DOW moves to all time high of 37kBad news aside, IYT is what pushes the DOW to 37k. IYT got pummeled back in June losing alot of ground. Airlines and Railroads have finally found their footing, basing, and slowly climbing up this past week. IYT to 300 soon!

DAL

WATCHING $DAL for ENTRY TARGET @ 42.98 WATCHING $DAL for ENTRY TARGET @ 42.98

I’m practicing to really nail my entries better… if it hits 42.98 I'll play.

AAL - Airlines recovery, BUY opportunityWe can see a nice wedge breakouts on rising volume in airlines.

Fundamentally, we should take into a consideration deffered demand on trips due to COVID restrictions. Combined with Technical Analysis it means that airlines have space to growth.

I am publishing this idea a bit later then I should, but still it is a great buy opportunity.

Keep in mind your possible risks. Probably AAL will give a chance to take a large position on retest (level 22.30). Stop Loss 21.00

$JETS - Recovery of the Airline Industry“The U.S. Global Jets ETF $JETS provides investors access to the global airline industry, including airline operators and manufacturers from all over the world.”

TECHNICALS

$JETS is currently trading at $25.50 which is 13% below their most recent high of $28.98 which was made in March 2021. The stock has been in an upward trend since October 2020 as a result of increased vaccinations around the world and strong guidance. As seen on the chart, between 2017 and early 2020 $JETS established a strong support zone between $27.50 and $28.50. With travel expected to increase into the summer and vaccinations continue to be rolled out, $JETS can potentially see a 10% move and settle between $27.50 and $28.50 in the coming months.

RECOVERY

Based on their most recent earnings reports, airline companies such as $AAL, $DAL, $LUV, and $UAL have all posted that their revenue is up 100% or more from their pandemic lows. Although revenue is sitting around 50% of pre-pandemic levels, the growing number suggests that the industry is recovering.

RISKS

The greatest risk to the travel industry at the moment is the massive increase in covid cases in India and the emergence of the new covid variant B.1.617. Although much more information is needed, the new variant appears to be spreading at a much faster rate than before and it is unknown if vaccines will help prevent the contraction of the virus.

Anthony, OptionsSwing Analyst

Airlines lagged as Dow Transports move upFEDEX and UPS have moved up alot in recent days along with some other dow transports. Airlines have lagged behind with no bids. This week, look for Airlines to move out of oversold conditions to move Dow higher. News will break out as passengers return to flying domestically. Volume will pick up accordingly. Breach 46.70 with volume, look out 52!

DAL Keep ClimbingAirlines and other travel based companies definitely got hit the hardest from covid and are still slowly recovering where as other stocks have already recovered and more.

First signaled $18 entry which was a 2013 start of the uptrend and is a monthly level support zone. aka very strong level

Next Best entry placed at $27.60

Target $30.54

Next Target $34.59

Eventual Target $51.41

please don't dump on me Ed Bastian i love delta good airline, my first choice for flying

DAL SwingDAL along with the rest of the travel sector is catching some big buyers as the economy is shifting to its reopening phase. Look for some strong movements along the next couple of weeks as the chart is preparing for a big move too. Sitting directly under the 20EMA and a perfect bounce off the 50 - the stock also caught many buyers yesterday exactly off of the resistance, which is also a sign of strength.

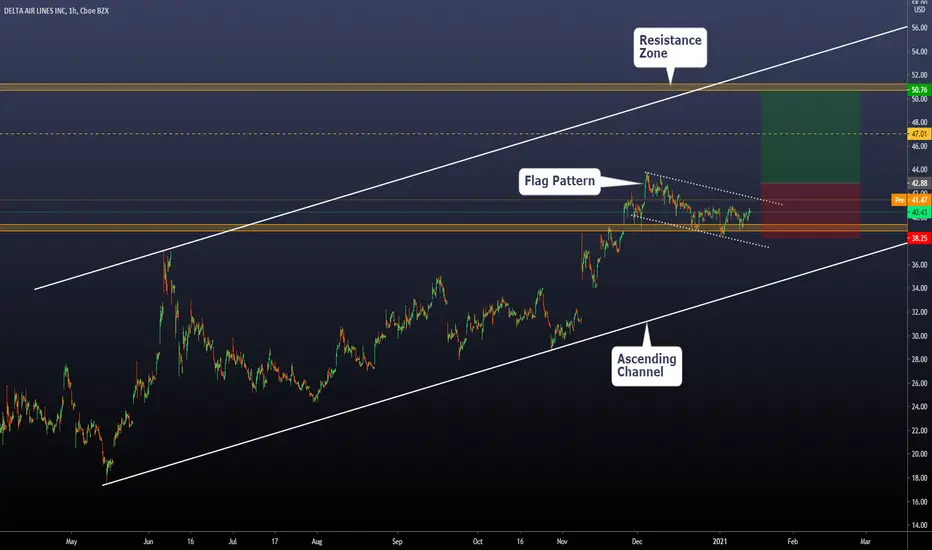

Flag Pattern on Delta Airlines - Bullish breakout expectedToday we will make a Daily and a 1h analysis on Delta + the setup we will take on this asset.

Daily Chart:

On the daily chart, we can see a Clear support zone and a resistance zone. The price is above the support zone, and we can project a bullish movement towards the next zone (Resistance)

On the 4hs chart, we will understand the setup:

Here we can see a Flag Pattern above the support zone.

Flag Patterns are considered continuation structures. That means that if we have a breakout of it, we can expect a continuation of the previous trend.

Our entry-level is a stop order at 42.88 / Stop level is at 38.25 / Break-even level is at 47.01 / Take profit at 50.76

The risk-reward ratio on this setup is 1.7, and we expect a resolution of 30 days.

If the price goes below the stop level without executing the setup, we will consider that the view is no longer valid.

Thanks for reading!

I am boarding the plane #stocksDelta has been hovering above its range for over a month now and I am looking for take into earnings. Assuming the breakout/trend to the upside will continue, I am hoping earnings will provide a catalyst for the stock to head toward 45. I don't think the numbers themselves will be good but I am hoping the have positive guidance about people traveling post the vaccine.

THE WEEK AHEAD: KBH, DAL, ICLN, SLV, EWZ, KRE, XLE, IWM/RUTEARNINGS:

There aren't a ton of earnings next week. Some financials are announcing, but I generally don't play those a ton for volatility contraction, since they never really frisk up that much, and all are below 50% 30-day implied here. KBH provides the best bang for your buck with the implied metrics I'm generally looking for (>50%), followed by DAL. Both, however, are at the low end of their 52-week range, in part due to the massive vol spike we experienced in March, which will make that metric somewhat misleading here.

KBH (18/56/14.5%),* Tuesday after market close.

DAL (7/53/12.9%), Wednesday before market open.

C (17/44/9.8%), Friday before market open.

JPM (14/32/7.8%), Friday before market open.

WFC (22/44/10.6%), Friday before market open.

EXCHANGE-TRADED FUNDS RANKED BY PERCENTAGE THE FEBRUARY 19TH AT-THE-MONEY SHORT STRADDLE IS PAYING AS A FUNCTION OF STOCK PRICE:

ICLN (14/79/20.0%)

SLV (31/48/11.3%)

EWZ (16/44/10.6%)

XLE (22/41/10.2%)

KRE (17/42/9.9%)

BROAD MARKET:

Pictured here is an IWM short put out in March at the strike paying at least 1% of the strike in credit. An IRA trade, I would look to roll up intraexpiry to lock in realized gain with >45 days 'til expiry, take profit on approaching worthless (<.20), and sell call against if assigned. Currently 67 days 'til expiry, it is understandably a bit long in duration, but I already have some on in the February monthly.

IWM (26/34/7.6%)

QQQ (21/31/6.9%)

DIA (14/24/5.2%)

SPY (11/24/5.0%)

EFA (14/21/4.7%)

* -- The first metric is the implied volatility rank or percentile (i.e., where implied is relative to where it's been over the past 52 weeks); the second, the 30-day implied volatility; and the third, what the at-the-money short straddle is paying as a function of the stock price.

DAL: Long now at 39, SL at close below 37, PTs - 45, 48, 51Broke out few weeks ago, consolidating, came down on lower volume. Ideal buy will be around 37, but can take a position now at 39 for a decent R/R

RCL and DAL BULLISH Recovery StocksSome price action this week got me very interested in stocks that were all the rage through the pandemic trading in 2020. NYSE:RCL is a trade I posted about yesterday that was up 4% on the day today. I like this price action to go more. NYSE:DAL is another stock in recovery that a friend had me look at and it has almost identical price action. He also took a LONG date option and I love it... he's getting PAID FOR PATIENCE!

Delta Air lines Inc. LONG📈 NYSE:DAL LONG H4

🛒BUY above = 31.43

🎯Target1 = 32.54

🎯Target2 = 33.23

🛑Trailing Stop loss = 29.62

❌Cancel trade and open reverse trade = 29.62

🙈Recommended risk = 1-2%

𝗧𝗿𝗮𝗻𝘀𝗽𝗼𝗿𝘁𝘀 𝗨𝗽𝗱𝗮𝘁𝗲: $DJT Weekly. False Breakout?Got the new highs, but a false breakout? If so, should revisit $10K or lower soon

$TRAN $IYT $FDX $AAL $UAL $DAL $LUV $EXPE $SPY $SPX $ES_F $VIX $DIA $DJI $YM_F #Stocks #Transports 🛫

DELTA AIR LINES INC. LONG📈 NYSE:DAL LONG H4

🛒BUY above = 33.30

🎯Target1 = 34.80

🎯Target2 = 35.70

🛑Stop loss or cancel trade = 30.90

🙈Recommended risk = (2%-3%)

Airlines Ticket to ride, pick your pricepointIt is ovious that this sector is heating up. Loads of bodies of their books, delincuent uncolectable debt. costly SLA fines waved, and cancelled plane orders with no penalties, on top of it loads of stimulous coming their way. The institutional buyers are shameleslly creating this pattern and its about to break. Lets take AAL as an example" Could it consolidate before it jump? Yes, but the top of the corridor is around the 15 dollar area so the run up its likely. I would enter this trades with tight stops, no point on giving away money, and a core position with a wider stop. The corridor goes from 11ish to 15iah, once it breaks its gonna be very very bullish. The hole point of this post is to direct your attention to the sector and evaluate trading oportunities we all profit from.

Important:

Amplitude for day trading : THis stock is more of a Swing trading stock but if you want to daytrade it, you need at least 100 shares as you have an amplitude or intraday tradable variance of 40 cents to a dolar. Anything below that would be hard to enter and exit...Size it for the amplitude.

Just a thought....

Good luck.

THE WEEK AHEAD: UAL, DAL, SLB, WBA EARNINGS; XOP, SLV, QQQEARNINGS:

There are four options highly liquid underlyings that pop up on my screener for next week with 30-day implied of >50%: UAL (23/88/22.6%)* (on Wednesday after market close); DAL (13/74/19.1%) (Tuesday before market open); SLV (18/59/16.4%) (Friday, before market open), and WBA (43/54/12.2%) (Thursday, before market open).

Pictured here is a directionally neutral 29/50 short strangle in the November monthly with the options camped out at the 16 delta, yielding a 2 x expected move break even on the put side and > 2 x expected move on the call. Delta/theta -.41/6.00; paying 1.87 at the mid price as of Friday close (.94 at 50% max).

The DAL November 20th, 16 delta 27/42 short strangle was paying 1.83 at the mid price as of Friday close; delta/theta 1.48/4.39.

SLB is small enough to short straddle, but would go "skinny," as the November only has 2.5 wides to play with. The November 20th 15/17.5 was paying 1.48 as of Friday close, but treating it as a short straddle and taking profit at 25% max (.37) isn't particularly compelling, so would probably pass on the play and deploy buying power elsewhere.

WBA suffers from a similar affliction (2.5 wides out in November), but the 32.5/40 is paying 1.54 there, albeit with break evens greater than the expected move, but not quite 2 x.

EXCHANGE-TRADED FUNDS RANKED BY PERCENTAGE OF STOCK PRICE THE NOVEMBER AT-THE-MONEY SHORT STRADDLE IS PAYING AND SCREENED FOR THOSE PAYING >10%:

XOP (15/56/14.5%)

SLV (45/51/13.1%)

GDXJ (15/49/12.9%)

EWA (15/42/11.6%)

XLE (27/43/11.2%)

GDX (15/40/10.7%)

XBI (29/43/10.3%)

USO (4/43/10.1%)

BROAD MARKET RANKED BY PERCENTAGE OF STOCK PRICE THE NOVEMBER AT-THE-MONEY SHORT STRADDLE IS PAYING:

QQQ (28/33/8.2%)

IWM (25/32/7.6%)

SPY (19/25/5.9%)

EFA (13/20/4.8%)

DIVIDEND PAYERS RANKED BY PERCENTAGE OF STOCK PRICE THE NOVEMBER AT-THE-MONEY SHORT STRADDLE IS PAYING AND SCREENED FOR THOSE PAYING >10%:

KRE (25/44/11.7%)

EWZ (15/42/11.6%)

XLE (27/43/11.2%)

GENERAL MUSINGS:

I already have a UAL covered call on, so am unlikely to partake in that underlying further here. Moreover, in the IRA/retirement account, I'm already deployed in everything at the top of the heap from an implied volatility standpoint, although I may carry on with my standard weekly 16-delta short put in the broad market instrument with the highest implied volatility, which would be QQQ. Alternatively, I'll do a QQQ 10-percenter (See Post Below) instead, as NDX isn't fantastically liquid, and a November 27th (currently, 48 days until expiry) will be available. To emulate a 50-wide, however, in NDX, I'll have to go 10-wide with 5 contracts or 5 wide with 10, etc. For example, the November 27th 240/245 is paying .50, and I'd have to sell 10 of those to emulate the NDX November 27th 9925/9975, paying 5.04. I would naturally prefer just selling one NDX spread, since it means fewer fees, but if the bid/ask is grotesque, I'll just have to go with QQQ or a RUT 50 wide. (The RUT November 27th 1385/1435 was paying 5.04 at the mid as of Friday close).

* -- The first metric is the implied volatility rank (where implied volatility is currently relative to where it's been over the last 52 weeks); the second, 30-day implied volatility; and the third, what the November at-the-money short straddle is paying as a percentage of stock price.

Our Stock of the day / DALToday, we have a short setup to share. Here we will give you a full explanation of what we expect

a) First we want to see the Weekly chart: We can see a major resistance level

b) Working from that level, we can go to the 1H chart. Here we can see a range with an inner zone ( Minor support zone / the expected target for the bearish movement)

c) Inside the Range, we can see a broken ascending trendline + corrective structure making a pullback on that broken structure

d) The corrective structure is composed of an ABC pattern. From a technical perspective, the structure is finished and is ready to trade

e) We have set our Entry orders below B and our Stop above C. Our Break Even level is defined with a horizontal yellow line. Finally, our Take profit is the Minor support zone

f) The risk Reward Ratio of this setup is 1.54

g) We will use 1% of our capital as maximum risk on this setup

h) We will cancel the setup if the price keeps rising and we lose our Risk Reward Ratio above 1.5

i) REMEMBER: Trade safe, protect your capital, and always understand what you are doing.