AFRM Short 2/28 - 3/10Short on AFRM on 2/28.

Sold Call Credit Spread $13.5/$14 with expiration 3/10.

Target 1: 13.31

Target 2: 12.88

Considering closing and/or rolling if price rises above $14 OR is loss 50% or greater.

Close for profit at 70-85% profit.

Creditspread

CMCSA Hitting Resistance?Sensing that the overall market is turning down after trying to hold above the 200 day moving average, one stock I had considered purchasing at a lower price is Comcast. Entered into Feb 17 45-40 call credit spread @ 0.63. The opening price surge could quickly reverse as the 200 day moving average may be too much to overcome for many stocks.

YUM Brands at PCZ of Bearish CypherWe have Bearish Divergence at a Bearish Cypher PCZ and right now the calls are super expensive so i will be buying some slightly OTM FEB Calls and selling some deep ITM APR Calls for a net credit. My main target is $115 but much lower is probable.

MDT: Ascending Broadening Wedge Targeting $24I have sold the $60 and $65 strike FEB 17th calls and bought the $75 JAN 20 Calls for a net credit and i am looking for MDT to pullback to atleast $55 in the next several weeks and it's overall target in time should even be well under $20 but i suspect we will get some bounces at $55 and $24 along the way.

IWM LOTTO PLAY > Call Vertical Spread

Taking a small Long here with Vertical Spread , playing for this bounce FOMC Trade .

MGM bull put spreadIF this trade does not work, one Real life trader will get a weekend at the MGM on me

;-)

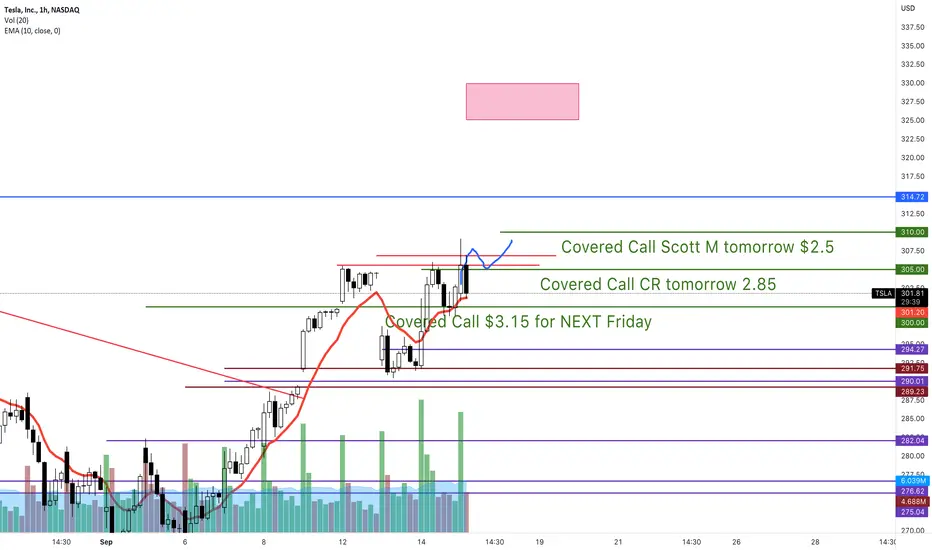

BEAR CALL SPREAD ON TSLA Likely will get into a bull put spread soon as well

$1.00 limit credit

Will only be concerned with a close above $315

US Economic Outlook ___ update (Spectral Analysis: SPX) Continued Thoughts & Ideas from previous post:

Accessing the Risks of US recession

~ Credit & Growth Concerns

~ FED will not Put

~ Equity Revaluations

"Bubbles" that have already bust

~ Used cars

~ Precious Metals.

~ Equities, Yields, Bonds

~ Crypto

"Bubbles" pending...

~ Housing

~ Agriculture

~ Credit

~ Unemployment

AVGO bull put spreadBelow the 200 SMA on daily. AVGO has had pretty decent strength for a bit. Not expecting it to TANK in 2 weeks.

AMD bull put spreadGood premium. 2 1/2 weeks. Let's see if THETA helps us OR if any bulls come into AMD to cause this bad boy to bounce. Protection level will happen with a close below the 100 SMA.

Credit Monitoring Basics: A Must Have SkillThese data series are all available in the Trading View platform.

Since the turn of the year the price of LQD, the investment grade corporate credit ETF, has declined nearly 10 points (-7.3%) and since early August is down 13 points (-10%). The important question is…. Why?

Knowing how to monitor credit is an important skill, particularly since so many in the commentary or advice business so misunderstand it. In this post I want to provide basic tools that will allow you to perform a down and dirty evaluation.

Why is credit so important? The Federal Reserve is much more sensitive to credit distress than they are to equity distress. If companies are unable to secure funding, they may face liquidity problems, and liquidity problems have the potential to become systemic. In 2008 and again in 2020 credit markets were, in essence, frozen. Particularly in 2008, even short term funding markets froze. There were plenty of offers but in many cases no bids. Being an old bond guy, I may be prejudiced, but credit makes the economy go and in general terms is much more important to short term functionality than equity. I think the Fed is more responsive to credit market functionality than it is to equity distress.

Listening to the angst of the want-to-be macro analysts or simply looking at the price of credit ETFs like LQD or HYG might lead one to believe that credit was generating an economic warning or danger sign. That narrative is, at least for now, false.

Corporate bond yield has two primarily components:

• Base rate: In the case of fixed coupon corporates the base rate is the nearest maturity on-the-run (most actively traded) U.S. Treasury (TR). The base rate is generally thought of as the risk free rate.

• Spread to the base rate: The spread above the base rate compensates credit investors for the higher risk of default and downgrade and the wider bid-offer (liquidity) spreads involved in corporate trading.

• For instance: 10 year Treasuries yield 2.00% and a ten year XYZ corporate security is offered at 120 basis points (bps) to TR. All-in-yield for XYZ is 3.20%.

Because there are two primary constituents of a corporate yield, price change can be driven by two things.

• Changes in the base rate. In other words, changes in treasury yields.

• Changes in the credit spread. Spreads widen/narrow to the base rate as investors seek additional/less compensation for default, liquidity and downgrade risk.

Normally the primary driver of changes in corporate ETFs and indices is change in the base rate/treasury yields. Said another way, TR yields are more volatile than corporate spreads.

• Big changes in Treasuries equate to big changes in corporate bond prices.

Chart 1: This is a long term chart of IEF (7-10 year Treasury ETF) plotted with LQD (the investment grade bond ETF).

• You can see how closely the two correlate.

• There will be some difference due to differences in duration (a measure of rate sensitivity) of the index versus the duration of the Treasury and changes in the spread component.

• But, clearly, changes in Treasury rates have an outsized influence on corporate bond rates/prices.

Chart 2: Option adjusted spread of the ICE BofA Investment Grade (IG) and High Yield (HY) Corporate Index's:

• The OAS offers a way to assess the credit spread component of a corporate bonds yield.

• Investment grade index is +1.08% to the base rate.

• High yield spread is +3.44% to the base rate.

○ There is more default risk in high yield, so the compensation, or spread to the base rate, is correspondingly higher than that of IG.

• Both IG and HY spreads remain very near historic lows with very little evidence that credit investors are growing fearful of default, downgrade, or liquidity risk.

Chart 3: All in yield BBB corporate index (top), BBB OAS or credit spread (center) and ten year treasury note yields (bottom).

• The all-in-yield, of the ICE BofA BBB index has risen significantly over the last few months.

○ Remember that in a bond, higher yields equate to lower prices. So a higher all-in-yield means that corporate bond prices are lower.

• BBBs are the lowest rating category of the Investment grade index and are more sensitive to the ebb and flow of default and downgrade risk than the investment grade index as a whole.

• While the all-in-yield has risen sharply over the last few months the OAS has barely budged from support.

Investors are not yet demanding more compensation for default risk. The change in corporate pricing has been driven by the sharp rise in rates.

Bottom Line: To understand the state of the credit market, you have to assess both changes in rate and changes in the spread. Hopefully you now have the tools to do a down and dirty assessment of your own.

Good Trading:

Stewart Taylor, CMT

Chartered Market Technician

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

XLE 55/53 Put Credit SpreadOpened for a 0.25 Credit

XLE is making a strong move upwards, this filled on the afternoon pullback. If this pulls back in the next few days I will add the call side to turn this into a IC. This will provide me delta neutrality and allow me to play the range from 55-60.

210/208 IWM Put Credit SpreadIWM is one of my favourites due to its range in the last year. I have played this range many times with credit spreads and Condors.

Trade setup:

Simple Put Credit Spread here opened for a 0.205 credit. Goal with these trades is to be a minimum of 10% RoM and no longer than 30 days.

Entry Criteria:

1. Red day, for increased premiums

2. Trading within a range (clear)

3. Short put is far enough away (see multiple support points lower)

4. Credit received meets RoM (Return on Margin) criteria.

$NVDA Key Levels & Analysis + Feb 18 Credit Spread$NVDA Key Levels & Analysis + Feb 18 Credit Spread

From a technical standpoint NVDA looks like it could go either way, but my directional bias here is down…

Feb 18 245 puts looking good…

——————

I usually trade both ways, but lately I’ve been focusing more to the downside because of how high the market is. It makes more sense to sell puts right now, and I’m usually at Target 2.

——————

I am not your financial advisor, but I will happily answer questions and analyze to the best of my ability but ultimately the risk is on you. Check out my ideas, but also do your own due diligence.

I am not a bull. I am not a bear. I just see what I see in the charts and I don’t pay too much attention to the noise in the news.

Very often you have to look at my charts from the perspective of where I’m looking to sell puts. But I also do open positions still once in a while.

If you want me to analyze any stock or ETF just leave me a comment and I’ll do it if I can.

Have fun, y’all!!

(\_/)

( •_•)

/ >🚀

$QQQ Credit Spread Jan 7 $QQQ Credit Spread Jan 7

Looking to Sell Feb 18 348 put when VIX spikes

——————

I usually trade both ways, but lately I’ve been focusing more to the downside because of how high the market is. It makes more sense to sell puts right now, and I’m usually at Target 2.

——————

I am not your financial advisor, but I will happily answer questions and analyze to the best of my ability but ultimately the risk is on you. Check out my ideas, but also do your own due diligence.

I am not a bull. I am not a bear. I just see what I see in the charts and I don’t pay too much attention to the noise in the news.

Very often you have to look at my charts from the perspective of where I’m looking to sell puts. But I also do open positions still once in a while.

If you want me to analyze any stock or ETF just leave me a comment and I’ll do it if I can.

Have fun, y’all!!

(\_/)

( •_•)

/ >🚀

$MSFT iron condor for 33% profit, 83% PoP #tradingHigh IVR, I'm not leaving money on the table.

Max profit: $250

Probability of 50%Profit: 83%

Profit Target relative to my Buying Power: 33%

Max loss with my risk management: ~$200

Req. Buy Power: $755 (max loss without management before expiry, no way to let this happen!)

Tasty IVR: 80 (ultra high for Microsoft)

Expiry: 50 days

SETUP: IC for $MSFT, because IVR ultra high, collecting 2.5cr

* Buy 1 MSFT Jan21' 290 Put

* Sell 1 MSFT Jan21' 300 Put

* Sell 1 MSFT Jan21' 360 Call

* Buy 1 MSFT Jan21' 370 Call

SAFETY ZONES: : Prev. resistance could act as support at ~$306, prev.ATH could act as resistance at $338.

Stop/my risk management : Closing immediately if daily candle is closing out of the the box, max loss in my calculations in this case could be ~$200.

Take profit strategy: 50% of max.profit in this case with auto buy order at 1.25db

Of course I'll not wait until expiry in any case!

If you liked this article, check my other ideas.

Anyway: HIT THE LIKE BUTTON BELOW , and for fresh option ideas FOLLOW ME( @mrAnonymCrypto ) on tradingview !

$AAPL Credit Spreads$AAPL Credit Spread

Target 1 - 173… feels a little too close to me, but if you’re feeling wild, Jan 7 173 puts might work…

I’m selling Jan 21 160 puts/ Jan 7 185 calls

GL

——————

I usually trade both ways, but lately I’ve been focusing more to the downside because of how high the market is. It makes more sense to sell puts right now, and I’m usually at Target 2.

——————

I am not your financial advisor, but I will happily answer questions and analyze to the best of my ability but ultimately the risk is on you. Check out my ideas, but also do your own due diligence.

I am not a bull. I am not a bear. I just see what I see in the charts and I don’t pay too much attention to the noise in the news.

Very often you have to look at my charts from the perspective of where I’m looking to sell puts. But I also do open positions still once in a while.

If you want me to analyze any stock or ETF just leave me a comment and I’ll do it if I can.

Have fun, y’all!!

(\_/)

( •_•)

/ >🚀

$SPY Credit Spread Jan 5th$SPY Credit Spread Jan 5th

And also a little further out at 30 days… and 53 days out

Sell further out targets when VIX spikes 15%+

GL

——————

I usually trade both ways, but lately I’ve been focusing more to the downside because of how high the market is. It makes more sense to sell puts right now, and I’m usually at Target 2.

——————

I am not your financial advisor, but I will happily answer questions and analyze to the best of my ability but ultimately the risk is on you. Check out my ideas, but also do your own due diligence.

I am not a bull. I am not a bear. I just see what I see in the charts and I don’t pay too much attention to the noise in the news.

Very often you have to look at my charts from the perspective of where I’m looking to sell puts. But I also do open positions still once in a while.

If you want me to analyze any stock or ETF just leave me a comment and I’ll do it if I can.

Have fun, y’all!!

(\_/)

( •_•)

/ >🚀

PYPL Weely Options PlayDescription

PYPL moving up into the gap that was created following the earnings release. Not all gaps will be filled, but they give a good clue as to how supply and demand will play out.

I would typically put on a call credit spread for a long position, but this low volatility, lethaly-injected environment lends to being a seller of options.

I am also "hedged" with plenty of long options in case anything goes haywire.

Put Credit Spread

By Expiration

Max loss occurs at any strike under the long put (207.5)

Max gain occurs at any strike over the short put (210)

SL < 210

*Stops based off underlying stock price, not mark to market loss

The Trade

BUY

11/19 207.5P

SELL

11/19 210P

R/R & Breakevens vary on fill.

Looking to make 26% return on collateral by EOW.

The short put is placed under the opening bar following the post-earnings gap

The long call is placed 2.5 points away IAW collateral requirements, risk tolerance, and R/R.

Manage Risk

Only invest what you are willing to lose

TSLA Weekly Options PlayDescription

TSLA has to stop at some point, right? Risk here is limited by time, 1 DTE to make a couple points.

Call Credit Spread

Levels on Chart

SL > 1250

*Stops based off underlying stock price, not mark to market loss

The Trade

BUY

11/05 1260C

SELL

11/05 1250C

R/R & Breakevens vary on fill, super tight trade though, risking 1000 to make ~200-300.

The short call is placed close to the money for higher profit.

The long call is placed 10 points away based off of collateral requirements and risk tolerance.

Manage Risk

Only invest what you are willing to lose

NVAX next weekly support with low rsi

what a perfect gap down with low rsi. I am buying extra time for this to work for us. I am loving the low rsi and this gap down on it today.

$DKNG Weekly Opened 48/47P credit spreads on DKNG for December. Approaching demand zone and looking for the bulls to step in these coming weeks similar to mid july's price action.

Asia Corp - Emerging Market Corporate Spread Asia Corporate spreads have been widening vs. Emerging Market Corporate OAS at the highest level since 1999. Any bounce in Asia must be led by Credit which is missing