$AMC cypher imaginationcypher harmonic pattern:

AB=0.61 XA

BC=1.41 AB

tp1=0.78 XA=$63

tp2=1.27 BC80$

tp3=1.6 BC=$223

tp4=2 BC=$689

shark reversal scenario:

3-4=0.61 Y-3=$36

4-5=1.6 3-4=$689

Consumer

Consumers are pulling back quickly as Uncertainty ReignsThe Indices will see a healthy correction into the Seasonal Period of Extreme Weakness.

We Anticipate a LARGE Selloff to begin during Globex Sunday followed by further selling

into Monday.

The PRICE of the things we need is an issue... it is not lost on Institutions.

They are heavily positioning for SELL.

AiHuiShou: Company with Strong Closed-Loop Chain CapacityThe second-hand 3C platform is among the most promising businesses in the space in China.

On June 18, 2021, Aihuishou was listed on NYSE under the ticker RERE by issuing 16.23 million American Depositary Shares (ADS). According to the company, 60% of the funds raised in the IPO will diversify services, and expand its AHS store network and sales. 20% will be used to improve technology capabilities further, and another 20% will be used for general operations. As the first ESG US-listed Chinese share offering, the IPO has attracted much attention.

Founded in 2011, Aihuishou is one of China's largest second-hand computer, communications and consumer electronics (3C) platforms and one of the pioneers in the industry. After ten years of development, it now has four major business segments, realizing a C2B + B2B + B2C closed-loop value chain: C2B recycling platform (Aihuishou), B2B trading platform (PJT Marketplace), B2C retail platform (Paipai Marketplace), as well as its overseas business (AHS Recycle). On the supply side, the JD.com and Aihuishou offline stores attract stable supply. At the processing end, it has set up seven regional operation centers and 23 city-level operation stations in China for proprietary inspection, grading and pricing. At the end of the sales, the PJT Marketplace can ensure the products flow at high speed (shortening the flow time by three times), while the B2C platform can make the products go directly to the C-end to improve the profit margin.

Aihuishou has completed six rounds of financing prior to its IPO. Many well-known institutional investors have great regard for the company, such as JD.com, 5Y Capital, IFC, Cathay Capital and Guotai Junan International. Before the IPO, JD Entities held 34.7%, being the largest institutional holder. 5Y Capital owns 14.0%, the largest VC investor, while Tiantu Investment and Tiger Global fund have 8.5% and 7.3%. Notably, in its IPO, two existing shareholders, JD and Tiger Global purchased USD 50 million Aihuishou ADSs respectively, showing an optimistic attitude towards its long-term development.

Financials

In 2020, Aihuishou achieved revenue of CNY 4.86 billion, up 23.6% year over year, and reported a shrinking net loss of CNY 470.6 million (CNY 202.8 million with non-GAAP adjustment). Then in the first quarter of 2021, its revenue surged by 118.8% to CNY 1.51 billion compared with the same period of 2020. It indicates a strong growth momentum of the company.

Further analysis of the company's revenue structure, net services revenue is a bright spot. The proportion of net services revenue rose from 0.4% in 2018 to 13.5% in the first quarter of 2021. In 2020, the company's net services revenue reached CNY 614 million, with a CAGR of 627.7% since 2018. Net services revenue comes from charging commission fees to merchants and customers for transacting in its online marketplaces, and the increase of the proportion indicates it gradually wins market recognition and continuously refines its revenue structure. As for the primary revenue source, the company's net product revenue reached CNY 4.24 billion in 2020, up 13.8% year-over-year, remaining robust.

High operating costs are serious problems for the company. In 2020, the company's costs reached CNY 5.35 billion. When deconstructing the costs, merchandising costs accounted for more than 70%, mainly consisting of the cost of acquired products coming through the AHS platform and inbound shipping charges for its product sales. Although we think that the rising costs reflect the company's expansion plan, the high cost may damage the company's profitability.

Opportunities and threats

The company's opportunities are obvious. First of all, Aihuishou joined a market with great potential. According to Aihuishou's prospectus, China's second-hand electronic products trading and service market has great potential. China's pre-owned consumer electronics transactions and services market size reaches CNY 252.2 billion GMV in 2020, and the market is expected to grow at a 30.8% CAGR to reach CNY 967.3 billion by 2025.

Secondly, the company occupies a high market share and maintains a high growth. Its total GMV reached 22.8 billion, and the number of consumer products transacted on its platform reached 26.1 million for the twelve months ending March 31, 2021, up 66.1% and 46.6%, respectively, year-over-year. In the second-hand 3C trading sector, in 2020, The company’s GMV for electronics and the number of devices transacted on its platform were both ranking the top and greater than the following five largest platforms combined.

At the same time, the profit model of the company's offline stores has been proved feasible. According to TMTPost, the early decoration cost of an Aihuishou offline store is estimated to be CNY 70,000 to 100,000, and the rent and salary expenses are about 30,000 CNY per month. Considering the average monthly sales revenue is about 600,000 CNY, and the gross profit rate is about 20%, the payback period of investing in such a store is less than three months. More than 98% of its stores have made profits, indicating that the company has a great chance to turn losses into profits in the future.

However, there are two obvious threats or risks. First, the company does not have an advantage in the whole second-hand e-commerce market, though it is a leader in the second-hand 3C sector. According to Big Data Research, in March 2021, Xianyu (Idle Fish) and Zhuanzhuan occupied about 90% of the second-hand e-commerce market, with a total MAU of over 70 million. In contrast, the MAUs of Aihuishou only take less than 2% of the whole market, through two platforms with only 1 million MAU. Although its main competitors may focus on other kinds of second-hand products, high traffic on these platforms means they can encroach on Aihuishou’s shares easily.

Another risk is that, before the IPO, the two founders sold their holdings at a discount, indicating a lack of confidence. According to the prospectus, founder and CEO Xuefeng Chen reduced 1,995,981 shares, and co-founder Wenjun Sun sold 600,645 shares in February 2021 in a series F with a price lower than the preferred shares. It may not be a good sign that the founders are selling their holdings at a discount when the company's operating cash flow is insufficient.

Valuation and bottom line

Considering that the company has yet to turn a profit and no Chinese ESG company can be used as comparable companies, we used EV/revenue ratios to analyze its valuation and picked five related companies: BQ, MKD MPNG.Y, PDD, and SECO. The average EV/revenue of the competition is 5.42x, while RERE's EV/revenue is 5.43x. Based on the valuation and the analysis of its opportunities and threats, we gave it a neutral rating.

Further analyzing the strategies that it should adopt, we think the company may need to focus on the following two ways to maintain its industry advantage. First, helping to establish industry standards is a way out. Second-hand recycling is a specific non-standard industry. The second-hand pieces of 3C equipment sold online and offline are numerous brands and of uneven quality. The establishment of a relatively transparent price evaluation mechanism can stabilize its market share. Secondly, it is necessary to control C-end costs. In the second-hand e-commerce market, both users and sellers naturally gather on the top platforms. A higher user utilization rate will also reduce the marginal cost of each offline store, which we think is the key to turning losses into profits. Considering this IPO aims to develop new sales channels for the B2C platform and further improve the penetration rate of C-end purchases, we think it is a good omen and is worth further attention.

For the full article with the charts, please visit the original link.

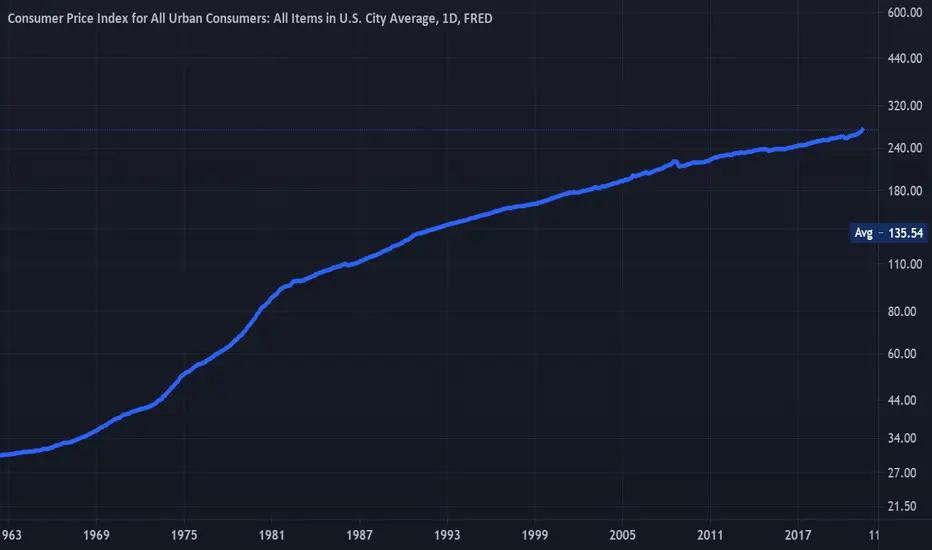

The higher U.S. consumer price may support the dollar in a shortThe higher U.S. consumer price may support the dollar in a short term period.

Inflation climbs for third straight month: U.S. consumer prices rose 5.4% in June from a year ago, again higher than expected.

The dollar became stronger after today's key report for U.S. inflation. The Dollar gained about 55 pips after the release of the news.

This year World-Signals.com expects to see the highest inflation in the last decade. As the dollar gains today by this news in a mid and long-term period the dollar may lose against the major currencies.

But the higher inflation is a signal that Fed policy to hike U.S. interest rates is close. The Fed last month announced that it will make two interest rate hikes with the minimum 0.25% but this high inflation may push the Fed to make higher than expected rates hike.

At the same time the inflation in the biggest European economy is 2.3% the same as expected and the same as in prior month of year base.

The Germany Consumer Price Index was released earlier today of 2.3% of year base and 0.4% for June the same as expected and prior month too.

For tomorrow (Wednesday July 14th) the most important event is Fed's Chair Powell testifying schedule or 16:00 GMT.

The news for U.S. Consumer prices may strengthen the Dollar in a short term period. Our prediction is to see EURUSD at levels of 1.1600.

$PINS overview*Before reading the information in this please understand the risks associated with both the stock market and investing as a whole. ALWAYS do your own research; invest with conviction, rather than emotion.*

*Please understand I am in no way a professional and offering investment advice, all ideas shared are simply opinion.*

*I work with a team of individuals that does research into potentially undervalued publicly traded companies. We use a mix of fundamental and trend analysis to formulate a trading plan for our securities.*

I've had a true love for Pinterest ($PINS) since the beginning of the year, they are one of my favorite public companies out. I myself am not an avid user of the platform, however I do know a great number of friends and family that are religious users of this social media platform. Pinterest is a community based message board that allows users to publicly share other ideas that they want to share to their followers; in pair, users can also post their own ideas for their follower base. Pinterest is great for people with in an interest in practically anything (within reason, of course). With a growing technology-driven world, an app like Pinterest will *likely* continue to see user growth, their average user growth was up 37% in 2020, which followed a 30% growth the following year.

I myself secured an entry at $66 per share, and as of this post $PINS is sitting at a share price of $76.99 at close Friday, July 10. I averaged up this past Thursday at the $75 price point, and am approaching my first take profit point. Short, mid, and long term simple moving averages have done a bowl pattern and have turned bullish, and momentum has followed. Although SMA has turned, momentum appears to be headed to be headed toward a resistance point. Though I love Pinterest and their operations, as well as their current price action, I am currently neutral on $PINS short term. Though both short and medium term bullish patterns have not been broken, but there are two potential bearish patterns forming, both formed at existing resistance at $90 per share. If $PINS can power through this momentum resistance, they have room to break through the current $90 price ceiling, and could touch a $100 share price by years end.

Price points are as follows:

ORIGINAL ENTRY: $66

AVERAGED UP/NEW ENTRY: $75

STOP LOSS: $66

TAKE PROFIT 1: $90

TAKE PROFIT 2: $110

There is 43% upside on this medium-term trade from its current entry point. Current stop loss is my original entry. I will be giving an update soon, Pinterest's activity on the charts in the next couple of weeks could tell the tale of what to expect for performance into 2022.

Be sure to follow me @bigshotrob for future updates and posts.

AtntI like Atnt even though their annuals financials are shaky. I love the acquisition of DISCA which will take effect next year. Atnt is at or near a strong support and I like the variety of things Atnt is involved with. I feel that they are making noise behind the curtain and is also claimed to be popularly known as a defensive stock. Stochastic is at support on the Daily and the 1 hour time frame matching the green of the Mac D. Previous was broken so I set a fibonacci tool to retrace up to 61% of the previous in case I want to take profit on some shares.

What do you think?

Is $AAPL headed to $150?*Before reading the information in this please understand the risks associated with both the stock market and investing as a whole. ALWAYS do your own research; invest with conviction, rather than emotion.*

*Please understand I am in no way a professional and offering investment advice, all ideas shared are simply opinion.*

*I work with a team of individuals that does research into potentially undervalued publicly traded companies. We use a mix of fundamental and trend analysis to formulate a trading plan for our securities.*

My team and I have always had a love affair with Apple ($AAPL) and their operations. It has recently been correcting on the charts from a $150 price point, and based on the the company's performance last week, we believe Apple has broken any bearish pattern that may have been apparent on the charts.

Apple is a notorious company with a brand equity that is currently unmatched in the electronics industry. Holding this company makes sense in any portfolio, this tech giant has showed time and time again it is the clear standard in consumer electronics sector. They have hold of a very large market by having a variety of products, these products all having some level of interconnectivity to one another. This interconnectivity has created a level of dependence for their consumers, meaning consumers do not want to buy non-Apple products simply because they already own many different Apple products. They are also able to sell older models of their devices at a discounted price, further increasing their market capitalization.

Regardless if you are chasing Apple to the $150 price point, securing yourself a good long entry for a long-term hold, or just riding Apple up on this bull run, buying at this price point certainly appears to be a good idea. Our price points are as follows:

ENTRY: $127

STOP LOSS: $120

TAKE PROFIT 1: $140

TAKE PROFIT 2: $145

TAKE PROFIT 3: $150

Check out my team over at @SimplyShowMeTheMoney

Members of our team are followed there.

$AMZN: Jeffery Bezos Fresh weekly setup here, could it be time for a breakout? Market is a bit saturated to the upside especially in tech but we'll see if $XRT has any more strength left to give

BUY at current levelretracement from recent spike is over.

has retraced a decent amount and green candles signal stock might go up from here.

small sl if we enter at current level.

Casino BoisLonging over 28, im am looking entry at 27.60.

Bullish pennant, hasnt recovered yet, seems to have good debt plan, would like divi to come back.

SL phasers set to 26.50 for me personally, will trail and scale in where appropriate.

J.

LULU in weekly oversold conditionsOther than the March 2020 crash, LULU only reached oversold weekly conditions in September of last year after which it rallied 25%. Will we see a similar bounce here? Will depend on strength in NASDAQ/QQQ.

Canadian dollar rises on strong Manufacturing PMIThe Canadian dollar has kicked off the trading week with strong gains. Currently, USD/CAD is trading at 1.2669, down 0.55% on the day.

US yields moved higher last week, particularly the 10-year treasuries, which rose as high as 1.6% per cent. This move boosted the US dollar against the major currencies, and USD/CAD climbed close to 1% last week. However, bond yields have since stabilised. Yields on the US 10-year treasuries are back around 1.40%. I expect bonds will continue to fluctuate and cause further volatility in the currency markets. The US dollar index fell below support at the 90-level late last week, but the greenback has flexed some muscle and the index is currently at 91.08.

The US economy continues to show signs of recovery, and expectations are high that first-quarter growth will be strong. A major driver behind economic growth is consumer spending, and the January Personal Spending release came in at 2.4%, its best read in seven months. Personal income levels were also up sharply, but inflation levels still remain muted. The Core PCE Price Index, which is believed to be the Fed's preferred inflation gauge, remained at 0.3%, a level not exceeded in over 10 years. There are concerns that the massive stimulus program of USD 1.9 trillion could cause higher inflation, and with it the danger of the US economy overheating.

After strong gains by USD/CAD late last week, we are seeing a reversal on Monday, with the pair losing ground. Resistance remains strong at 1.2787, as this line has held since the first week in February. Above, we find resistance at 1.2842. USD/CAD is putting pressure on support at 1.2632. If the pair breaks below this line, it could fall sharply, with no support until 1.2532. This is followed by a swing low at 1.2468, which the pair touched late last week.

.

China's Consumer Discretionary ETFFrom the beginning of 2020, emerging markets, and specially China, had been really outperforming.

The sector has taken a 12% correction from its high on February 16th. Which was coincidental with the past sell signals from the drawn channel.

We have tested the 50sma, which has worked as the lower channel trend line in this system.

Risk-reward-ratio is fantastic as we can a stop below the moving average; with a target around $42.

Top 5 Holdings:

Meituan (10.38%)

Alibaba (7.92%)

NIO (7.42%)

JD (6.98%)

PDD (5.94%)

Sugar as an Inflation ProxySugar is confidently surging for now into this thin zone toward 20. Consumer inflation will be felt when food prices are soon passed on, similarly with Oil and other commodities. Broad implications economically but when will the true inflationary pressures be communicated?

See my cursive inflationary pressure roadmap for the next 5 years attached. Peace

Ferrari is a good portfolio diversifier from hereWhen growth and inflation around the world are seemingly increasing on a MoM basis, consumer discretionary stocks perform well. We've seen this across the board so far this year, and in the latter parts of 2020. Ferrari is no exception, with a premium luxury brand with international recognition. Recently, RACE has been pulling back, and I'd look to start to leg into a position here, with capital to buy more slightly lower as well. Technically, we're near the bottom of the 2std dev Bollinger, as well as oversold on the RSI 1D/4H timelines. The risk/reward from here is favorable.

Tattooed Chef Inc - Outbreak ALERT - Bullish for 2021 - Hey fellow Traders,

first of all i wish everyone a succesful and happy new year, may your dreams come true!

Now lets get back to business, today i´d like to talk about NASDAQ:TTCF

As we already saw it was forming an strong resistance at the 24 ish level , but we could finally manage to break that with good volume coming through and positive newsflow.

What does this mean for future investors?

So it would be a very healthy and good sign to turn the previous resistance level into a new support line.

Also it signals us that the stock is ready to move higher to the next targets.

But letme give you some reasons we are bullish going long into 2021:

Incredibly well positioned in such a fast growing market.

Vertically integrated company = from designing the to growing and packaging - everything comes from one hand.

38 Current SKUs in market, 62 by end 2021.Competitor BYND for example only has 9 SKUs.

2 Billion AD Impressions in 2021.

First huge marketing campaing will happen this year with the agency NitroC.

Expansion to Mexico and Europe is about to start.

More than 17% held by Institutions which will only increase by time.

Profit margin more than 20% which will only increase.

Already in the 4 biggest US retailers

Target and Walmart tests are outperforming.

Category sales are up huge.

Analyst coverage promised soon.

Fiesty CEO & Highly Innovative with Sarah.

Sells through Q4 was said to have been incredible.

Media coverage through Cramer on CNBC , Youtubers and Blogger talking about this stock.

Introduced to Puplix,Kroker , 7 Eleven and dozen more.

I could continue this list like forever but i want to encorouge you guys to do your own research.

Investing is always invvolved with a risk of loosing your capital , so this is no investment recomendation at all. Just my personal opinion.

You will soon realize this is the start of something big, and they haven´t even been paying dividends yet.

This could be a hold forevere stock if things play out as planned.

If you like this idea please feel free to leave a comment or follow , it would be greatly appreciated.

Greetings,

Sebastian

MFLOURMaintain in an uptrend channel

Collection area 610-645

Cl below 600 (break uptrend)

Looking forward to increasing demand for flour due to MCO

Long term prospect

PCCS Sektor Consumer Products & ServicesTunggu break downtrendline

Shareholder acquire

Boleh monitor peers Cheetah, Prlexus, Caely

Since mid Oct, hidden reveal from 4 big names of Consumer Disc.Since mid Oct, this particular group of marquee Consumer Discretionary stocks - McDonalds MCD, Dollar General DG, Home Depot HD, Lowe's LOW - show a deteriorating pattern which the Dow DJI and the NASDAQ indices do not.

$BYND Accending Triangle, Strong Resistance @142 and @144Daily and 4H chart confirm these strong resistance levels, Ascending triangle forming over a month. MACD on daily pointing upwards and possibly break trend. A great long term hold, look for a 2%-5% break @ 141 for direction.

Procter & Gamble ~a safe gamble~The green arrow in the chart show the support being tested around $135.

The upside is around $144, and a stop-loss exit below the 100ema makes sense for at least 50% of the trade.

RSI has slightly improved, showing bullish intent.

PG is probably being used to collect dividend, so choppiness in the drawn channel isn't a negative thing.