HG1! Copper Day Trade 28-Sept-2023TRADE DIRECTION: LONG

Price broke and closed above the Short-Term Trendline (red line). Before that, there were many candlesticks with long lower wicks (yellow eclipses) and bullish reversal candles (green arrows) formed around the lower line of the Parallel Channel (green dashed line), indicating buyers had started to accumulate long positions and sellers took profit off their short positions.

KEY LEVELS:

1. Short Term Trendline (red line)

2. Parallel Channel (green dashed line)

3. Daily Pivot (Traditional Type)

TRIGGER SIGNAL:

Bullish Pin Bar (yellow arrow) and prior bullish reversal candles.

Copper

HG1! Copper Day Trade 26-Sept-2023TRADE DIRECTION: Downtrend; as indicated by the red trendline

KEY LEVELS: Daily Pivot and the red trendline

TRIGGER SIGNAL: Dark Cloud Cover and Bearish Pin Bar closed below the Daily Pivot

HG1! Copper Day Trade 25-Sept-2023

TRADE DIRECTION: Downtrend; as indicated by the red trendline

KEY LEVELS: Daily Pivot and the red trendline; price failed to break and close above it.

TRIGGER SIGNAL: Bearish Engulfing (red arrow)

Copper ~ 2H Intraday Chart (Sept-Oct)CAPITALCOM:COPPER chart mapping/analysis for short-term & intraday trades.

Copper ~ Daily Swing Chart (Sept-Oct)CAPITALCOM:COPPER chart mapping/analysis for med-long term swing trades.

CU Copper 22 / 09 MovePair : CU - Copper

Description :

Impulse Correction Completed and it will again make its Impulse in a Corrective Pattern Bearish Channel in Short Time Frame. We have Break of Structure if it breaks the Upper Trend Line then Buy and If it Rejects from the Demand Zone then Sell

$Copper Trend line break In the context of technical analysis, when CAPITALCOM:COPPER experiences an uptrend trend line break to the downside, it typically serves as a warning sign for investors that the previous bullish momentum may be waning. Such a break could indicate that the asset is shifting from a bullish to a bearish trend. This is often considered a sell signal or at least a reason to reconsider long positions in the asset.

Investors considering this development should look for additional confirmation signals such as increased trading volume during the break, bearish candlestick patterns, or other technical indicators turning bearish, such as the MACD crossing below its signal line or the RSI moving below 50.

It's also advisable to check for any fundamental factors that may be influencing the price of copper, such as economic data releases or changes in market sentiment, to ensure that the technical signal is not a false one.

In summary, a trend line break to the downside in an uptrending CAPITALCOM:COPPER market could be a significant bearish indicator, and investors should exercise caution and consider employing risk management techniques like setting stop-loss orders.

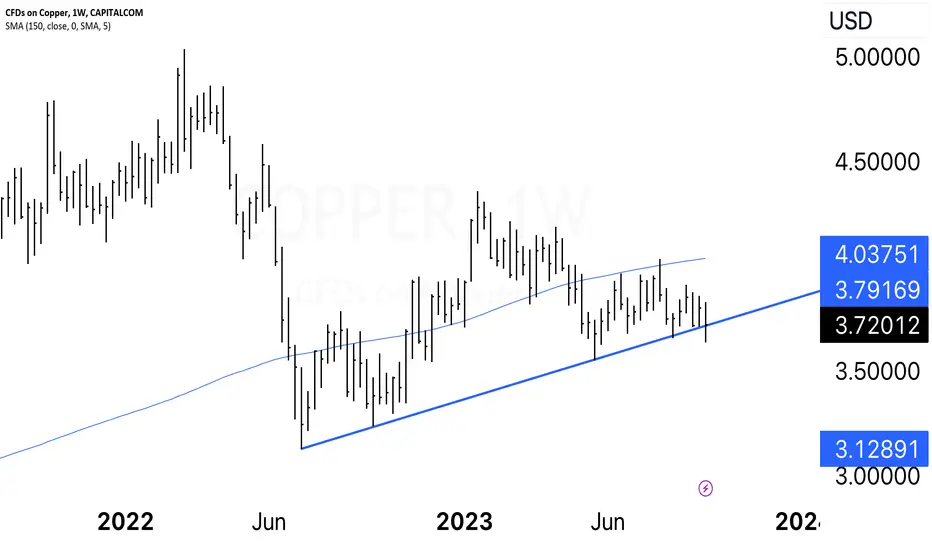

COPPER Two year Triangle is about to break out!Copper (HG1!) has been trading within a Triangle pattern for more than 2 years and recently the price action has gotten so narrow that it prompts to a break-out soon. The 1D MA50 (blue trend-line) has been acting as the Pivot level while the 1D MA200 (orange trend-line) had the last rejection on record on September 01.

The 1D RSI since the May 24 Low has been printing a similar price pattern to July - October 2022 (so far). That fractal was also using the 1D MA50 as the Pivotand after it broke its Resistance, it rose aggressively almost as high as the 2.0 Fibonacci extension. We will purse a more modest target, below the 1.5 Fib at 4.2000. The R/R is worth it as a break below the Higher Lows (bottom) of the Triangle will make us close the trade on minimum loss and open a sell instead targeting 3.5500 (Support 1).

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Silver - A 50% Long Setup. Trade Only. No HODL.In a post on Silver from June, I analyse that a run to $33 is on deck:

Silver - 33 Moons And An Options Opportunity

In the time that has passed, we've had two ~10% bounces that have been sold off.

To me, this is a peculiar pattern for a trendline play that leads to new lows in the immediate term future, and represents confirmation that $33 is on deck.

However, I'm also expecting a very bearish September across all markets, which I outline in a recent call on Nasdaq:

Nasdaq Futures - Are You Prepared For Red September?

Because I believe that we'll have a giant rally that takes out the tops of a lot of things heading into the end of 2023, and 2024 will mark the beginning of the real economic calamity.

When it comes to silver and gold being bullish in the long term, they should be, but the market manipulators will keep price supressed for a few reasons.

The first is that a renaissance in precious metals, or even a bubble in precious metals, will amount to promoting bullion, coins, bills, and even ore. These things are mankind's traditions, and are at odds with the current International Rules Based Order (IRBO) pseudo-Chinese Communist Party culture that more or less wants to install something like a cross between Shanghai's Zero-COVID social credit system and the Taliban.

The second is that China, which is still governed by the CCP and Xi Jinping, has bought an incredible amount of gold in recent times, if reports are true and not fabricated at least.

And so a short raid on precious metals would amount to a de facto economic sanction against China, which the IRBO claims to be de-risking against.

Moreover, if something should happen to the Party, whether that be natural disaster, a greater pandemic, Xi performing a Gorbachev-style coup against the Party overnight, or Heaven finally dealing with the CCP's 24-year persecution and organ harvesting genocide against Falun Dafa's 100 million spiritual practitioners, because China holds so much gold, there will be open selling into the market.

Prices will crash because the very wealthiest families on this planet are safeguards of tradition and will take advantage of the situation to purchase back that physical bullion and jewellery at record low prices amid the chaos.

"Buy when there's blood in the streets, even if it's your own," they say.

So here's the current call on silver.

The fake double top below the early May gap at $25.5~ is definitely manipulation.

It's traded back too far and hasn't shown any bullishness to give us confidence that we're going to go from $23 to $26 or $27 as a breaker pattern.

Because "resistance" has been printed, many very large players and retail traders who are short will position their stop losses over $26 and $27.

This becomes a target.

And in the meantime the goldbug moonboys have long stops under $22 and $21, which just so happens to be an untested gap.

So the trade here is to either look at a short on a retrace to $24 with a target of $21~, or just wait for $21 with a target of $33 by year end.

And then sell it all. Sell your spot. Sell your bullion, if you can't be hedged short.

Silver will eventually truly appreciate, and in a significant way, but it's not very likely to manifest before the new future unfolds.

And so in 2024, we may really see numbers sub $15 again. Ergo, because metals are, in reality, ranging and not trending, it's not a market for "buy and hold" to be an intelligent strategy.

Good luck.

COPPER: Neutral. Wait for a breakout.Copper is technically neutral, as also dipicted by the 1D outlook (RSI = 50.817, MACD = -0.013, ADX = 24.251) inside the HL trendline of the Bullish Megaphone and the LH trendline of the January High. This movement can only offer scalping opportunities.

If you want to commit beyond those, buy over the LH and target R2 on the medium term (TP = 4.1950) and sell under the HL and target S2 (TP = 3.5450).

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

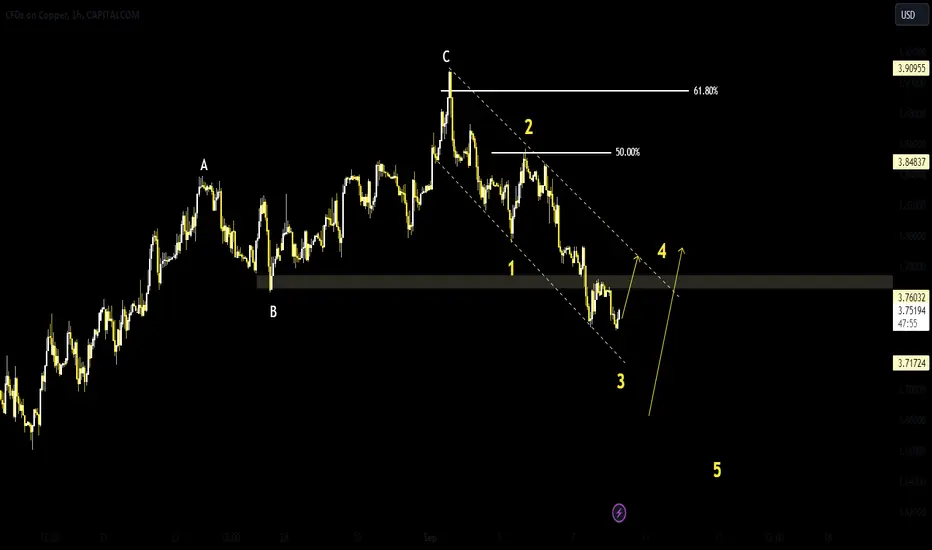

Copper 08/09 MovePair : CU - Copper

Description :

It has Completed its " 12 " Impulsive Wave at Fibonacci Level - 50.00 or Demand Zone. Bearish Channel in Short Time Frame and Impulse Correction in Long Time Frame completed its Impulse and Correction at Fibonacci Level - 61.80% it will again make Impulsive move

Industrial metals continue to face headwinds as Chinese data disIndustrial metals were the worst performing commodity sector last month and were down 2.7%1. Over the last six months, the sector is down 15.2% and has created the biggest drag on the overall performance of commodities.

China's real estate sector, once the engine of its economy, is now teetering on the edge of crisis because of excessive borrowing, overbuilding, and a housing slowdown. The government's crackdown on risky practices and sudden intervention in 2020 to prevent a housing bubble have led to over 50 Chinese developers defaulting or failing to make debt payments in the last three years. The consequences include reduced consumer spending due to falling housing prices, disappearing jobs tied to housing, and decreased business confidence. While policymakers have taken modest steps to address the situation, the real estate turmoil has spread to financial institutions and the broader economy, prompting concerns of a larger crisis. A build-up in industrial metal inventories over the last 3 months is consistent with market expectations of ample supply of the metals for the rest of the year, given relatively modest demand. Zinc inventory is up 96% while lead inventory is up 85% compared to 3 months ago.

This is clearly weighing on sentiment towards industrial metals. Copper (COMEX) was down 2.8%1, and aluminium down 2.8%1. The only bright spot in the basket was lead, which was up 3.7% last month. Speculative positioning in COMEX copper has been oscillating between positive and negative territories in recent months and entered negative territory again last month after briefly becoming positive2. COMEX copper inventory is up around 46% compared to 3 months ago. And although copper held in COMEX is one of the smaller stores of the metal, when combining London Metal Exchange, Shanghai Futures Exchange and COMEX, copper inventory is still 27% above where it was 3 months ago.

Nickel was down 5.7% last month1. Although nickel is widely known for its use in electric vehicle batteries, a growing market, it still draws around two-thirds of its overall demand from the production of stainless steel. China's steel market has been facing pressure in August due to continued high steel production despite sluggish end-user demand. Blast furnace utilization rates have risen, but some local mills in key steelmaking provinces like Hebei and Jiangsu have not received official communication about output reductions. Uncertainty surrounds the extent of China's steel output cuts for the rest of the year, with expectations of smaller scale cuts targeting environmentally sensitive regions. Rising steel inventories are attributed to robust production and weak demand. Despite potential production cuts, market sentiment remains cautious due to these challenges, and steel prices have declined. This, in turn, is weighing on nickel.

Source:

1 Bloomberg as of 21 July 2023 to 21 August 2023

2 Commodity Futures Trading Commission (CFTC) as of 15 August 2023

3 change in inventory over the past 3 months by United States Department of Agriculture

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Copper: Letting go🕊️The copper price is slowly but surely breaking away from our blue target zone between $3.7730 and $3.5445. Since the price has already placed its low of the magenta wave (x) within this zone, we expect significant rises above the resistance at $4.19. It should then go down to our green target zone between $3.0860 and $2.5965.

Copper - Did Social Media Tell You To Long The CCP Again?They call copper "Doctor Copper" because it's said to forecast the overall world economic conditions on account of being tightly wed to manufacturing.

Well, what people are really yammering about with that over the last 20 years is whether or not the Chinese Communist Party is healthy, and the world by proxy being healthy because it tied itself to the most heinous regime in history, the one responsible for the 24-year persecution of Falun Gong by former Chairman Jiang Zemin and the accompanying organ harvesting and genocide.

Unfortunately for all the blind bulls, the early 2021-2022 price action was a pretty good indication of a top, and that top is really confirmed by the fact that since October of '22, this bounce has been pretty weak, and starting this month, with all the drama surrounding the slow collapse of the Chinese economy, took out the previous two months' lows.

Monthly shows you that August price action took both the July and June lows.

Like, that's not the kind of "signal" you want to see to get long for a new all time high.

When something is retracing to take out major highs, you want to see lows rarely violated with something of a freight train towards the old highs.

Weekly bars show us something of a subtle pattern where it looks like it's just taken some lows and is consolidating and continually flirting with going back up.

But in reality the market makers are, most likely, just selling more under the previous $4.00 area.

And if that's really true, it means another gap down is imminent, especially after an entire quarter of ranging.

If you ask me, the first area that you can look for a long that is more than a scalp on copper is under $2.8, which is a critical pivot from September.

And a more likely target in the next 12 months is the $2.00 mark, which was barely swept out in the COVID drama.

The reality is, my friends, the Chinese Communist Party is going to fall overnight in our lifetimes. Not five or ten years from now. But very shortly, and everything is going to change.

Whether that is caused by Xi Jinping throwing away the CCP to protect himself and China from being taken over by the International Rules Based Order as it uses Taiwan as a soft proxy war, or because the whole world collapses under the results of the persecution of Falun Dafa, since everyone's been going to Shanghai to worship the toads and the Devil Red to get financial benefits.

This is the danger.

The danger is imminent.

But copper trades painfully slowly, so if you want to do this you have to have long duration, ignore the noise, and be willing to suffer some drawdown.

China under the CCP is never going to recover. Things are never going to be okay ever again.

Things will be okay once mankind returns to tradition.

But there won't be an international stock market like this anymore that day.

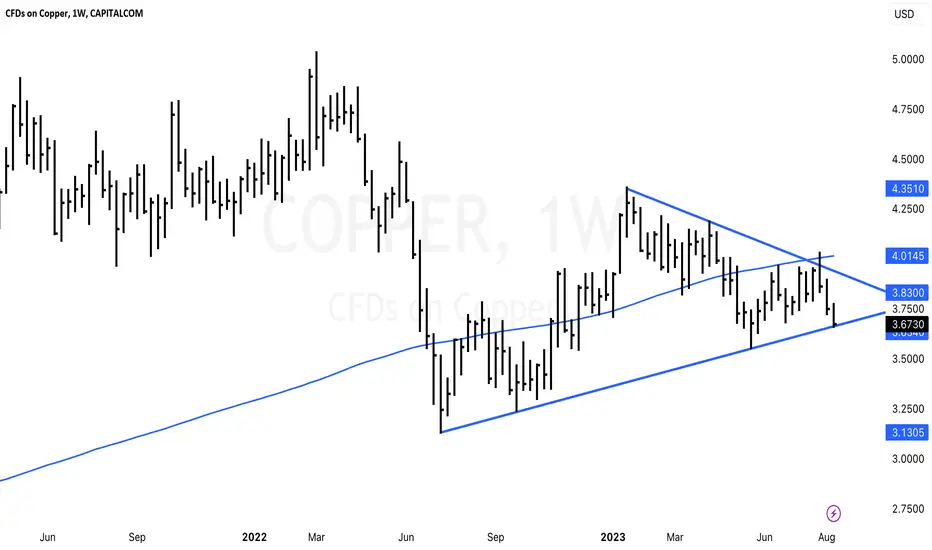

Dr Copper ~ Snapshot TA / Contraction x Expansion = InflectionIt ain't easy being DR CAPITALCOM:COPPER

Peaked in March 2022, only to crash -38% & bottomed-out in July 2022.

Since then it has fluctuated between Contraction (will Global Economy collapse?) versus Expansion (will Global Economy recover?), while also contending with outlook of China's Economy, yeesh lol.

Copper's price action has also been compressing, as descending trend-line squeezes current Trading Range against ascending Parallel Channel.

This suggests momentum will eventually need to "pop" in either direction...but it could also continue trading sideways a little longer while more data is disseminated by Market Makers to make a confident decision, TBC.

Tick tock, time is running out for the Doctor..

Boost/Follow appreciated, cheers :)

AMEX:COPX AMEX:CPER COMEX:HG1! COMEX:HG2!

COPPER 24-08 MovePair : COPPER

Description :

Impulse Correction Impulse

Break of Structure

Bullish Channel in STF as an Corrective Pattern

RSI - Divergence

Fibonacci Level - 50.00%/ 61.80%

Gold - The Tea Leaves Say: More Downside On Deck3.5% is a lot in gold, and that's about the range of the total landslide we've been through the entirety of August so far.

It's the kind of pattern where goldbugs and USD collapse narrative nerds go long and go long or hodl and hodl but the price never goes up.

In my last call on gold from the beginning of July, I warned that $2,000 was a death trap. That call was pretty successful, coming just a few dollars shy of the target, abeit it was because the next month's futures contract settled some 2% higher.

Gold - $2,000 Is a Death Trap

And with the index markets at large, I caution that Nasdaq not breaking 15,000 is actually a real bull trap

QQQ - Is It Rally Time? Or Are You Too Early?

With gold, geopolitical risks are heightened because Xi Jinping and the Chinese Communist Party he has yet to throw away bought a lot of gold, and at relatively high prices, according to media reports at least.

And thus, because of this, a form of subtle on-the-low economic sanctions against Xi and/or the CCP can be to devalue the price of gold, which puts the central bank in a bind.

And this is a real problem for China right now with all the other economic catastrophes that land one after another, and the flooding, and the instability, and the posturing of the International Rules Based Order about war/invasion via Taiwan.

The CCP won't invade Taiwan. But China might get invaded by the IRBO via Taiwan.

You might not believe it. But give it some sober thought. Tacticians are tacticians for a reason. Hitting from the shadows and blind spots is a real useful thing.

But for Xi, he can always weaponize the 24-year persecution against Falun Dafa that was launched on July 20, 1999 by former Chairman Jiang Zemin against the entire world.

Because the whole world has been going to Shanghai to train under the Jiang faction for economic and social benefits. Which means a lot of closet skeletons. Which means a lot of data dumps can serve as weapons delivered to international media in the future.

Anyways, here's the call, friends.

Gold is obviously going down and will go down farther. It really looks like it's seeking at least the short term lows, which means $1,900 is longzo-gonzo.

And so on a dump from where we're at at time of posting to, say $1,850, you're getting 5% on a very safe short.

You can short the hole.

And 5% is a lot of money on gold.

Probably only at $1,850 can we look for reversal longs towards new all time highs.

But with how lethargic gold has been, we may very well just have seen the top on the re-run to $2,080.

$copper buy the rumor sell the news tradeChina news are more often..

I won't mind if the prices continues to go down, because of the low risk of my position at the moment.

Confluences:

-false brake-downs

-61.8 retracement

-buy the rumor sell the news

-MAs work

#COPPER Weekly Chart Trend Line TestDOC COPPER Weekly Chart Trend Line Test. Guess who was the legendary trader that said this?

"Copper is a very sensitive barometer of the business cycle. It is the first metal to feel the pulse of trade. When copper goes up, it is a sign that business is improving. When copper goes down, it is a sign that business is declining."

Precious Metals Schematics: A look into the Macro of FibonacciI have Listed Silver, Copper, Platinum, Palladium, Aluminum, and Gold into one chart. These are 6 of the top Metals all in Heikin Ashi Candle form.

They all have their own complex Fibonacci Clusters within each one. It may look confusing at first. But understand that one set of lines are horizontal extensions and another set are angled extensions within each one.

Why Silver stands out.In the ever-evolving landscape of global economics, precious metals like silver, often serve as key indicators and safe havens. This week, we'll explore the factors making silver an interesting prospect in today's market.

Current Macroeconomic Indicators:

The latest Consumer Price Index (CPI) data indicates a slight increase in the US for July, registering at 3.2%, up from the previous month's 3%. Predictive models from the Reserve Bank of Cleveland suggest an impending rise for the August CPI. Concurrently, the Reserve Bank of Atlanta's GDPNow model projects a rise in GDP figures.

Silver, Inflation & GDP:

The above becomes important when historical data reveals that significant spikes in silver prices often follow periods of simultaneous rises in GDP and inflation. Notably, in years that saw increases in both indicators, silver recorded gains of 38% and 46% in 2009 and 2020, respectively. Conversely, 2002 saw a modest 2% return.

Silver vs. Gold:

A measure of relative value between the two major precious metals via the ratio of Silver to Gold, further substantiates the idea of a potential strength in Silver. The ratio is trading just off a trend support-turned-resistance and at the upper end of the symmetrical triangle. Resistance here can play out in the format of silver strengthening relative to gold.

Yields and Silver:

The longstanding inverted relationship of yield and silver can be observed in the chart, but the ratio provides some insights into the limits of this relationship. What’s immediately obvious to us post 2008 there has been a regime change in this relationship as yield grinded lower and silver remains elevated. With no immediate large catalyst on the horizon, it is likely the current regime will hold and hence, the ‘floor’ in this relationship is near. Meaning relative to current levels of yield, Silver is trading on the lower side.

Equities vs ‘real’ economy:

Beyond being a precious metal, silver's industrial applications—from automotive to solar panels and electronics manufacturing—make it a bellwether for the 'real' economy, akin to copper. Comparing the Nasdaq 100 against industrial metals illustrates a disparity between equities and the 'real' economy, positioning silver as significantly undervalued relative to peers like copper and gold.

Positioning:

Current market positions, particularly among net Non-Commercials, seem to favor silver with a growing bullish sentiment.

Technical Analysis:

A noteworthy observation is the persistence of the 22.5 level as a pivotal support and resistance mark for silver, a trend tracing back to the 80s.

Prices currently thread above this level and remain supported by an uptrend that began in August 2022. Additionally, RSI points to oversold, and in the past 4 instances when RSI reached such levels, prices quickly rebounded thereafter.

Against the above factors, we see support for Silver, on multiple fronts, such as economic cycle, relative value against equities, and underpriced when compared against gold. Hence, to express our view on Silver, we can set up a long position on the Silver Futures at the current level of 22.67 with a stop at 21.8 and take profit at 25.10 . Silver prices are quoted in U.S. dollars and cents per troy ounce and each 0.005 move is equal to 25 Dollars.

The charts above were generated using CME’s Real-Time data available on TradingView. Inspirante Trading Solutions is subscribed to both TradingView Premium and CME Real-time Market Data which allows us to identify trading set-ups in real-time and express our market opinions. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Disclaimer:

The contents in this Idea are intended for information purpose only and do not constitute investment recommendation or advice. Nor are they used to promote any specific products or services. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios. A full version of the disclaimer is available in our profile description.

Reference:

www.cmegroup.com

www.atlantafed.org

www.clevelandfed.org

Copper: A bit lower 🪜The copper price is back in our blue target zone and dedicates itself to extending the low of its blue wave (c). After this fall, we expect significant rises in the context of the magenta wave (y) above the resistance at $4.19. In the short term, speculative opportunities are thus given here on the long side with the active blue target zone. Subsequently, however, new downward movements to our green target zone will be interesting for long-term investors.

TMC Offers Massive Upside Mining the Seafloor The weaker dollar has led to prices for commodities climbing sharply and quality mining stocks generating substantial gains. This has occurred in the face of the Federal Reserve raising interest rates at the fastest pace in history. Rising rates normally strengthen the dollar and we did see a USD rally in the first half of 2022 when the Fed began raising rates. But that rally fizzled and the dollar took a sharp turn lower in September of 2022, even with the Fed continuing to raise rates, doubling the Fed Funds rate from 2.5% to over 5%.

This can be explained by the markets being forward-looking and anticipating an end to rate hikes on the horizon. But this is also partially due to inflation remaining stubbornly high with no signs of fiscal responsibility from the current administration. And now that most of the rate hikes are behind us and we are at or near a terminal Fed Funds rate, we think the dollar decline will accelerate, which will translate into significantly higher commodity prices.

TMC the metals company Inc. (TMC)

TMC the metals company Inc., a deep-sea minerals exploration company, focuses on the collection, processing, and refining of polymetallic nodules found on the seafloor in the Clarion Clipperton Zone (CCZ) in the south-west of San Diego, California. It primarily explores for nickel, cobalt, copper, and manganese products. This company is interesting because they are the first publicly-traded company to attempt mining valuable metals from the sea floor.

They claim to be developing the world’s largest estimated source of battery metals, with enough nickel, copper, cobalt and manganese to electrify the entire U.S. passenger vehicle fleet. They estimate massive In situ quantities of nickel, copper, cobalt and manganese with a total resource of 15,700,000 t Ni / 2,400,000 t Co / 13,300,000 t Cu / 350,000,000 t Mn. Some nickel projects have high grade, some have a large resource, but TMC is an outlier among peers with the largest NiEq resource and highest NiEq grade.

The company estimates an NPV of over $10 billion at current nickel prices, based on just 22% of the NORI-D resource. Yet the company is trading at a market cap of around $300 million. This is a multiple of 10x to 20x less than their land-based peers, implying huge upside should they be successful obtaining permits and moving into production.

In just the past week, TMC said it plans to apply next year for a license to start mining in the Pacific Ocean, with production expected to start as early as late 2025. The company has signed non-binding MoU with Pacific Metals Company (PAMCO) of Japan to evaluate the processing of 1.3 million tonnes per year of wet nodules But environmental campaigners say seabed mining could have a catastrophic impact on marine ecosystems, so it is still unclear if they will get the license needed to start mining. There are also questions around the costs to pull these nodules up from deep locations on the seafloor.

TMC is an interesting speculative mining play. Management believes it has rights to the globe’s largest undeveloped Nickel project. Nickel is one of the most widely used minerals for EV batteries and will see increased demand in the years ahead. A supply gap is likely to push prices for nickel much higher in the years ahead, potentially increasing the value of TMC as well. Much will hinge on getting final regulations from the International Seabed Authority, which seems to be in no hurry. But if this happens and TMC gets permits, I think this stock is going to be 5x to 10x for investors buying shares ahead of the news.

The share price spiked higher on increased media coverage lately, but dropped back just as fast. I recommend this balanced article from CNBC for continued reading on TMC. The price went from 65 cents to $3.00, before falling back to $1.10 currently. Everyone will have to decide for themself if this is a good opportunity to buy the pullback or simply catching a falling knife. A small allocation as a lottery ticket could be of interest for risk-tolerant investors.