BIMI time for a big breakoutBIMI had a run and left many gaps opened , now its time to fill out those gaps and fly in the sky .

This is a very risky trade

High risk / high reward.

Don’t enter if you can’t manage your trade

Trade Safe

Chinastocks

The inflation is taking TBLT to the moonKeep it easy simple and safe

Enter at current price

TP1 0.72 (42% gain)

TP2 0.89 (74% gain)

TP3 1$+

SL 0.49 (4% loss )

Safe trade , trade safe ><><

NIO Setting Up + Upcoming Catalyst NIO DAYNIO, the electric vehicle company is setting up again after being on a serious downtrend since its surge in January. This surge was the result of lots of "hype" around the name, the rise of Tesla, and its upcoming NIO day which happened on January 9th, 2021. We saw a massive run up the month before, around 60%.

This year, NIO day is happening on Dec 18th, 2021. This should cause an influx of volume and talk about the name. Keep an eye on this one.

In order to confirm the Elliot waves, we still need to create the (E) section of the triangle. Once this is confirmed, I believe we can start rising. However, with NIO day approaching soon, there is the possibility of NIO ripping before the set up completes. I will be watching for any signs of a pullback and be entering calls and shares around the 38-40$ mark.

Definitely keep this one on watch because we know from previous bullish runs, that this thing can RUN. The upside potential is very high here.

Weibo Announces Q3 2021 Financial ReportThe leading social media in China, Weibo (NASDAQ: WB), released its unaudited financial results for the third quarter of 2021.

According to the Q3 performance report for 2021:

- The revenue totaled USD 607 million (CNY 3,882 million), increasing 30% year-on-year. As of September 30, 2021, the total cash, cash equivalents and short-term investments amounted to USD 2.71 billion (CNY 17.333 billion).

- The operating profit was USD 213 million (CNY 1,477 million), showing an upward trend of 32%, while the net profit was USD 182 million (CNY 1,164 million), growing 438% from the same period last year.

- The advertising and marketing revenue increased by 29% to USD 538 million (CNY 3,441 million), which was mainly due to stronger demand for advertising from key industries.

- Revenue from value-added services was USD 69.8 million (CNY 446 million yuan), up 42% year-on-year.

- The revenue cost was USD 394 million (CNY 2.520 billion), which was mainly related to increased staff-related costs and marketing expenses. Specifically, revenue costs, marketing costs, product development and administrative expenses were USD 103 million (CNY 659 million), USD 141 million (CNY 902 million), USD 119 million (CNY 761 million) and USD 31.75 million (CNY 238 million), respectively.

- As of September 2021, Weibo has 573 million monthly active users, and 94% of them are mobile users. In September 2021, the average daily active number of Weibo users reached 248 million. Affected by events such as the Olympics, its user base and traffic re-peaked in July and August after the outbreak since March 2020, reaching 302 million once.

Tencent's Profit Down 2% YoY for the First Time in 10 YearsThe drop was a result of regulatory crackdowns on media and restrictions on teenagers' gaming time.

Despite enhancing its parental control policy and constrained gaming time for teenagers (from 6.4% in Q3 2020 to 0.7% in Q3 2021), Tencent saw its domestic gaming service revenue increase by 5% and 20% for the overseas markets. However, Tencent's top moneymaker – mobile gaming – has seen its growth slow down for three consecutive quarters.

A series of media crackdowns in China has been influential on Tencent's advertising income. The YoY revenue grew only 5% due to the political impact on industries, such as education and insurance. In addition to the latest regulatory change, media advertising revenue primarily from the Tencent news app has dropped 4%.

Meanwhile, Tencent's free cash flow decreased by 14%.

TSMC To Produce Chips In Japan By 2024 In Deal With SonyThe deal worth USD 7 bn establishes joint venture company Japan Advanced Semiconductor Manufacturing.

TSMC's board of directors officially approved plans to build a chip factory in Kumamoto Prefecture, its first-ever Japanese plant. Sony is set to invest USD 500 million and will hold no more than a 20% stake in the joint company, according to a statement released on Tuesday. The project will be Japan’s largest financially supported endeavor for a foreign-controlled company with billions of Japanese Yen in subsidies. It will create 1,500 high-tech professional jobs in Japan with the construction of the chip plant scheduled to begin in 2022 and production slated to begin in 2024. TSMC already has a plant in Nanjing and is currently constructing a plant in Arizona in the U.S. with considerations to build a new chip facility in Germany.

The semiconductor industry has been a top priority for many nations grappling with recent supply chain shortages. Japan’s response to the crunch is a framework for subsidies that allows companies to build chip factories in the nation. The conditionality is that firms must respond to requests for increased production and prioritize supply to domestic companies should supplies of semiconductors become tight. Sony specifically is TSMC’s biggest client in Japan making the deal quite worthwhile for both ends. The plant will produce state-of-the-art 7-nanometer chips as well as less advanced but versatile 22- to 28-nanometer chips.

TSMC was founded in February 1987 by Zhang Zhongmou and is headquartered in Taiwan. It is a professional integrated circuit manufacturing server with the world's most advanced semiconductor technology.

NIO Q3 Earnings: What to ExpectWill the chip shortage affect Nio's Q3 results?

NIO will report unaudited third-quarter earnings on November 9 after the US market closes. So what can investors expect?

NIO has already released data showing that it delivered 24,439 vehicles in the third quarter, up 100 percent year-on-year and 11.6 percent from the second quarter. Of those, 5,418 ES8s, 11,271 ES6s, and 7,750 EC6s were delivered.

In a research note sent to investors on November 3, Deutsche Bank analyst Edison Yu's team said the delivery figures were largely in line with their latest forecast.

The team expects NIO's revenue to be CNY 9.33 billion in the third quarter, representing a 106.1 percent year-on-year increase and a 10.4 percent increase from the second quarter.

Yu's team expects NIO to report a gross margin of 17.0 percent in the third quarter and a vehicle margin of 18.6 percent. As a comparison, the company had a gross margin of 18.6 percent and a vehicle margin of 20.3 percent in the second quarter.

The team attributed their lower gross margin forecast to higher depreciation amortization.

Based on these figures, the team expects NIO to report a loss of CNY 0.82 per ADS in the third quarter. This compares with a figure of CNY 0.21 in the second quarter.

For the fourth-quarter outlook, Yu's team expects NIO's management to likely give guidance of 24,000-25,000 deliveries, considering that October's downtime resulted in only 3,667 deliveries for the month.

NIO's management has hinted that their order book has exceeded 10,000 units for several months in a row, so Yu's team expects NIO's deliveries in November and December to improve back to more than 10,000 units, and expects the company's guidance for fourth-quarter revenue may be in the CNY 9.5 billion-10 billion range.

NIO has previously said it aims to deliver three models next year, including its flagship sedan ET7, Yu's team noted, adding that they don't think NIO's management will do a complete refresh of its current models next year, as it believes they can remain competitive with the most competing German luxury models with minor updates.

Yu's team raised NIO's delivery forecast for next year from 150k to 160k and for 2023 from 245k to 285k.

Based on the latest delivery forecast, the team raised its price target on NIO by USD10 to USD70, still based on 8x 2023E EV/sales.

In a separate report sent to investors on November 4, Yu's team noted that NIO's stock has significantly underperformed its local peers over the past three months, but that could change soon.

The team believes that there are 2-3 potential catalysts that could help change the narrative on the stock next. Here's what they say:

1) 3Q21 earnings on 11/9: management will provide 4Q guidance that shows large step-up in volume recovery for Nov/Dec and while official consensus is likely too high, we believe buy-side expectations have already been reset.

2) November monthly deliveries: likely reported on 12/1 and should confirm robust demand for existing models despite greater competition.

3) NIO Day: will be held on 12/18 and we expect new models/technology to be unveiled that should boost both investor and consumer sentiment.

Notably, the team also cautioned that risks including further constraints from the supply chain, a sudden shift in EV investor sentiment and poor initial acceptance of new products could also invalidate these judgments.

NIO shares are up about 10 percent so far this month and up about 20 percent in the past month.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

Haier Founder Zhang Ruimin Steps Down as ChairmanZhang volunteered not to participate in the nomination of new directors. Zhou Yunjie was elected as the new chairman of the board and appointed as CEO. Liang Haishan was appointed as president.

During Zhang’s 37-year stint at Haier, the firm has grown from a Qingdao refrigerator factory with a sale revenue of only CNY 3.48 million but a deficit of CNY 1.47 million in 1984 to a global enterprise with a worldwide sale of more than CNY 300 billion and a pre-tax profit of more than CNY 40 billion in 2020.

According to the Qingdao-based firm, Zhang proposed a management model called Rendanheyi in 2005, which has 'become a trend during the era of Internet of things.'

As a legend in China's household appliance industry, Zhang, known as the 'godfather of Chinese management,' has been selected as one of the 50 most influential global management philosophers. In September 2021, Zhang and Eric Cornell, president of the European management development foundation, jointly signed the first international certification of innovative management, signifying that the Chinese enterprises have created the first international standard of management mode.

Consequently, Haier pioneered a new inheritance mechanism, enabling the company to keep evolving after transforming from its bureaucratic model into a self-driven enterprise.

Zhang was also among the 100 Chinese who were awarded the medals of reform pioneers during a grand gathering in December 2018 to mark the 40th anniversary of the country's reform and opening-up.

Lenovo Group's Net Profit Reached CNY 222.5 Bn in 2021 H1Hong Kong stocks of Lenovo Group fell by 0.35% to HKD 8.47/share, with a total market value of HKD 102 billion.

Lenovo Group has three major business groups, namely the intelligent equipment business group (IDG), the infrastructure solution business group (ISG), and the solution service business group (SSG).

The 2021 H1 financial reports for the Lenovo group are as follows:

- Revenue was USD 34.8 billion, a 24.87% year-on-year increase.

- Net income was USD 978 million, an 87% year-on-year increase.

- IDG's revenue reached USD 30 billion, an increase of 24.14% year-on-year, with USD 2.3 billion in net profit.

- ISG's revenue was USD 3.8 billion, an increase of 23.57% year-on-year, with USD 16.9 billion in net loss.

- SSG's revenue recorded USD 2.5 billion, an increase of 33.39% year-on-year, with USD 548 million in net profit.

The six months performance period ended September 20, 2021, are as follows:

- R&D expense was USD 948 million, accounting for 2.72% of revenue.

- SG&A expense was USD 3.3 billion, accounting for 9.44% of revenue.

The 2021 Q2 performance are as below:

- Revenue was USD 17.9 billion, a 23.07% year-on-year increase.

- Net income was USD 512 million, a 65.16% year-on-year increase.

TuSimple Releases 2021 Q3 Finanical ReportBank of America reiterated TuSimple at a 'buy' rating, with a target price of USD 60. The bank said TuSimple had plenty of liquidity despite still losing money in the third quarter.

According to TuSimple's financial announcement for the third quarter of 2021:

- The revenue was USD 1.80 million, increasing by 205.65% compared with the same period last year.

- The net loss was USD 115 million, increasing by 28.56% compared with the same period last year.

- The research and development expenditure increased by 40.75% to USD 84.51 million.

- The revenue cost was USD 3.49 million.

- The sales and marketing expenses were USD 910,000.

- The general and administrative expenses were USD 28.83 million.

- TuSimple holds USD 1,41 million in cash and cash equivalents as of September, 30.

- At the end of the reporting period, TuSimple's road mileage was 5.4 million miles (about 8.69 million kilometers), showing an upward trend of 17% compared with last month. Among them, the fully automated truck bookings totaled 6,875, 100 more than that in the second quarter; and map mapping miles totaled 9,900 miles, growing 16% from last quarter.

- TuSimple expects the full-year revenue would be USD 5 million to USD 7 million, with USD 200 million to USD 220 million investments in research and development.

NIO: Added Over 10k Orders in Oct, No Chip Shortage for OctNIO said in an announcement on its website yesterday that it delivered 3,667 vehicles in October, including 218 ES8s, 2,528 ES6s and 921 EC6s. That delivery volume fell 27 percent year-on-year and was 65.5 percent lower than in September.

After a short explanation of the dip in October deliveries on the NIO App yesterday, NIO co-founder and president Qin Lihong gave more details in an interview.

NIO's factory in Hefei ran at full capacity for only 10 days in October, so deliveries were low, but sales in October were excellent and reached a record high, local auto media Chedongxi said, citing an interview with Qin today.

Qin said he could not disclose the number of new orders, but said "it's definitely over 10,000, and we've been over 10,000 for several months in a row."

Chedongxi reports that their visits to NIO stores also confirm Qin's claims. A salesperson at an NIO store in Beijing's Wukesong said the store sold more than 100 units in October, a good month for the year.

"Because loan rates are going to be raised in November, 1,400 cars were sold across Beijing on October 31 alone," the salesperson said.

The company attributed this to lower production volumes due to production line restructuring and upgrades and preparations for new product introductions between September 28 and October 15, as well as certain supply chain fluctuations, but did not provide more details.

In the latest interview, Qin said NIO began a revamp of the JAC NIO manufacturing site in April and May this year to allow the ET7 to be produced and delivered in the first quarter of next year and to expand the plant's capacity.

The renovation was carried out in several phases so as not to affect the production of NIO's existing models, with the latest upgrade, which began at the end of September, being a very important phase, Qin said.

One of the tasks was the expansion of the body welding line, with more than 100 new robots alone. "After the equipment goes in and is commissioned, there's another week of complementing the line and capacity creep," Qin said.

As some car companies continue to blame the chip shortage for the decline in deliveries, Qin was also asked by Chedongxi if the decline in NIO deliveries was related to that, and Qin answered in the negative.

NIO's factory was open for just 10 days, and that little production wasn't enough to be affected by the chip shortage, he said.

Separately, according to Beijing News, Qin said NIO's current production pace is normal and orders in the clog will soon be cleared.

Consumers who order NIO vehicles now can get deliveries in six weeks at most, Qin said, adding that NIO deliveries will get back on track in November and December.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

Tencent Meeting Held 4 Bn Meetings in 2020, Hit 200 Mn UsersThe outbreak of COVID-19 in 2020 damaged many sectors. The videoconferencing market was among the winners.

Tencent Meeting (global version – VooV Meeting) took its second mover advantage and tightly followed its global counterpart – Zoom. Released in late December of 2019, Tencent Meeting, although coming out seven years later than Zoom, has now become the most used video conferencing app in China. According to Tencent's vice president Yuepeng Qiu, Tencent Meeting now attains (source in Chinese) 200 million users and held more than 4 billion meetings in 2020.

At the time Tencent Meeting was presented, no one could predict its future impact in China. From its bare-bone functionalities and dated UI in earlier versions (even today 26% of its user ratings are 1-star), we could speculate that this app initially wasn't the tech giant's top priority.

Resulting from its unexcepted success, Tencent Meeting now joins the Tencent enterprise services ecosystem. The following months will see more integration between Tencent Meeting and Enterprise WeChat.

BOE Reached CNY 20 billion in Net Profit as of Q3 2021In the first half of 2021, BOE continued to rank first in the world in terms of display shipments in the five application areas of smartphones, tablets, notebook computers, monitors, and TVs.

BOE released its Q3 earnings report for the period ended September 30, 2021, on October 28.

· Operating income was CNY 56 billion, a 46.8% year-on-year increase.

· Net profit was CNY 7.3 billion, a 441.1% year-on-year increase.

· Debt ratio was 13.88%.

· Gross margin reached 44.32%.

· Financial expenses were CNY 99 million.

The First three-quarter financial reports for the IoT firm are as below:

· Revenue was CNY 163.3 billion, a 72% year-on-year increase.

· Net profit was CNY 20 billion, a 708.4% year-on-year increase.

BOE issued the "Announcement on Provision for Asset Devaluation in the First Three Quarters of 2021." The company’s provision for inventory depreciation in the first three quarters of 2021 was 3.949 billion yuan, transferred back 1.24 billion yuan, and resold 792 million yuan. Inventory impairment losses in the first three quarters of 2021. The total profit is 1.918 billion yuan.

The company also released the investment project – "BOE Chengdu vehicle display project" with CNY 2.5 billion. The project strives to start production at the end of 2022, with an annual output of approximately 14.4 million onboard display screens after reaching full capacity.

Midea Announces the First 3 Quarters' Financial Results for 2021For the first three quarters, the domestic revenue increased by 24.7% and the overseas revenue increased by 15.51% compared with the same period last year.

According to Midea's financial results for the first three quarters of 2021:

- The revenue increased by 20.57% to CNY 261.342 billion, and net income attributable to the parent company was CNY 23.455 billion, with an increase of 6.53% year-on-year. Among them, Q3 revenue achieved CNY 87,532 million (up 12.66% YoY), while the net profit attributable was CNY 8,446 million (up 4.4% YoY).

- The company's domestic revenue increased by 17% in the third quarter of 2021, while overseas revenue increased by 6.4%. By the end of September, the company had added more than 36,000 overseas private label outlets for the whole year.

- The net cash flow from operating activities was CNY 27,897 million, with an increase by 11.52% compared to the same period last year, while its own capital amounted to CNY 128.1 billion (up 2.4% YoY).

- The company's research and development expenses amounted to CNY 8,765 million, showing a year-on-year increase of 30.51%.

- The online and offline shares of the domestic air-conditioning market are 34.8% and 35.8%, respectively.

- The online and offline shares of washing machines are 35.2% and 27.5%, respectively.

- The online and offline shares of refrigerators are 18.6% and 14.5%, respectively.

Founded in 1968, Midea is a global technology group covering five business sectors. It has about 200 subsidiaries with more than 60 overseas branches and 10 strategic business units, whose products and services benefit more than 200 countries and regions around the world for over 400 million users. It was listed on the Shenzhen Stock Exchange on September 18, 2013. As of the close of trading on October 29, 2021, the company's share price edged up by 0.95% to CNY 68.77, with a market capitalization of CNY 480.2 billion, ranking first in the domestic white home appliances industry.

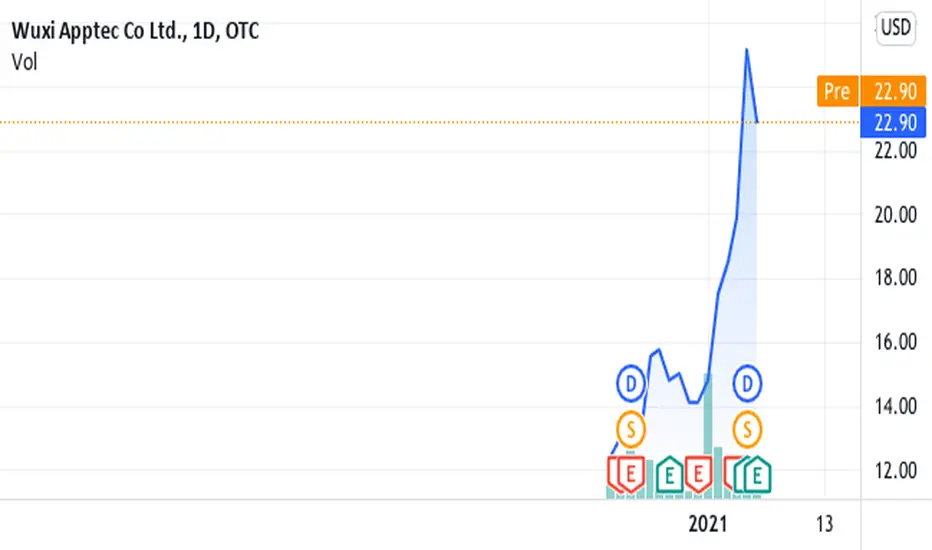

Wuxi Apptec Embraces a More Health-Conscious ChinaAfter a booming year in 2018, Wuxi has yet to slow down. The following article analyzes the success of Wuxi and its shortcomings.

China has released a number of new policies to help make the biopharma industry more transparent and efficient.

By 2020, China had full coverage of medical service systems in rural and urban areas; 90% of residents in China can access the nearest medical point within 15 minutes.

Wuxi Apptec has achieved consecutive quarter-over-quarter revenue growth for 13 quarters since the first beginning of 2018 (other than the first quarter of 2020 due to Covid-19).

Wuxi PharmaTech, a contract research and manufacturing organization, was founded by Dr. Ge Li in 2000. The company changed its name to Wuxi Apptec after Wuxi acquired Apptec Laboratory Services Inc., a US-based medical device and biologics testing company. Wuxi was delisted from the NYSE after going private, with a valuation of USD 3.3 billion. The company has thrived under the leadership of Ge Li as Wuxi went from just 4 people in 2000 to over 28,000 employees in 2021. Ge Li claims that the company's main mission is to provide high-quality research services at a low cost.

Wuxi has been growing rapidly since its inception, but we expect more imminent growth as China rolls out new healthcare-related policies and people become more health-conscious. Although the thriving healthcare market will inevitably attract new entrants that may evolve into strong competitors, Wuxi Apptec is highly likely to withstand the competition.

Rising health awareness

While brands like GNC and The Vitamin Shoppe helped raise healthcare awareness in the west, China was lackluster in this department and put little emphasis on personal well-being. Over the past decade, however, China's healthcare industry grew exponentially as society's attitude towards healthcare took a massive turn. The rising disposable income has led to the paradigm shift from being reactive consumers to proactive consumers. 84% of 3,000 respondents in China, in a survey conducted by Ipsos, reported that they are consciously making health-oriented decisions now.

According to a report by McKinsey, the global wellness economy, accelerated by COVID-19, has an estimated market size of USD 1.5 trillion as of 2021 with 5% to 10% annual growth each year. China reported the highest share of wellness spending online out of the six countries, including Japan. Monosodium glutamate (MSG) is a controversial flavor-enhancing ingredient for its possible adverse effects after consuming more than 3 grams. Major MSG producer Henan Lotus is experiencing a steady decrease in sales as the Chinese population, once the largest consumer of MSG, is becoming more health-aware. Bain and Kantar Worldpanel also reported that sales of chewing gums have also decreased by 14% in the last two years, chocolate sales decreased by 6%, and confectionaries decreased by 4%.

Favorable policies

President Xi announced the initiation of the Health China 2030 (HC 2030) plan in October 2016. The main goals are to prioritize healthcare on a national level, spur innovations in the healthcare industry, promote scientific development, and bring equal access to public health services to all parts of China, especially the country's rural areas. HC 2030 also aims to establish and enhance social policies and institutional systems regarding health, cultivate a healthy environment and intensively promote the advancement of the healthcare industry. Companies in the healthcare industry have seen something of a boost in their revenue as the healthcare trend continues. By 2020, China had extended medical service coverage so thoroughly that 90% of residents could access the nearest medical point within 15 minutes. The medical cost growth was also curbed as 2020 marked the lowest proportion of residents' medical expenditure in 20 years, with 27.7%.

Government policies have favored the development of the healthcare industry in China, especially that of Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs). In 2015, China had a backlog of over 20,000 drug registrations pending review and approval. The National People's Congress (NPC) held a meeting to discuss the reformation of the drug registration system. As a result, China Food and Drug Administration (CFDA) regulators received more resources than in the past, and the government launched the Market Authorization Holder Program (MAH) to make it easier to bring new drugs to the market. Furthermore, the Review and Approve Process (RAP) was simplified and made more efficient. For example, high-quality generics for orphan conditions with robust bioequivalence data will be eligible for expedited review during the CFDA's regulatory process. As of July 2021, a rare disease database (Orphanet) has recognized over 6,000 diseases, propelling pharma companies to roll out more medicine that will undergo a newly implemented process. CROs and CDMOs benefit from these new policies as pharma companies look to increase their research output to develop and produce new drugs. The expedited RAP incentivizes companies to roll out new drugs to cope with the increasing number of orphan diseases recorded.

The unique advantage

Wuxi Apptec is a "fully integrated contract research development and manufacturing organization with the ability to provide one-stop services that offer its clients assistance in discovery, development and manufacturing service demands." The wide variety of services that Wuxi covers allows the company to embrace the soaring healthcare market in China. Wuxi Apptec expects to extend its impact further as the global new drug R&D outsourcing market snowballs. However, Wuxi must persist in its R&D investment to fare well against companies with more flexible cash flow and new entrants with newer technology.

With a boom in customer demand, China's pharmaceutical R&D and manufacturing service market is expected to maintain its current high-speed growth. Wuxi's unique competitive advantage comes from its cost-efficient services. As of 2021, Wuxi has over 28,000 employees, most of whom are chemists, making Wuxi possibly the biggest employer of chemists in the world. Since the company has cheaper labor costs than the industry average, Wuxi can produce almost the same amount of research output for a fraction of the price (around 25% to 40% less than western companies' services).

Additionally, policies such as the MAH, expedited reviews, and HC 2030 have encouraged pharmaceutical innovations in China. Wuxi can capture the rising demand from Chinese pharma companies with its rather high R&D efficiency. Although Wuxi may not have the financial strength of some significant pharma companies with in-house R&D departments, the company will retain its leading position as one of the most profitable R&D and manufacturing businesses in China.

Financial metrics

According to Wuxi's interim report this year, the company realized CNY 10.54 billion total revenue, a year-over-year growth of 45.70%. CNY 2.50 billion came from China, which represents year-over-year growth of 48%. This data showcases the company's ability to capture the rising healthcare tides and demands for research and innovations. 48% growth also marks the largest increase compared to the company's revenue growth in the US and Europe. Wuxi also has a 100% retention rate of its top 10 customers from 2015 to the interim of 2021. As of June 30, 2021, the company's new clients have contributed CNY 849 million in revenue. Frost & Sullivan published a market research report in June 2021, which ranked Wuxi Apptec first by market share in the China-based drug discovery CRO market, pre-clinical and clinical CRO market, and small molecule CDMO market.

Bottom line

The combined forces of new policies and rising healthcare awareness have put Wuxi Apptec in a prime position to consolidate its leadership in China. The company should remain profitable as long as it maintains below industry average labor cost, heavy investment in its R&D department and reasonable M&A strategies to help expand and improve Wuxi's services and operations. Given the recent regulatory crackdown on Chinese tech companies, Wuxi should tread carefully in its effort to capture a more significant share in the Chinese market.

China's rapid growth in the healthcare industry bodes well for the nation, but what does it mean for its people? While the government poured resources into promoting innovations and development in the medical field, the affordability issue gained little attention. Although China has over 90% of residents with basic health insurance plans, it still poses a hefty paycheck for the average worker. Despite the rising wave of healthy living, China has to do more to provide sustainable healthcare.

For the full article with the charts, please visit the original link.

Tesla's Record in Q3 Reflective of China's Solid EV FoundationDespite a great Q3 overall, Tesla in China sees demand reduce as competitors begin to catch up.

Share prices for Tesla have soared to all-time highs after earnings and amidst reports of a 100,000-car deal with car rental company Hertz. Demand has not been the main issue for Tesla outside of China seeing that orders have backlogged out as far as May and prices on models have been raised. The global supply crunch has been their biggest obstacle to navigate so far. Tesla in China though is in fact seeing an isolated demand crunch while domestic firms are pouncing to shift demand in their favor.

We believe Tesla's record revenue of USD 13.76 billion in Q3 is not only reflective of Tesla's success but China's impactful support. The earnings report states, "For all of Q3, China remained our main export hub. Production has ramped well in China, and we are driving improvements to increase the production rate further." Not only are a significant amount of all Tesla models produced in Giga Shanghai, but Ningde-based CATL already has a contract to produce batteries for Tesla until 2025. CATL also signed a 10-year contract with Great Wall Motor in June of 2021. EV's are getting a foothold in China the way internal combustion engine vehicles were in Japan around the 90s.

Domestic brands are gaining on Tesla's share of the Chinese EV market

Sales in China leaped nearly 50% in August but only 20% in September for Tesla. Their market share of BEV sales has declined from 17% in April to 11% despite the steep price reduction for the Model Y SR+ and amidst intense media scrutiny. BYD is now atop them with 14% of BEV sales in China. The domestic brands are clearly gaining consumers' favor in China as of Q3 sales for BYD, Xpeng, and Li Auto nearly tripled and NIO's sales doubled all year-over-year(YoY). Going forward, Tesla still generally expects to “achieve 50% average annual growth in vehicle deliveries” over a multi-year horizon which is quite impressive. In the world's biggest EV market, however, it does seem demand for Tesla is declining at least relative to the competing rivals. Even if Tesla can recuperate some consumer appeal, investors should expect Chinese automotive firms to continue to gain ground assuming supply can keep up in scaling for 1.45 billion people.

More players both new and old

Nonetheless, as other emerging players begin to throw their hat in the ring like Xiaomi, Evergrande Auto, as well as international makers like Volkswagen and Toyota, there could be less room for Tesla to dominate demand. Especially if the market's fragmentation gets remedied and China solidifies its leaders of the industry, the winners of this race will be the Chinese investors. NIO has already started selling its ES8 electric SUV in Norway, challenging Tesla outside of China for the first time and has targeted Q4 of 2022 for launch in Germany. Tesla expects production up and running at Giga Berlin by the end of 2021.

Legacy automakers will certainly be Tesla’s biggest global competitors because of high client adhesiveness as well as industry expertise. Within China, however, it is likely that there is only so much space in the EV market for successful international firms to squeeze in with the nationally favored domestic firms. Since Tesla has the technological prowess and resilience as a company to continue to spearhead the global EV market, it should end up in the long run as China’s premier foreign producer of EV’s. Though China isn't a completely autarkic environment, investors should still expect a sturdy path forward for Chinese EV’s to grow profitable and successful. Though there are limitations in the current global economic climate, those who can weather the storm will be rewarded.

The bottom line

Tesla has benefitted competing firms with good influence and transparency as well as a commitment to growing China's EV market. In 2021 though, Tesla's declining position could be attributable to issues with recalls to refine autopilot systems as well as other negative sentiments from the trade war. The US does claim China unfairly favors its domestic producers and contributes to accelerating the negative press. Investors should expect that regardless of legality in their execution, China will aggressively promote their EV makers at home and abroad. Even if Tesla overcomes these road bumps in navigating this massive foreign market, there should and likely will be enough room for the best EV firms in China to grow and flourish. After all, Tesla is likely to grow too big to ignore especially in the world's current hottest EV market. But China's more urban-oriented driving habits do favor domestic producers of mini EV's. With that being said, these infantile EV makers have a lot on their side and will cater directly to the needs and appeal of Chinese consumers.

For the full article with the charts, please visit the original link.

Luckin Coffee Settles USD 175 Mn Class Action Lawsuit Over FraudLuckin denied wrongdoing in agreeing to settle while its U.S.-based lawyer did not immediately respond to media requests for comment on Tuesday.

After their founding in 2017, Luckin Coffee's hype and share price peaked around early 2020 as they broke out to rival global coffee icon Starbucks. Then Muddy Waters Research dropped a bombshell claim of falsified revenue on behalf of the company to inflate share prices. The internal probe found that its chief operating officer and other staff fabricated about USD 310 million of sales in 2019, or about 40% of annual sales projected by analysts. The SEC stated that Luckin raised more than USD 864 million from equity and debt investors while the fraud was taking place. The Securities and Exchange Commission consequentially delivered accounting fraud civil charges and fined Luckin USD 180 million last December.

Then came the fall from grace. Within two months their share price sank more than 80%. Shares are now trading around USD 15 as the stock is up an impressive 220% in the past year. Their unaudited financials for the first half of 2021 show that they achieved a 16% store-level profit margin and that net revenues increased over 106% resulting from higher net selling prices and an increase in items sold. They've still managed to achieve positive revenue growth amidst all of the settlement fees and negative publicity. Luckin Coffee also still manages to operate around 5,259 stores in China maintaining a firm presence. Things should be looking up for Luckin as the clouds clear while investors can capitalize on their refocus.

XPeng to Launch 800v, 480kW Overcharge... and Super Energy Storage Station.

The CEO of XPeng Inc. predicted that the penetration rate of new energy vehicles would reach 50% in 2025.

On October 24, Xiaopeng He, CEO of XPeng Motors, said that XPeng hopes to be the first 800V high-voltage platform equipped with silicon carbide chips in mass production, aiming to achieve the endurance of 200 kilometers after charging for 5 minutes. Meanwhile, XPeng will also launch the supporting 480kW high-pressure overcharge pile.

The energy storage station designed by XPeng can meet the overcharge of 30 vehicles at the same time. In other words, XPeng will launch three schemes in terms of energy supplement, that is, 800V, 480kW overcharge and Super Energy Storage Station, respectively.

In addition, XPeng also announced its exploration progress in electrification and intelligence. It is reported that it's Xpilot 2.5 accounts for 89.74%, and the activation rate of version 3.0 with high-speed NGP is 59.29%. He pointed that intelligent-assisted driving is not automatic driving, where man-machine driving will be an inevitable choice for a long time.

It is worth noting that Xinzhou Wu, vice president of XPeng's auto-driving business, said that the urban NGP function is expected to be launched in the first half of 2022 and will be tested on some roads in the first batch of cities.

In January 2021, XPeng's NGP was officially opened to users. Users can realize automatic navigation-assisted driving from point A to point B based on the set navigation route. The high-speed NGP function realized by XPeng P7 can cover most domestic expressways and some urban expressways. Apart from the functions of ACC adaptive cruise, LCC lane-centering assistance, ALC automatic lane change assistance, some other functions include but are not limited to automatic lane change, automatic speed limit adjustment, overtaking at night, ramping in, and out.

BYD Reportedly to Raise Battery Prices by Over 20% Next MonthBYD's reasoning is that the raw materials for lithium batteries have been rising due to market changes, power restrictions, and production limitations.

BYD, China's largest new energy vehicle company, is also the second-largest local supplier of power batteries after CATL. As costs rise, the company is said to be raising the price of its batteries.

BYD will raise the unit prices of its battery products, including CO8M, by no less than 20 percent from November 1, the Securities Times said Tuesday, citing a document.

BYD argues that the raw materials for lithium batteries in 2021 continue to rise with the price of cathode material LiCoO2 rising by more than 200 percent and electrolyte prices rising by more than 150 percent.

Material supply continues to be tight, resulting in a significant increase in comprehensive costs, according to the Securities Times.

Since November 1, BYD and its customers will sign new contracts for new orders and implement new prices, and orders for old contracts that have not been completed will be closed and canceled, according to the report.

Local media cls.cn then quoted BYD insiders as saying that the information is currently being verified.

It's unclear whether CO8M batteries are power cells used in new energy vehicles, and public sources can't find an explanation of the term.

BYD is also one of the world's largest suppliers of batteries for cell phones and ranks second in China's power battery market.

Data released earlier this month by the China Automotive Battery Innovation Alliance showed that BYD's installed power battery capacity in China was 14.73 GWh from January to September this year, with a 16 percent market share.

CATL's installed capacity from January to September was 46.79 GWh, ranking first with a 50.8% market share.

It is worth noting that BYD's power cells are mainly supplied to itself and have been used in some other brands' new energy logistics vehicles since 2018.

This year Ford Mustang Mach-E and some FAW Hongqi models started using BYD's power cells.

In May, the Digi Times reported that with the price increase of China-made Tesla Model 3, rumors said CATL might follow with a 10 percent price increase.

The report mentioned that LFP raw material prices have jumped 50 percent this year, but battery suppliers have taken on the pressure of the price hike themselves for fear it would lead to lost orders.

Citing sources, the report said most LFP battery makers want CATL to take the lead in raising prices in response to the steep rise in LFP material costs, making it easy for the industry to follow suit.

CATL later responded that the report that its LFP battery offer would be raised was not true.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

Alibaba Sheds USD 344 Bn Since October 2020Following the exile of Jack Ma, shares of BABA tumbled down from all-time highs a year ago.

No company has incurred more of a loss in market capitalization than Alibaba in the last year. None have come close to the large figure. Ever since Ma publicly expressed forthright discontent with the financial system of China, investor sentiment around the successful giant has dwindled. The price of shares consequently halved into late September and are still fairly dormant improving to USD 173.

Jack Ma has recently been photographed in the Netherlands browsing agriculture tech after his public reappearance in Spain a week ago. Shares have rallied around 7% ever since. The company's presentation of a new server chip on October 18 has further helped improve share price. The chip is based on advanced 5-nanometer technology designed to support the company's growing cloud computing business.

Alibaba will likely report earnings on November 4th where investors can expect strong business growth, and another revenue beat. Though there are still considerable risks that investors should not ignore, Alibaba should still be a solid pick for the coming years.

China fear was an entry opportunityIn my latest post on the 19th Jul 2021, I mentioned: "It is possible that wave 2 is not complete yet and we may see another leg down before taking off hard to make new highs as the 3rd impulsive wave."

This is what happened and we should be on our way to the higher prices. Target 1 should be $59 and Target 2 should be $74 for the medium term. Note that still there is a slim possibility of morphing this correction to a more complex pattern, however as China fear pushed the Chinese stock prices to lower prices and offered an opportunity to get in at lower prices, such a pattern conversion should be regarded as an entry opportunity. EV stocks will shine in 2022 and 2023 as the sales will be more prevailing and more companies will come up with new EVs and technologies. As an example, Toyota has promised the introduction of 70 new models until 2025 out of which 15 will be fully electric. $LCID and $FSR are the two notable EV companies in the US that will introduce their luxury sedan and cross-over SUV in 2021 and 2022 respectively.

My last post on $XPEV:

Please DYODD. This is not financial advice.

Volkswagen's EVs Taking Off, May Surpass NIO's Market Share Volkswagen's EVs Are Taking Off in China, May Soon Surpass NIO's Market Share

On October 22, SAIC Volkswagen ID.3 was launched in the country at CNY 159,888 to CNY 173,888 per vehicle.

Volkswagen China achieved a milestone of 10,000 EV sales in September 2021.

We dissect Volkswagen's EV sales through three perspectives: product, production and marketing.

A solid EV lineup, concrete production capacity and improved marketing have made VW one of the fastest legacy brands shifting to an EV company status.

We expect VW to surpass NIO and Xpeng's market share very soon but remain shy of Tesla or BYD.

The global chip shortage has hurt the auto industry, with companies at the risk of cutting more production. Electric vehicles built on more technology attributes that need more chips should have been hit badly. However, Volkswagen China delivered stellar EV sales in Q3, which grew from 3,415 units in June to 10,126 units in September, eclipsing NIO and Xpeng's growth rates in the same period. As an EV brand once underrated by some Chinese consumers, how did the company lift its sales so quickly? This article will rewind Volkswagen's EV story in China and give it an outlook.

Entering the mainland market

Before entering China, in 2020, Volkswagen Group sold 56,500 ID.3 in Europe during the final four months, which proved ID's strong product power. One year later, VW started to consider launching and manufacturing special ID models in China. According to an official announcement, Volkswagen Group (China) rolled out two new IDs based on MEB's innovative modular electric drive platform at the end of 2020, including pure electric models FAW-Volkswagen ID.4 CROZZ and SAIC Volkswagen ID.4 X. The two models are larger than ID.3 and tailored to Chinese consumers. They had started production in Foshan and Anting factories, and the products would be launched in early 2021. These two plants have a total annual production capacity of 600,000 vehicles. So, Volkswagen is one of the earliest legacy car makers that put EVs into production in the Chinese market.

With a concrete production line, the company began to pre-order ID.4 in China at the beginning of 2021. Compared with Tesla, Xpeng and NIO's lineup, some argued ID series were uncompetitive for shorter driving ranges, lacking intelligent features. But VW China has refreshed people's minds with spectacular sales growth.

In the beginning stage of selling, ID didn't perform well. The auto insurance data showed April saw 2,140 units sales of ID.4, which is tiny for the auto behemoth. Later on, VW adjusted its policy with the dealership network to stimulate them to sell more EVs, set a new team to deal with NEV sales and trained a special EV sales team to find the momentum.

Another critical initiative Volkswagen made is an omnichannel selling strategy. ID models are sold in the existing 4S stores and shopping malls. The shopping mall stores are invested and built by existing dealers, and there is no directly operated shop of OEMs. The company learned new retailing strategies from Tesla and NIO's success using multi-channels to acquire traffic. Volkswagen is opening EV-only stores in more malls, namely through ID. Stores. There are dozens of stores in Shanghai. It is also expanding into other megacities.

Following more ID models exhibited in shopping malls and 4S stores, ID saw a surprising increase in sales, which broke 10,000 monthly sales six months after delivery. By comparison, it cost NIO and Xpeng two years.

Will VW keep growing sales fast in the future?

We expect VW to acquire a larger market share in the following period. We judge the future delivery range of an NEV company from a perspective of the product, production capacity and marketing. ID models' product has won EU consumers' acceptance and should be accepted by the Chinese. The production capacity may be a problem, but Volkswagen has a one-million-global-EV-sales target this year, which was set when the firm was well aware of the supply issues. It ought to prioritize new energy vehicles production, and the inventory purchased at the end of 2020 can be used for some time. So, sales should continue to rise, but supply chain issues will impact capacity. Besides, the popularity of Volkswagen electric cars is increasing as more shops are built. By the end of this year, monthly sales are very likely to set a new record again.

To discuss the sales 'ceiling' of ID, we have to benchmark it to the industry leaders such as Tesla and BYD. After one year of mass delivery in China, Tesla gained its EV market share between 10-15%. BYD is shifting towards a full-EV brand and takes around 20% of China's NEV market. We believe Volkswagen is far from catching up with these two companies for being a legacy player but can surpass NIO and Xpeng's respective market shares in a year based on recent sales momentum.

In a nutshell

VW's solid EV product, concrete production capacity and omnichannel sales system made it one of the fastest legacy brands to complete an 'EV shift.' The sales momentum hints its future delivery will keep jumping. Although we don't think the company will quickly transform into an EV leader like Tesla in the premium segment or BYD in the lower price bands, it is very likely to grow its market share to overtake NIO or Xpeng's in the short run.

For the full article with the charts, please visit the original link.

Alibaba Cloud to Launch New Data Center and AI-Powered AssistantAn exciting day arrived for Alibaba Cloud as the company unveiled its new meeting assistant AI and announced the launch of a new data center planned for next year in South Korea. The company is trying to end the year strong as it continues to roll out more innovations and future plans.

Alibaba Cloud announced the launch of its first data center in South Korea in the first half of 2022. The new data center will offer its clients in South Korea more reliable and secure cloud services as well as highlight the company's effort in its commitment to empowering South Korean businesses' digitalization.

Unique Song, the regional general manager of Japan and South Korea, said that "South Korea is a strategic market for Alibaba Cloud and we are building the new data center to address the increasing demand for cloud infrastructure services from local clients. Together with our global data network, we will continue to help our South Korean customers heighten their pace of digital transformation and global expansion through the latest cloud computing technologies and ecosystem support".

Alibaba Cloud also unveiled the brand-new AI-powered meeting assistant, Tingwu, and a new version of the company's cloud computing. These new enterprise solutions aim at the growing popularity and surging demand of working remotely. Tingwu was developed by the global research initiative Speech Lab of Alibaba DAMO Academy. The meeting assistant is able to convert spoken words during a meeting into writing with 98% accuracy. Tingwu can also distinguish up to 10 meeting participants' voices and can handle English, Mandarin and 14 other Chinese dialects as well as generate meeting summaries and highlights.