CLOSING (IRA): SPY MARCH 20TH 319, 320, 322 SHORT CALLS... for a .31/contract debit.

Notes: Hard to believe that these were well in the money a few days ago, but they've largely done their job. Over time, I collected 11.70/contract in credits, and am closing out here for .31, so made 11.39 ($1139)/contract, all while protecting my SPY position from most of the bruising it got over the last week. (See Overwriting Post, Below). The downside (if it really is one) is that the entire position has returned to net delta long, although I've still got a QQQ long put diagonal hanging out there (See Post, Below) providing me with some short delta that was erected as a secondary hedge against.

The 370's have gone no bid, so will just leave those on to expire ... . Generally, I like to erect these on strength, but may re-up if I can sell calls clear of those all-time-highs and get paid to do so.

Coveredcalls

TUTORIAL: BUYING POWER EFFICIENT CC OVERWRITINGLet's face it. Being in a net delta long covered call in a market downturn can blow. Typically, the vast majority of covered calls are 70-80 net deltas long per one lot, depending on how aggressive your are with your short calls. There are a number of solutions to cutting that net delta to something more tolerable: (a) sell calls; (b) sell short call verticals/diagonals; (c) buy long put verticals/diagonals; or (d) drive your short calls to at-the-money or into-the-money. This post discusses overwriting your covered calls with short call diagonals.

While selling calls against is the most straightforward of approaches, many brokers won't allow naked call selling, particularly in cash secured environments like IRAs. Moreover, selling naked against may not be the most buying power efficient of approaches. The short call diagonal not only provides a work-around to the "no naked call" prohibition, it may also afford some buying power relief over going naked.

Pictured here is a laddered, short call diagonal, overwrite setup (say that quick three times) in the September, December, and March expiries of SPY with the short options camped out at their respective 20 delta strikes, the longs at "cheap." It pays 6.31 in credit, has a theta of 5.49, and is -53.77 delta. It's naturally applicable to any underlying and can be modified to afford you the amount of overwrite/delta-cutting that you want, even where you're not in a one lot.*

You can naturally also just ladder out short call verticals with the short legs at the 20's and the longs at "cheap"; my preference, however, is for getting into the longs once so that I can work the calls as though they were naked if they have to be managed, as opposed to managing a spread. Moreover, I can leave the longs alone throughout the life of the setup and re-use them even if they're no bid as buying power effect cutters, thus saving a bit on fees, since I'm only in and out of a single contract, as opposed to two, as I would be with a spread.

As usual, there are pluses and minuses to the setup. The pluses: (1) it flattens net delta, thus smoothing out your P & L in a downturn; (2) it provides additional cost basis reduction on top of any dividends you might be receiving by being in shares and/or with the short calls you've already got covering your shares. The minuses: (1) It ties up buying power to the extent of the width between the short call and long call strikes minus any credit received; (2) the additional short calls have to be managed if tested.

* -- For example, the pictured setup would flatten the net delta of a 53 share SPY position to virtually flat, since 53 shares of SPY are 53 delta long and the setup is 53.77 short.

OPENING: ANF "MONIED" COVERED CALLHere, I'm going covered call because ANF has a small divvy that I want to attempt to grab (.20/$20 per 100 shares), so I need to own the shares to do that. The record date is 3/3, so I will need to hold the shares until at least then. I'm going monied because I just don't trust this thing not to implode somewhat post earnings ... .

Metrics:

Probability of Profit: 73%

Max Profit: $52/contract (+$20 dividend)

Max Loss: $948/contract (assuming the stock goes to $0)

Break Even: 9.48

Notes: Naturally, I'm hoping that the 10 short call stays ITM post-earnings. If it doesn't, I'll be rolling that out to reduce cost basis in my shares. I'll otherwise look to take the trade off as a package for $10 after the date of record, since that's cheaper than being called away (for which there is an onerous fee).

OPENING: GDX COVERED CALLBought shares at 26.02 and sold the Oct 21st 26.5 call for a 24.86 ($2486) per 100 shares/contract debit.

In this particular case, I'll be looking to take this off for 105% of what I paid to put it on: 1.05 x 2486 = 2610, which should yield about $120/contract in profit. I usually shoot for 110% (or a 10% ROC), but am just looking to get in and out of the trade in short order if I have a shot at it ... .

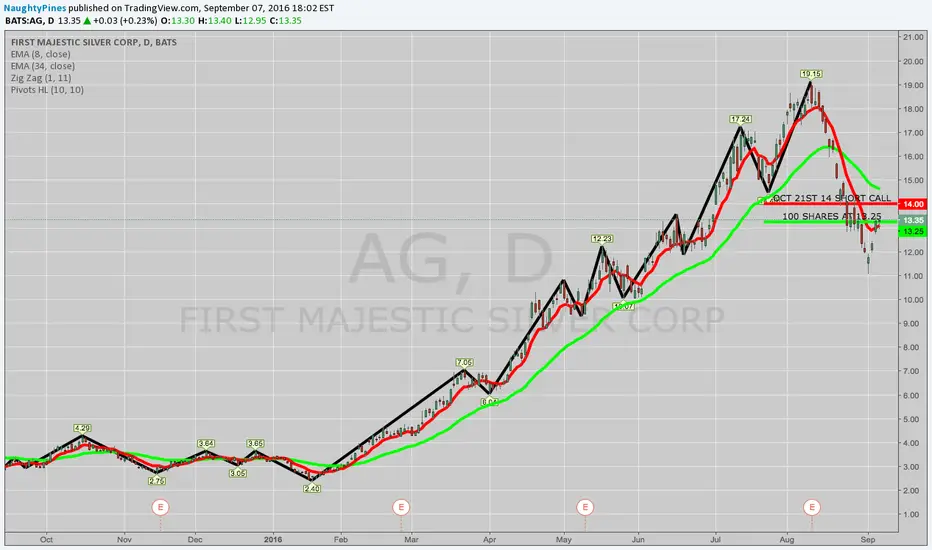

OPENING: AG COVERED CALLMy timing could have been somewhat better on this at the sub-12 dip, but better late than never ... .

Metrics:

Bought 100 Shares at 13.25

Sold Oct 21st 14 call

Whole Enchilada: 12.30 db

Max Profit: $170 (if called away at 14)

ROC: 13.8%

Notes: I promised myself after closing out my XME short put that I wouldn't be dipping into any more miners ... . Just couldn't help myself ... .

FOR 45 DTE SETUPS, ROTATING INTO ETF'SSometimes life just plain ass gets in the way of your trading ... . Starting October 1st, my "number's up" for jury duty for the entire month of October. I may be called to serve any time during this period, sit for a lengthy period of time in a room, and then be excused because the parties have reached a last minute agreement or I may have to sit through an actual trial that goes on fairly continuously for a week or two. In sum, there's no way to plan your day, your week, or, really, your month ... .

Since I don't think the environment will be very conducive to trading (even assuming I could do that effectively on my phone or iPad), I'm going to go with trading low key setups that I don't need to keep an eye on, as compared to, for example, short strangle earnings trades with short DTE. As of Friday close, there are several >35% ETF's I have eyeballs on -- GDX (gold miners), XME (miners), EEM (emerging markets), EWZ (Brazil), and XBI (36.1).

Most of these are, in the scheme of things, "fairly cheap," so I may go covered call rather than with an options strategy that has a clock on it (i.e., spreads, strangles with "date certain' expiries).

Naturally, we have the "FOMC dance" coming up, so I may hand sit out this week until the tsunami of media spin, speculative positioning and such, passes ... .

OPENING: WLL COVERED CALLDid this at open, after which the underlying tanked ... . Heck, what hasn't tanked in today's market. In any event, continuing to work this sub $10 high IV underlying here.

Metrics:

Bought 100 Shares at 7.48

Sold Oct 21st 8 call

Whole Package: 6.94 debit

Max Profit: $106

ROC: 15.3%

WITH VIX SUB-15, PREEM SELLING OPPS ARE OUSTIDE BROAD INDICESAs I've posted several times before, my preference generally is to (1) sell premium in broad-based index instruments (e.g., SPY, IWM, QQQ, SPX, RUT) if VIX > 15; and (2) if VIX < 15, look for premium selling opportunities in non-index exchange traded funds with implied volatility of >35% and/or individual underlyings with implied volatility of >50% and where the implied volatility percentage is in the 70th or greater percentile for the preceding 52-weeks. Unfortunately, VIX <15 here and underlyings -- whether exchange traded funds or individual underlyings -- with implied volatility both in the 52-week 70th percentile and above 50% implied volatility are absent here.

Consequently, I am "settling" for mere >50% implied volatility plays in exchange traded funds and in individual stocks. This isn't ideal, but I'm playing these small, keeping quite a bit of powder dry in the event that volatility does pick up at some point in the weeks ahead.

There are some opportunities out there, and they're where they've been for the past several weeks: in gold, miners, oil and gas, and biotech. The top IV individual stocks with liquid options are: NVAX (195.0) (biotech); RTRX (132.4) (biotech); GNW (100.3) (financial); WLL (80.5) (O&G); CLF (76.1) (iron ore/mining); AG (75.6) (silver miner); CHF (73.9) (oil and gas); AKS (70.0) (steel); EGO (62.7) (gold miner); VRX (61.9) (biotech); AMD (61.8) (semiconductor); and AUY (61.6) (gold miner). The top IV exchange traded funds are GDX (43.7) (gold miners); and XME (39.2) (mining).

And, because of the "smallness" of many of these underlyings (many are under $10), I'm taking a slightly different strategic tack here, either doing covered calls from the outset or selling puts as a precursor to a covered call, the notion being in the later case to either keep the premium or get put the stock at a lower price, after which I'll sell calls against. Things like short strangles and iron condors simply will not yield enough premium on setup to bother with in most of these smaller stocks.

In the one play that I currently have on in XME (see post below) that I could have strangled, I opted to just naked short put to leave open the option of covered calling it if I get put the stock or rolling the short put down and out for additional duration and credit should the underlying move that way rather than dealing with the hassles of call side risk. Naturally, these options would still be open to me were I to strangle, but doing just the short put relieves me of call side risk (there's always trade-offs).

For me personally, I'm looking to move into plays involving something other than gold, miners, or oil and gas, since I have quite a few of those on already. Unfortunately, this makes for pretty slim pickings in my little list, with the potential focus being on AMD and (ick) VRX. I'm already in NVAX and GNW, and I'm not fond of RTRX (it only offers monthlies and currently the Oct monthly expiry only offers 2 1/2 wide strikes; naturally, that may change ... ).

HIGH IMPLIED VOLATILITY OPTIONS (8/28)One of the first things I do when searching for either covered calls to do or just general premium selling plays is to look for high implied volatility underlyings with relatively decent expirations, strike widths, and fairly tight spreads (i.e., having weeklies is best with $1 wide strike widths and a bid/ask that is no more than .15 wide from top to bottom is ideal, although I'll bend those rules from time to time; $TWLO's a good example of this, nasty wide spreads, but premium too juicy to pass up).

After I identify those, I start looking at actual plays to see if I can make something out of them, looking at all possible premium selling strategies -- short nakeds, short straddles/strangles, credit spreads, iron condors, etc.

Here's today's lists of stocks, sector exchange-traded funds, and broad-market exchange traded funds, ranked by their implied volatility percentage:

Stocks

RIGL 219 (biotech) (in a trade), NVAX (biotech) 185 (in a trade), GSAT (telecomm) 152, TDW (O&G) 117, SDRL (O&G) 93, MX (semicon) 78, CHK (O&G) 78 (in a trade), GLNG (solar) 76, CLF (mining) 75 (in a trade), WLL (O&G) 73 (in a trade), CDE (mining) 72, HL (gold/mining) 70 (in a trade), GNW (financial) 69, LC (financial) 65, VRX (biotech) 62, AUY (gold/mining) 60, AMD (semicon) 60, NE (O&G) 60 (in a trade).

Sector Exchange-Traded Funds

GDX (gold miners) 42, XME (mining) 38 (in a trade), XBI (biotech) 36, XOP (O&G) (33).

Broad Market Exchange-Traded Funds

EWZ (Brazil) 34.6, EEM (Emerging Markets) 21.4, IWM (Russell 2000) 18.5, QQQ (Nasdaq) 15.7, EFA (Word, ex. US/Canada) 14.4, SPY (S&P) 14, DIA (DJIA) 13.5.

Notes: The $RIGL play posted here is the play I'm in. It's not currently workable except possibly as a naked 2.5 short put play due to strike width -- 2.5, 5.0, etc.

BUYING POWER EFFICIENCY: "POOR MAN'S" VS. TRAD COVERED CALLSThere is more than one way to skin a cat. But some ways are more buying power efficient than others ... .

Here, I'm looking at a covered call in X. The implied volatility is >50%, so I can get a bit of premium on the call side to reduce my cost basis in any stock I buy here. For example, if I buy shares at 20.38, and sell the Sept 30th 20.5 call against (for a 1.50 ($150) credit at the mid), I can get into the whole package for a 19.03 debit ($1903), my cost basis in the shares will be $19.03 per share, and my max profit is $147 if called away at 23. However, for some, that $1903 stick price can be hefty, especially if they're working with a smaller account. The drawback is that I'm (a) stuck with stock I bought at 20.38 per share; and (b) the buying power effect may be larger than I'd like.

In comparison, I can also do a PWCC or poor man's covered call. Traditionally, this is set up using a long-dated, deep ITM long call option to stand in for the stock and -- like the covered call -- a call sold 30-45 DTE. Most of the time, I set these up using the 70 delta strike for the long option and the 30 delta strike for the short. As with the traditional covered call, I'm looking to reduce my cost basis in my "synthetic stock" (here, the long option) by selling calls against. Compared to the traditional covered call, the PWCC has a smaller price tag -- $361 (which is also my max loss for the setup, assuming I do nothing at all), and I look to exit the setup as a whole at 10-20% of what I paid for the setup which, in this case, isn't as attractive as the $147 max profit of the covered call. However, there is one other aspect of the setup worth noting -- my buying the Jan 20th 18 call gives me the right to exercise for shares at $18. With the covered call, I'm locked in with 20.38 shares; with the PWCC, I'm not.

NEXT WEEK'S COVERED CALL CANDIDATES: NE, CLF, AMD, WLL, OASHere are my candidates for covered calls next week. Right now, they're based solely on ROC metrics, the key being to get at least a 10% ROC if the shares are called away at the short call strike. Additionally, the focus is on sub 10.00 debit plays; underlyings of higher dollar value are generally more amenable to other strategies.

After looking at the charts, as well as doing some due diligence on the companies, I'll cull the herd ... .

$NE (O&G): Buy shares at 6.21; sell the Sept 30th 6.5 call; 5.85 db; $65 max profit (11% ROC).

$CLF (Mining): Buy shares at 6.09; sell the Sept 30th 6.5 call; 5.75 db; $75 max profit (13% ROC).

$AMD (Semiconductor): Buy shares at 7.62; sell the Sept 30th 8 call; 7.21 db; $79 max profit (11% ROC).

$WLL (O&G): Buy shares at 8.04; sell the Sept 30th 8.5 call; 7.36 db; $114 max profit (15.5% ROC).

$OAS (O&G): Buy shares at 10.27; sell the Sept 30th 11 call; 9.84 db; $116 max profit (11.8% ROC).

NEXT WEEK'S COVERED CALL CANDIDATES: ZIOP, NVAX, LC, WLLHere's my "short list" for covered call candidates for next week generated by looking at Barcharts.com high volatility stock options list and the Dough grid:

WLL buy shares at 7.66; sell Sept 16th 8 call; 7.10 debit; $90 max profit (12.7% ROC)

CC buy shares at 11.45; sell Sept 16th 12 call; 10.78 debit; $122 max profit (10.6% ROC)

LC buy shares at 5.40; sell Oct 21st 5.5 call; 4.85 debit; $65 max profit (13.4% ROC)

ZIOP buy shares at 5.46; sell Oct 21st 6 call; 4.65 debit; $135 max profit (29.0% ROC)

NVAX buy shares at 7.04; sell Oct 21st 8 call; 5.42 debit.; $258 max profit (47.6% ROC)

FCX buy shares at 11.92; sell Sept 30 12 call; 10.90 debit; $102 max profit (9.3% ROC)

JCP buy shares at 10.55; sell Sept 30th 11 call; 9.59 debit; $96 max profit (9.6% ROC)

Notes: (1) WLL's a petro play. Because so many small petro companies are in trouble of one kind or another (i.e., shale and/or offshore oil exploration exposure), I generally prefer playing something with a little less "single company exposure" (e.g., XOP). But, hey, it meets my general rule of >10% ROC. (2) CC is a basic materials/chemical play. It spun off from DuPont and has had quite an up run here in spite of a recent punitive damages judgment for chemical dumping (weirdly, the stock dipped and then subsequently popped on the news, probably out of relief that the debacle was in the rear view mirror). (3) LC's been in a downtrend since IPO. At best, a money, take, run play. (4) I still like ZIOP. It's biopharma and has a fairly diverse pipeline such that if one drug fails, they still have more in the hopper. And that 29% ROC, well ... drop dead gorgeous if it can get to $6. (5) I'm also in NVAX (biopharm). In comparison to ZIOP, their pipeline is quite narrow and currently devoted to a single vaccine (RSV). sg.finance.yahoo.com (vaccine "could be breakthrough," but not time to "break out the champagne" (code for "it could suck ... or not")). (6) FCX (mining). I covered called this in late 2015, early 2016 which commodities were at a cyclical low and then bailed out when it appeared to be topping. Looking back, it kind of looks pricey here in comparison, and I'm not so hot on the ROC. However, it's highly liquid, and it has some room to pop to 14.00 resistance (and naturally some room to cave; the 2016 low is sub-$4). (7) JCP. Well, it's JCP. Plus, it's had a bit of a run up here, and if past performance is indicative of future results, well, it could zombie trade back to sub-$9 and with the ROC, well, not at the top of my list ... .

THREE COVERED CALL IDEAS: WTW, NVAX, AND FEYE(?)WTW: Buy at 10.56/share; sell Sept 16th 11 call; 9.27 debit at the mid; max profit $173/contract (18.7% ROC).

NVAX: Buy at 7.51/share; sell Sept 16th 8 call; 6.01 debit at the mid; max profit $198/contract (32.9% ROC). (I'm already in a similar NVAX trade .. ).

FEYE: Buy at 13.95/share; sell Sept 16th 14 call; 10.67 debit at the mid; max profit $333/contract (31.2% ROC). The reason why I put a question mark next to the FEYE is that it's still gyrating about post-earnings and the pricing on the short call is unlikely to be accurate (it will change at open). So this may not be nearly as sexy at NY open as it looks to be right now ... .

NEXT WEEK'S "SHOPPING LIST" -- FEYE, ANFI, FIT, RTRX, MCRB(?)With broad market volatility abysmally low (VIX <12), it's a game of hunt and peck for "diamonds in the rough" in terms of premium selling.

For the most part, I'm looking for sub-$20 underlyings here with high implied volatility for either selling naked puts (bullish assumption) or initiating covered calls where the purchase of the stock, combined with selling the first out-of-the-money call 30-45 DTE, will yield at least a 10% ROC if the stock is called away at the short call strike.

The reason why I'm sticking with particularly low priced underlyings is (a) I don't want to tie up a bunch of buying power on these short-term (basically) engagement trades; and (b) don't want to take a lot of risk on dollar and cents wise. The max loss you can experience with an outright stock purchase, a covered call, and/or a naked short put is the risk associated with the stock going to "0"; less room to fall equals less room for loss. Additionally, the reason why I'm going covered call/naked short put over a short strangle/iron condor (my standard go-to's) is because you simply cannot get enough premium out of a short strangle or iron condor to make doing those on these low-priced underlyings worthwhile with those kinds of setups.

With all that background in mind, here's what I'm looking at:

FEYE: It announces earnings in a few days here, but the metrics are good enough to either go naked short put or to just dive right into a covered call. (Covered Call: 100 shares at 17.42; Sept 16th 18 short call for 1.54 credit; whole package, 15.95 debit; max profit 2.05 ($205); ROC 12.85%; Sept 16th 16 short put: 1.05 cr at the mid).

ANFI: I've never played this little specialty foods company before. (Covered Call: 100 shares at 7.11; Sept 16th 7.5 short call for .75 credit at the mid; whole package, 6.70 debit; max profit .80 ($80); ROC 11.94%). This isn't the most liquid thing in the world, so whether the package is as "sexy" as it is in the off hours remains to be seen.

FIT: This is a one trick pony, and I generally don't like one trick ponies; nevertheless, I'm glad to ride a one trick pony for a little bit if the premium is there. (Covered Call: 100 shares at 13.66; Sept 16th 14 short call for 1.23 credit; whole package 12.37; max profit 1.63 ($163); ROC 13.18%).

RTRX: Another high volatility biopharma stock. I'd rather be put at $12 a share than $15, but the underlying is afflicted with odd-ball, $2 1/2 wide strikes to work with, so it's either 12.5 or 15 short put, if you decide to take that path. (Sept 16th $15 short put goes for 1.52 ($152) at the mid; Covered Call: 100 shares at 17.93; Sept 16th 20 short call for 2.30; whole package: 16.20; Max Profit: 3.80 ($380); ROC 23.5%). Unfortunately, the first short call strike above current price is at 20, so the underlying will have to move from 17.93 to 20.00 for you to get called away, so this might be a longer term sort of play than the others due to the short call's distance from current price.

MCRB: This thing has tanked mightily, due to lackluster trial data on one of its drugs. There are other drugs in the pipeline, but the question is whether its losing some 70% of its value on Friday is a buying opportunity or the start of a long death spiral. Currently, I'm unable to get pricing on puts below the underlying's current stock price, so I'll have to take a look at it at market open.

EFA: PULL THE TRIGGER AT 51 OR WAIT UNTIL 45.50?One of the other brutalized issues post-Brexit is EFA, which is basically "everyone" besides Canada and the U.S.

Here, the point at which I would consider a buy for my covered call portfolio is subject to change, depending on what happens at 51, which is the 50 Fib from the 2009 to the 2014 high. That would not be a bad buy area, but obviously lower is better and if it's going to express fragility at the 50 Fib by breaking through that level precipitously, well, then, I don't want to pull the trigger there ... . Another one to set an alert on for 51, at which time I'll check the chart to see what's goin' on ... .

Sidenote: For EFA, you can actually get pretty decent money for just selling the 51 put (currently priced at 1.11 in the Aug monthly expiry) if you want to shoot for assignment at that price level ....

UNG -- COVERED CALL IDEATruth be told, I was burned somewhat by UNG this year, as I was expecting a seasonality bounce which has not come due to mild temperatures associated with El Nino. Moreover, in 20-20 hindsight, a debit spread was probably not the way to go due to inflexibility of the setup if you are just totally directionally wrong or if your timing as to the directionality is off.

In any event, and although volatility in the underlying has diminished somewhat since the making of a significant low around 7.00, there remains sufficient volatility in UNG to go covered call here.

The setup:

100 Shares UNG at 7.69

1 Feb 19 8 Short Call

Entire Package: 6.91 debit (meaning your break even for the setup is $6.91/share, excluding fees commissions)

Max Profit: $109 (if called away at $8)

Tips: Look to take off the entire setup in profit before expiry if profit approaches what you would get if called away. Roll out the short call to a later expiry if it is nearing worthless; look to roll to a strike that at least exceeds your cost basis in the underlying.

CHK COVERED CALLS (LONG NATGAS PLAY)Okay, so my long UNG play didn't work out; after I entered the trade, NGAS continued to tank -- horribly, as forecasts for a mild winter came to the forefront and natty gas reserves continued to build to record levels. Ugh.

Nevertheless, i still want a natty gas long play. CHK is the most beaten down price-wise of the top ten nat gas producers, so it makes for a potentially cheap covered call play that offers a little bit more flexibility in terms of "working off" an error in timing the entry.

So, I'm diving in here, with the full expectation that this could dive further, in which case I will continue to sell short calls against the long stock position:

100 Shares CHK at 4.47

Sell Feb 19 5 Short Call (.55 credit at the mid price)

$388 for a mid price fill (i.e., cost basis in the 100 long shares will be reduced to 3.88/share).

P COVERED CALL IDEABuy 100 Shares P @ 11.64

Sell 1 Feb 19th 12 Call

Entire Package: 10.36 debit (10.36/share)

Max Profit: $164/contract (if called away at 12/15.8% ROC)

USO COVERED CALL IDEAHaving waited a long time for West Texas Intermediate to hit 2009 levels, I figured I'd put my money where my mouth was and go long USO when it did.

I filled this one earlier today:

Bought 100 Shares USO @ 10.05

Sold 1 Feb 19th 11 Call

Total Package: 9.69 debit

Max Profit: $131 (if called away at 11)

You could probably get a slightly better fill than I did, as USO ended the day at 9.90 ... .

S -- COVERED CALL IDEAWith an implied volatility rank of 70, an implied of 63, and a 10%+ return for the nearest out of the money short call, S meets my criteria for a decent covered call play (plus the darn thing's so cheap).

Buy 100 Shares S at 3.85

Sell 1 Feb 19 4 short call

Entire Package: $358/contract

Max Profit: (If Called Away at 4) $42/contact

MRO -- COVERED CALL IDEAWith an implied volatility rank of 98 and an implied volatility of 79, MRO presents a good covered call opportunity here with a return on capital of greater than 10% if called away at the nearest short call strike (13).

Here's the setup (which, as always, may require tweaking after NY open, since these off hours quotes have a tendency to have wide bid/asks):

Buy 100 shares MRO at 12.59

Sell 1 Feb 19 13 short call

Entire Package 11.20/contract ($1120)

Max Profit: $180 (if called away at $13)

Notes: A word of caution is in order here with this one. The universe of downtrodden oil and gas plays is quite large and is growing (for obvious reasons). finance.yahoo.com This company -- along with a bunch of others in the sector and, in particular, those exposed to oil/shale sands operations (this one is) -- may continue to trundle into the dirt. Moreover, earnings is right around the corner (on 2/17) and they, in all likelihood, are going to continue to disappoint. Their last profitable earnings quarter was for the period ending 8/20/14 and the only bright spot has been that, for the last couple of earnings, earnings did not disappoint as much as expected ... .

CHEAPER WAYS TO PLAY GOLD -- GDXJ/GDXFor the longest time, my go-to to play gold is GLD, which is intended to emulate the price of gold bullion. However, this can tie up a disproportionate percentage of buying power due to the price of the underlying.

Naturally, there are alternatives out there to GLD that are either ETF's (like GDXJ and GDX) or outright securities in companies that acquire, develop, and operate precious metals properties (e.g., AUY, GG, AEM, KGC, ABX). Although some of the individual names are better than others, they all seem to be struggling to varying degrees in this market, and it is possible that some of them will not survive bullion's downturn from the atmospheric highs gold experienced in late 2011. Because of this possibility, I would opt going for an ETF over an individual name in this sector to reduce the risk that taking a position in an individual name entails (i.e., total implosion; AUY comes to mind).

Neither a GDX short strangle nor a short straddle will yield much premium here. Selling a naked short put at the edge of the expected move to the downside in the underlying (around the 12.5 strike for the Feb 12th weekly) will yield about $30 in premium/contract; not that great a figure after fees and commissions are considered. Additionally, doing a covered call here isn't quite up to my standards, since a Feb 19 covered call setup with a short call at 14 would only yield a max profit of $99 if called away with a $13.01 per share cost basis ($99/$1301 < 10% ROC).

The best thing to do is probably wait for higher volatility in the underlying to make a play (it's below the 50th percentile right now for the past 52 weeks), since this will make premium richer for a covered call setup. Right now, then, good for the watchlist as an alternative to a GLD trade going forward ... .

AA -- WATCH FOR VOLATILITY POP AROUND EARNINGSI have not played AA for it seems like eons. This is because my go-to, premium selling play for earnings is the short strangle, and you won't get sufficient premium out of a low priced underlying like AA via short strangle for the life of you. The other option, naturally, is a short straddle , but even then it's a slog to squeeze sufficient premium out of the setup to make it worthwhile.

However, given where AA is at in its trajectory (another beaten down commodity/basic materials play), it's literally begging for a covered call at some point. But those are best put on when volatility in the underlying is high, since volatility enrichens premium in the short call of the setup and reduces your cost basis to a greater degree. Consequently, what I'm watching for is a volatility pop around earnings such that doing a covered call with a short strike slightly above current price is worthwhile (a dip like we had last post-earnings would also be helpful).

It's frankly not horrible right now, but I generally look to put these on when implied volatility rank is above 70 and the setup will yield 10% return on capital if called away at the short call price of the setup. A 100 @ 9.87/Feb 19th 10 short call will cost 9.13 to put on with a max profit of .87. Could be better, naturally.