMX looking bearish. Looking to alter some cash and pick up HSTECH.

Pairs trade with FXI and EEM**Spread Trade***

An opportunity to initiate a pairs trade by buying FXI and selling EEM. Spread between both etfs grew substantially (over two sigma), spread should start narrowing make sure you execute trade using ratio of both prices.

For instance, you could go long fxi 26 units and short EEM 20 units (capital 2000usd)

Chart symbol of spread —> input the following in the symbol box: FXI - EEM

COIN- BUY THE DIP AND FORGET THE CHINA FUDCoin is very undervalued here at these prices, and is setting up for a amazing risk to reward ratio to open a position.

If i was just trading this, i would set a stop loss for somewhere below $215 and Set Profit targets at: $250/$290 & $330.

I wouldnt be surpised at all if this ran similar to APPS the past month where the stock price has surged from below 450 a share to pushing $75 a share recently.

This for me is starting a long-term position, but i may add extra capital and play some shares as a shorter swing trade.

Goodluck Traders!

AUDUSD ShortA Series of Valuation Signals produced by our models on a range of AUD pairs show a potential downside move about to hit AUD/USD.

Our analysis shows Chinese Credit Default Swaps are the top driver negatively impacting AUDUSD, which have been uplifted by the recent Evergrande Crisis.

Since this macro driven signal emerged on October 2nd, 2x Hidden RSI Divergence Signals have appeared, with the spot value making lower highs while becoming further overbought.

Should there be further downside from China, AUDUSD looks to be the way to express it...

LOOK UP™

@hsi long there is an HSI idea with going long a few weeks ago.. I was wrong :)

now it is a better chance to accumulate some long positions; as I marked on the chart, there are 3 ways to go; as you know, the lines/channels are there just for guidance

Sunac 1198.HK Bounce of extension target ending?Sunac bounced off the extension target after announcing securing funds from a major shareholder.

Down 11.5% today

a test of 12.90 again on the cards as the move is impulse. A failure puts the stock for an accelerated move down.

Bitcoin Will Drop... Alot. But it Will Rise Above the Ashes.Markets are going to keep going down in fear of Chinese real estate powerhouse Evergrande defaulting; Bitcoin will drop alongside it in the short term. My chart shows we may still rebound after we hit the 38k area.

With that being said, if the Chinese housing bubble crashes, which represents 28% of China's entire economy, we will enter a global correction. Combine that with current inflation rates (6% on the year), and if this spending bill passes congress, we will enter a long term bearish outlook; which will shred BTC down to the 20K's in the short term as people liquidate assets in fear of them dropping further. That will be the ultimate buy opportunity, as BTC will serve as an inflation hedge long term, and only augments Bitcoin's use case - despite China working overtime to thwart the coin at every new opportunity it seems.

The only chance Evergrande has, is if the Chinese government bails it out. But that will only alleviate things for a short time, a band aid. If that happens, and the markets rebound, im looking to liquidate my stock portfolio and hold cash.

The whole world is looking at China right now...

dunno but this shit looks like going deeperchina 50 doesn t look good, head and shoulder looks like forming...tonight will look if i enter the trade, by now i got stopped out because my broker ended contract

HUYA (1W) - Midterm Plan Hi Traders,

Below is my Idea about this very good loking company .... from CHINA !!

Compared to competitors (like Twitch) is discountedm same like DOYU. WHich are both owned by TENCENT as one of biggest investors.

After some FUD price from chinese government the price is Dummping.

In my Opinion, we are approaching end of impulsive wave DWON. you can also see touch with downtrend line + RSI COnvergence + MACD Convergence. Which are very bullish signs for me.

ALso fundamentally, this could be very good investment. But lets see. My plan is to take around 75-100% and sell everythin from actual price around 8.40 USD.

Trade safe. Enjoy the ride.

Tesla, shortIncreased my short in tesla, good luck all stupid buyers at these resistance levels! U gonna need it, se you at 700.

ETHUSD ❗Local counter-trend📉The price is currently below the local resistance level, on the watch you can see a clear local counter-trend line. Be very careful, there will likely still be drawdowns. TC the market has not yet recovered after last week.

Do you agree?)

Your Solldy.

Gaotu Hints at Vocational Education Shift Due to the recent introduction of the 'double reduction' policy by the state to regulate the country's expensive private education industry, Gaotu is looking to adjust its focus.

The Chinese edtech firm Gaotu released its Q2 earnings report for the period ended June 30, 2021, on September 23 2021.

- Net revenue was CNY 2.23 billion, a 35.3% year-over-year increase.

- Net revenues of online K-12 courses increased 51.0% year-over-year to CNY 2.09 billion.

- Gross billings were CNY 2.69 billion, a 12.2% year-over-year increase.

- Gross billings of online K-12 courses increased 17.2% year-over-year to CNY 2.57 billion.

- Paid course enrollments increased 4.1% year-over-year to 1,631 thousand.

- Paid course enrollments of online K-12 increased 4.5% year-over-year to 1,563 thousand.

- Net loss was CNY 918.8 million, compared with a net income of CNY 18.6 million in the same period of 2020.

- Non-GAAP net loss was CNY 763.9 million, compared with non-GAAP net income of CNY 72.7 million in the same period of 2020.

- Deferred revenue was CNY 1.97 billion, compared with CNY 2.73 million as of December 31, 2020.

Larry Chen Xiangdong, Founder and CEO of Gaotu, said in the financial report that Gaotu has adjusted its organizational structure, transformed its focus to vocational and STEAM education instead and would further work on digital products and vocational education.

Shen Nan, CFO of Gaotu, further expressed that in exploring vocational education, the public service examination has maintained a high level. The number of paying users of financial certificates has increased fourfold year-on-year, Shen said, "In the future, we will focus on areas strongly supported by the government and create a multi-faceted interactive platform covering all education categories to achieve lifelong learning."

17EdTech Hits USD 104 Million in Revenue for Q2 2020The Chinese edtech firm’s K-12 tutoring service contributes 98.7% of its revenue

17EdTech released its Q2 earnings report for the period ended June 30, 2021, on September 23.

- Net revenue was CNY 671 million, a 147.2% year-over-year increase.

- Net revenues of K-12 tutoring service increased 163.9% year-over-year to CNY 662 million.

- Paid courses enrollment reached 1.18 million, a 131.1% year-over-year increase.

- A 68.3% increase in operating expense year-over-year consists of CNY 307 million in S&D and CNY 230 million in R&D.

- Net loss was CNY 218 million, narrowing down by 73% compared to Q1 2021.

- Cash and cash equivalent CNY 2.16 billion, an 23% decrease from last fiscal year.

- Monthly average users reached 1.65 million, a 24% decrease year-over-year

17EdTech also announced that Co-founder Mr. Xiao Tong resigned from the board of directors due to personal reasons effective from September 23, 2021. Since the uncertainty in the supervision of the firm and the operation circumstances 17EdTech did not release the performance guideline for the next quarter.

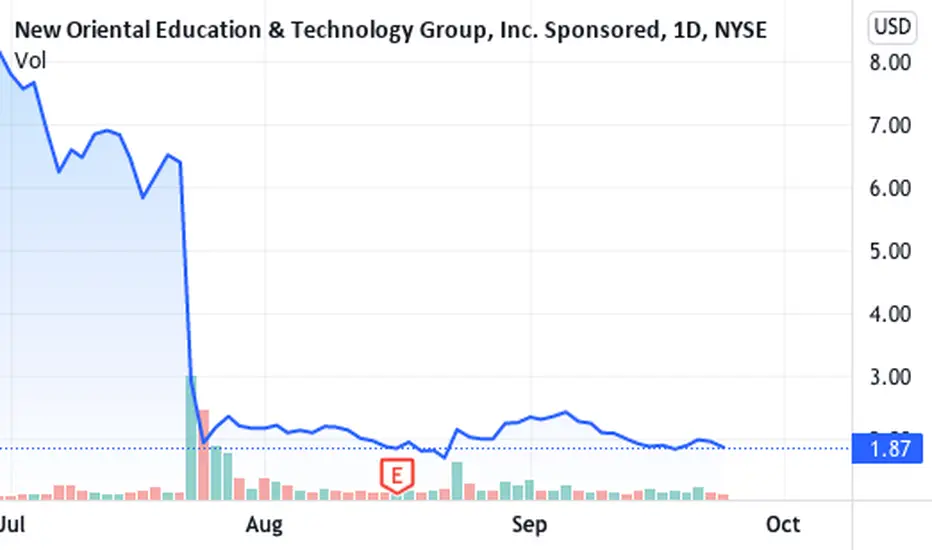

New Oriental Records USD 4.27 billion Revenue in FY 2021AccordinAccording to the latest regulatory developments, it plans to shut down a certain number of learning centers in the fiscal year 2022.

The Chinese edtech giant released the audited performance report for the fiscal year 2021 on September 24

Revenue was USD 4.27 billion, a year-on-year increase of 19.5%.

The net profit was USD 230 million, a year-on-year decrease of 35.03%.

The net profit attributable to shareholders was USD 334 million.

The revenue of New Orientals plans and services in the fiscal year 2021 was USD 3.93 billion, accounting for 92.1% of the total revenue while the revenue of books and other services was recorded as USD 340 million, accounting for 7.9% of the total revenue.

The firm's business is mainly divided into seven categories, including K12 after-school counseling, examination preparation courses, adult language training, kindergartens, primary and secondary schools, textbook development and distribution, online education, overseas study consultation, overseas study tour and other services.

- New Oriental's revenue from K12 after-school counseling, test preparation and other courses was USD 3.66 billion, accounting for 85.8% of the total revenue, an increase for three consecutive years.

Online education revenue was USD 211 million, accounting for 4.92% of the total revenue, with a year-on-year increase of 37.91%.

- The revenue of kindergartens, primary and secondary schools, textbook development and distribution, study abroad consultation, overseas study tour and other services was USD 399 million, accounting for 9.33% of the total revenue.

- In terms of the number of students, as of the reported period New Oriental has 6.723 million students participating in extracurricular counseling courses for middle school and high school students, and 5.348 million students participating in extracurricular counseling courses for kindergarten and primary school students. There are about 390000 students enrolled in the preparatory courses, including 198000 overseas preparatory courses and 193000 Chinese preparatory courses. About 5000 students enrolled in the adult English course.

- In terms of the number of teachers, the financial report shows that as of May 31, 2021, New Oriental has employed 54200 teachers, mainly full-time teachers, followed by contract teachers.

In terms of expenses, the total operating costs and expenses of New Oriental during the reporting period were USD 4.159 billion. Among them, the revenue cost was USD 2.037 billion, the sales and marketing expenses were USD 600 million, the general and administrative expenses were USD 1.49 billion, and the impairment loss of intangible assets and goodwill is USD 31.79 million.

- In this report, New Oriental believes that the measures taken to comply with the 'double reduction' policy will have a significant adverse impact on the firms' business, financial condition, operating performance and prospects.

New Oriental said that it may take further actions on discipline counseling services in the stage of compulsory education in the near future to ensure its legal compliance, including closing some learning centers and layoffs when necessary, so as to maintain continuous operation.

Bitcoin closer to $65,000 than $0RSI on the daily went down close to 30RSI. 4hr chart is already heading up and the hourly is set to make a decision sometime tonight or by tomorrow. I am bullish so I see us heading back up to $50,000 which has been resistance. Once we break this resistance, $65,000 and above will be exponential. Regulations and bans on Bitcoin up to this point seem weak for the long term Hodler.

MADE IN CHINAMADE IN CHINA

-

-

-

-

-

-

-

-

-

LOL China doing Many FUD to bitcoin, but Evergrande Dump verry hard

Evergrande: A DiscussionConcerns Investors May Have:

China is said to contain more of the world's real estate assets than any other country.

Therefore one concern is the potential impact a possible default may cause to international property markets.

Consumer confidence in real estate investments could reduce and perhaps lower property demand, potentially reducing real estate prices.

Should this occur to a great extent, pre-existing property loans could outvalue the revaluation of the real estate asset.

This potential major contrast between loans outvaluing the associated properties could collapse some banks internationally.

A possible mass sell-off of property globally by investors and banks could burst the property bubble.

Another concern is investors could forfeit involvement in companies offering similar services.

There ore other confounding factors involving the current pandemic, employment, inflation and among others.

Thank you for reading.

Please share your thoughts.

Do you believe this company could be bailed-out or would other companies in a similar position expect similar treatment?

----

Disclaimer:

This does not constitute any form of advice including legal, financial or investment advice and should not be construed or relied on as such. Always seek advice from a qualified and registered legal practitioner or financial or investment adviser. Information presented is for entertainment purposes only.

Bitcoin: Two Main Scenarios here for the next couple of weeks.Scenario A:

Considering BTC is failing to get above the 0.618 fibonacci level located around 43700-43900 this may be a early warning sign that cheaper prices are coming, but there is still hope:

In the top image the 0.618 is claimed as support quickly taking us to the next resistance area above, if further resistances were claimed this bearish idea would obviously be invalidated.

-------------------------------------------------------------------------------------------------------

Scenario B:

In the below image (Scenario B) the 0.618 we fail to claim as support and this adds further panic into the market with the China Banning Bitcoin Transaction news, and Evergrande Debt Crisis leading to a deep market sell off, the most logical area being the 0.382 fibonacci at 38300 or the Previous Strong Support Area at 29200 for Bitcoins next key area of reversal.

-------------------------------------------------------------------------------------------------------

Evergrande Debt Crisis:

edition.cnn.com

China Widens Ban on Crypto Transactions:

www.bloomberg.com

$VET at resistance#VeChain is facing heavy R after the latest bounce.

As you can see in the chart, the 200D EMA and year long trendline resistance is holding it down here.

Caution is needed here too.

China Bans Crypto - Fact or FUDHello Traders! We got something interesting for you!

Chinese authorities ordered a fresh crackdown on crypto mining and trading Friday, according to a statement posted on the People’s Bank of China site.The statement, signed by China’s top financial and cyberspace regulators, gives a comprehensive list of crypto activities that are forbidden, and orders local governments to crack down on them.

China’s State Council issued a statement in May ordering a crackdown on crypto mining and trading. The statement sent dozens of crypto companies abroad.The regulators banned banks and other financial institutions from offering services related to crypto and called for increased censorship of information related to crypto.The regulators also want to establish a mechanism for early warning and stopping “hype” in crypto trading and mining activities.

Honestly speaking, the intentions of the Chinese government are not clear to me. However, one thing is for sure - this situation will have an extremely negative impact on the cryptocurrency market and may lead to the start of a bear run. We will keep our finger on the pulse and keep you updated on all the latest news from the world of cryptocurrency.

Honestly speaking, the intentions of the Chinese government are not clear to me. However, one thing is for sure - this situation will have an extremely negative impact on the cryptocurrency market and may lead to the start of a bear run. We will keep our finger on the pulse and keep you updated on all the latest news from the world of cryptocurrency.

Nevertheless, let’s have a look at the chart. As you can see the price I lying on the Support 1. If it’ll close bellow it, the continuation of fell if very probable. The next level is Support 2. It’s kinda difficult look in future deeper:). If the scenario works, we will update out analysis. But, it seems to me that today’s candle is able to close above the support 1. In this case, it may retrace rapidly.

Well guys, I don’t want such news get you into trouble, it’s the big game that’s named «Market». The rules are trivial - there are no rules or the are always be rewritten. Try to make deal even in such tough periods and we’ll help you with it.

🔥 China Banning Crypto FUD: Why You Shouldn't WorryAs of today, the Chinese central bank has announced that all crypto transactions are deemed illegal.

Investors who have been in the crypto space for a while know that once in a while China announces that they are banning crypto (again). This FUD comes in once in a while and often sends the market down, but fails to make a lasting impact on the market.

A quick google search has netted me a decent amount of times that China has banned crypto, see the chart. I'm sure that if you dig deeper you'll find many more occasions of China "banning" crypto. Feel free to share them below.

What you can deduce from this graph and the corresponding news is that, in the long-term, China banning crypto has had no significant impact on the markets. As for today, it seems that the market is already rallying higher with many coins close to their opening prices of today.

Happy trading!

Bitcoin in Freefall Towards the Closest Psychological SupportBitcoin's tumble was bolstered today following the decision of China's central bank to declare all cryptocurrency activities illegal. The price action is currently testing the 23.6 per cent Fibonacci retracement level at 41764.04. A potential pullback could ensue to the 38.2 per cent Fibonacci, which is about to be crossed by the 50-day MA (in green) and the 100-day MA (in blue).

Conversely, a decisive breakdown below the 23.6 per cent Fibonacci would likely be followed by a dropdown to the psychologically significant support level at 40000.00.