DYNAMIC CABLES LTDStock fundamentally strong

Breakout with DOJI above key resistance and both EMAs.

Strong volume spike.

Bullish structure with higher highs and higher lows and trend line support.

Earnings

PBF Energy turnaround happening?Fundamentals:

The stock is trading at 0.42x book value, and pays 5.58% dividend. Of course, if profitability deteriorates further, the dividend can be cut and the P/B value can fall lower, but!

PBF is doing a good job on cost cuts, in the last earnings report posted narrower loss than expected

The mexican company 'Control Empresarial de Capital' is continously buying shares of the company, and nor Carlos Slim, neither another insiders-holders selling shares.

Technicals:

The 100 day moving average is the Boogeyman for PBF Energy.

One year ago, early May 2024 the price lost it, and never got back above.

Death cross happened in 2024 July.

Got rejected by the 100MA 4 times, as seen on the picture. The 50day got under the 100, but not worked as support. In 2025 Jan-Feb it tried, but failed.

Is this time different?

A final washout is already happened to $13.45 in April.

In May 2025, the 100MA rejected the price again, but this time the 50MA held as support.

Now the price battles with the 100MA again, break above means a target of $25, as this is an unfilled gap of 2025 February, and the 200 day MA.

Short-term traders can set $25 as target.

Long-term investors can eye $32-36 with proper risk management, or continous buying-selling. Can take a year or two.

100% run up into earningsChance to get hot with semis if SPX can claim above 5950

High $8 for buying until we lose the 50MA.

Break above 12 with strength/volume will be key for continuation to 20.

Price-To-Earnings ratio (12.6x) is below the US market (17.8x) *

Revenue is forecast to grow 17.78% per year *

Earnings grew by 47.8% over the past year *

Short Interest 6.94M

Short Previous Month 7.16M

Short % of Shares Out 23.30%

Short % of Float 26.13%

Short Ratio (days to cover) 17.67

they will have tariff issues, so guidance is likely to bring uncertainties

SGMO May Be the Most Mispriced Opportunity of 2025-26

-SGMO is shaping up to be a high-potential trade with both short- and long-term upside. After entering an uptrend in late 2023, the stock is showing strong bullish signals, with technical indicators and moving averages pointing to a favorable buy zone. Fundamentally, it's hitting a key turning point — EPS is moving from negative to positive for the first time, and revenue is projected to grow from \$50M to \$200M by 2028.

-Typically, SGMO experiences a major price jump every year, and it’s currently coming out of a low period. A breakout is expected within the coming month. Even under conservative estimates, a 200% return is possible in the near term. But if SGMO revisits its historical highs around $20 — a level it’s touched multiple times in the past — the upside from its current $0.50 range could exceed 4,000%. The financial structure is far stronger than it was during previous lows (like March 2020), making this a classic high-risk, high-reward setup worth watching closely.

NVDA GEX Earnings Outlook by OptionsNVDA reports earnings this Wednesday, and it’s a big deal. A major move could impact both the indexes and broader tech sector.

The OTM 16 delta curve essentially overlaps with both the GEX profile and the expected probability zone — signaling strong confluence.

📈 Rising IV with falling call skew: Volatility is rising into earnings, while the call skew is dropping — a sign of growing interest in downside hedging/speculation.

🔷 Key inflection zone (129): Above 129, the market is unlikely to surprise. Below it, however, a domino effect could trigger increased volatility and put-side flows.

Implied move into earnings is 6.62%, reflecting binary risk expectations from the options market.

Strong gamma squeeze territory exists between 140–145, with significant call wall buildup around 140.

The nearest expiry shows a positive net GEX — supporting short-term mean-reversion or hedging flow stability above 129, at least until the earnings print.

🔴 Downside risk scenario:

In the event of a downward move, the market is most heavily hedged around the 125 level, which aligns with the deepest put support.

💡 Wheeling Opportunity Idea

ONLY IF you want to own NVDA long-term around the $130 level (even if it drops short/mid-term), this might be a great time to start the wheeling strategy.

Because earnings inflate volatility, you can sell a near-term cash-secured put (CSP) for solid premium — even on a 53DTE (July) option.

Based on current GEX levels, we’re seeing:

-Support (squeeze zone) around $125

-Call resistance around $140

-A potential upside squeeze extending to $145-$150

These align roughly with ~20 delta OTM options, so the premium is attractive.

How would I personally start this:

Sell a CSP for May 30 with the intention to get assigned if NVDA drops.

If I do get assigned, I’m happy to own shares.

Then, I sell a 60DTE covered call right after to collect another round of premium.

If I’m not assigned, I sell a new 45–60DTE put the following week — still benefiting from the relatively high IV.

👉 Remember: High IV = synthetic time value. With this two-step method, you can harvest premium twice in quick succession.

I used the same technique with NASDAQ:INTC , and it’s been performing well.

💥 ONLY IF you want to own NVDA long-term around the $130 level (even if it drops short/mid-term)!

Unity Software (U) – Strong Earnings and Bullish FlowsFundamental Overview

Unity Software has been consolidating within a defined range for approximately a year following a significant decline in its stock price. Despite previous challenges, the company has consistently surprised investors with its earnings over the past year, maintaining strong performance. Historically, Unity tends to perform well during the May–June period. Looking ahead, projections suggest a decline in net margin, though net income is expected to increase, reinforcing the company's strong execution.

Additionally, Unity has exceeded expectations for four consecutive earnings reports, underscoring its resilience and growth trajectory.

Technical Outlook

- Momentum & Price Action: The stock exhibits solid momentum and is currently situated in a buy zone.

- Options Flow: Bullish sentiment is evident in options activity, signaling strong institutional interest.

- Analyst Ratings:

- Needham analyst Bernie McTernan maintains a Buy rating but lowers the price target from $33 to $30.

- Barclays analyst Ross Sandler maintains an Equal-Weight rating and lowers the price target from $26 to $25.

Given the current trends, bullish options flows, and favorable seasonality, Unity Software appears poised to test $25 in the upcoming weeks, particularly if momentum continues to drive price action.

HAE (Very bullish)

I see a big oppertunity in this stock.

The cash per - employ is risen to a very high level.

The stock has positive earnings.

Stock has some momentum.

DCA into $FI- NYSE:FI is big recognizable brand in Point of Sales. You might have seen clover handheld machines.

- I believe fundamentals on this blue chip company is getting cheap. I'm not going all in but have started DCA into this name.

- If it falls further 20-30 or even 40% I will be happy to DCA further.

- Fundamentally, I am buying it close to fair value.

Year | 2025 | 2026 | 2027 | 2028

EPS | 10.21 | 11.91 | 13.88 | 15.72

EPS% | 16.35% | 16.63% | 16.51% | 13.25%

- Any company which is growing EPS% mid teens with a recognizable brand value deserves a fair forward p/e of 20

Base Case Fair Value w/ forward p/e = 20:

Year. | 2025 | 2026 | 2027 | 2028

Fair Value | $204 | $238 | $277.6 | $314.4

Conservative Base Case fair value w/ forward p/e=15:

Year. | 2025 | 2026 | 2027 | 2028

Fair Value | $153.15 | $178.65 | $208.2 | $235

Bull Case Fair value w/ forward p/e=25:

Year. | 2025 | 2026 | 2027 | 2028

Fair Value | $255 | $297 | $347 | $393

Bear Case fair value w/ forward p/e = 10:

Year. | 2025 | 2026 | 2027 | 2028

Fair Value | $102 | $119 | $138 | $157

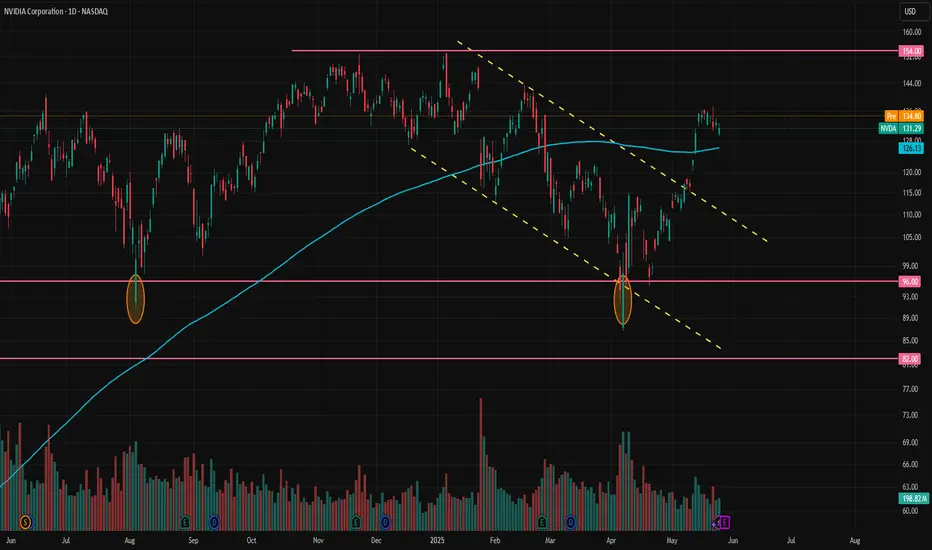

What to Watch in Nvidia Earnings and Key Technical LevelsStock markets around the globe are turning their focus to one key earnings report: Nvidia. AI has been the primary driver of the U.S. stock market over the past few years, and Nvidia’s earnings are widely viewed as the best indicator of growth in the AI sector. The correlation between Nvidia and broader U.S. stock performance as well as its influence on global equities, crypto, and FX is strong enough for the world to fixate on this report.

Nvidia is expected to report $0.88 EPS for the first quarter of FY2026, representing a 43.36% year-over-year increase, but a slight decline quarter-over-quarter. The company previously guided revenue between $42.14 billion and $43.86 billion, with market consensus currently at $43.317 billion, in line with that range.

The key revenue stream, Data Center, is expected to generate $39.357 billion, reflecting 74.44% growth. Some analysts are forecasting as high as $42.051 billion for this segment alone.

At a forward P/E ratio of 27.6x, Nvidia is trading well below its 1-year (32.1x), 2-year (33.7x), and 5-year (40.1x) historical averages. This more favorable valuation, coupled with strong AI tailwinds, could present a solid medium- to long-term buying opportunity if earnings and guidance support the growth narrative.

After breaking out of the downtrend, NVDA approached the 140 resistance level but failed to break through. Following the upcoming earnings release, if Nvidia pulls back to either 118 or 110, those levels could present buying opportunities, assuming the report isn’t significantly negative.

It’s worth noting that sometimes real market expectations run much higher than the analyst consensus, which can lead to a selloff even after a strong earnings report.

The 154 level remains the key resistance for now, and in our view, a breakout this week carries a relatively low probability. If the report tomorrow exceeds expectations, 154 could still act as a barrier and trigger some profit-taking by Nvidia bulls.

TMGH Rebound ExpctationTMG Holding trend has reached its downward zone at the support line 51.142. In case of a rise, it is expected to breach the resistance line 51.233 and reach the resistance line at 51.625 points, then reach the third resistance line at 51.777 points. This upward direction is expected due to TMGH signs MoU For Development of New Large-Scale Mixed-Use Project In Iraq, which is expected to generate total sales of $17 Billion, and income of $1.5 Billion per annum upon project completion. In case of falling, it's expected to break the 1st support line at 50.961 points, then the second support line at 50.900, then the third line at 50.779.

STAR breakout candidateThis is the chart of Strides pharma science ltd. The stock currently is trading sideways.

Stock has approached the resistance with very high relative volume.

Stock has continuously performed financially well with triple digit earnings growth and margins expansion.

The recent approach to resistance with very high relative volume suggests a high probability for breaking out resistance zone because the stock has very high earnings but not reflected in price hence the reason. Keep watching the stock.

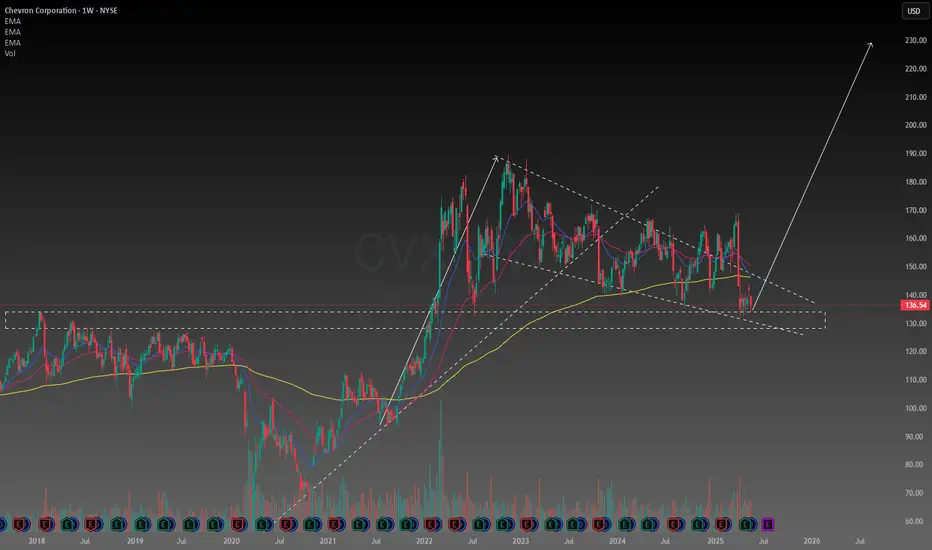

Chevron wedge bull flagChevron stock is well below its intrinsic value, I found a decent setup based on technical analysis for my entry, because of the attractive dividend payouts I will buy and hold CVX for awhile and see what happens.

ETOR Going UP?It looks like Etoro has found its Resistance and Support trend line.

Just wait for the earnings release.

TMGH Trend Line Rebound AnalysisTMG Holding trend is still in a downward zone, but rebounded at the support line 52.019. In case of a rise, it is expected to breach the resistance line 52.472 and reach the resistance line at 52.805 points. In case of falling, it's expected to break the 1st support line at 51.535 points, then the second support line at 51.475, then the third line at 50.779, which is fundamentally not a preferable expectation because of the Omani Ministry of Housing and Urban Planning signing a $4.7 Bln real estate deal with TMGH. For developing two real estate projects spanning 4.9 million square meters, to deliver around 12.9 thousand residential units. In addition, the combined sale value of units is projected at $4.7 billion.

Breakout in SkipperStock has broken out of range of 4 months in long term uptrend with high relative volume.

Fundamentally, stock has delivered double digit earnings growth for straight 4 quarters.

Margins have also been increasing for last 3 quarters.

Overall, it's a good technofunda pick to watch out for.

TSM great potential before earnings call? Value to be collected!Hi guys we would be taking a look into our analysis for TSM!TSMC (TSM) Stock: Positioned for

Strong Growth Despite Tariff Pressures -

Taiwan Semiconductor Manufacturing Company (TSMC), the world’s leading contract chipmaker, continues to shine as a long-term winner in the semiconductor space, even amid renewed trade tensions and potential tariffs.

1. Resilience Amid Tariffs and Trade Tensions

While the U.S. has recently introduced or hinted at higher tariffs on tech-related imports from China, TSMC stands out due to its strategic positioning. As a Taiwan-based company with increasing investments in the U.S., including a major Arizona facility, TSMC is well-insulated from the harshest tariff implications. In fact, the shift toward U.S. domestic chip production could boost TSMC's presence and government support, solidifying its role in global supply chains.

2. Unmatched Technological Leadership

TSMC is years ahead of competitors in cutting-edge semiconductor manufacturing, particularly in advanced nodes like 3nm and 2nm chips. This technology edge secures high-value contracts with top-tier clients like Apple, NVIDIA, and AMD, ensuring a steady and growing revenue stream.

3. Surging Demand for AI and High-Performance Computing

With the global explosion of demand for AI infrastructure, data centers, and high-performance computing, TSMC is perfectly positioned. It is the go-to foundry for the most advanced AI chips, giving it a critical role in powering the next generation of tech innovation.

4. Strategic Global Expansion

TSMC’s global expansion—including new plants in the U.S., Japan, and Germany—reduces geopolitical risks and enhances its ability to serve major markets locally. These moves also align with government incentives and support from the CHIPS Act and similar programs.

Outlook:

TSMC is not only weathering the global trade climate—it’s thriving. Its dominant market share, world-class technology, and expanding global footprint give it a strong competitive moat. With rising AI demand and the shift toward local production, TSM is set to benefit on multiple fronts.

TSM stock remains a high-conviction play for investors looking to capture the future of tech.

TSMC has consistently delivered impressive financial results, with the company surpassing analyst expectations in the past 12 consecutive quarters. For instance, in the fourth quarter of 2024, TSMC reported earnings per share (EPS) of $2.24, exceeding the consensus estimate of $2.16. This track record underscores the company's robust operational efficiency and market demand for its advanced semiconductor solutions.

Upcoming Earnings Call

Investors are anticipating TSMC's next earnings call scheduled for Thursday, April 17, 2025, before the market opens. Analysts expect the company to report an EPS of $2.02 for the first quarter of 2025. Given TSMC's history of exceeding expectations, there is optimism that the company will continue its trend of strong financial performance.

EPS beat estimates 16 times in 17 quarters!!!!!

We are targeting approximetly 18% increase!!!

📌 Trade Plan

📈 Entry: 152

✅ Target 183

❌ SL: 128

City Group this weeks best choice from the earnings calendar!Hi guys we would take a look into our perspective for Citygroup, which out of this weeks earnings stocks gives us the best potential, we are targeting a whoping 20% increase for our end goal.

Citigroup (NYSE: C) is demonstrating strong growth potential in 2025, driven by robust earnings, strategic initiatives, and favorable market conditions. Here's our comprehensive analysis focusing on Citigroup's growth prospects:

📈 Recent Performance Highlights

Q1 2025 Earnings: Citigroup reported a 21% year-over-year increase in net income, reaching $4.1 billion ($1.96 per share), surpassing analyst expectations of $1.85 per share. Revenue rose 3% to $21.6 billion, exceeding forecasts. The growth was primarily driven by a 23% surge in stock trading revenues amid market volatility and increased client activity.

Return on Tangible Common Equity (RoTCE): The bank's RoTCE improved to 9.1%, nearing its target range of 10–11%, indicating enhanced profitability and efficient capital utilization.

📊 Growth Metrics & Analyst Outlook

Earnings Per Share (EPS) Growth: Analysts project a 15.3% annual EPS growth for Citigroup over the next five years, outpacing peers like Bank of America (9.0%) and JPMorgan Chase (3.9%).

Revenue and Earnings Growth: Citigroup is forecasted to achieve a 9.8% annual earnings growth and a 7.9% revenue growth over the next three years.

Share Repurchase Program: The bank has initiated a $20 billion share buyback program, reflecting confidence in its financial strength and commitment to returning capital to shareholders.

🚀 Strategic Initiatives & Market Position

Operational Efficiency: Citigroup is investing in technology and streamlining operations, including reducing reliance on external IT contractors and enhancing data management systems. These efforts aim to improve efficiency and regulatory compliance.

Market Leadership: The bank's diversified business model, encompassing trading, wealth management, and banking services, positions it well to capitalize on various market opportunities.

⚠️ Market Considerations

Economic Uncertainty: While Citigroup's performance is strong, broader economic uncertainties, including potential recessions and regulatory changes, could impact future growth. Analysts are monitoring these factors closely.

✅ Our Conclusion

Citigroup's robust earnings growth, strategic initiatives, and strong market position make it a compelling candidate for investors seeking growth opportunities in the financial sector. The bank's focus on operational efficiency and capital return strategies further enhances its growth prospects!

The entry would go as following -

Entry point : 63.80

Target 1 : 71.69 - just above the GAP which was previously formulated, when we pass it this would cement our uptrend formation.

Target 2 : 75.30 - finalizing almost 20% growth of the stock which would be around the strong resistance area.

Stop Loss : 55.50 - around the bottom zone , which there was a lot of volume supported by the buyers.

META - Another great earnings, allowing us to collect value?Hi guys ,we would be looking into our analysis for META stock.

Meta Platforms Inc. has demonstrated robust financial performance, underscoring its strategic investments in artificial intelligence (AI) and digital advertising.

Strong Financial Performance

In Q4 2024, Meta reported revenue of $48.39 billion, marking a 21% increase year-over-year. Net income surged by 49% to $20.84 billion, with diluted earnings per share (EPS) rising 50% to $8.02. The company's operating margin improved to 48%, up from 41% the previous year, reflecting enhanced operational efficiency.

AI-Driven Advertising Growth

Meta's advancements in AI have significantly bolstered its advertising capabilities. In Q3 2024, advertising revenue grew by 18.6% year-over-year, reaching $39.89 billion. The integration of AI technologies has enhanced ad targeting and delivery, contributing to this growth.

Our Confidence

Overall analysis maintains a bullish outlook on Meta's stock, with an average price target of approximately $634, suggesting a potential upside of around 17% from current levels. The company's strategic focus on AI and its strong financial results support this positive sentiment.

In summary, Meta's strong earnings report, driven by AI advancements and advertising growth, positions the company favorably for continued success in the evolving digital landscape.

📌 Trade Plan

📈 Entry: 550

✅ Target: 630 - below the ATH to give an achievable destination

❌ SL: 480 - below the support zone to protect the trade

First step towards ATH BULIISH FLAG on DOGE

In several time frames DOGE has formed a Bullish Flag from around $0.16 going to $0.32.

This is the first dog step to the ATH!

"MASTER OF SOCIAL REALMS, META" How Does Meta Make Money?The long-term outlook for META stock looks pretty promising. Thanks to heavy investments in AI and the metaverse, along with steady growth in its advertising business, analysts predict the stock price could climb from its current level (around $640) to anywhere between $700 and even $2,000 by 2030. AI-driven improvements in ad efficiency and growing user engagement on platforms like Facebook and Instagram are major drivers. Plus, the company’s solid financials give it plenty of room to keep investing in the future.

That said, there are risks to watch out for, like tougher regulations in Europe, increasing competition, and uncertainty around the metaverse’s success. Overall, though, META’s strong position in tech and the market makes it a solid pick for long-term investors. Just make sure to weigh those risks before jumping in.

trend and corrections(1H)As I said multiple hours ago , we saw that gold declined both in the four-hour and the one-hour charts.Now I'm gonna mention that in 1 hour chart again so if we follow the trend and correction strategy we will find an another possible correction that says and shows a sell opportunity after happened.Good luck

simple and natural :-!Dears the gold has decreased and broken the lines and has corrected now in my opinion.It's the time to get sell position.It's easy *^_^*

UnitedHealth Group | UNH | Long at $323.00UnitedHealth Group NYSE:UNH currently has a P/E near 15x, steady rising revenue (2024 = $400+ billion), EPS of 6.24x, dividend of 2.2%, and earnings are forecast to grow by 10.8% per year. The stock, however, has plummeted recently due to negative news, rising healthcare costs, CEO changes, and suspension of 2025 outlook. Every company has bumps, but I view solid companies like NYSE:UNH as pure opportunities for long-term investment - especially with America's aging population.

From a technical analysis perspective, the stock price has entered my "crash" simple moving average zone (which currently extends down near $307.00). Personally, this is the zone I am starting a position due to the odds of a future bounce from here. However, I am very aware that there is an open price gap near $265.00 that may get filled this year or early next. I could see a bounce in my crash zone to bring in the bulls and then a drop to that level to heighten the fear. That is another area I plan to grab more shares and build a strong position. But, in case it doesn't extend that low, I have started a position at $223.00, with future investments near $307.00 and below. I doubt this will be a quick turnaround stock - patience is where money is made.

Targets (into 2028):

$375.00

$475.00

$580.00