SHORT ON EUR/USDEUR/USD has Reached a Major Resistance Area/Zone and is highly over brought.

The Dollar (DXY) is inverted with the Eur/usd negatively. The dollar is highly oversold and should rise from its major Demand zone.

This should cause the Euro to Fall from its resistance zone.

Dollar has news at 8:30 for Unemployment claims. If the news is somehow good for the dollar and causes it to rise, the Euro will have the potential of reaching about 400 pips over the next few days.

I will be selling EUR/USD to the demand level shown.

Dollar

Fundamental Market Analysis for March 6, 2025 GBPUSDThe GBP/USD pairing pressed the accelerator pedal and produced another strong session on Wednesday, rising a further 0.85% and marking a third consecutive session of solid gains.

Despite warnings that the UK economy as a whole is weakening, markets rose following Wednesday's Bank of England (BoE) monetary policy hearing. Bank of England Governor Andrew Bailey said inflation is expected to rise moderately despite weaker growth figures, prompting markets to adjust expectations of a rate cut before the end of 2025. Rates markets now expect less than 50bp of overall interest rate cuts before the end of the year.

ADP's employment change for February showed just 77k new jobs, well below the forecast of 140k and March's 186k. Despite this, ADP results have not consistently correlated with Non-Farm Payrolls (NFP) since the reporting change in 2022, so the low reading is of little significance.

There is little of note on the UK side of the economic data list this week, so the key data for traders remains US Non-Farm Payrolls (NFP), which will be released this Friday.

Trading recommendation: BUY 1.2900, SL 1.2820, TP 1.3050

DXY DXY has moved in the great downward channel since its inception. Locally, the index may rise to the resistance line. Eventually, I expect it will achieve its lows during the 20s.

Best regards EXCAVO

DXY will go first to 95 and then 86.Hi, another dollar index DXY chart today.

You can make many predictions about how the world will be in the future, I have all just cycles + structures and charts.

At this point, that opinion may not be in line with those policy statements by world leaders. But we're not here to discuss politics.

Best regards EXCAVO

Remaining Bullish on Goldyesterday was the Non Farm Payroll news. Price stalled till it was time for news then pulled back to fill in a H4 Gap. Now I'm looking for price to continue bullish. There is not Area that they did not fill in so I'm thinking they might just come out the gate running soon as we are inside of the killzone. waiting for the killzone is the key though.

USOIL reaching the vital decision-making point... Are you a Buyer or a Seller at this point?

Chart is clean and clear...

XAU/USD Weekly Analysis XAU/USD Weekly Analysis with support and resistance levels tailored between $2,800 and $3,000:

XAU/USD Weekly Analysis: March 3–7, 2025

🔹 Overview:

Gold (XAU/USD) has entered a critical consolidation phase, trading between $2,800 and $3,000. The market remains sensitive to macroeconomic developments, including U.S. jobs data, Fed commentary, and geopolitical events.

🔹 Key Support Levels:

Immediate Support:

$2,835–$2,850: Critical support zone, aligned with the 38.2% Fibonacci retracement of the recent rally.

$2,800: Psychological support and a key structural level, reinforced by the 50-day SMA.

Major Support (Downside Breach Scenario):

$2,765–$2,780: Long-term trendline support from the 2024 lows.

$2,735: Key swing low; a break below here could signal a deeper bearish trend.

🔹 Key Resistance Levels:

Immediate Resistance:

$2,900–$2,920: Key consolidation range high and near-term target for bullish momentum.

$2,950: Previous week’s high and a critical barrier to further gains.

Major Resistance (Upside Breakout Scenario):

$2,975–$3,000: Psychological resistance and the upper bound of the bullish channel.

$3,075: Fibonacci 127.2% extension and a potential breakout target.

🔹 Technical Scenario Breakdown:

Bullish Case (Breakout):

Trigger: Fed dovishness or USD weakness.

Action: Break above $2,950 confirms bullish momentum.

Targets: $2,975 (psychological level), then $3,075 (breakout extension).

Bearish Case (Reversal):

Trigger: Strong USD or risk-on sentiment.

Action: Breakdown below $2,835 signals bearish shift.

Targets: $2,800 (key support), then $2,765–$2,735 (trendline and swing low).

Neutral/Range-Bound:

Range: $2,835–$2,950.

Action: Fade extremes (buy dips near $2,835, sell rallies near $2,950).

🔹 Price Action Drivers During the Week:

U.S. Jobs Data (March 7):

Weak NFP (<150k jobs) → USD sell-off → Gold rallies toward $2,950–$3,000.

Strong NFP (>250k jobs) → USD strength → Gold tests $2,835–$2,800.

Fed Commentary (March 5):

Hawkish tone → Gold pressured below $2,835.

Dovish tone → Rally toward $2,950+.

Geopolitical Surprises:

Escalations → Safe-haven surge → Gold breaches $2,975–$3,000.

De-escalations → Profit-taking → Drop to $2,800.

🔹 Technical Tools to Monitor:

RSI (14-day): Overbought above 70 indicates pullback risk; oversold below 30 signals potential rebound.

MACD: Bullish crossover above the zero line strengthens upward bias.

Volume: Confirm breakouts above $2,950 with rising volume.

📈 Summary:

Support: $2,835–$2,850 (critical), $2,800 (structural), $2,765–$2,735 (trendline).

Resistance: $2,900–$2,920 (immediate), $2,950 (key breakout), $2,975–$3,000 (psychological).

Catalysts: U.S. data, Fed commentary, and geopolitical factors remain key drivers.

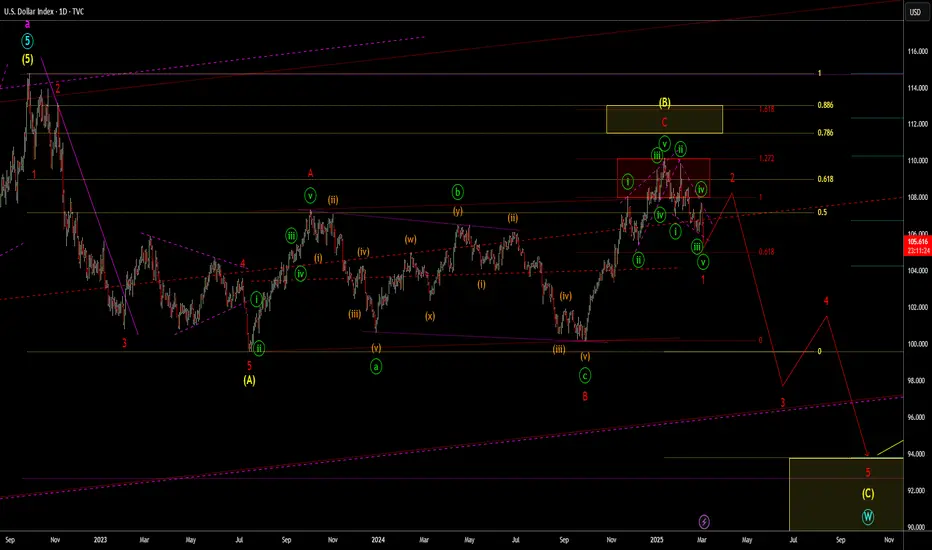

DXY Dollar Index OutlookThis is my current Elliott Wave count for the DXY Dollar index. I have a couple of variations which I will share but this one sees a decline starting with a leading diagonal in red wave 1 which is close to completion. May see a pull back in red 2 before a strong move lower in 3. The alternative is a nesting 1,2,1,2. If that's the case then a strong decline could continue from here.

Gold Confirms its Bullish for the week!The bullish play that I was looking for ended up playing out. Now I'm looking for it to continue but sitting on hands till it gives up a solid entry point. Waiting for the killzone is key.

DXY BULLISH BIAS|LONG|

✅DXY is going down now

But a strong support level is ahead of 105.400

Thus I am expecting a rebound

And a move up towards the target of 106.200

LONG🚀

✅Like and subscribe to never miss a new idea!✅

LETS GOOOO!!! NEW WEEK ON GOLD!!!Looking for the moves an I think we will come out the gate moving bullish all week. Practicing patience and waiting for the killzone before getting active on anything. Expecting some good moves starting tonight.

USDJPY - Potential upside from here?USD/JPY is currently consolidating within a range after a sharp downtrend from the 159.00 level. The price has established support around 148.50-149.00, forming a clear pattern. We're now waiting for a decisive break above the current consolidation area, which would signal renewed bullish momentum.

Once we see this breakout, expect a minor retracement to retest the broken resistance as new support – this will be our key buying opportunity. With the descending trendline already broken and the forecast indicating potential upside to the 154.00 area, traders should focus on buy positions following this retracement, with stops below the support zone.

LONG ON NZD/USDNZD/USD is giving nice uptrend structure from the higher TF.

Currently it has pulled back to a key support area and is looking good for a rise.

Dollar (DXY) is overall bearish and currently falling. (This has a inverse correlation with XXX/USD pairs)

I will be buying NZD/USD to the next resistance level / previous high for about 150-200 pips.

Fundamental Market Analysis for March 3, 2025 GBPUSDThe US Dollar Index (DXY), which tracks the dollar against a basket of currencies, started the new week on a weak note and has already cancelled out most of Friday's gains to more than a one-week high.

The British Pound (GBP), on the other hand, continues to post relative gains amid expectations of a less aggressive easing policy from the Bank of England (BoE). That said, concerns over US President Donald Trump's retaliatory tariffs and their impact on the UK economy may keep GBP bulls away from new bets. In addition, geopolitical risks could limit deeper USD losses and limit GBP/USD gains.

Meanwhile, signs that the disinflation process in the US has stalled, reinforcing the case for the Fed to take a wait-and-see approach to future interest rate cuts, could also serve as a tailwind for the USD. This could help to further contain GBP/USD and warrant some caution before positioning for a resumption of the recent uptrend from levels below 1.2100, or the yearly low reached on 13 January.

The main focus will be on the closely watched monthly US employment data on Friday. The widely-reported Nonfarm Payrolls (NFP) figure will shape expectations on the path of the Fed rate cut and drive demand for the dollar in the near term.

Trading recommendation: BUY 1.2610, SL 1.2560, TP 1.2690

New Month, New Week, New Opportunities on Gold! looking for price to flip back to bullish this week but we need to wait for a break in structure of a possible sweep of the lows first before we see it. Monday might just be flaky so being hesitant until Tues for the best move.

EURUSD: Bearish Outlook For Next Week Explained 🇪🇺🇺🇸

With the Friday's turmoil in the White House,

EURUSD went down sharply.

The price broke and closed below a significant daily support.

It is a strong event that increases the probabilities that the market

will continue going lower.

Next support will be 1.032

❤️Please, support my work with like, thank you!❤️

Trump Pump. Trump Dump. Trading Family,

We had our Trump pump. Now, we are seeing a Trump dump. Tariffs and other geopolitical events are causing market uncertainty. Let's take a look at our charts to find out how much more pain we are in for. And, a positive sign. Smaller cap altcoins and many memecoins appear to be holding strong!

✌️ Stew

Fundamental Market Analysis for February 28, 2025 EURUSDEUR/USD remains under selling pressure near 1.0390 during Asian trading on Friday. The euro (EUR) is weakening against the US dollar (USD) amid risk-off sentiment. The US Personal Consumption Expenditure (PCE) price index will take centre stage later on Friday.

Late Thursday, US President Donald Trump said that 25 per cent duties on imports from Canada and Mexico will take effect on March 4, rather than April 2 as he had anticipated the day before. Trump also said goods from China would be subject to an additional 10 per cent duties. He also promised this week to impose 25 per cent tariffs on shipments from the European Union. Tariff uncertainty from Trump is likely to weigh on the common currency in the near term.

Cleveland Fed President Beth Hammack said on Thursday she expects the US central bank's interest rate policy to be put on hold for now amid a search for evidence that inflationary pressures are easing and returning to the 2 per cent target. Meanwhile, Atlanta FRB President Raphael Bostic said late Wednesday that the Fed should keep interest rates on hold, which continues to put downward pressure on inflation. The Fed's cautious stance could boost the US Dollar and serve as a headwind for EUR/USD.

Trade recommendation: SELL 1.0380, SL 1.0430, TP 1.0300

GOLD Closing out the MonthLooking for Gold to fill in the Weekly FVG then turn around to flip back bullish going into the new month. Price will show its hand between now and London. We just have to wait for it. Patience is key!

XAUUSD UPDATED VIDEO ANALYSIS XAU/USD Analysis for 21 February 2025

Here’s a detailed breakdown of the factors influencing Gold (XAU/USD) for tomorrow, based on technical and fundamental insights from recent market data and forecasts:

1. Technical Analysis & Key Levels

Resistance Levels:

Immediate resistance at 2,940–2,943 USD (record high observed on 19 February)

A breakout above this zone could target 2,970 USD (next psychological barrier) or even 3,030 USD (Triangle pattern completion)

Support Levels:

Critical support at 2,887–2,906 USD. A drop below this range might trigger a deeper correction toward 2,850 USD

Indicators:

RSI (54.58): Neutral but leaning bullish.

MACD & Williams %R: Buy signals

Stochastic Oscillator: Overbought, suggesting short-term correction risks, though the broader uptrend remains intact

2. Fundamental Drivers

Fed Minutes Impact:

The release of the Federal Reserve’s January meeting minutes (scheduled for 19–20 February) is critical. A hawkish tone (e.g., delays in rate cuts) could strengthen the USD, pressuring Gold. Conversely, dovish hints may fuel bullish momentum

Geopolitical Tensions:

Ongoing US-Russia negotiations over Ukraine and Trump’s renewed tariff threats (e.g., 25%+ tariffs on pharmaceuticals and semiconductors) may sustain safe-haven demand for Gold

Dollar Dynamics:

The inverse correlation between XAU/USD and the USD remains pivotal. A weaker dollar (due to risk-off sentiment or Fed easing expectations) could propel Gold higher

3. Price Action Scenarios

Bullish Case:

A sustained break above 2,943 USD confirms the Triangle pattern breakout, targeting 3,030 USD

Continued safe-haven demand (geopolitical risks, tariffs) and dovish Fed signals may drive prices higher

Bearish Risks:

Failure to hold 2,900 USD support could trigger a correction toward 2,850 USD

Hawkish Fed rhetoric or USD strength (e.g., strong economic data) may cap gains

4. Strategic Takeaways

Entry Points:

Long positions: Consider buying on dips near 2,900–2,877 USD with a stop loss below 2,850 USD

Short-term traders: Target 2,970 USD if resistance at 2,943 USD breaks

Risk Management:

Monitor Fed Minutes and USD volatility. Adjust stop-loss levels dynamically based on news flow

Conclusion

Gold remains in a bullish trend, supported by geopolitical uncertainties and inflation hedging. However, tomorrow’s Fed Minutes will be pivotal in determining short-term momentum. A breakout above 2,943 USD opens the door to new highs, while a breakdown below 2,900 USD signals profit-taking or a deeper correction. Traders should align positions with technical levels and news-driven volatility.

LIKE US BOOST US SHARE OUR IDEA COMMENT AND MOTIVATE

Gold Ready for Selloff toward 2800 Level!!(sell Setup)See how price action plays out during in the next 15 min we gonna probably see a nice fakeout from the new york volume before a further continuation to downside.

Always remember to use proper risk management.

Follow me for more Analysis!!

Gold Temp Bearish Pressure Price looks like its going to sweep the lows. I mentioned this in my previous update. Being that it is the end of the month and coming up to end week we might not get the bullish play this week but if they move inside of the Weekly FVG then they have my attention.

BTC USD UPDATEWe have seen an excellent drop to lower levels. Now, we're waiting to reload some spot trades. We're looking for a clear bullish shift before entering any spot positions. However, short positions taken into these levels have performed well, as indicated by the green on the screen. Currently, we're observing market reactions. If market makers are genuinely bullish at these levels, we should see a rapid price delivery. This means we have potentially long weeks ahead, and we need to be v [atient to avoid missing any smoves. Wait for safe trading opportunities.