Stocks went from pump to dump, what's in store?#stocks went from basing & curling higher to topping and rolling over.

DJ:DJI had 5 green candle days. It turned to 3 red days.

TVC:NDQ bounced nicely but it reversed the hardest and FAST.

CBOE:SPX is in between both indices,

CBOE:VIX had a GOOD day.

WARNING!!! The more it hangs around here the MORE DANGER equities are in.

Have a great week!!!

D-DJI

$DJI - Rising Trend Channel [MID-TERM]💡 Pattern: Cup & Handle

💡 RSI: Neutral

💡 Risk: Low

✅ Resistance: 34200

✅ Support: 32800

PERFORMANCE

🔴 ST: NEGATIVE

🔴 MT: NEGATIVE

🟡 LT: HOLD

*ST: Short-term | MT: Mid-term | LT: Long-term

Verify it first and believe later.

WavePoint ❤️

DOW JONES is in an expansion Cycle and people still shorting it!Dow Jones on the 3M chart gives you the clearest picture you can get.

Every 10-15 years it consolidates inside a Megaphone (fundamental reasons like war, recession etc) and then an expansion phase follows.

In the 90s this expansion phase was extended due to the uprecedented boom of Dotcom.

While the index is on its expansion phase, the RSI trades inside a Falling Wedge, which warns of the loss in bullish strength and eventually leads to the new Megaphone.

Right now it is obvious that we are in an expansion phase. Needless to say it will last for as long as the MA50 holds.

The real question is will it be short like in the 1950s or extended like in mid 1980s-90s?

Follow us, like the idea and leave a comment below!!

DOW JONES May be starting a new Bull rally under our nose..Dow Jones (DJI) is printing on its RSI on the 1W time-frame an astonishingly symmetric Higher Lows pattern as 2015/ 2016. As with today, the price was within a Rising Wedge at the time, making a fake-out bearish break but still was emphatically supported by the lower Bollinger. In fact the Bollinger Bands have been instrumental in containing the price action.

It we are indeed (based on the 1W RSI) on a bottom similar to October 31 2016, then a very aggressive Bull rally is about to begin. And as always the majority isn't taking notice.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

DOW JONES Small pull back on the cards.Dow Jones hit the 1day MA200 yesterday and failed to close over it.

As a result, the price got rejected and started pulling back today.

Based on the 1day RSI, we could be in a minor corrective candle similar to March 22nd, which found Support between the 0.618-0.786 Fibonacci range.

Buy on the 0.618 Fibonacci and target 35000 (Resistance A).

Previous chart:

Follow us, like the idea and leave a comment below!!

DOW JONES: This is only the beginning of the recovery.Dow Jones touched yesterday the 1D MA100 and with it turned the 1D technical outlook neutral (RSI = 47.338, MACD = -251.570, ADX = 41.460). As presented last time (see idea link at the bottom) the rebound level was the bottom of the Channel Up and now that is confirmed as the 1D MACD formed a Bullish Cross.

Much like the bearish wave of February-March, the 1D MA50-100 Bearish Cross signifies the bottom and the beginning of a new long term rally. Since the drop has been remarkably similar (both -6.46%) it is possible that the rise will be proportional too (+7.18%). This will be a little over the R1 level (TP = 35,100).

Prior idea:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

Hellena | DJI (4H): Long to 38.2% Fibonacci level 33888.Dear colleagues, I believe that wave 4 is complete. I expect that wave 5 will go minimum to 38.2% Fibonacci level 33888. Updating the minimum and reaching the Invalidation level will mean canceling the scenario, because wave 4 cannot update the minimum of wave 2.

Manage your capital correctly and competently! Only enter trades based on reliable patterns!

DOW JONES has considerable upside potential targeting 34850.Dow Jones touched the MA200 (1d) today after bouncing off the bottom of the Channel Up.

This is a standard V shaped reversal, much like the one in March.

Trading Plan:

1. Buy on the next MA200 (1d) break out.

Targets:

1. 34850 (Falling Resistance contact in similar fashion with April 14th).

Tips:

1. When the RSI (1d) is rebounding after being oversold, which is what took place on the March 13th Low. The two patterns are identical, this is why we expect the same target symmetry as then.

Please like, follow and comment!!

Notes:

Past trading plan:

Dow Jones 10/10 MoveDow Jones - DJI

Description :

Bullish Channel as an Corrective Pattern in Short Time Frame and it has Breakout the Lower Trend Line , It will Complete its Retracement at Previous Strong Support or till its Lower Trend Line at Fibonacci Level - 61.80% / 78.60%

Entry Precautions :

Wait until it Rejects with Strong Bearish Price Action

$SPX almost like clockwork to 2022TVC:NDQ has traded back above the NECKLINE (from Head & Shoulders Break down) - Amazing!!!

DJ:DJI has not traded above and neither has the $SPX.

In this chart we see the SP:SPX illustrating the resemblance to 2022.

We've been showing this chart for some time now.

It's amazing how similar they are trading.

AMEX:TYD is running today (leveraged bonds ETF) likely an anticipated demand for "safety" causing #yields to fall.

SGX:SQQ NASDAQ:TQQQ NASDAQ:SQQQ

AMEX:DIA AMEX:UDOW AMEX:SDOW

AMEX:SPY AMEX:SPXL AMEX:SPXS

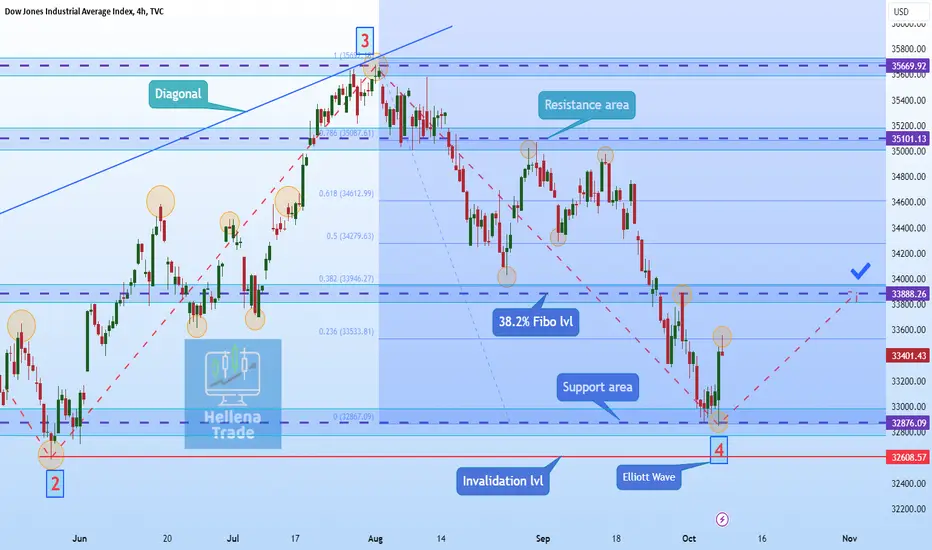

Hellena | DJI (4H): Long to sresistance area 33587.Dear colleagues, the price continued its downward movement. This means that wave 4 is stretching further than I thought. At the moment I assume that the price may reach the support area 32613.28. Then I expect growth and the beginning of the formation of wave 5. The nearest target is the resistance area 33587.94.

Manage your capital correctly and competently! Only enter trades based on reliable patterns!

Combined US Indexes bounce!Just noted that the combined equity index chart showed an interesting bullish setup.

The downtrend has been a little stronger than (probably) warranted, and now a sign is showing a probably bounce off a support level. Support broke and the next day rebounded to recover. This formed the bullish Piercing Line Pattern and it reclaimed the support that was broken only the previous day. Technical indicators are showing bullish divergence in alignment as well (green arrows).

Looks like time for a rebound. What happens next depends on how robust this bounce is, and if it forms a higher low, or just reverses to breakdown further again.

Heads up!

✅ Daily Market Analysis - FRIDAY OCTOBER 6, 2023Key events:

USA - Average Hourly Earnings (MoM) (Sep)

USA - Nonfarm Payrolls (Sep)

USA - Unemployment Rate (Sep)

US stocks faced a minor setback on Thursday, recovering from earlier session lows, as investors awaited the monthly jobs report to gain insights into potential future interest rate trends. The S&P 500 managed to maintain its position above the 200-day moving average, currently hovering around 4,206.

Although bond selling remained subdued on Friday, it may be short-lived. Tokyo's Nikkei index remained relatively stable, and currency markets followed suit, despite the persistent bond selloff's impact on the dollar.

During the Asian session, ten-year US Treasury yields remained unchanged at 4.72%. However, this comes after a five-week period of significant selloff in the bond markets, causing fluctuations in risk appetite among investors worldwide.

US10Y treasury yields daily chart

San Francisco Fed Bank President Mary Daly stated during an address at the Economic Club of New York that US monetary policy has shifted into a "restrictive" phase. Given the recent uptick in US Treasury yields, she suggested that there may not be a necessity for further interest rate hikes.

Investors are eagerly anticipating the commencement of third-quarter earnings reports later this month. S&P 500 companies are expected to reveal a 1.6% year-over-year increase in earnings for the quarter.

In terms of market performance, the Dow Jones Industrial Average dipped by 9.98 points, or 0.03%, while the S&P 500 experienced a 5.56-point decline, equivalent to 0.13%. The Nasdaq Composite also recorded a drop of 16.18 points, or 0.12%.

NASDAQ Index daily chart

S&P500 Index daily chart

DJI Index daily chart

Tesla, under the leadership of Elon Musk, has garnered attention by reducing the prices of its Model 3 and Model Y vehicles in the United States. The price cuts range from approximately 2.7% to 4.2%, as indicated on the company's website. This decision comes on the heels of a similar price reduction for its premium Model S and Model X cars, which occurred just a month ago.

Tesla's aggressive approach to price reductions in 2023 is a strategic move to address the challenges posed by a decelerating electric vehicle (EV) market and the escalating competition from both newcomers and established players. Notably, the standard Model 3 has witnessed a price decrease of approximately 17% since the beginning of the year, while the long-range variant of the Model Y experienced a reduction exceeding 26%.

Tesla stock daily chart

These price adjustments coincide with Tesla's plans to introduce a refreshed standard version of the Model 3 in the fourth quarter, which will come at a higher price point. The company recently reported third-quarter delivery figures that fell below expectations. This shortfall was attributed to production halts related to planned factory upgrades necessary for the new Model 3 version.

Despite this, the US labor market continues to demonstrate resilience, contributing to overall economic demand. This has raised the possibility of the Federal Reserve implementing further interest rate hikes before the year concludes. While many economists believe that the Fed has completed its rate hikes, it is expected to maintain a tight monetary policy for an extended period.

The Labor Department's employment report for September, highly anticipated by investors, is likely to reveal a moderate slowdown in job growth. However, it is also expected to show a decline in the unemployment rate from its recent high. Wage gains are anticipated to remain elevated, underscoring the ongoing strength of the labor market.

Some economists even suggest that the payroll numbers may surpass expectations. They point to a decrease in first-time unemployment benefit applications in September and a more favorable seasonal adjustment factor as indicators of a potentially robust report.

Despite market fluctuations, the US labor market continues to be a driving force in sustaining the economy. Third-quarter growth estimates have reached as high as a 4.9% annualized pace, well above the level that the Fed considers non-inflationary.

While the prospect of another round of bond selling could extend the dollar's winning streak, especially against the euro, the yen has displayed some resilience amid speculation of potential intervention by monetary authorities.

US Dollar Currency Index daily chart

The dollar index has recorded 12 consecutive weeks of gains, maintaining its strength. During this period, the euro has remained near an 11-month low, while the British pound has hovered close to a seven-month low.

Despite a sudden yen jump during London trading hours earlier in the week, Japanese authorities have denied intervening in currency markets. This has left traders cautious and uncertain about the potential for further market interventions or currency fluctuations.

USD/JPY daily chart

The yen is currently stable, trading at 148.5 per dollar. Gold, on the other hand, has experienced nine consecutive days of losses due to rising bond yields but is currently holding steady at $1,820 per ounce.

XAU/USD daily chart

DOW JONES Channel Up Double Bottom. Solid buy entry either way.Dow Jones (DJI) is rising following a vastly oversold 1D RSI reading (reached even 23.60) at the bottom of the (blue) Channel Up. Based on the RSI pattern itself, we can draw comparisons with the December 2022 - March 2023 correction. According to that the 1D RSI has one more Low to make before it bottoms and that bottom will be leg (e). This will justify the emergence of a diverging Channel Up (dotted), where leg (e) will be its Higher Low while also completing a symmetrical -9.30% decline from the top.

Still, the price has dipped well below the 1D MA200 (orange trend-line), which was March's bottom formation, thus either entry is equally probable. As a result it is best to buy on both levels so that a low risk indeed opportunity won't be missed. Our target is 35000, which is the 0.786 Fibonacci retracement level as well as Resistance 1.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

$DXY topping short term?Good Morning!

Trying to get an idea of where #stocks may go. IMO bias is up BUT we cannot be deterred by biases, can we?

TVC:DXY

4Hr is showing weakness.

Circles = moving avg bear crossovers.

We see the quick drops BUT they RECUPERATE hours later.

The 2nd chart shows DAILY vs 4Hr.

Makes it easy to see how decent the drops are.

TVC:DJI TVC:NDQ SP:SPX

Do Stocks Now Pump Again?Traders,

With the dollar and VIX down, there are no surprises with our SPY chart showing a nice big green candle on the daily. The question remains though, will we stay in my channel and above the 200-day sma or will we continue to proceed down to the H&S target of 410? My best guess is that we'll remain in our channel. As postulated previously, the 200-day SMA along with the bottom of my channel may be all the support that is needed to guide us onward and upward. This along with more than 11 straight weeks of DXY strength (time for a break) means that the beginning of Uptober could start today. And look at that RSI helping us out as well! Wave #5 is still well intact.

Best,

Stew

Bear rallies the most furious, could be in one!Bear rallies tend to be the MOST FURIOUS!!!

Be careful but take ADVANTAGE!!!

SP:SPX upcoming resistance @ 3 areas:

4280

Moving avg is a little above that (weakest resistance imo).

MAJOR = 4330 (it closes above this will post further levels).

Keep an eye as the RSI closes in on 50.

#stocks DJ:DJI TVC:NDQ TVC:RUT TVC:VIX TVC:DXY TVC:TNX #GOLD #SILVER

$DXY trading alongside $TNX & both divergent to Stocks Post #2TVC:DXY on left in all charts (only DJI shown here)

DJ:DJI & CBOE:SPX & TVC:TNX on right.

Short term we are badly due for some sort of relief rally, we nibbled in this area AMEX:UDOW AMEX:SPXL

Not sure how high this can go so we have been nibbling and will sell in tranches.

#stocks TVC:NDQ AMEX:DIA AMEX:SPY NASDAQ:QQQ

$DXY makes history (Update idea) Post #1Historically, the YELLOW support area NEVER holds when TVC:DXY is on its way back down.

HOWEVER, the US #Dollar is showing strength. (this is vs a basket of currencies that are also weak.) 1st time it bounced back this hard.

This looks like it wants to keep going, longer term. We'll see.

This is NOT good for #stocks (longer term).

TVC:TNX has been trading closely.

UPDATE: Dow hit target 1 - heading to target 2 at 32622The dow broke below the Symmetrical Triangle and it was beautiful text book style.

We set the first target at the bottom of the pattern at 33,607.

Now that the momentum is still negative, we can expect it to head to the next target at 32,622.

The signs are all bearish and this is one of those hold and adjust stop loss if need be.

Dow JonesDJI Chart

Checking some TA, which I should have done more thoroughly on SPY, I would have seen the obvious TA screaming we go higher.

Both the SPY and DJI technicals are stating we go higher. RSI, MACD, MFI, and 50MA are pointing to higher moves in the market. In fact, taking a look at the 10YR is another confirmation of where we're heading.