Balla is still Bullish on BITCOIN. Cup & Handle pattern. The trend is still our friend.

I still see bullish developments in the price action.

We must have patience.

Dips still must be bought.

The plan hasn't changed.

We still aiming for that time period of 9 -15 months post #BTC Halving.

We are only one month down :)

Cupandhandlepattern

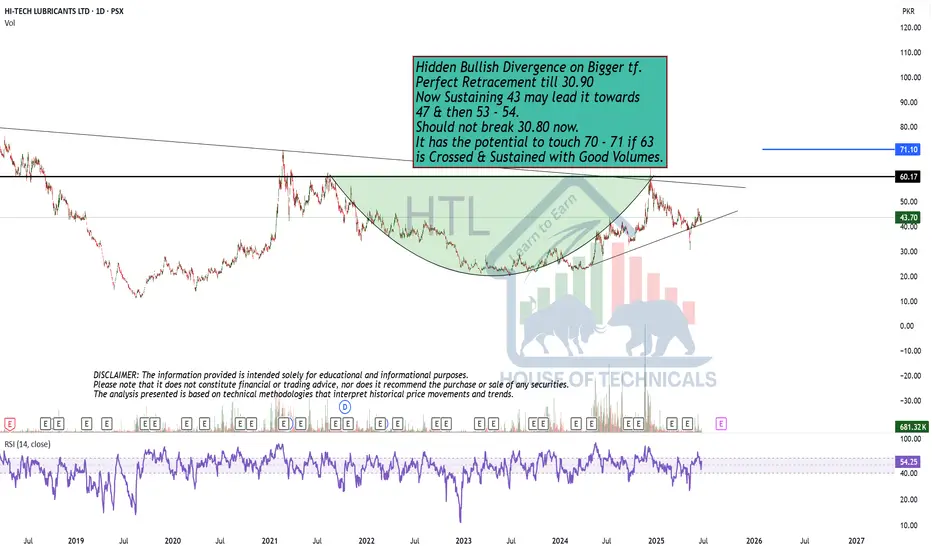

Perfect Retracement till 30.90Hidden Bullish Divergence on Bigger tf.

Perfect Retracement till 30.90

Now Sustaining 43 may lead it towards

47 & then 53 - 54.

Should not break 30.80 now.

It has the potential to touch 70 - 71 if 63

is Crossed & Sustained with Good Volumes.

Cup and handleAfter many months, we now have a cup and handle formation. Regardless of Michael Saylor's constant buying, we have a bull flag in play that takes us to $491 USD.

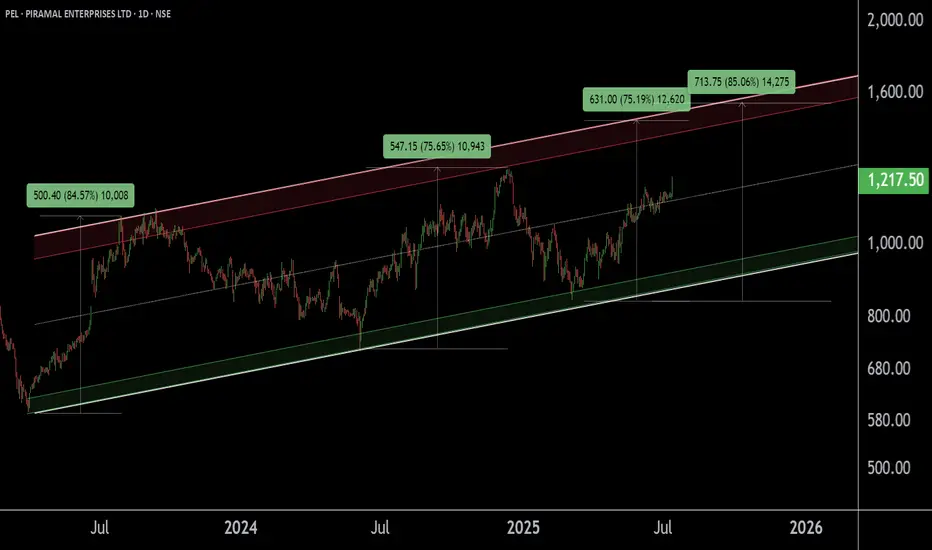

PEL !! PIRAMAL ENTERPRISES LTD appear to be in a Breakout phase This is the Daily Chart of PIRAMAL ENTERPRISES LTD.

PEL is trading above the midline of its ascending parallel channel, with strong support in the ₹1080–₹1150 zone. Historically, whenever it sustains above the midline, it tends to retest the upper boundary resistance of the channel near at 1500 -1540.

If this level is sustain then we may see higher prices in PEL.

Thank You !!

Transrail Lighting with beautiful Cup and handle pattern Have a SIP in this Cup of coffee. Looks good for Short /Longterm.

Enjoy it

EID PARRY - TASTE THE 2ND CUP OF COFFEE Second Cup and handle pattern is ready. Taste the sweetness of it.

ETH | Bullish Pattern - Cup and Handle +15%A Bullish pattern is appearing on the Ethereum chart.

From a Cup and Handle pattern, we can easily expect atleast a 15% increase. This is true for the near term. A +15% would put us here:

Just under $3K we may see heavy resistance. This is also the neckline resistance, as it was the previous support for the breakout that ultimately led to a new ETH ATH.

_______________________________

BYBIT:ETHUSDT

KFINTECH Bullish Signals on Daily TimeframeKFINTECH is displaying multiple bullish signals with healthy volume on the daily timeframe. It is currently consolidating and may experience a slight dip, which could offer a good accumulation opportunity.

Stop loss: Your strategy

$IWM 4 hour cup and handleLooks like a cup and handle pattern formed with a retest of the neck line.

A break above $215.53 would confirm bullish momentum back in. A break and hold below the neckline would invalidate the pattern.

Happy hunting!

THELEELATHELEELA is giving resistance + cup and handle breakout above 414 level. Market participation has also increased in recent sessions. So if it sustains and closes above 414 then it looks very attractive and may start new momentum rally. 398 seems very good support. On upper side we may see momentum of 10-12%. Make sure that it sustain and closes above 414!

Cup and Handle with a shot of espresso: A bullish blendSince March, Starbucks ( NASDAQ:SBUX ) has been in a sustained downtrend, gradually rounding out a base. Now, the chart is showing early signs of a trend reversal.

Yesterday, price broke out of a bull flag formation on the daily chart and is now testing the $95.50 zone — a critical neckline level of a cup and handle pattern.

✅ Bullish Scenario:

A clean break and hold above $95.50 would confirm the cup-and-handle breakout.

If confirmed, this setup could target a measured move that eventually retests all-time highs.

More conservative traders may want to wait for a back test of the $95.50 neckline as confirmation, especially given its past historical significance.

⚠️ Bearish Invalidation:

A break and hold below $95.50 would invalidate the cup-and-handle pattern, suggesting the breakout has failed.

📌 This is a purely technical idea. No fundamentals involved.

As always, Happy Hunting!

This is not financial advice. Always do your own due diligence

Cup & Handle Formation.GFIL

Closed at 9.70 (30-06-2025)

Hidden Bullish Divergence on Bigger tf.

& Bullish Divergence on Daily tf.

If anyone wants to Take Fresh Entry, 6.30

should be the Stoploss.

Otherwise, wait for the Resistance (13.50) to

Cross & Sustain and then take Entry for

the Targets around 17 & then 23.

TITAN ' s Key Point | Breakout | Swing.This is the 4 hour Chart of the TITAN COMPANY.

Titan has formed a Cup and Handle pattern and given a breakout .

Two possible scenarios:

If the breakout sustains with volume, the rally may continue.

If it retests the breakout level, it would offer a safer entry before the next leg up.

If this level is sustain then we may see higher prices in Titan.

MSTRMSTR after looking above and failing in the attempt to test the highs it has been consolidating for a period of time and is show some signs of strength. If BTC can get a nice push above all time highs I believe you will see ATHs on MSTR.

COIN- Cup and Handle FormationThere is more to this, but the basic formation is here. Other systems seem to also support the formation (such as Gann, and Harmonics).

There are a few 6 month candles overlaid in the entry to this that I was creating- illustrating the 6 month gains to form the cup. The handle portion did catch me off guard as we are typically use to seeing a cup form at the initial correction, but this one seems to have formed inside of the down move (very interesting).

Lets see how it works out. If true- its 50% gain on the bone here.

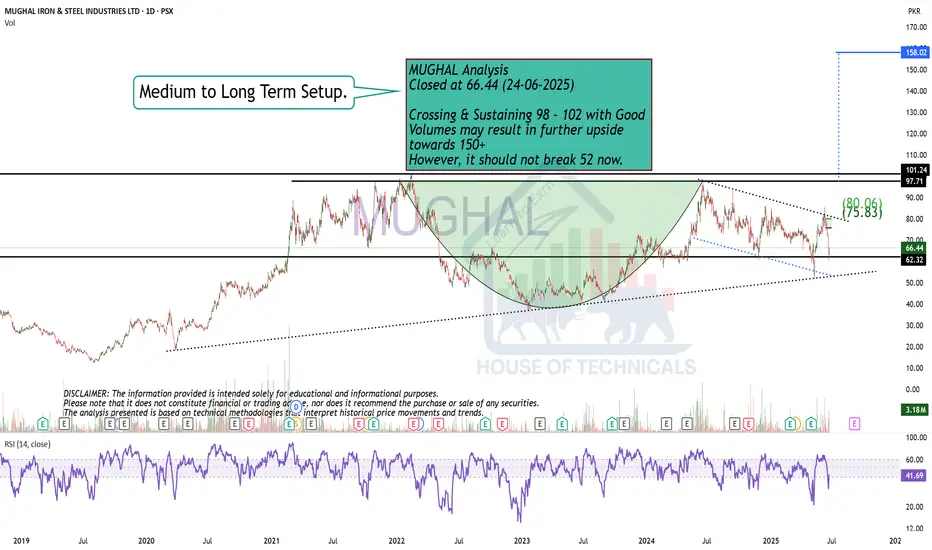

Cup & Handle FormationMUGHAL Analysis

Closed at 66.44 (24-06-2025)

Crossing & Sustaining 98 - 102 with Good

Volumes may result in further upside

towards 150+

However, it should not break 52 now.

HIMS 1D — This pattern didn’t cook for nothingOn the daily chart of Hims & Hers Health, we’re looking at a textbook cup with handle formation — not just a pattern, but a structure backed by time, volume, and classic price behavior. The base of the cup formed steadily from February to May 2025, and as soon as the curve was complete, price transitioned into a tight consolidation — the "handle" that often masks real accumulation.

Right now, price is testing the resistance area. And it’s not just floating up there — it’s coming in hot: price has already broken through EMA 20/50/100/200 and SMA 50/200. That’s a full stack flip. This isn’t sideways noise — it’s a structural shift in control.

Volume is starting to build as price rises, confirming that demand is real and institutional positioning likely active. We’re watching a breakout zone above the handle — and when that breaks, the structure unlocks with a clear target: $107.25, roughly a 2x move from current levels.

This setup isn’t noise. It’s a long-cooked formation that’s now about to boil over. If the handle holds and price breaks through — the rest is just follow-through.

BTC - Cup & Handle?BTC forming a cup and handle on the 1D chart which seems to be the main timeframe/narrative of play..

Bullish on All Time Frames.SSGC Closed at 44.24 (18-06-2025)

Bullish on All Time Frames.

Important Resistance Zone : 50 - 57

Important Support Zone : 35 - 41

Very Strong Bullish Patterns appearing

on Bigger Time frames.

Crossing 56 - 57 with Huge Volumes, may

result in further upside move of price

towards 80+

However, this time it should not break 24.

Cup & Handle Breakout - NAVINFLOURCurrent Price: ₹4,703

Technical Analysis:

Cup & Handle Breakout Pattern: The provided chart for NAVIN FLUORINE INT. LTD. shows a pattern that resembles a Cup & Handle. The current price action indicates it is at or near a potential breakout level.

Waiting for Confirmation: Your statement "Waiting for confirmation" is crucial. A confirmed breakout typically involves the price sustaining above the resistance level with strong trading volume.

Immediate Target: ₹7,000

Time Frame: 6 months to 1 year.

Fundamental Analysis:

Sales (Revenue from Operations): Consistently growing over the years, from ₹486 Cr in Mar 2014 to ₹2,349 Cr in Mar 2025.

Operating Profit: Shows a strong upward trend, from ₹66 Cr in Mar 2014 to ₹534 Cr in Mar 2025.

Net Profit: Also shows consistent growth, from ₹68 Cr in Mar 2014 to ₹289 Cr in Mar 2025.

EPS in Rs.: Increased from ₹13.47 in Mar 2014 to ₹58.19 in Mar 2025. This indicates healthy year-on-year growth in earnings.

Compounded Sales Growth: Healthy growth with 14% (TTM), 17% (3 Years), 17% (5 Years), and 15% (10 Years).

Compounded Profit Growth: Very strong growth with 25% (TTM), -7% (3 Years), and 20% (10 Years). The negative 3-year profit growth needs to be investigated, as the net profit has consistently increased in the past 3 years (258 Cr in Mar 2022, 375 Cr in Mar 2023, 270 Cr in Mar 2024, 289 Cr in Mar 2025). This might be due to a specific high base year or non-recurring items impacting the compounded calculation for that period.

Return on Equity (ROE): Strong and consistent, with 12% (Last Year), 13% (3 Years), 14% (5 Years), and 16% (10 Years).

Dividend Payout %: Consistent dividend payouts, with 21% in Mar 2025.

Stock P/E: While not provided in the specific image for Navin Fluorine's fundamental ratios, based on the current price of ₹4703 and FY25 EPS of ₹58.19, the trailing P/E would be approximately 80.82. This is a very high P/E ratio, indicating significant growth expectations are priced into the stock.

Corporate Actions & Latest News:

Dividends: The company has a consistent history of paying dividends.

Capacity Expansion/R&D: As a specialty chemicals and fluorochemicals company, corporate actions and news for Navin Fluorine often revolve around:

New project announcements or capacity expansions to meet growing demand.

R&D initiatives for new products or applications.

Strategic partnerships or collaborations.

Client wins in niche chemical segments.

Q4 FY25 Results: The latest news would include the Q4 FY25 financial results, which show a Net Profit of ₹289 Cr.

Company Order Book:

For a specialty chemicals company like Navin Fluorine, the "order book" typically includes long-term contracts with key clients and new project wins. A growing sales trend suggests a healthy order pipeline.

Overall Assessment:

Navin Fluorine International Ltd. presents a fundamentally strong picture with consistent growth in sales and net profit, along with robust profitability ratios like ROE. This strong fundamental performance supports the company's premium valuation.

The Cup & Handle breakout pattern is a bullish technical indicator. If confirmed with strong volume, it could potentially lead to the stock moving towards higher levels.

Key Considerations:

High Valuation: The calculated P/E of approximately 80.82 is very high. This means the market is already pricing in substantial future growth. The company needs to continue delivering exceptional results to justify and sustain this valuation.

Confirmation of Breakout: It's crucial to wait for proper confirmation of the Cup & Handle breakout with strong volume to validate the technical signal.

Profit Growth Anomaly: Investigate the negative "Compounded Profit Growth" for 3 years, despite the increasing net profit trend shown in the table. This might be a calculation anomaly or specific high-base effect.

Given the strong underlying business, consistent growth in key financial metrics, and the bullish technical pattern, the immediate target of ₹7,000, while ambitious, could be plausible within the 6-month to 1-year timeframe, provided the technical breakout is confirmed and the company continues its strong fundamental performance.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Investing in stocks, especially those with high valuations, carries inherent risks. Always conduct your own thorough research, carefully analyze the stock chart, assess your risk tolerance, and consult with a qualified financial advisor before making any investment decisions. The stock market carries inherent risks.