EBAY

Ebay: Another company Amazon will put out of businessIt is no secret that Amazon has taken the world by storm in the past few years as its market cap nears the unbelievable 1 trillion mark. Amazon now provides a service for nearly every demand you can think of. Food, retail products, shipping, a place to sell your goods/services, cloud services, etc. In the next few years, Amazon will probably increase its user base and put smaller companies out of business, such as Blue Apron, Barnes and Noble and Ebay.

Ebay is a great fundamental short. In the next few years, their annual revenue will decrease as they begin to lose money, inevitably going bankrupt due to Amazon's dominance. Technically, the chart tells the same story. Ebay recently announced terrible earnings, causing the stock to gap down hard. It has now fallen below all significant moving averages. The 50 day moving average (yellow line) also crossed below the 200 day moving average (blue line), a very bearish sign known as a death cross.

Due to the drastic recent decline, Ebay could be in for a short term bounce, but will continue to fall in the near and long term. I recently picked up Ebay puts with a break even price of $30 that expire January 18th. I would be astonished if they are not deep in the money by that time.

THE WEEK AHEAD: NFLX, EBAY, IBM, XOP, EWZ, TLT/TBTWe're back into the thick of earnings season again ... .

NFLX (rank 64/implied 52) pops the top on Monday after market close, so you're going to want to slap anything you want to do on before session end to take maximum advantage of a volatility contraction play.

Pictured here is a 20 delta iron condor in the weekly with a buying power effect of 6.59 per contract, and a max of 3.41 (a smidge greater than one-third the width of the wings). Naturally, you'll have to adjust the strikes shortly before fill, since it's a mover. Look to take profit at 50% max ... .

EBAY hits the bricks on Wednesday after market close. I'd rather have background implied at >50% (it's currently at ~33%), but it may be worth watching to see if it ramps up in the Monday through Wednesday sessions.

IBM gets its party on on Wednesday after market close, too, but that background implied of 25% doesn't exactly get my motor running.

On the exchange-traded fund front, there isn't much premium to be had, and what there is to be taken is to be found in the places where it's been over the past several weeks: Brazil (EWZ -- 33.5% background), and petro (XOP/OIH -- 30%). Me personally, I'm hand sitting on those until I can see the whites of September's eyes (it's still 68 days out). That being said, if you're willing to go a little more long-dated here: the XOP Sept 21st 43 short straddle is paying 4.36 with break evens at 38.64/47.36, theta of 3.12, and -7.82 delta; the EWZ Sept 21st 34 short straddle: 4.06 credit, 29.94/38.06 break evens, 2.9 theta, -6.74 delta.

Other "Major Food Group" Directionals: TLT continues to bop annoyingly along horizontal support/resistance near 122.50 like a toddler kicking the back of your seat in economy class. My tendency has been to short on retrace in a tightening rate environment, with the preference being for more flexible, longer-dated setups like diagonals where I've got time to reduce cost basis, as opposed to using static one-off spreads where you could find yourself in the middle of a short-term risk off event that ruins your day.

Inversely, TBT is holding on by its fingernails to 35.25. I could see pulling the trigger on either here -- a long-dated TLT downward put diagonal or covered short combo/a TBT upward call diagonal/covered long combo. (See TBT Upward Call Diagonal Post, below).

BTCUSD (BTC) and SPY tracking EBAY's Wyckoff AccumulationPotential Re-accumulation on SPY and Accumulation on BTC

Strong similarities in horizontal levels of support and resistance for SPY and BTC when tracking versus EBAY's accumulation phase:

Selling climax (1), double top (2, 3, 4), secondary test of lows (5), test of double top neckline (6), then down to a new low into a spring (7), then onto mark up.

Looking for a spring on both to confirm upward trend.

EBAY shares Buy IdeaEBAY shares Buy Idea @Monthly Demand Zone (38.06 - 34.33)

Buy Limit: 38.01

Stop Loss: 33.20

Take Profit: 45.51

t's not just @Facebook. Thousands of companies are spying on youWe’re At A Critical Tipping Point Data Control and Privacy-Wise PROTEST BIGDATA - GET YOUR LIFE BACK - SELL TECH

crwd.fr

SHORT ON EBAY!We've got a short on Ebay guys!

I believe that once prices have penetrated the 41.00 region we could see a potential bearish pull down to the 37.00 Region or even lower!

Let's see how things turn out!

TP: 37.00

THE WEEK AHEAD: EBAY, FB, MSFT, BABA, AAPL, XOM EARNINGSMore earnings ... .

EBAY announces on the 31st (Wednesday) after market open: implied volatility percentile/rank 72/background 33.

FB, on the 31st after: 90/34

MSFT, also on the 31st after: 100/29

BABA, on February 1st before: 94/40

AAPL, on February 1st after: 97/30

XOM, on February 2nd before: 91/19

Of these, BABA looks the most promising. Preliminarily, the Feb 9th 192.5/222.5 20 delta short strangle pays 4.71 at the mid, with its defined risk counterpart -- the Feb 9th 187.5/192.5/222.5/227 iron condor -- paying 1.77.

On the exchange traded fund front: While there are underlyings with implied volatility in the greater than 70 percentiles, background implied remains muted, so these are likely to be of limited productiveness. Here are the top five: IYR (100/17); FXI (100/27); XLU (93/17); XLB (87/18).

Volatility products: While VIX finished Friday lower to 11.08, futures didn't follow suit and were off only between .05-.10 across the term structure. Feb was off .10, but the March contract actually finished up by .05, meaning that neither VXX nor UVXY were down much. While I'm not in a position to read the minds of /VX futures traders, my guess is that they're positioning anew for the expiry of the continuing resolution that expires on February 8th (that play wasn't particularly productive the last go-round) or, more likely, a debt ceiling showdown in March, which has far more important ramifications for the market than a government shut-down, since a debt ceiling actually involves U.S. default concerns (historically, virtually illusory), while a failure to fund the government does not.

In any event, I missed the opening of the March 9th weekly in VXX to put on my weekly short volatility play, and have spreads on in the monthly at current levels (short leg at 27), so will look to add in spreads in the March 23rd when it opens. Granted, what I have on looks a little battered here, particularly in the late February, early March expiries. The only thing to do is be patient, wait, and see whether the futures succumb to pressure to unload at least their February contracts so they're not left holding the bag and then to roll out for duration if particular spreads can't be taken off in profit or scratched out at expiry ... .

Signs of WeaknessHi guys. Here's another idea for the brave hearts. Humbly posted for public viewing and judgement. Have a nice day.

Long Ebay @ WK Demand AreaPrice on EBAY has retraced to WK D area, 3M, MN and WK TL are all up so long is valid. Targeting 41-42.

Ebay Gap FillEbay should be able to rally into the gap fill for a small gain.

Price is rallying from a demand zone currently.

Short term buying opportunity towards Black Friday? EBAY is testing support as we approach Black Friday and Cyber Monday.

The shopping spree expected can boost EBAY following its recent decline and send it back towards the bottom of the rising triangle, to test it as resistance.

Read more about EBAY, SPY, DAX, FTSE, DXY Gold and more in this week's newsletter

#WeeklyMarketsAnalysis in Twitter

EBAY Long 2-6 Weeks Technicals and valuation support a bullish rebound. Supports at 35 from the channel it has been trading in since June. PE of 5.2 is a steal in this market where the S&P trades at a PE of 25. Excellent margins support their profitability. There should be enough space in e-commerce for both Ebay and Amazon NASDAQ:AMZN allowing both to continue to grow.

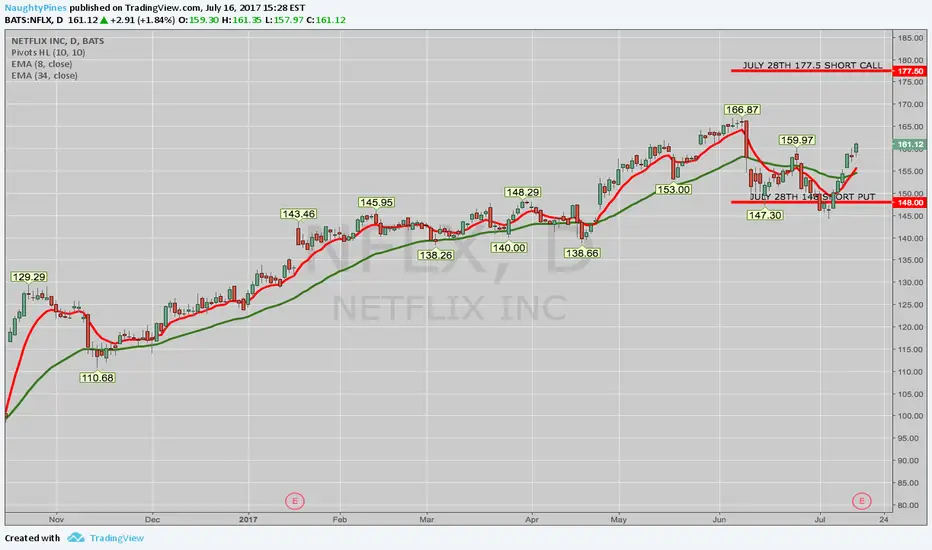

THE WEEK AHEAD: NFLX, IBM, CSX, EBAY, MSFT EARNINGSAlthough many of next week's earnings plays aren't up to my usual snuff due to lower implied volatility invading the entire market with VIX at sub-10 levels, some of these announcements might offer decent premium even though the metrics for a volatility contraction play aren't ideal (>70 implied volatility rank, >50 background implied volatility). Here, I'm looking for at least 70% probability of profit setups and -- for defined risk -- greater than one-third the width of the widest wing in credit. Look to put these plays on in the waning hours of the session immediately before the announcement and take profit for short strangles and iron condors at 50% of the credit received; 25% for short straddles/flies.

NFLX: Announces Monday after market close

July 28th 148/177.5 short strangle

Probability of Profit: 74%

Max Profit: $391 at the mid

Max Loss/Buying Power Effect: Undefined

Break Evens: 144.09/181.41 (> 1 SD, both sides)

July 28th 141/146/175/180 iron condor

Probability of Profit: 68%

Max Profit: $169 at the mid

Max Loss/Buying Power Effect: $331

Break Evens: 144.31/176.69 (> 1 SD put side, slightly less than 1 SD call)

IBM: Announces Tuesday After Market Close

July 28th 149/160 short strangle

Probability of Profit: 69%

Max Profit: $251 at the mid

Max Loss/Buying Power Effect: Undefined

Break Evens: 146.49/162.51 (at 1 SD, both sides)

July 28th 144/147/162.5/165 iron condor

Probability of Profit: 71%

Max Profit: $68 at the mid

Max Loss/Buying Power Effect: $232

Break Evens: 146.32/163.18 (at 1 SD, put side; > 1 SD call)

Notes: The iron condor is probably not worth it, given the fact that you're being paid less than 1/3rd the width of the strikes in credit for a 70% probability of profit setup.

CSX: Announces on Tuesday After Market Close

July 28th 53/57.5 short strangle

Probability of Profit: --

Max Profit: $96 at the mid

Max Loss/Buying Power Effect: Undefined

Break Evens: 52.04/58.46

Notes: For some reason, my platform isn't generating probability of profit metrics for this setup. The short strangle is likely to be around 70% with 1 SD break evens; given the fact that the short strangle is only paying $96, there is no way an iron condor with a >70% probability of profit would pay that, so it's not set out here. The defined risk alternative is to go iron fly: July 28th 51/55/55/59, Probability of Profit: 50%, Max Profit: $212 at the mid; Max Loss/Buying Power Effect: $188; Break Evens: 52.88/57.12 (expected move, both sides). In spite of the 50% probability of profit, not too shabby with reward/risk, since you're risking about one to make one.

EBAY: Announces Thursday After Market Close

July 28th 35/39 short strangle

Probability of Profit: 70%

Max Profit: $93 at the mid

Max Loss/Buying Power Effect: Undefined

Break Evens: 34.07/39.93 (at 1 SD, both sides)

Notes: As with the CSX play, there's no way a 70% probability of profit defined risk iron condor will pay 1/3rd the width of the widest wing if the short strangle's only paying .93. Again, the alternative is go iron fly: July 28th 33/37/37/41, Probability of Profit: 50%; $210 at the mid; Max Loss/Buying Power Effect: $190; Break Evens: 34.90/39.10 (expected move, both sides).

MSFT: Announces Thursday After Market Close

July 28th 70/75.5 short strangle

Probability of Profit: 70%

Max Profit: $118 at the mid

Max Loss/Buying Power Effect: Undefined

Break Evens: 68.82/76.68 (1 SD, both sides)

July 28th 67/70/75.5/78.5 iron condor

Probability of Profit: 66%

Max Profit: $86 at the mid

Max Loss/Buying Power Effect: $214

Break Evens: 69.14/76.36

Notes: The iron condor's payout is on the edge of being worthwhile; implied volatility would need to ramp up a little bit running into earnings.

EBAYOur preference: bullish as long as 33.2 is support with goal 36.6.

Alternative Scenario: The 33.2 will be depressed, triggering a return to 32.2 and then 31.6.

Comment: The RSI is greater than 50. The MACD is positive and below its signal line. A correction could occur. Additionally, prices are below their moving average 20 (34.7285) but above their moving average 50 (34.0411).

SHOP Shopify has too much movement, can it continue?SHOP, crushed earnings and is an amazing position for the future of e-comerce with its FB & AMZN partnership.

With it being a Canadian company we could see....

- an increase in investor awareness of the company

- possible takeover/merger (eBay might buy SHOP???)

- lots of growth on a Small cap stock of mkt. cap - $8 Bil.

- I've held since 4/10/17 sitting on ~20% Gains

Ebay Bearish Trade due to normal pullbacksIt is normal for the market to make corrections when things get to high up and for people to start profit taking once earnings are announced. I know ebay as a stock that is volatile when it comes to earnings. So due to the big upswing this has been in it is natural to expect a downward swing to come bring others to reality. It can always go against me, that I do know. But I believe the chances of me winning out weight the chances of me losing on this trade which is a bearish credit spread with a credit taken in of $105.01 after commissions with this particular trade I went ahead and loaded up twice on the same trade so I took in around $209. With a risk of around $188, and max return of $209. Wish me luck. This strategy will set the precedent for the Macy's trade I have outlined in my "ideas" section on tradingview. I told my significant other that I am a bit afraid of this trade going against me because it is ecommerce, and I believe so much in ecommerce that I find this risky to bet against. BUT in the short term (which is what i'm doing) I would believe this can go down on earnings.

EBAY building a baseI'm kinda biased on the long side for EBAY but let's just wait until it breaks out of this pivot at 34.05 with supporting volume before taking any action.

EBAY short on strong MACD, Force Index divergencesStrong bearish divergence on weekly MACD and Force Index. Bulls have lost steam at the upper line of the 8 year-old channel, while impulse system has turned blue, thus letting us sell. Entry -$33.83. Stop is at $34.67, target - $30.48

THE WEEK AHEAD: EARNINGS TAKE THE STAGEYou wouldn't have known it last week with all the inauguration hoopla, but we're in earnings season. Now that the hoopla's in the rear view mirror, earnings will take the market stage (and, yes, a bit of digesting of what all "the hoopla" meant).

SPY et al. (Broad Market)

From a premium seller's perspective, "SPY and friends" continues to be an unproductive area in which to sell premium unless you're willing to go out farther in time. (See SPY April Iron Condor Trade Idea, below).

Earnings

There are some "big names" coming up this week (BABA, MSFT, CAT), but not all currently have the metrics that would make premium selling hugely productive (>70% implied volatility rank/>50% implied volatality). I'm keeping an eye on BABA, EBAY, and SBUX, but their implied volatility needs to pop a bit before I'm willing to play.

Non-Earnings

GDXJ remains the only non-earnings underlying with decent liquidity and the right volatility metrics for a play. I already have one on. (See GDXJ Post Below).

VIX/VIX Derivatives

Any way, you cut it, VIX is low here, having caved mightily into Friday's opex close to sub-12.

Consequently, I'm loathe to pile into further VIX "Term Structure" trades here, since I already have a March 16/19 short call vert on, as well as April 17/20, and I could easily see a modest (or not so modest) VIX rise to 14.0-ish (what the Feb /VX future is currently trading at) if the market gets indigestion processing what exactly "Trump World" will look like going forward ... .