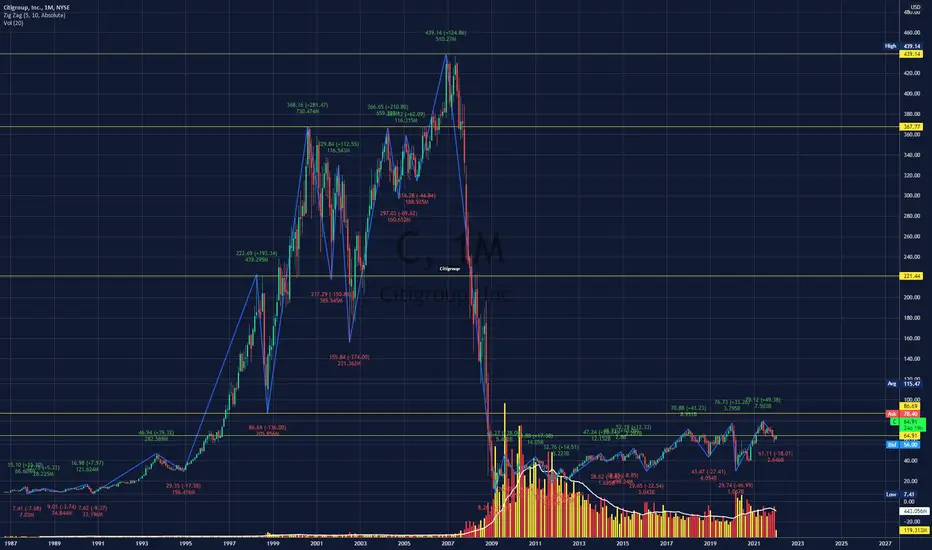

C - Movement Along Major Trend LineC dropped very sharply but recovered and has been moving consistently along this major trend line that formed in the beginning of price action

Circles in green are very similar points and should be treated the same

Safe buy along the strong trend line

Citigroup

Real economy beating expectations yet markets trading in red 🤔INVESTMENT CONTEXT

President Vladimir Putin said that Russia was not blocking Ukrainian wheat from being exported, and that the grain could be dispatched via ports controlled either by Russia or Ukraine. Before the war, Russia and Ukraine accounted for ca. 29% of international annual wheat sales

U.S. economy added 390,000 jobs in May, beating analyst expectations (325,000) and showing resilient real economy in the face of rampant inflation and higher interest rates

Crude oil inventories in the U.S. fell to 414.7 million barrels in the wake of strong demand, yet limiting chances of further releases to cool domestic energy prices

Goldman Sachs COO John Waldron followed JPMorgan's CEO Jamie Dimon saying “This is among if not the most complex, dynamic environment I’ve ever seen in my career". On a similar tone, in a leaked Tesla email, Elon Musk cited having a "super bad feeling" about the economy as the main reason for shedding 10% of the company's workforce

PROFZERO'S TAKE

When good news are met with S&P 500 dropping more than 1.50%, and Nasdaq doing even worse at 2.47% in the red, we know something is off. That's what happens when bears are in control, and policy makers are desperate to understand how far can they move with tightening before the backlash. A remarkably strong U.S. economy just added 390,000 jobs in May, beating analyst expectations and reassuring the Fed it could maintain the trajectory of 50bps rate hikes in July and August. ProfZero clearly welcomes Main Street's resilience and rising wages - yet, as anticipated in Step99 podcast, it cautions against the forward-looking effects of monetary policy vs. the actual state of the economy. As pointed out by The Economist, "A recession in America by 2024 looks likely" - today's strength of the real economy may at best soften its blow

Citigroup CEO Jane Fraser sees "three R" whiplashing EU economy - rates, Russia and recession, this latter happening in Europe ahead of the U.S. because of "the energy side (...) really having an impact". ProfZero has made energy a key theme of this Parlay, with potentially more decisive effects on the real economy than monetary policy. With Brent testing again USD 120/boe and fading cushion inventories from the U.S., it is hard to imagine how the EU will cope with the next cold season without rationing output, hence slashing GDP growth. Regasification plants and last-generation nuclear are definitely tools of the future; but by then, are seaborne imports going to be enough?

Equities are definitely off the lows witnessed in April and early May - perhaps Musk's "super bad feeling" and Mr. Dimon's "hurricane" are rather looming on the real economy? Not an inch less worrying...

BTC once again confidently breaking up the mid-term triangle pattern and trying to regain 32k after trading below 30k on June 4-5 - and yet ProfZero's eyes are set on the lurking death cross on 200MA

PROFONE'S TAKE

After sharing about lithium and nickel, ProfOne completes the overview of rare minerals that are crucial for the production of batteries setting its eyes are on cobalt. Cobalt prices soared from USD 30k/ton in January to USD 52k in May - on top of the 2x surge in 2021 vs. 2020. According to the Cobalt Institute, in the next five years cobalt demand is expected to hit 320k/ton, up from 175k/ton in 2021. ProfOne argues that meeting such demand won’t be operatively easy. For once, cobalt is yet another highly concentrated resource: about 70% of world’s cobalt comes from the Democratic Republic of Congo, where production is dominated by Chinese companies and commodities trader Glencore (GLEN). Adding to it that world's second supplier of cobalt is Russia, the metals puzzle turns out to be a fairly intricate one

Banks to crash in larger financial crisis than 08/09I am expecting economical-sensitive investments like banks to crash to far lower levels than they reached in march 2020 due to even worse economic circumstances ( Contraction + Inflation entrenched)

Citigroup - nice catch a wave hi,

looking on ticker c Citigroup, I see positive move up, I don't know if it is a long wave up or a short term but, I hope that we will go to 56 USD or 60 USD.

There are rates from FED to be raised and as we know banks will increase their income with the rising of them.

Also the stock is undervalued, and we see that there is long term of accumulation of it and moving in the same range.

Please be advised that this type of stock is one of the "biggest" one in the NYSE. In long therm I hope to gain some money on it.

Like always we can see "play" of algorithms and computers - it likes to play with SME - moving average in range M15 and H1.

I hope that it will help.

Look on it in long term.

it is not a investing advise, it is only my opinion, please do not consider it in the light of law for any advise how to invest your money, it is your risk and your luck.

Citigroup, Inc. Bank Stocks to BuyMACD shows a bullish confirmation.

Traders can buy stocks when the price breaks above the downward sloping resistance line.

Target price is defined by Fibonacci retracement 50% level.

Position: LONG

$XLF tons of overhead supply ; will the gaps fill?Financials on full display going into earnings . Will those GAPS fill? Keep them on your radar.

#XLF #JPM #C #BAC

Interest Rates continue to rise on 30 year home mortgages and the federal interest rates consumers begin feeling the pain of being both pushed out of the market and every direction they turn.

In most cases higher interest rates help the banks and some could say, “higher rates drive up prices, which increase companies earnings and consumer price index ( CPI );” however, I think many are overlapping the current with past recessions. In most cases that may work – but this time isn’t like any time of our past. The amount of headwinds on the global fronts and out of control printing of debt holistically.

In any case, I am cautious on banks with all the segments of their lives being impacted with oil , shipping, economic contraction, rising rates, etc. not to mention rising wages being outpaced by inflation and poverty increase by x-hundreds of thousands per month.

Tons of overhead supply that could be potential opportunities for entries on rejection. WILL THE GAPS FILL?

** What happens when households cannot afford to acquire loans and it’s too late for them to refinance their homes… just food for thought.

CITIGROUP: earnings coming soonNext week will be published the US most important banks earnings and among them, Citigroup is for sure the one with the best focus. In particular, the US bank is the one with higher exposition in Russia: almost 10 billion dollars.

So, what can be the next scenario?

I'm short on CITI due to both fundamental reason and technical reason:

We are in a short trend, so basically, being trend follower, I will search for retracement to be in.

CCI oscillator gives long signal plus bullish divergency on the price. This can give the necessary boost to the stock to retrace up to 56-58 dollars before getting back to its lowest price.

Citigroup going to town. CShort term only. NFA

Goals 66, 69. Invalidation at 57.

We are not in the business of getting every prediction right, no one ever does and that is not the aim of the game. The Fibonacci targets are highlighted in green with invalidation in red. Fibonacci goals, it is prudent to suggest, are nothing more than mere fractally evident and therefore statistically likely levels that the market will go to. Having said that, the market will always do what it wants and always has a mind of its own. Therefore, none of this is financial advice, so do your own research and rely only on your own analysis. Trading is a true one man sport. Good luck out there and stay safe

C Citigroup Long IdeaCitigroup recently broke through swing high AVWAP implying a nice chance for more upside.

I'm in May 70/75 Debit Spreads here to play any run up to ER as well.

Looking for a move similar to AUG price action .

Rejection at AVWAP invalidates the trade . Emergency FED meeting and rate headwinds, along with Russia and Covid - keeping positions small and respect stop losses !

More correction in banks..!It seems Banks will correct in the coming days..!

Considering their weight it will affect the S&P 500 and Dow!

You can see the most important support(green line) and resistance (red line) levels.

Best,

Moshkelgosha

DISCLAIMER

I’m not a certified financial planner/advisor, a certified financial analyst, an economist, a CPA, an accountant, or a lawyer. I’m not a finance professional through formal education. The contents on this site are for informational purposes only and do not constitute financial, accounting, or legal advice. I can’t promise that the information shared on my posts is appropriate for you or anyone else. By using this site, you agree to hold me harmless from any ramifications, financial or otherwise, that occur to you as a result of acting on information found on this site.

Short Citigroup regarding channel!Short the C regarding descending channel and ichi leading span B.

Take profit at around next level.

Enter the market between 66.00 to 67.81

Citigroup Is Seen to Have an 18% Upside PotentialJPMorgan, Citigroup and Wells Fargo are going to publish their quarterly earnings reports on Friday.JPMorgan’s Earnings per share (EPS) is expected to be at $3.03 and its revenue is forecasted to be $29.89 billion.

Wells Fargo is expected to report EPS at $1.12 and revenue at $18.9 billion, while Citigroup is seen to report EPS at $1.38, and revenue at $16.75 billion.According to Refinitive polls the strongest upside potential is expected to be seen from the Citigroup stocks at $80.47 per share, or with an uprise of 18.72% of the current prices.

Let’s look closer at the technical incentives of this possible spike. Firstly, stocks are moving within the upward trend that started in March 2020, and the last time this trend line has reached was at the end of 2021. The recent upside wave started on December 20, 2021.

However, the upside potential at the moment is limited by the resistance line of the junior downside trend from February 2021. This junior trend was approached by the price from the downside for the fourth time. This increases the chances of a possible breakthrough. Once successful, if the price surpasses the $68.70-69.00 area, it would lead the price to the previous highs at $80-83 per share. The last time Citigroup stock prices were located at $80.29 and at $80.70 was in June 2021 and January 2018 respectively. The all-time high for the stock prices was established at $83.11 in January 2020.

So, technically there are no reasons to stop the climb after stock prices would break above $69.00 per share. However, even the ongoing attempt of a breakthrough would be less successful this time so Citigroup stocks should not be left behind, as they may perform a short downside correction to $64.50-65.00 to the crossing of the EMA21 and EMA55 moving averages on the daily chart. From this zone buy operations could be resumed as the next attempt of an upside breakthrough could finally succeed.

Citigroup Target Price 73.72Price closed above the October 2021 Trend Line. Expect price to increase. If price continues to stay above 63.50, then Citigroup is bullish.

1H Time Frame

2H Time Frame

3H Time Frame

4H Time Frame

Daily Time Frame

Citigroup - BULLISH - BUYAn easy one here Citigroup profits in the market environments = stock goes up simple.

NYSE:C

BMV:C

BCBA:C

NYSE:C/PK

MOEX:C-RM

GLOBALPRIME:C.NYSE

XETR:TRVC

NYSE:C/PN

BMFBOVESPA:CTGP34

NYSE:C/PJ

SWB:TRVC

BCBA:C.D

SIX:C

SIX:C.USD

LSIN:0R01

BVL:C

BCS:C

EUREX:CITG1!

EUREX:CITG2!

EUREX:CITGF2022

EUREX:CITGG2022

BVC:C

BER:TRVC

MUN:TRVC

EURONEXT:2CIT

HKEX:11287

Citigroup | Fundamental AnalysisCitigroup CFO Mark Mason lately visited the GS financial services conference and noted that the bank would suspend its share buybacks in Q4. This hidden comment took many shareholders by surprise.

Part of the thesis of needing to own Citigroup now is that the bank can buy back a large number of shares as long as the stock is trading below book value (TBV), which is what the bank would be worth if it were liquidated. In case a bank buys back shares below TBV, the math works so that TBV goes up, and bank shares usually trade relative to TBV, so a rise in TBV is very good for the stock in the long run.

The ability to buy back shares below TBV is rare, so investors were excited that Citigroup would be able to grab this opportunity while eliminating all of the bank's other problems and planning a new growth path. Let's take a look at why the bank was forced to suddenly suspend share buybacks and what this implies for the stock going forward.

Banks are complex organizations, and they have numerous rules about how much capital they must hold in reserve for all their operations that could lead to losses (such as loans). In 2022, another intricate regulatory rule, called the standardized approach to assessing counterparty credit risk (SA-CCR), will come into force. Basically, the SA-CCR will require large banks like Citigroup to modify the way they calculate the risk associated with derivatives contracts.

As you know, derivatives, which are financial instruments such as mortgage-backed securities, played a role in the Great Depression. The overall result of the SA-CCR is that most large banks will see an expansion in risk-weighted assets (RWA). Banks hold regulatory capital based on accumulated RWA, so if their internal regulatory capital ratio is 10% or 11% and then the RWA grows, they must hold more regulatory capital to maintain that ratio. And the more regulatory capital a bank holds in reserve, the less money it has left to invest in the business or distribute capital, such as paying dividends or repurchasing shares.

Mason said the SA-CCR would result in a $60 billion to $65 billion increase in RWAs, which could require Citigroup to hold an additional 0.50-0.60 percent of its regulatory capital. That's not an inconsequential amount. Curiously, however, I haven't heard of any other major banks that have suspended share buybacks because of the SA-CCR despite the need to increase RWA.

This may have been the case with Citigroup because the bank has embarked on a strategy update with many moving parts. For example, the bank is exiting 13 global consumer banking franchises as part of a broader idea to wind down areas where it does not have enough scale to compete and is instead investing in the bank's higher-margin businesses. Citigroup announced in the fourth quarter that it was winding down its consumer banking franchise in South Korea, which could result in costs of up to $1.5 billion. Citigroup posted a $680 million pre-tax loss in the third quarter due to the sale of its Australian consumer banking operations.

Mason said the fourth quarter will be something of an "anomaly" when it comes to the bank's capital return philosophy and share buybacks, especially mentioning SA-CCR and expenses for Korea. Since SA-CCR requires an increase in RWA, and Korea expenses affected earnings this quarter, the bank may have run out of room over its target regulatory capital ratio to be able to conduct the stock buyback it originally planned.

The suspended stock buyback is disappointing because it appears that management either didn't plan the capital buyback very well or didn't effectively communicate that information to shareholders. Mason said the bank will resume share buybacks next quarter at the level of the third quarter, which also fell a bit short of investors' expectations in terms of Citigroup's buyback volume.

With Citigroup trading at such a low stock price and now well below TBV, the bank should buy back as much stock as possible. With the poor track record that Citigroup has had over the previous years, it really can't afford to make such mistakes because shareholders are sick of it.

However, analysts still believe in the renewal strategy and the Citigroup story. But that's mainly because a bank with the kind of U.S. deposit market share that Citigroup acquired and its successful investment banking unit shouldn't be trading so below book value.

Integrity is Important!Please review the analysis published on November 4th, 2021:

Title: Negative days ahead for banks!

You can see the most important support (green lines) and resistance (red lines) to watch in the coming days in these charts!

Best,

Moshkelgosha

DISCLAIMER

I’m not a certified financial planner/advisor, a certified financial analyst, an economist, a CPA, an accountant, or a lawyer. I’m not a finance professional through formal education. The contents on this site are for informational purposes only and do not constitute financial, accounting, or legal advice. I can’t promise that the information shared on my posts is appropriate for you or anyone else. By using this site, you agree to hold me harmless from any ramifications, financial or otherwise, that occur to you as a result of acting on information found on this site.

Negative days ahead for banks!It seems Banks have run out of steam and in the near future, they will make a correction or go sideways!

BAC: Fails to close above 48.50

WFC: Got rejected from resistance level and may retest 46 in the coming days

C: struggling at the support line

MS: pure consolidation between 96-106

JPM: 2-3% correction is expected!

GS: could retest 370 level once again!

You can see the most important support (green lines) and resistance (red lines) to watch in the coming days in these charts!

Best,

Moshkelgosha

DISCLAIMER

I’m not a certified financial planner/a certified financial analyst, an economist, a CPA, an accountant, or a lawyer. I’m not a finance professional through formal education. The contents on this site are for informational purposes only and do not constitute financial, accounting, or legal advice. I can’t promise that the information shared on my posts is appropriate for you or anyone else. By using this site, you agree to hold me harmless from any ramifications, financial or otherwise, that occur to you as a result of acting on information found on this site.

Citigroup $C is cheap and oversoldBanks are still very cheap, $C trades at 6 PE with a 3.14% dividend yield and technically speaking its stock price is now at the lower part of its trading range for most of this year. Both the Range Strength and Hurst Exponent indicate the price is in a non-trending ranging mode, the RSI is at 22 and price is 8.38% below it's 50 day MA which is a lot for a mega cap like Citi, here looks like a good long play back to the 50 day MA.

CitigroupThis action has shown weakness under resistance 68.5 producing a good sell signal that can continue until 64.7.

$C Citigroup

$ C

Citigroup looks interesting enough.

It can be long from the current ones with a stop below the 200 MA (68.7).

Breakdown level 0.886 (73.52)

Looking like wide angle with breakdown after black level 2

Financial Sector needs a pull backXLF is over-inflated (financial sector)

BlueWave will give a red dot sell signal soon.

Stochastic RSi is overbought.

Citigroup Stock OpportunitiesCitigroup rejected nicely from my prz zone. Expect a long term move to the downside.