Is this the bottom? Double your money from these levels?It may or may not be the bottom, may be another $10 downwards. But this is the time to buy chinese stocks. If it looses another $10 then buy more. My long term target is $150.

Chinastocks

BYD, China's Next Hardware GiantAccording to Wilson's report, the average price of BYD's vehicles has surpassed that of popular joint venture brand Volkswagen by about CNY 10,000.

BYD is an automobile company that provides vehicles, EV batteries, semiconductors and electronics foundry services.

We estimate its stock's value based on the sum-of-the-parts (SOTP) method.

The company's EV and battery businesses account for most of the valuation.

We consider BYD to be currently undervalued and expect a 22% upbeat.

In 2020, the Chinese NEV market had a stellar performance – NIO, Xpeng and Li Auto all delivered considerable volumes of vehicles. Meanwhile, we spotlight BYD, a car maker once invested by Warren Buffett, as a best-in-class electric vehicle company. With its solid fundamentals, BYD is likely to become a major hardware conglomerate – much like Tencent or Alibaba in the consumer Internet sector. This article will examine the company's business segments, touch upon potential risks, and conduct an SOTP analysis to value its shares.

Intro

Wang Chuanfu incorporated BYD in 1995, inspired by the prospects of the Li-ion battery applications. Since then, he has led the company, building it into an agile manufacturing mammoth capable of starting new ventures and succeeding quickly across many fields. For one, BYD started to produce face masks in the first days of the COVID-19 outbreak and has now become the biggest mask producer worldwide. Its business segments remain the same though – those are internal combustion engine (ICE) vehicles, EVs, power batteries, auto semiconductors and electronics assembly services.

Auto OEM

BYD sells both ICE vehicles and EVs, primarily in China (but is getting more active abroad).

In 2020, it sold 231,000 units of ICE cars, a year-on-year (YoY) increase of 3.8%. The parts sales accounted for a significant share of total revenue but remained less profitable. Now, BYD is full speed ahead to transform itself into an EV-based company. Because BYD didn't disclose its total ICE car sales revenue, we broke down its revenue streams and assumed the average selling price (ASP) was between CNY 100,000 to CNY 110,000. Therefore, ICE generated revenue of CNY 24 billion in 2020. We expect the ICE business will drop 10% in the next few years as the sales momentum will shift to EV. In 2022, the revenue will reach CNY 19.4 billion. With a 2x PS ratio based on Great Wall Motor and Geely Auto, the ICE business will be valued at CNY 38 billion.

In the meantime, EV sales has become the most valuable business – last year, BYD sold 162,000 EVs, a YoY decrease of 12.5%. After upgrading the 'dynasty' EV series, BYD entered the middle-to-high-end market. The series adopts self-made 'blade batteries' to prevent EV from battery catching fire. The hit model 'Han,' a car somewhat similar to Tesla's Model 3 and Xpeng P7, sold 8,522 units in July, surpassing the sales volume of NIO and Xpeng.

According to the 2020 financial report, BYD made CNY 24.4 billion in revenue from EV sales. We project the EV sales will increase by 100% (based on the fact that sales from January to July 2021 surpassed last year's figure) and by 25% in 2021 and 2022, respectively. We also assume the ASP will increase by 5% in 2021 and 2022 as more high-end models are delivered. For these two years, the revenue will hit CNY 51 billion and 67 billion. With a 10x 2022 PS ratio, the EV department is worth CNY 670 billion.

Power battery sales is another core business for BYD alongside EVs. According to SNE research, BYD's installed capacity reached (link in Chinese) 7.8 GWh during the first half of 2021, ranking No.4 worldwide. This is 23% of CATL's installed capacity. Therefore, conservatively speaking, we estimate the market capitalization of BYD's battery division will be one-fifth of CATL's. Thus, the power battery business is worth CNY 240 billion, based on the fact that CATL's market cap had already reached CNY 1,200 billion as of August 9, 2021.

BYD Semiconductors

Semiconductor manufacturing is another important segment for BYD. It is set to be spun off from BYD to go public. It features auto semiconductors, which provide IGBT, smart control IC, sensors and optoelectronic semiconductors. BYD semiconductors can independently design, manufacture, package and test chips. It is the only company to achieve this in China. Based on our latest report, auto chips will be in high demand as more vehicles will be electrified in the future. As per BYD's 2020 report, the semiconductor business was valued at CNY 7.5 billion in May 2021. We believe the figure will triple while launching on the open market. It is estimated that BYD will deliver semiconductors worth up to CNY 20 billion.

BYD Electronic

Apart from providing high-end products, BYD also made CNY 60 billion toplines (38% of total 2020 revenue) from assembling smartphones, tablet computers and laptops. These products show low profitability similar to other electronics foundries like Hon Hai Precision. We refer to Hon Hai's 0.25x 2022 PS ratio and project 12% growth in the next two years. We calculated that BYD Electronic is valued at CNY 18 billion.

To sum up, BYD is valued at CNY 988 billion. Even so, we think the estimation is a bit conservative as some assumptions aren't considered in it. BYD's EV will deploy more self-made batteries and chips, which will save a lot of costs for the company in the long term. What's more, rumors said BYD's battery had been tested by Tesla and would likely be equipped with Tesla's vehicles. This potential opportunity will significantly boost BYD's valuation in the battery division.

Risks

BYD's EV sales were affected by the industry's downslide in 2019 and 2020. Moreover, the EV market has been involved with intensified competition, as proved by the price slash of a few models and few companies leaving. BYD, with its comprehensive business mix, should have the means to face these challenges.

Conclusion

Viewed as part of the big picture, BYD is a company less profitable than some of its auto peers – one with a 2.6% net profit margin in 2020. We consider the company to have set margin improvement as a long-term goal, while also expanding in the EV battery and related battery segments. Although BYD just saw a market cap rally in the past few days, we believe it is still undervalued and has a 22% upbeat opportunity as of August 20, 2021.

$KXIN Ready for a Rally ? Merger Talk?!Scince the announcement of $KXIN that they will enter the "small Electro Vehicel" market shares are already going strong with high volume ...

Now we have news about a merger and there are some rumors of possible partners in play ....

technical we see some S/R flips in and we have just recently closed above another resistance ...

in case we can break this resistance zone there are no doubt of a price around 5$ a share ,this is also our next bigger resistance level , after market is able to break that level we have open space all the way to 10$ a share ...

Time will tell .... and always remember you are not married to the stock nor you wanna be a bag holder ;-)

good luck and have a great week

Trueman23

Niu Technologies Announces Q2 2021 Financial ResultsIn Q2 2021, the company generated CNY 944.7 million in revenue, with a year-on-year increase of 46.5%.

According to Niu Technologies' Q2 2021 financial announcement:

- Revenue rose by 46.5%, reaching CNY 944.7 million.

- The gross profit margin was 22.7%, compared with 23.0% in the same period of 2020.

- Net profit hit CNY 91.8 million, representing a 61.6% growth, and the net profit margin was 9.7%.

- In Q2 2021, the company's sales volume hit 253,000 units (up 58.0%), with only 2.8% sales from overseas markets.

- Among the firm's major business, the revenue of electric scooters in the domestic market recorded CNY 758 million, representing a growth of 44.9%; its overseas revenue from electric scooters hit CNY 57.7 million, increasing 1.2% compared with 2020.

- The sales from low-priced models G0 and F0 represented 30.4% of total sales volume, declining from 38.2% in Q1 2021, with revenues pre scooter up 8.3% month-on-month.

- At the same time, Niu Technologies' sales and marketing expenditure reached CNY 68.9 million, showing an increase of approximately 51.1%; its R&D expenses hit CNY 30.8 million, with a rise of about 28.7%.

- By the end of August 16, 2021, the company's market capitalization was USD 1.7 billion (about CNY 11.0 billion), evaporating by CNY 15.4 billion.

The worst is over for Chinese stocks BABAIf you are a long term investor I hope you used the panic to top up your holdings. If you are a momentum trader you still have the opportunity to ride the bounce or accumulate your position a bit later. Possible scenario for BABA but all names have something similar is as follows.

I treat that panic as an exhaustion and behavioural pattern confirms that so I consider the worst is over.

Personally, I played that dangerously catching falling knives and loosing hairs so my words bring some sort of hope, but from technical perspective the situation is as follows.

Another option is to treat the current leg up as a retest of the previous support but usually when you have seen that sort of panic and all the papers writing the same thing - it is just over.

I expect some turbulence at this resistance since bears will try to play down the move but final move is gonna be UP.

The first arrow is my initial momentum play. I expect to see some kind see-saw after the first leg and the second arrow reflects my further expectations.

The worst is over for Chinese names BIDUIf you are a long term investor I hope you used the panic to top up your holdings. If you are a momentum trader you still have the opportunity to ride the bounce or accumulate your position a bit later. Possible scenario for BIDU but all names have something similar is as follows.

I treat that panic as an exhaustion and behavioural pattern confirms that so I consider the worst is over.

Personally, I played that dangerously catching falling knives and loosing hairs so my words bring some sort of hope, but from technical perspective the situation is as follows.

Another option is to treat the current leg up as a retest of the previous support but usually when you have seen that sort of panic and all the papers writing the same thing - it is just over.

I expect some turbulence at this resistance since bears will try to play down the move but final move is gonna be UP.

EO500 Tracker: Tencent Boost Overseas Sales Amid COVID-19Founded in 1998, Tencent is one of the oldest big tech companies in China. The tech giant has dominated the entertainment universe, focusing on integrating its digital ecosystem.

With the acquisition of Riot Games, Tencent has amplified its global influence in the entertainment and game industries. In recent years, while its funding activity in some countries, like Korea, were entertainment-focused, the firm's M&A and investment in other regions, such as India, were more comprehensive, aiming to build an ecosystem.

In 2020, the company invested more than CNY 275 billion (year-on-year growth of 84%) in overseas markets, focusing on North America, Asia and Europe. Meanwhile, its overseas revenue hit CNY 33.9 billion in 2020 compared with CNY 16.7 billion in the previous year.

EO500 Tracker: BYD Boosts Overseas Sales Amid COVID-19 PandemicCOVID-19 has severely affected global markets. As per the recent IMF report, the world's GDP declined by 3.5% in 2020, with a significant increase in unemployment, disposable income reduction and lowered productivity in secondary and tertiary industries.

At the same time, this period of turbulence separated the wheat from the chaff, filtering out uncompetitive companies. Adjusting their businesses, many firms have responded with localization strategies, while others have seized opportunities in overseas markets to reinforce their global influence.

Among the 45 largest (by market cap) publicly-traded EO500 companies, 16 firms saw their overseas revenues increasing in 2020. In this regard, BYD, Xiaomi and Tencent were among the best performers, with year-on-year growth of 203%, 34% and 103% respectively.

Founded in 1995 and swiftly known as a pioneer in battery technology, BYD (01211:HK) expanded its footprint worldwide, with operations in over 50 countries and regions. It has a strong market presence, principally participating in the automobile business, offering traditional fuel-engine vehicles and new energy vehicles, rechargeable batteries, handset components and other related products.

With the strongest performance in the international market amid the pandemic and global economic uncertainty, the company's overseas revenue rocketed from CNY 19.5 billion to CNY 59.1 billion, establishing a leading position in the global new energy vehicles sector.

Such a massive growth was driven mainly by the combination of improved product quality and growing demand. With a patent portfolio covering lithium iron phosphate batteries, control technologies in bidirectional converters and high-power charging systems, BYD continues building its high-tech prowess.

Besides the firm's technological advancements, cost advantage is speeding up the process as well. In recent years, BYD tried to localize its production worldwide, establishing manufacturing plants in numerous countries like the US, Brazil, France and Hungary. This long-term development strategy helps the company minimize costs and avoid tariffs, providing advanced after-sale services.

EO500 Tracker: Xiaomi Boosts Overseas Sales Amid COVID-19Among the 45 largest (by market cap) publicly traded EO500 companies, 16 firms saw their overseas revenues increasing in 2020. In this regard, BYD, Xiaomi and Tencent were among the best performers, with year-on-year growth of 203%, 34% and 103% respectively.

Xiaomi (01810:HK), established in 2010, has emerged as a top consumer electronics brand. The company offers numerous products like smartphones, laptops and smart home products, garnering support in more than 100 countries and regions around the world.

With a large share of many European and Asian countries' markets, its overseas revenue increased steadily amid the epidemic from CNY 91.2 billion to CNY 122.4 billion, accounting for 49.8% of total revenue.

In June 2021, the firm's global mobile phone market share rose to 17.1%, overtaking Samsung (15.7%) and Apple (14.3%). Meanwhile, its mobile phone sales grew by 26% on the back of Huawei's decline and prioritization of 4G and 5G-enabled smartphones, marking it the fastest-growing brand for the month.

Cautiously Optimistic for BABABABA currently has strong support at ~180 level. This beaten-up stock has a lot of China uncertainty built into the current price, and it is an extreme discount from fair value evaluations. More turbulence in China could cause more turmoil in the future, but BABA is still a compelling long-term opportunity in the 180-190 range.

iQIYI Earns CNY 7.6 Bn in Q2 2021Owing to the success of original TV dramas, the large Internet content company still maintains remarkable revenue in the off-season.

On August 12, 2021, iQIYI published the unaudited financial report for the second quarter of 2021. In the second quarter of 2021, its total revenue reached CNY 7.6 billion, up 3% year over year. Among them, the revenue from member services reached CNY 4 billion, accounting for 52% of the total revenue, while the revenue of online advertising services reached CNY 1.8 billion, accounting for 23%. Meanwhile, in the second quarter, iQiyi's revenue cost reached CNY 6.9 billion, of which the content cost was CNY 5.1 billion, basically the same as the same period in 2020. It is worth mentioning that the company's net loss was reduced to CNY 1.4 billion, which has narrowed year-on-year for five consecutive quarters. The company also announced that, as of June 30, 2021, the company had 106.2 million subscribers.

Yu Gong, CEO of iQIYI, said that although the second quarter was an off-season, driven by the company's continuous launch of original TV dramas, its subscription members increased significantly and continued to lead the market in a number of operational indicators. At the same time, iQIYI Extreme App for users in sub-tier cities in China and the company's overseas business have shown a strong development momentum.

A Glance at Ant Group 's Technology VentureThe wave of fintech has spread to the insurance industry, giving rise to the 'Insurtech' and the related niche markets. However, in China, the insurance penetration rate (2.7%) and premium per capita (USD 47) are both lagging, leaving much room for potential. Chinese Big Tech is seizing this opportunity and the competition is just getting started.

The term 'Insurtech' is self-explanatory, expressing the blending of technological solutions with insurance. By applying such technologies to various scenarios, insurance companies boost service quality and expand their product portfolios. In a broader sense, Insurtech is an innovative technology cluster consisting of new digital tools developed to optimize the performance of insurance companies and to deliver a better customer experience. A strong point of Insurtech to date has been strengthening companies' underwriting abilities by incorporating artificial intelligence-based risk assessment. This boosts revenue by allowing them to move into adjacent niche markets.

The emergence of new technologies has installed new dynamics in insurance products while also adding more complexities. When traditional insurance companies and Internet giants are drawn to share a piece of the market, the competition is likely to intensify in the short term.

The Chinese insurance market has grown rapidly over the past decade, and so has the Insurtech segment. The tremendous development that Insurtech has experienced was mainly driven by changes in customers' behaviors (according to EY, 59% of mainland China's life insurance consumers' preference for interactions and relationships with insurers skews strongly toward digital), technology advancements (big data, IoT, blockchain, Cloud computing, etc.) and more supportive policies. Several internet giants in China have entered the market as distributors by utilizing their large volumes of traffic, while the traditional risk carriers – or to say, insurance incumbents, have also made scaled investments in technology solutions. Other technology enablers, such as start-ups focused on specific pain points in insurance operations, have accounted for a part of the whole market as well.

Ant Group's insurance play

In July 2017, China Banking and Insurance Regulatory Commission (CBIRC) announced the approval of the establishment of Hangzhou Baojin Insurance Agency Co., Ltd, a wholly-owned subsidiary of Ant Financial. After six months, the company officially changed its name to Ant Insurance Agency Co., Ltd — the same old trick other big names always play — which hinted at the company's ambition to fully enter the insurance industry.

AntSure (as it is named in the English version of Alipay), a one-stop platform for servicing insurance needs, is designed to assist insurance company partners to provide a wide range of innovative, customized and easy-to-obtain products. Up to H1 2020, the Alipay-owned insurance platform had closely cooperated with over 90 Chinese partner insurance institutions, offering over 2,000 products, covering areas from life insurance, health insurance to property insurance and other customized products.

The company's revenue mainly comes from the technical service fees paid by the partners based on the premiums and apportioned amounts promoted by Ant Insurance Agency. According to the prospectus for the Hong Kong IPO, the insurance premiums enabled through Ant Group's platform – as well as contributions by Xianghubao (i.e. an online healthcare mutual aid program launched in October 2018, which aims to provide mutual protection with no upfront payment or admission fees required) participants – reached CNY 52 billion for the 12 months ending June 30, 2020, and the total number of customers served reached 570 million.

The biggest advantage of the in-house agency platform is the huge traffic acquired through Ant Group's products. The huge user base accumulated in the early stage of superapp Alipay and Alibaba-based e-commerce have laid a solid foundation for the rapid expansion of Ant Insurance Agency, making it the largest online insurance services platform in China, according to the prospectus.

In addition to platform-based insurance, Ant Group also has scenario-based insurance offers that are closely connected with Alibaba, Alipay and other businesses, such as consumer insurance, Alipay's account security insurance, freight insurance and so on.

NIKOLA: NKLA Can Be A Good Buy NowTraders, Nikola price has been it badly but it has reached a level where it can be a good buy on the completion of a good FCP pattern. Beware of the fact that this pattern can become extended to the downside. Hence we have to possible BUY zones

Rules:

1. Never trade too much

2. Never trade without a confirmation

3. Never rely on signals, do your own analysis and research too

✅ If you found this idea useful, hit the like button, subscribe and share it in other trading forums.

✅ Follow me for future ideas, trade set ups and the updates of this analysis

✅ Don't hesitate to share your ideas, comments, opinions and questions.

Take care and trade well

-Vik

DiDi: Charged by Regulators, Stumbles after Launching its IPOThe central government's probes into major tech-oriented transportation companies are obscuring the development of the likes of DiDi.

DiDi took only 20 days to be listed in the US market, which appeared odd to investors and regulators.

With over 22 rounds of financing, the mobility company has long been under pressure to make profits for its shareholders.

DiDi has occupied a large share of the world's mobility market but still struggles to reach profitability because of high operating risks.

The Chinese government's investigation inserted high political risk into any plan to invest in the company's stock.

On June 30, 2021, DiDi was listed on the New York Stock Exchange with a ticker of DIDI. It offered 317 million ADS with an initial price of USD 14 and raised at least USD 4 billion during its IPO. Oddly, the company took only 20 days to go public and determined the issue price only three days after the roadshow, one of the shortest IPO processes in recent years.

The IPO price increased to USD 16.65, up 18.93%, on the IPO day, and the company's market value reached USD 79.8 billion. However, its stock continued to depreciate after that.

Founded in 2012, DiDi Global has been constantly strengthening its business in a quest to become the world's largest mobility technology platform. In 2013, owing to massive investments from Alibaba, Tencent and a few other companies, Kuaidi Dache and DiDi formed a duopoly market in the mobility field in China. The two companies merged in 2015, rebranding as DiDi Global. In 2016, the company acquired the Chinese branch of Uber, monopolizing the domain in the country.

As of March 2021, DiDi spanned more than 4,000 cities and towns in 15 countries, providing online car-hailing, taxi, free riding, bike-sharing, motorcycle sharing, agency driving, car services, freight, finance and automatic driving services. DiDi currently has 15,914 full-time employees globally, including 7,110 researchers (accounting for 44.7%), indicating the company's emphasis on technology-intensive operations. Qing Liu, the daughter of Chuanzhi Liu, former chairman of Lenovo, joined DiDi in 2014 and was promoted to the president a year later. Previously, Qing Liu served as managing director of Goldman Sachs Asia. According to the company's prospectus, she and Wei Cheng, the founder and CEO, have become two DiDi controllers, holding over 48% voting rights.

Since its establishment, DiDi has received 22 rounds of financing, with a total amount of more than USD 20 billion. These funds came from the finest investment institutions such as SoftBank, Sequoia Capital and well-known companies such as Apple, Toyota, Tencent and Alibaba Group. According to its prospectus, prior to the IPO, Softbank (Vision Fund), Uber and Tencent became DiDi's largest shareholders, with about 41% shares. The company has also attracted investment from several state-owned institutions, such as Ping An and Bank of Communications.

Possible reasons behind DiDi's accelerated listing

We found at least two reasons why DiDi chose to be listed so quickly. First, DiDi has attracted a bunch of investors since the company was founded. But for many years it did not make a profit, remaining a money-burning startup. In other words, the IPO of DiDi was intended to keep the lights on. Second, we believe that the blocked IPO of Ant Group also had a negative impact. Completing the preparation of all the documents and going public within one month may have been to avoid the supervision of the Chinese government. The latter argues that DiDi may have some operation data that does not conform to the laws of either China or the United States.

According to some industry insiders, DiDi earlier planned an IPO – in 2015. This is mainly due to the rapid rise of the Chinese stock market in 2015, with the Shanghai Composite Index soaring by 60% and the Shenzhen Component Index soaring by 122% that year. However, the stock market disaster in the following year postponed its listing.

In 2021, with the demise of COVID-19, the US economy is expected to become overheated, and Fed rates are expected to rise in 2022, which may have a negative impact on the stock market. 2021 might be the last chance for DiDi to go public in the recent economic cycle. If DiDi is not listed yet this time, the initial investors' payback periods may be further prolonged, with some even choosing to divest.

Financials

According to the IPO prospectus, DiDi's total revenue in 2020 reached CNY 141.7 billion (USD 20.5 billion), slightly lower than that in 2019. From 2018 to 2020, DiDi's annual net losses were CNY 15 billion, CNY 9.7 billion and CNY 10.6 billion, respectively. Among the revenue segments, China's travel business accounts for more than 94% of DiDi's total revenue in recent years, of which online car-hailing income contributes more than 97%. This indicates a skewed revenue mix.

DiDi attracted services to over 493 million annual active users and powered 41 million average daily transactions by the end of Q1 2021. According to the company's estimate, there are 15 million active drivers in the world every year. In the 12 months ending March 31, 2021, DiDi's global average daily trading volume reached 41 million. The total trading volume of the whole platform was CNY 341 billion, ten times ahead of the nearest rival in China. DiDi has formed a monopoly market in the country's ride-hailing sector. And it seems abnormal for an absolute industry leader to have continuous large losses.

It is worth noting that DiDi broke even and made a net profit of CNY 5.5 billion in the first quarter of 2021. Nevertheless, about CNY 12.4 billion was a floating investment profit, and the company still suffered an operational loss of CNY 5.5 billion. Before March 31, 2021, the last day of the reporting period, DiDi deconsolidated the community group-buying business, Chengxin (which was only put into operation for one year) from the Group. The split removed the loss of Chengxin from the statements and converted it into a floating profit of 9.1 billion investment revenue, which looks like window dressing. This, we think, also showed an aim of going for a quick listing and a high valuation.

High political and operational risks

On July 2, 2021, three days after DiDi's IPO, the Chinese government conducted a network security review of the company on suspicion of collecting user information in serious violation of laws and regulations. Shortly, new user registration of the DiDi app was banned, and then 25 apps related to the company were required to be removed from the App Store and Google Store.

According to EqualOcean's research, DiDi launched a drive recorder in 2017. This device provides high-precision surveying and mapping data of China's urban and rural areas, and it is mandatory for all contracted drivers to install the recorder – otherwise, they won't be qualified to leverage the firm's platform.

On March 31, 2021, the SEC issued the Holding Foreign Companies Accountable Act (HFCAA), which stipulates that the Public Company Accounting Oversight Board (PCAOB) is responsible for supervising the audit institutions of listed foreign companies. For example, the inspection team should have access to all working papers. However, DiDi's papers contain much important information, such as the mentioned high-precision surveying and mapping data. Considering DiDi's monopoly position and huge user base, once the US government obtains these data, China's national security is bound to face a great crisis. The company was investigated because it was suspected of unauthorized transmission of important data secrets to the United States. Although the investigation is not over, DiDi's bizarre listing and the extremely harsh wording of the Chinese government have magnified the political risk enormously.

Another risk comes from its revenue model. The single revenue model determines that the company can only rely on increasing the commission rate taken from drivers. As a result, the drivers are often the object of complaints and dissatisfied feedback, which has also led to the intervention of the regulatory authorities many times. According to Xinhua.cn, the de facto commission rate has risen to 25% or even higher, far higher than the 21% promised by DiDi. Meanwhile, the detailed calculation of the commissions is unavailable for drivers. Even if DiDi continues to increase the commission rate, the company still does not achieve consolidated profit growth, indicating problems in the operation of the company and its business model.

Bottom line

To sum up, considering the political risks and potential operational problems, we do not think DiDi stock is a good short-term investment target. Besides, there is a looming risk of delisting. (Wall Street Journal reported on July 29, 2021 that DiDi is considering going private and compensating investors, but DiDi commented later on that the information was untrue).

DiDi is likely to continue to rely heavily on China's mainland market to generate profits.

The company will remain in the government agencies' scope for a while.

The board and principal shareholders of the company are likely to change.

We anticipate that DiDi will pay more attention to the development of foreign markets, expecting the proportion of overseas business income to increase in the short term.

We also believe the company will market its international products separately from the domestic ones, as ByteDance is trying to do.

China Tower Achieves CNY 42.67 Bn in Revenue in H1 2021Benefiting from the pulling effect of 5G construction, China Tower revenue and profit have gradually increased in recent reporting periods.

On August 9, 2021, China Tower released the H1 interim performance of 2021. According to the financial report, the company achieved operating revenue of CNY 42.67 billion in the first half of the year, up 7.2% year-on-year. The net profit of the company reached CNY 3.46 billion, a year-on-year increase of 16.1%. At the same time, more surprising is that the company's capital expenditure has been reduced to CNY 10.36 billion, down 27.6% compared with the same period last year.

Revenue from 5G is the driving force to its remarkable performance. Jilu Tong, the CEO of China Tower, said at the 2021 interim performance meeting that 5G contributed 64.1% to the company's revenue. In the first half of this year, about 256,000 5G construction projects were completed in China, of which 97% were conducted using existing towers, leading the whole work.

China Tower has also drawn wide attention, with China Telecom and China Mobile returning to the A-share market one after another. For this rumor, the company responded that the company has no plan to return to the A-share market at this meeting.

For full articles with the charts, please visit the original link.

China ETF GXC - the music ain't overRecently, the China market had dived on regulatory action over the past couple of weeks. It hit a low point way out of range, and then bounced back technically. And the past week saw a range bound attempt to break out. This attempt failed to extend the rally higher out of the range, but instead fell down to the range support. In the process, it left a gap support and held above this in a range.

The weekly chart has a rather unique candlestick pattern, where a long tailed hammer body is engulfed by a down candle. This is ominously bearish.

The Daily chart is no better, with a failed breakout, and a gamp down to follow through, ending the week at support with ailing technicals.

A revisit to the last low is due...

More downside incoming!

Farmmi Set to Capitalize on New Wellness TrendsStriving to vertically integrate its business, the company has been preparing for a major boost.

● Farmmi has a long record of unstable financial performance.

● The company's solid supply chain system and business model can integrate online and offline platforms and trigger potential future growth.

● Along with the public's increasing health awareness, Farmmi can seize more opportunities to build extensive global networks and explore new products, like fungi-based snacks.

● The share price of the company is currently hovering at low levels, which might provide investment opportunities in the middle term.

Farmmi (FAMI:NASDAQ) is a Chinese agriculture products provider that mainly processes and sells, as of July 2021, four different kinds of products: Shiitake mushrooms, wood ear (or Mu Er) mushrooms, other edible fungi and other packaged dried fungi. The company runs both an e-commerce platform and offline stores. Founded in 2003 and headquartered in a small city in east China, Farmmi is experienced in forming alliances with local family farms that allow the company to offer products to restaurants, cafeterias, local specialty stores, as well as through distributors.

Here, we analyze this small share opportunity and discuss the company's potential.

Quality – volatile profitability and cash flow generation

Farmmi's financials have lately been somewhat unstable. The revenue has been growing slowly – and even declined in 2020; operating income peaked in 2018 and has kept declining since. Farmmi's net income has also shown high volatility. Since 2015, the company has been reporting unstable and negative operating cash flows. Basically, it delivered unfavorable financials all the way after its IPO in February 2018.

What is more, the company's capital expenditure kept growing, but the limited value has been generated, resulting in a downward-moving return on capital.

Growth – optimistic trends and industry dividends

Despite Farmmi underperforming in the past years, investors should not be overly concerned about the lasting effects on the company's future development. We believe the company has a more positive side on financial growth and cash flow stability that will reflect in its future growth.

As mushrooms and fungi are categorized as 'wellness food,' Farmmi focuses on such products, exploring overseas markets. Now, 94% of the company's revenue is generated domestically, while 6% comes from international markets, including the United States, Japan, Canada and the Middle East. An insider has informed EqualOcean that Farmmi's top executives have recently been actively building networks and seeking major brand cooperation to further expand in the North American market this year. By May 2021, Farmmi had raised USD 7.4 million of post-IPO financing to fund its business expansion.

What is more, with the decreasing price of raw materials and improving cost control capabilities, Farmmi is expected to report better operating margins. So far, the figures have never fallen below the peer average level.

Unlike many traditional agriculture producers in the space, Farmmi has been utilizing trendy tools, like web-based products, to ensure its future competitiveness. The recently raised funds are leveraged by the company to enhance its e-commerce capabilities, IT and supply chain systems. These capital expenditures and the integration of online and offline business models may generate more income for the company.

The entire industry will release more dividends for Farmmi as well. The Chinese fungi market has been constantly growing since the noughties, providing growth momentum for Farmmi. The health and wellness trend has also expanded the market capacity for mushroom and fungi-based snacks, which Farmmi is building its future strategy around.

For most food companies, it is almost impossible to survive for over ten years without a solid supply chain system, technology support and cost and risk management abilities. Paying close attention to these aspects, Farmmi is poised to ride the global wellness trend with the increasing fungi consumption.

Price Momentum – upward

The stock of Farmmi seems to be currently undervalued. Without any warning signs in its financial performance, the share price has been going down since it went public in 2018, reached the lowest level ever.

As a small Chinese food brand, Farmmi might have less recognition among global investors, and we expect this situation to continue in the near future. However, the big picture appears brighter, as the company its making progress in cost control, harnessing technology and has a lot of room for development – both geographically and scope-wise.

For the full article with the charts, please visit the original link.

EVK "Fibbin" again?EVK hasn't been a stranger to big moves quickly. Nor has it been a stranger to the 382 Fib level either. Now the second time it's tested this area, EVK continues to fail to break and hold above it (as of right now). While there's still a clear uptrend with higher lows, there's a pretty important level that may be of interest right now which is the 50 fib line. It's in "no man's" land after today's spike and looking for some solid support is going to be important for longs. If it does settle around this level, it would be the first time it's established support above the 618 fib line in quite some time. We'll have to see how much follow-through, if any, is in play heading into August.

"The main reason for this move comes as the China-based clothing supplier and retailer announced that it would be repurchasing roughly $5 million worth of its shares. 'We believe our stock is a good value, and the Board’s approval of this stock repurchase program is recognition of the long-term prospects in our Company’s intrinsic value and the undervalued price of our stock. Repurchasing stock underscores our commitment to enhancing shareholder value and demonstrates confidence in our business.' - The CEO of EVK, Mr. Yihua Kang. For some added context, Ever-Glory International is the first Chinese apparel company to be listed on a U.S. stock exchange. It offers several brands that cater to middle-high end customer markets. As a vertical company in this market, Ever-Glory is able to control all aspects of its day-to-day operations."

Quote Source: 4 Hot Penny Stocks to Watch as August Turns Bullish

Xpeng Delivered Record 8,040 Vehicles in JulyThe company plans to have the P5 officially available in the third quarter of 2021, with deliveries expected in the fourth quarter of 2021.

XPeng Motors delivered 8,040 vehicles in July, its highest monthly delivery record, up 228 percent year-over-year and up 22 percent from June.

The company's flagship sedan, the P7, delivered 6,054 units in July, the highest monthly delivery record since its launch, XPeng's data released Monday showed. Cumulative deliveries of P7 reached 40,612 units since its launch in July 2020.

XPeng's compact SUV, the G3, delivered 1,986 units in July.

As of July 31, the company's total deliveries for the year reached 38,778 units, up 388 percent year-over-year.

XPeng previously said the P7 sedan with lithium iron phosphate (LFP) batteries has seen strong demand since its launch in March this year. Deliveries of the model began in May, with sales increasing 27 percent in that month compared to April.

In March, XPeng announced the launch of the P7 and G3 with LFP batteries, with deliveries of the former starting in May and the latter in April.

The new P7 is available in two variants a combined range of 480km.

The new P7 is equipped with Xmart OS in-vehicle intelligence system, with the lower-priced version equipped with XPILOT 2.5 + automatic driving assistance system, priced from CNY 229,900 (USD 35,600).

The higher-priced version is equipped with XPILOT 3.0 automatic driving assistance system, priced from CNY 239,900.

Together with the newly released model with LFP battery, the XPeng P7 is now available in four models: rear-wheel drive standard range, rear-wheel drive long-range, rear-wheel drive extra long range and four-wheel-drive high performance. Their price range covers CNY 229,900 to CNY 339,900.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

2022 Might Be a Winning Year for Xpeng – and the Stock Is FinallOn July 7, 2021, the company was listed on the main board of the Hong Kong Stock Exchange under the code '9868.'

We estimate Xpeng's 2022 revenue to show the value of the stock.

The methodology includes the forecast of sales of P7, G3&G3i and the upcoming P5 and SUV models.

The results indicate that the stock is currently fairly priced

Risks primarily come from supply chain and market regulation but remain controllable.

With the current global chip shortage, most major auto OEMs have suffered from a lack of electronic supplies. Amid these concerns, China's EV sales are burgeoning, with light EV sales hitting 241,000, or 15% of total light vehicles sales in June, 2021. Among the country's EV pioneers, Xpeng (XPEV:NYSE) has recently presented some positive results: its half-year delivery number has surpassed last year's figure. This article presents a forecast of the company's EV sales in 2022 and evaluates its stock by analyzing each model of Xpeng and using the valuation multiples.

Model-level breakdown

P7 is Xpeng's hit product. Simplifying the modelling, we project the sales of P7 to increase by 184, 100 and 50 units month-on-month until 2023; 184 is the average monthly increase since the model's launch, while the incremental decrease is due to the upcoming P5 and 2022 SUV models. The average selling price will be around CNY 250,000, the same as in 2020.

G3&G3i are the oldest models of Xpeng. The updated version G3i transformed into a more unified family design and attracted more sales. We estimate G3 and G3i will keep lifting sales volume by 46 per month during the same period. The average selling price will be around CNY 150,000 per unit.

P5 will shoulder the company's expectations to become a family sedan. We estimate P5's first-month delivery number in October will be at around 1,000, referring to P7's data. Then the delivery figure will increase by 143 units per month, of which 100 will be at the cost of P7 sales declining, as the two models compete with each other, and 43 is organic growth. Based on the official price starting from CNY 160,00 to 230,000, we predict the ASP will be at CNY 190,000.

Xpeng is planning to launch a new SUV model. The SUV has a family design 'X' logo that brings its length to 4,800 mm. The car design shares the same platform as the P7, the Edward platform. In addition, it will be equipped with premium specifications like XPilot 4.0 and air suspension. Some industry experts predict the price will be around CNY 300,000. We assume Xpeng will finish its launch day by September 2022. The first-month sale will be 300 units, which will increase by 145 units per month similar to the sales trajectory of NIO's ES6.

Apart from EV sales, other services will account for 5% of total revenue. The 2022 EV sales won't be significantly impacted by the chip shortage.

To sum up, Xpeng's 2022 revenue is projected to reach USD 4.3 billion (CNY 28 billion). Specifically, the company will sell 122,253 vehicles to make USD 4.1 billion topline, and USD 0.25 billion will be from other services. According to the Street's expectations, the stock is priced at 16, 8.8, 5.6, 4, 2.9 forward PS ratios by 2025. We select 9x as the 2022 multiples. Thus, the market cap will be USD 38.7 billion, around 10% up from the market cap on July 27, 2021.

Risks

Although the expectations for Xpeng are rather bright, the whole industry is facing the chip shortage problem – that is also the biggest threat to Xpeng. For NEV companies, production is challenging while orders are packed. Through our research, we found that most auto stakeholders in China expect the imbalance to last through 2021, affecting the global light-vehicle sales by 2.5-5.0%, but recover slightly in 2022.

The edtech sector's regulatory update drove the recent sell-off in Chinese concept stocks. However, this crackdown won't be a long-term issue for EV innovators like Xpeng. According to Bloomberg, the government's motivation is to cut family workloads to turn the declining birth rates up. On the other hand, the 'Made in China 2025' scheme supports EV development radically. So the policy will rather play a positive role in the new energy vehicle market in the long term.

Conclusion

Up to the present, Xpeng has been on the right track, leveraging business through unified family designs, new stores opening, capacity boost and charging facilities build-up. The company's 2022 revenue would be a realistic basis for stocks to start. The most significant potential risk at present is the capacity problem caused by supply chain shortages. Investors should keep an eye on this topic in the company's upcoming Q2 earnings conference.

For the full article with the charts, please visit the original link.

DIDI Global ideaAt the time of DIDI`s IPO i was tempted to enter this stock because i was listing to Jim Cramer`s blessing: 'I would try to get as many shares as you can'. i hope he didn`t. and i haven`t entered either because i considered the valuation too high for a company that last year had negative earnings, -10.84Bil.

And in comparison i was listing to analysts saying that UBER will never be a profitable company. So why would i invest in the Chinese copy of a business that didn't find the path to profitability for so many years?!

The funny thing is that after going down 55% from the IPO day, Jim Cramer reevaluated the Chinese stocks: "You can't own Chinese stocks"! :)

I`m looking forward to read your opinion on Chinese stocks right now.

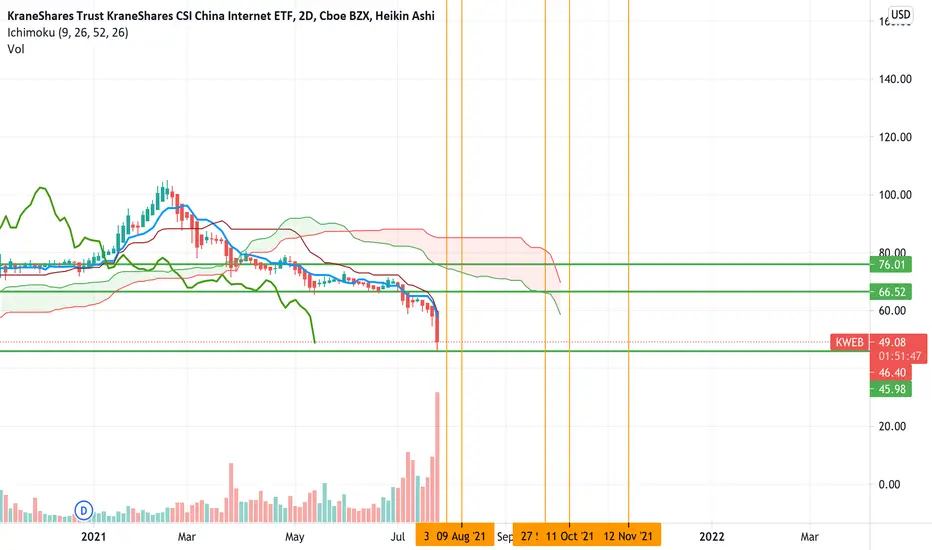

$KWEB due for a bounce here at $46?Extreme bearish sentiment at $46 support? Looks due for a bounce to me. First upside target $66 and then $76. Unlikely to make it much higher than $76.

Watch for reactions to price action on key dates and levels on the chart.