Gbp-jpy

possible GBP/JPY sellHere is my analysis on GBP/JPY.

Price has come up to the daily golden pocket zone, now made a choch.

I'm now waiting for a possible lower low (bos) to be formed and then a possible mitigation from the 30 minute supply zone

( 163.320 ) for a possible sell entry.

potential 100 pip reward to downside, targeting the 1 hour demand at 162.408

please like and subscribe to help grow this channel.

have a great week trading!

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: WEAK BEARISH

1. Monetary Policy

At their May meeting, the BoE delivered on expectations by raising the bank rate by 25bsp to 1.0%. There was an initial hawkish surprise as the vote split was 9-0 (no dissent from Cunliffe) and 3 of the 9 MPC members voted for a 50bsp move at the meeting. However, the hawkish reaction soon faded as it was also revealed that 2 of the 6 members who voted for a hike thought that this marked the end of the current hiking cycle. The dovishness didn’t stop there though as the BoE revised up their forecasts for peak inflation to >10% which added to the stagflation fears as the bank also saw possible GDP contraction in 2023. Furthermore, the bank took their first real stab at overly aggressive STIR pricing for the 2022 rate path by saying the current path would imply a big undershoot of their 2% inflation target in 2023 and was later backed up by Governor Bailey who said even though he thought rates should continue to rise he didn’t agree with those who think the MPC should be raising interest rates by a lot more. As the bank rate was raised to 1.0%, the markets expected some clarity from the bank on their plans to reduce the balance sheet . However, the bank decided to play for more time and said the bank will provide an update on their plans at the August meeting, pushing back expectations of active QT from Q2 to Q3. As a result of the overall dovish tone, Sterling fell to its lowest levels since 1Q21. The meeting confirmed market calls that the bank would look to hold rates steady after reaching 1.50%.

2. Economic & Health Developments

With inflation the main reason for the BoE’s recent rate hikes, there is a concern that the UK economy faces stagflation risk, as price pressures stay sticky while growth decelerates. That also means that current market expectations for rates continues to look too aggressive even after the BoE’s recent push back. This means downside risks for GBP if growth data push lower and/or the BoE continue to push their recent dovish tone.

3. Political Developments

Political uncertainty is usually GBP negative, so the PM’s future remains a risk. If distrust grows question remains on whether a no-confidence vote can happen (if so, short-term downside is likely), and whether he can survive the vote (a win should be GBP positive and a loss GBP negative). The Northern Ireland protocol remains a focus, with previous UK threats to trigger Article 16 and EU threats to terminate the Brexit deal if they do. Markets have rightly ignored this as posturing, but any actual escalation can see sharp GBP downside.

4. CFTC Analysis

Mostly mixed signals from positioning data again, but with aggregate positioning still well below 1 standard dev from the 15-year mean GBP looks stretched. Even though the outlook for Sterling shifted to weak bearish from neutral, positioning means we are not too excited to chase the Pound lower from here.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Monetary Policy

The BoJ kept all policy settings unchanged at their April meeting, which was in line with broad consensus expectations, but given the price action after the event did imply that a sizeable chunk of the market was expecting something more (us included). Due to the JPY weakness in recent weeks, markets wanted to see whether the bank would potentially increase their Yield Curve Control target band from 0.25%--0.25% to 0.50%--0.50%. But the bank decided to stick to their guns and maintain their ultra-easy policy despite the rapid depreciation of the JPY. The bank doubled down by saying they will conduct special open market operations on every working day as needed to keep the 10-year GBP capped at 0.25%. As expected, the bank reiterated their view that rates will stay low for the foreseeable future and won’t hesitate to add stimulus if the economy needs it. On the JPY, Gov Kuroda made familiar comments by saying they desire stable currency moves which reflect economic fundamentals. As a result of the bank’s inaction, all eyes will now be on the MoF to intervene if the rapid depreciation of the JPY continues.

2. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is usually the primary driver. Economic data rarely proves market moving, and although monetary policy expectations can affect the JPY in the short-term, safe-haven flows are typically more dominant. Even though the market’s overall risk tone saw a huge recovery and risk-on frenzy from the middle of 2020 to the end of 2021, recent developments have increased risks. With central banks tightening policy into an economic slowdown, risk appetite has soured. Even though that doesn’t change our med-term bias for the JPY, it does mean we should expect more risk sentiment ebbs and flows this year, and the heightened volatility can create strong directional moves in the JPY, as long as yields play their part.

3. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares a strong inverse correlation to moves in US yield differentials. Like most correlations, the strength of the inverse correlation between the JPY and US10Y isn’t perfect and will ebb and flow depending on the market environment from both a risk and cycle point of view. With the Fed tilting more aggressive and targeting demand, we expect U10Y to push lower in weeks ahead (especially as inflation tops out). If that happens there could be mild upside risks for the JPY if US10Y corrects, but we shouldn’t look at that in isolation and also weigh it alongside risk sentiment and demand for the USD.

4. CFTC Analysis

Another bullish signal from JPY positioning as net-shorts decreased across all three participants once again. With aggregate JPY positioning close to 2 standard deviationsfrom its 15-year mean, the risk to reward to chase the JPY lower from here is not very attractive. Last week saw some additional correction in JPY pairs, but without a more substantial reason for US10Y to push lower the attractiveness to buy the JPY is limited as well.

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: WEAK BEARISH

1. Monetary Policy

At their May meeting, the BoE delivered on expectations by raising the bank rate by 25bsp to 1.0%. There was an initial hawkish surprise as the vote split was 9-0 (no dissent from Cunliffe) and 3 of the 9 MPC members voted for a 50bsp move at the meeting. However, the hawkish reaction soon faded as it was also revealed that 2 of the 6 members who voted for a hike thought that this marked the end of the current hiking cycle. The dovishness didn’t stop there though as the BoE revised up their forecasts for peak inflation to >10% which added to the stagflation fears as the bank also saw possible GDP contraction in 2023. Furthermore, the bank took their first real stab at overly aggressive STIR pricing for the 2022 rate path by saying the current path would imply a big undershoot of their 2% inflation target in 2023 and was later backed up by Governor Bailey who said even though he thought rates should continue to rise he didn’t agree with those who think the MPC should be raising interest rates by a lot more. As the bank rate was raised to 1.0%, the markets expected some clarity from the bank on their plans to reduce the balance sheet . However, the bank decided to play for more time and said the bank will provide an update on their plans at the August meeting, pushing back expectations of active QT from Q2 to Q3. As a result of the overall dovish tone, Sterling fell to its lowest levels since 1Q21. The meeting confirmed market calls that the bank would look to hold rates steady after reaching 1.50%.

2. Economic & Health Developments

With inflation the main reason for the BoE’s recent rate hikes, there is a concern that the UK economy faces stagflation risk, as price pressures stay sticky while growth decelerates. That also means that current market expectations for rates continues to look too aggressive even after the BoE’s recent push back. This means downside risks for GBP if growth data push lower and/or the BoE continue to push their recent dovish tone.

3. Political Developments

Political uncertainty is usually GBP negative, so the PM’s future remains a risk. If distrust grows question remains on whether a no-confidence vote can happen (if so, short-term downside is likely), and whether he can survive the vote (a win should be GBP positive and a loss GBP negative). The Northern Ireland protocol remains a focus, with previous UK threats to trigger Article 16 and EU threats to terminate the Brexit deal if they do. Markets have rightly ignored this as posturing, but any actual escalation can see sharp GBP downside.

4. CFTC Analysis

Mostly mixed signals from positioning data again, but with aggregate positioning still well below 1 standard dev from the 15-year mean GBP looks stretched. Even though the outlook for Sterling shifted to weak bearish from neutral, positioning means we are not too excited to chase the Pound lower from here.

5. The Week Ahead

It will be an extremely light week ahead for Sterling with no tier 1 data point, but we also have UK bank holidays on Thursday and Friday as well. All of that means that there will be very little to drive Sterling this week and given the thinner liquidity and lower volume it could be a choppy week. Sterling’s med-term outlook remains weak bearish , but the currency has been stretched to the downside at the index level. That means we are not too keen on looking for opportunities to short the currency until we see some upside we can use to sell in to. Brexit will be in focus, where recent threats of terminating the Brexit deal has been rightly seen as posturing, but if any side goes through with their recent threats that could open up a decent EURGBP buy opportunity regardless of stretched positioning.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Monetary Policy

The BoJ kept all policy settings unchanged at their April meeting, which was in line with broad consensus expectations, but given the price action after the event did imply that a sizeable chunk of the market was expecting something more (us included). Due to the JPY weakness in recent weeks, markets wanted to see whether the bank would potentially increase their Yield Curve Control target band from 0.25%--0.25% to 0.50%--0.50%. But the bank decided to stick to their guns and maintain their ultra-easy policy despite the rapid depreciation of the JPY. The bank doubled down by saying they will conduct special open market operations on every working day as needed to keep the 10-year GBP capped at 0.25%. As expected, the bank reiterated their view that rates will stay low for the foreseeable future and won’t hesitate to add stimulus if the economy needs it. On the JPY, Gov Kuroda made familiar comments by saying they desire stable currency moves which reflect economic fundamentals. As a result of the bank’s inaction, all eyes will now be on the MoF to intervene if the rapid depreciation of the JPY continues.

2. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is usually the primary driver. Economic data rarely proves market moving, and although monetary policy expectations can affect the JPY in the short-term, safe-haven flows are typically more dominant. Even though the market’s overall risk tone saw a huge recovery and risk-on frenzy from the middle of 2020 to the end of 2021, recent developments have increased risks. With central banks tightening policy into an economic slowdown, risk appetite has soured. Even though that doesn’t change our med-term bias for the JPY, it does mean we should expect more risk sentiment ebbs and flows this year, and the heightened volatility can create strong directional moves in the JPY, as long as yields play their part.

3. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares a strong inverse correlation to moves in US yield differentials. Like most correlations, the strength of the inverse correlation between the JPY and US10Y isn’t perfect and will ebb and flow depending on the market environment from both a risk and cycle point of view. With the Fed tilting more aggressive and targeting demand, we expect U10Y to push lower in weeks ahead (especially as inflation tops out). If that happens there could be mild upside risks for the JPY if US10Y corrects, but we shouldn’t look at that in isolation and also weigh it alongside risk sentiment and demand for the USD.

4. CFTC Analysis

Another bullish signal from JPY positioning as net-shorts decreased across all three participants once again. With aggregate JPY positioning close to 2 standard deviationsfrom its 15-year mean, the risk to reward to chase the JPY lower from here is not very attractive. Last week saw some additional correction in JPY pairs, but without a more substantial reason for US10Y to push lower the attractiveness to buy the JPY is limited as well.

5. The Week Ahead

For the week ahead, the focus will remain on the key drivers which is US10Y and more recently risk sentiment. With CPI starting to inch higher in Japan, there have been some speculation that the BoJ could make a move on policy in the months ahead. Until last week majority of participants expected a bigger YCC target band to be the preferred policy option, but after BoJ Kuroda’s comments last week it seems like a possible rate hike does not seem out of the question anymore. Any further hawkish comments from the BoJ will be closely watched in the sessions ahead. Given the move in yield differentials and commodity prices, the JPY had very little safe haven appeal as US10Y was making fresh cycle highs, but as US10Y have started to slow its assent, we’ve seen some classic safe haven demand for the JPY in the past few weeks. This means, apart from the regular focus on US10Y, we’ll also be paying attention to any sharp moves in risk sentiment as well. Apart from that, eyes will also be on any jawboning from Japanese officials where the BoJ has placed the ball firmly in the MoF’s court to try and curb JPY depreciation. With the recent safe haven demand seeing some inflows into the JPY, as well as the hawkish comments from the BoJ, it seems like jawboning might not be around the corner.

Entry GBPJPY Buy 01/06/2022Details on chart - entry once price closed bullish on the 15m with triple wick rejection

GBPJPY ShortHey traders, in today's trading session we are monitoring GBPJPY for a selling opportunity around 162.3 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

GBPJPY PRETTY SIMPLELooking like a simple reversal pattern. Inverse head and shoulders. Currently the neckline has been broken and we look to revisit highs.

GBPJPY VIP SHORT! (890pips!)GBPJPY SHORT

Why are we entering?

- Expecting JPY strength & GBP weakness

- We are waiting for rejection from our structure level and trendline

What is our confirmation?

- Break of RISK trendline and WFB

- Rejection from structure and trendline

Entry

- Safe Entry: Break of RISK trendline & Rejection from structure and trendline

- RISK Entry: Rejection from structure and trendline

- RISK Entry 2: Early break of RISK trendline

Once entered, where will our Stoploss be?

- Above structure & trendline (161.7) 30 pips

- Move SL to BE after running 30 pips

Where do we take profits?

- Secure profit multiple times along the way (30 pips, 60 pips, 120 pips, 200 pips)

- First TP previous low :155.9 (530pips)

- Final TP: If structure breaks, 152.4 (890pips)

GBPJPY ShortHey traders, in the coming week we are monitoring GBPJPY for a selling opportunity around 160.5 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: WEAK BEARISH

1. Monetary Policy

At their May meeting, the BoE delivered on expectations by raising the bank rate by 25bsp to 1.0%. There was an initial hawkish surprise as the vote split was 9-0 (no dissent from Cunliffe) and 3 of the 9 MPC members voted for a 50bsp move at the meeting. However, the hawkish reaction soon faded as it was also revealed that 2 of the 6 members who voted for a hike thought that this marked the end of the current hiking cycle. The dovishness didn’t stop there though as the BoE revised up their forecasts for peak inflation to >10% which added to the stagflation fears as the bank also saw possible GDP contraction in 2023. Furthermore, the bank took their first real stab at overly aggressive STIR pricing for the 2022 rate path by saying the current path would imply a big undershoot of their 2% inflation target in 2023 and was later backed up by Governor Bailey who said even though he thought rates should continue to rise he didn’t agree with those who think the MPC should be raising interest rates by a lot more. As the bank rate was raised to 1.0%, the markets expected some clarity from the bank on their plans to reduce the balance sheet . However, the bank decided to play for more time and said the bank will provide an update on their plans at the August meeting, pushing back expectations of active QT from Q2 to Q3. As a result of the overall dovish tone, Sterling fell to its lowest levels since 1Q21. The meeting confirmed market calls that the bank would look to hold rates steady after reaching 1.50%.

2. Economic & Health Developments

With inflation the main reason for the BoE’s recent rate hikes, there is a concern that the UK economy faces stagflation risk, as price pressures stay sticky while growth decelerates. That also means that current market expectations for rates continues to look too aggressive even after the BoE’s recent push back. This means downside risks for GBP if growth data push lower and/or the BoE continue to push their recent dovish tone.

3. Political Developments

Political uncertainty is usually GBP negative, so the PM’s future remains a risk. If distrust grows question remains on whether a no-confidence vote can happen (if so, short-term downside is likely), and whether he can survive the vote (a win should be GBP positive and a loss GBP negative). The Northern Ireland protocol remains a focus, with previous UK threats to trigger Article 16 and EU threats to terminate the Brexit deal if they do. Markets have rightly ignored this as posturing, but any actual escalation can see sharp GBP downside.

4. CFTC Analysis

Mixed signals from positioning, but aggregate positioning (large specs, leveraged funds & asset managers) is still below 1 standard dev from the 15-year mean. Even though the outlook for Sterling shifted to weak bearish from neutral following the recent BoE meeting, we don’t want to chase the GBP lower from here.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Monetary Policy

The BoJ kept all policy settings unchanged at their April meeting, which was in line with broad consensus expectations, but given the price action after the event did imply that a sizeable chunk of the market was expecting something more (us included). Due to the JPY weakness in recent weeks, markets wanted to see whether the bank would potentially increase their Yield Curve Control target band from 0.25%--0.25% to 0.50%--0.50%. But the bank decided to stick to their guns and maintain their ultra-easy policy despite the rapid depreciation of the JPY. The bank doubled down by saying they will conduct special open market operations on every working day as needed to keep the 10-year GBP capped at 0.25%. As expected, the bank reiterated their view that rates will stay low for the foreseeable future and won’t hesitate to add stimulus if the economy needs it. On the JPY, Gov Kuroda made familiar comments by saying they desire stable currency moves which reflect economic fundamentals. As a result of the bank’s inaction, all eyes will now be on the MoF to intervene if the rapid depreciation of the JPY continues.

2. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is usually the primary driver. Economic data rarely proves market moving, and although monetary policy expectations can affect the JPY in the short-term, safe-haven flows are typically more dominant. Even though the market’s overall risk tone saw a huge recovery and risk-on frenzy from the middle of 2020 to the end of 2021, recent developments have increased risks. With central banks tightening policy into an economic slowdown, risk appetite has soured. Even though that doesn’t change our med-term bias for the JPY, it does mean we should expect more risk sentiment ebbs and flows this year, and the heightened volatility can create strong directional moves in the JPY, as long as yields play their part.

3. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares a strong inverse correlation to moves in US yield differentials. Like most correlations, the strength of the inverse correlation between the JPY and US10Y isn’t perfect and will ebb and flow depending on the market environment from both a risk and cycle point of view. With the Fed tilting more aggressive and targeting demand, we expect U10Y to push lower in weeks ahead (especially as inflation tops out). If that happens there could be mild upside risks for the JPY if US10Y corrects, but we shouldn’t look at that in isolation and also weigh it alongside risk sentiment and demand for the USD.

4. CFTC Analysis

A bullish signal from JPY positioning as net-shorts decreased across all three participants. With aggregate JPY positioning still close to 2 standard deviations away from a 15-year mean, the risk to reward to chase the currency lower from here is not very attractive. Last week saw some additional correction in JPY pairs, but without a more substantial reason for US10Y to push lower the attractiveness to buy the JPY is limited.

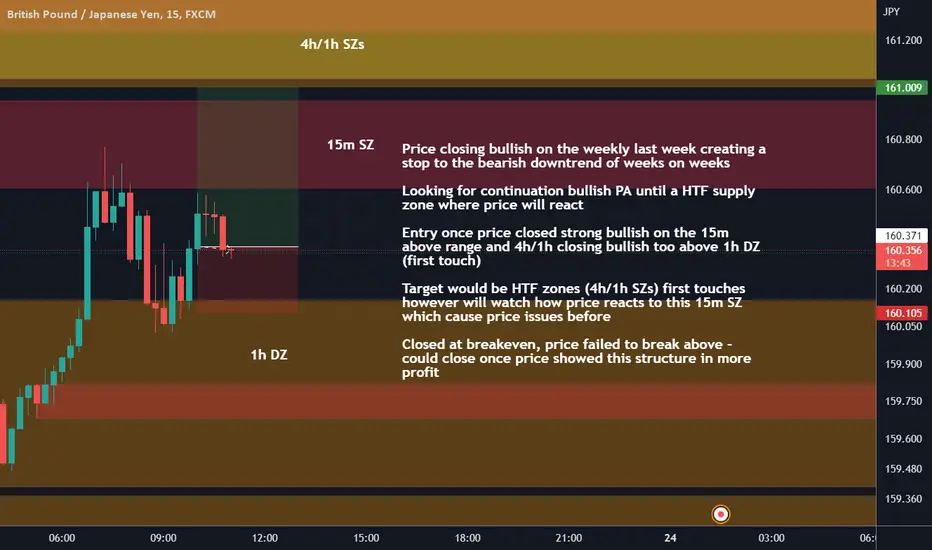

GBPJPY ShortHey traders, in today's trading session we are monitoring GBPJPY for a selling opportunity around 160.3 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: WEAK BEARISH

1. Monetary Policy

At their May meeting, the BoE delivered on expectations by raising the bank rate by 25bsp to 1.0%. There was an initial hawkish surprise as the vote split was 9-0 (no dissent from Cunliffe) and 3 of the 9 MPC members voted for a 50bsp move at the meeting. However, the hawkish reaction soon faded as it was also revealed that 2 of the 6 members who voted for a hike thought that this marked the end of the current hiking cycle. The dovishness didn’t stop there though as the BoE revised up their forecasts for peak inflation to >10% which added to the stagflation fears as the bank also saw possible GDP contraction in 2023. Furthermore, the bank took their first real stab at overly aggressive STIR pricing for the 2022 rate path by saying the current path would imply a big undershoot of their 2% inflation target in 2023 and was later backed up by Governor Bailey who said even though he thought rates should continue to rise he didn’t agree with those who think the MPC should be raising interest rates by a lot more. As the bank rate was raised to 1.0%, the markets expected some clarity from the bank on their plans to reduce the balance sheet . However, the bank decided to play for more time and said the bank will provide an update on their plans at the August meeting, pushing back expectations of active QT from Q2 to Q3. As a result of the overall dovish tone, Sterling fell to its lowest levels since 1Q21. The meeting confirmed market calls that the bank would look to hold rates steady after reaching 1.50%.

2. Economic & Health Developments

With inflation the main reason for the BoE’s recent rate hikes, there is a concern that the UK economy faces stagflation risk, as price pressures stay sticky while growth decelerates. That also means that current market expectations for rates continues to look too aggressive even after the BoE’s recent push back. This means downside risks for GBP if growth data push lower and/or the BoE continue to push their recent dovish tone.

3. Political Developments

Political uncertainty is usually GBP negative, so the PM’s future remains a risk. If distrust grows question remains on whether a no-confidence vote can happen (if so, short-term downside is likely), and whether he can survive the vote (a win should be GBP positive and a loss GBP negative). The Northern Ireland protocol remains a focus, with previous UK threats to trigger Article 16 and EU threats to terminate the Brexit deal if they do. Markets have rightly ignored this as posturing, but any actual escalation can see sharp GBP downside.

4. CFTC Analysis

Mixed signals from positioning, but aggregate positioning (large specs, leveraged funds & asset managers) is still below 1 standard dev from the 15-year mean. Even though the outlook for Sterling shifted to weak bearish from neutral following the recent BoE meeting, we don’t want to chase the GBP lower from here.

5. The Week Ahead

After last week’s busy data schedule, the calendar is much lighter this week with flash PMIs the only real event of note for Sterling. Retail Sales was an interesting print for the UK. Even though there is very little to celebrate with a -4.9% YY print, all four measures printed much higher than expected. With Sterling still so tactically stretched to the downside, a surprising positive beat in PMIs could offer some tradable upside for Sterling in the short-term. Sterling’s med-term outlook remains weak bearish , but the currency has been stretched to the downside at the index level, and another positive surprise could offer attractive upside. That also means that we won’t be too interested in getting back on the long side of EURGBP just yet. Brexit will also be in focus, where recent threats of terminating the Brexit deal has been rightly seen as posturing, but if any side goes through with their recent threats that could open up a decent EURGBP buy opportunity regardless ofstretched positive for the Pound.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Monetary Policy

The BoJ kept all policy settings unchanged at their April meeting, which was in line with broad consensus expectations, but given the price action after the event did imply that a sizeable chunk of the market was expecting something more (us included). Due to the JPY weakness in recent weeks, markets wanted to see whether the bank would potentially increase their Yield Curve Control target band from 0.25%--0.25% to 0.50%--0.50%. But the bank decided to stick to their guns and maintain their ultra-easy policy despite the rapid depreciation of the JPY. The bank doubled down by saying they will conduct special open market operations on every working day as needed to keep the 10-year GBP capped at 0.25%. As expected, the bank reiterated their view that rates will stay low for the foreseeable future and won’t hesitate to add stimulus if the economy needs it. On the JPY, Gov Kuroda made familiar comments by saying they desire stable currency moves which reflect economic fundamentals. As a result of the bank’s inaction, all eyes will now be on the MoF to intervene if the rapid depreciation of the JPY continues.

2. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is usually the primary driver. Economic data rarely proves market moving, and although monetary policy expectations can affect the JPY in the short-term, safe-haven flows are typically more dominant. Even though the market’s overall risk tone saw a huge recovery and risk-on frenzy from the middle of 2020 to the end of 2021, recent developments have increased risks. With central banks tightening policy into an economic slowdown, risk appetite has soured. Even though that doesn’t change our med-term bias for the JPY, it does mean we should expect more risk sentiment ebbs and flows this year, and the heightened volatility can create strong directional moves in the JPY, as long as yields play their part.

3. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares a strong inverse correlation to moves in US yield differentials. Like most correlations, the strength of the inverse correlation between the JPY and US10Y isn’t perfect and will ebb and flow depending on the market environment from both a risk and cycle point of view. With the Fed tilting more aggressive and targeting demand, we expect U10Y to push lower in weeks ahead (especially as inflation tops out). If that happens there could be mild upside risks for the JPY if US10Y corrects, but we shouldn’t look at that in isolation and also weigh it alongside risk sentiment and demand for the USD.

4. CFTC Analysis

A bullish signal from JPY positioning as net-shorts decreased across all three participants. With aggregate JPY positioning still close to 2 standard deviations away from a 15-year mean, the risk to reward to chase the currency lower from here is not very attractive. Last week saw some additional correction in JPY pairs, but without a more substantial reason for US10Y to push lower the attractiveness to buy the JPY is limited.

5. The Week Ahead

For the week ahead, the focus will remain on the key drivers which is US10Y and more recently risk sentiment, but CPI data could also be interesting. With CPI starting to inch higher in Japan, there have been some speculation that the BoJ could make a move on policy in the months ahead. Rate hikes seems out of the question at this stage but extending the yield curve control range would make sense. JP10Y have been staying very close to the upper range at 0.25%, and a higher-than-expected CPI print could put more pressure on the BoJ to act. Given the move in yield differentials and commodity prices, the JPY had very little safe haven appeal over recent weeks, but that was not the case in the past few weeks where we saw some classic safe haven demand for the JPY. This means, apart from the regular focus on US10Y , we’ll also be paying attention to any sharp moves in risk sentiment. Apart from that, eyes will also be on any jawboning from Japanese officials where the BoJ has placed the ball firmly in the MoF’s court to try and curb JPY depreciation. With the recent safe haven demand seeing some inflows into the JPY, that might give Japanese officials some solace and could mean more patience from their side regarding recent JPY weakness.

GBPJPY on a short move 🦐GBPJPY on the 4h chart after the last retracement reached the 0.5 Fibonacci level over a daily support.

The price can now look for a lower low to the downside below the support structure.

How can i approach this scenario?

I will wait for the possible break of the support level and at that stage, i will look for a possible entry point to set a nice short order according to the Plancton's strategy rules.

-----

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: WEAK BEARISH

1. Monetary Policy

At their May meeting, the BoE delivered on expectations by raising the bank rate by 25bsp to 1.0%. There was an initial hawkish surprise as the vote split was 9-0 (no dissent from Cunliffe) and 3 of the 9 MPC members voted for a 50bsp move at the meeting. However, the hawkish reaction soon faded as it was also revealed that 2 of the 6 members who voted for a hike thought that this marked the end of the current hiking cycle. The dovishness didn’t stop there though as the BoE revised up their forecasts for peak inflation to >10% which added to the stagflation fears as the bank also saw possible GDP contraction in 2023. Furthermore, the bank took their first real stab at overly aggressive STIR pricing for the 2022 rate path by saying the current path would imply a big undershoot of their 2% inflation target in 2023 and was later backed up by Governor Bailey who said even though he thought rates should continue to rise he didn’t agree with those who think the MPC should be raising interest rates by a lot more. As the bank rate was raised to 1.0%, the markets expected some clarity from the bank on their plans to reduce the balance sheet. However, the bank decided to play for more time and said the bank will provide an update on their plans at the August meeting, pushing back expectations of active QT from Q2 to Q3. As a result of the overall dovish tone, Sterling fell to its lowest levels since 1Q21. The meeting confirmed market calls that the bank would look to hold rates steady after reaching 1.50%.

2. Economic & Health Developments

With inflation the main reason for the BoE’s recent rate hikes, there is a concern that the UK economy faces stagflation risk, as price pressures stay sticky while growth decelerates. That also means that current market expectations for rates continues to look too aggressive even after the BoE’s recent push back. This means downside risks for GBP if growth data push lower and/or the BoE continue to push their recent dovish tone.

3. Political Developments

Political uncertainty is usually GBP negative, so the PM’s future remains a risk. If distrust grows question remains on whether a no-confidence vote can happen (if so, short-term downside is likely), and whether he can survive the vote (a win should be GBP positive and a loss GBP negative). The Northern Ireland protocol remains a focus, with previous UK threats to trigger Article 16 and EU threats to terminate the Brexit deal if they do. Markets have rightly ignored this as posturing, but any actual escalation can see sharp GBP downside.

4. CFTC Analysis

Mixed signals from positioning, but aggregate positioning (large specs, leveraged funds & asset managers) is still below 1 standard dev from the 15-year mean. Even though the outlook for Sterling shifted to weak bearish from neutral following the recent BoE meeting, we don’t want to chase the GBP lower from here.

5. The Week Ahead

After last week’s busy data schedule, the calendar is much lighter this week with flash PMIs the only real event of note for Sterling. Retail Sales was an interesting print for the UK. Even though there is very little to celebrate with a -4.9% YY print, all four measures printed much higher than expected. With Sterling still so tactically stretched to the downside, a surprising positive beat in PMIs could offer some tradable upside for Sterling in the short-term. Sterling’s med-term outlook remains weak bearish, but the currency has been stretched to the downside at the index level, and another positive surprise could offer attractive upside. That also means that we won’t be too interested in getting back on the long side of EURGBP just yet. Brexit will also be in focus, where recent threats of terminating the Brexit deal has been rightly seen as posturing, but if any side goes through with their recent threats that could open up a decent EURGBP buy opportunity regardless ofstretched positive for the Pound.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Monetary Policy

The BoJ kept all policy settings unchanged at their April meeting, which was in line with broad consensus expectations, but given the price action after the event did imply that a sizeable chunk of the market was expecting something more (us included). Due to the JPY weakness in recent weeks, markets wanted to see whether the bank would potentially increase their Yield Curve Control target band from 0.25%--0.25% to 0.50%--0.50%. But the bank decided to stick to their guns and maintain their ultra-easy policy despite the rapid depreciation of the JPY. The bank doubled down by saying they will conduct special open market operations on every working day as needed to keep the 10-year GBP capped at 0.25%. As expected, the bank reiterated their view that rates will stay low for the foreseeable future and won’t hesitate to add stimulus if the economy needs it. On the JPY, Gov Kuroda made familiar comments by saying they desire stable currency moves which reflect economic fundamentals. As a result of the bank’s inaction, all eyes will now be on the MoF to intervene if the rapid depreciation of the JPY continues.

2. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is usually the primary driver. Economic data rarely proves market moving, and although monetary policy expectations can affect the JPY in the short-term, safe-haven flows are typically more dominant. Even though the market’s overall risk tone saw a huge recovery and risk-on frenzy from the middle of 2020 to the end of 2021, recent developments have increased risks. With central banks tightening policy into an economic slowdown, risk appetite has soured. Even though that doesn’t change our med-term bias for the JPY, it does mean we should expect more risk sentiment ebbs and flows this year, and the heightened volatility can create strong directional moves in the JPY, as long as yields play their part.

3. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares a strong inverse correlation to moves in US yield differentials. Like most correlations, the strength of the inverse correlation between the JPY and US10Y isn’t perfect and will ebb and flow depending on the market environment from both a risk and cycle point of view. With the Fed tilting more aggressive and targeting demand, we expect U10Y to push lower in weeks ahead (especially as inflation tops out). If that happens there could be mild upside risks for the JPY if US10Y corrects, but we shouldn’t look at that in isolation and also weigh it alongside risk sentiment and demand for the USD.

4. CFTC Analysis

A bullish signal from JPY positioning as net-shorts decreased across all three participants. With aggregate JPY positioning still close to 2 standard deviations away from a 15-year mean, the risk to reward to chase the currency lower from here is not very attractive. Last week saw some additional correction in JPY pairs, but without a more substantial reason for US10Y to push lower the attractiveness to buy the JPY is limited.

5. The Week Ahead

For the week ahead, the focus will remain on the key drivers which is US10Y and more recently risk sentiment, but CPI data could also be interesting. With CPI starting to inch higher in Japan, there have been some speculation that the BoJ could make a move on policy in the months ahead. Rate hikes seems out of the question at this stage but extending the yield curve control range would make sense. JP10Y have been staying very close to the upper range at 0.25%, and a higher-than-expected CPI print could put more pressure on the BoJ to act. Given the move in yield differentials and commodity prices, the JPY had very little safe haven appeal over recent weeks, but that was not the case in the past few weeks where we saw some classic safe haven demand for the JPY. This means, apart from the regular focus on US10Y, we’ll also be paying attention to any sharp moves in risk sentiment. Apart from that, eyes will also be on any jawboning from Japanese officials where the BoJ has placed the ball firmly in the MoF’s court to try and curb JPY depreciation. With the recent safe haven demand seeing some inflows into the JPY, that might give Japanese officials some solace and could mean more patience from their side regarding recent JPY weakness.

FOREX ANALYSIS : GBPJPYFX:GBPJPY

The blue and red lines mean: I think prices can return in these areas.

Green lines mean: I think the price can reach these areas. They are therefore known as transaction targets.

If you want to use this deal, please risk only one percent of your account balance.

GBPJPY 600 pips potential setups. It is heading to 154?Hey traders, in today's trading session we are monitoring GBPJPY for a long term selling opportunity around 160 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

Entry GBPJPY Buy 23/05/2022Details on chart - entry once price closed bullish on 15m with triple wick rejection

GBPJPY SHORTHellooo traders!!! Great opportunity to make some pips for the week. Wait for the order block to be taken out before you look for a really good sell. Take profit is set at the equal lows. Trade with care

GBP JPY - FUNDAMENTAL DRIVERSGBP

FUNDAMENTAL BIAS: WEAK BEARISH

1. Monetary Policy

At their May meeting, the BoE delivered on expectations by raising the bank rate by 25bsp to 1.0%. There was an initial hawkish surprise as the vote split was 9-0 (no dissent from Cunliffe) and 3 of the 9 MPC members voted for a 50bsp move at the meeting. However, the hawkish reaction soon faded as it was also revealed that 2 of the 6 members who voted for a hike thought that this marked the end of the current hiking cycle. The dovishness didn’t stop there though as the BoE revised up their forecasts for peak inflation to >10% which added to the stagflation fears as the bank also saw possible GDP contraction in 2023. Furthermore, the bank took their first real stab at overly aggressive STIR pricing for the 2022 rate path by saying the current path would imply a big undershoot of their 2% inflation target in 2023 and was later backed up by Governor Bailey who said even though he thought rates should continue to rise he didn’t agree with those who think the MPC should be raising interest rates by a lot more. As the bank rate was raised to 1.0%, the markets expected some clarity from the bank on their plans to reduce the balance sheet . However, the bank decided to play for more time and said the bank will provide an update on their plans at the August meeting, pushing back expectations of active QT from Q2 to Q3. As a result of the overall dovish tone, Sterling fell to its lowest levels since 1Q21. The meeting confirmed market calls that the bank would look to hold rates steady after reaching 1.50%.

2. Economic & Health Developments

With inflation the main reason for the BoE’s recent rate hikes, there is a concern that the UK economy faces stagflation risk, as price pressures stay sticky while growth decelerates. That also means that current market expectations for rates continues to look too aggressive even after the BoE’s recent push back. This means downside risks for GBP if growth data push lower and/or the BoE continue to push their recent dovish tone.

3. Political Developments

Political uncertainty is usually GBP negative, so the PM’s future remains a risk. If distrust grows question remains on whether a no-confidence vote can happen (if so, short-term downside is likely), and whether he can survive the vote (a win should be GBP positive and a loss GBP negative). The Northern Ireland protocol remains a focus, with previous UK threats to trigger Article 16 and EU threats to terminate the Brexit deal if they do. Markets have rightly ignored this as posturing, but any actual escalation can see sharp GBP downside.

4. CFTC Analysis

Overall bearish signal as aggregate net-short positioning increased, pushing aggregate positioning (large specs, leveraged funds & asset managers) further below 1 standard dev from the 15-year mean. Even though the outlook for Sterling shifted to weak bearish from Neutral following the recent BoE meeting, we don’t want to chase the GBP lower from here. Not with both price action and positioning looking tactically stretched.

JPY

FUNDAMENTAL BIAS: BEARISH

1. Monetary Policy

The BoJ kept all policy settings unchanged at their April meeting, which was in line with broad consensus expectations, but given the price action after the event did imply that a sizeable chunk of the market was expecting something more (us included). Due to the JPY weakness in recent weeks, markets wanted to see whether the bank would potentially increase their Yield Curve Control target band from 0.25%--0.25% to 0.50%--0.50%. But the bank decided to stick to their guns and maintain their ultra-easy policy despite the rapid depreciation of the JPY. The bank doubled down by saying they will conduct special open market operations on every working day as needed to keep the 10-year GBP capped at 0.25%. As expected, the bank reiterated their view that rates will stay low for the foreseeable future and won’t hesitate to add stimulus if the economy needs it. On the JPY, Gov Kuroda made familiar comments by saying they desire stable currency moves which reflect economic fundamentals. As a result of the bank’s inaction, all eyes will now be on the MoF to intervene if the rapid depreciation of the JPY continues.

2. Safe-haven status and overall risk outlook

As a safe-haven currency, the market's risk outlook is usually the primary driver. Economic data rarely proves market moving, and although monetary policy expectations can affect the JPY in the short-term, safe-haven flows are typically more dominant. Even though the market’s overall risk tone saw a huge recovery and risk-on frenzy from the middle of 2020 to the end of 2021, recent developments have increased risks. With central banks tightening policy into an economic slowdown, risk appetite has soured. Even though that doesn’t change our med-term bias for the JPY, it does mean we should expect more risk sentiment ebbs and flows this year, and the heightened volatility can create strong directional moves in the JPY, as long as yields play their part.

3. Low-yielding currency with inverse correlation to US10Y

As a low yielding currency, the JPY usually shares a strong inverse correlation to moves in US yield differentials. Like most correlations, the strength of the inverse correlation between the JPY and US10Y isn’t perfect and will ebb and flow depending on the market environment from both a risk and cycle point of view. With the Fed tilting more aggressive and targeting demand, we expect U10Y to push lower in weeks ahead (especially as inflation tops out). If that happens there could be mild upside risks for the JPY if US10Y corrects, but we shouldn’t look at that in isolation and also weigh it alongside risk sentiment and demand for the USD.

4. CFTC Analysis

Increase in Large Spec & Asset Manager net-shorts, but some reduction from Leveraged Fund net-shorts. With aggregate JPY positioning still close to 2 standard deviations away from a 15-year mean, the risk to reward to chase the currency lower from here is not very attractive. Last week saw some overdue correction in JPY pairs, but without a more substantial reason for US10Y to push lower the attractiveness to buy the JPY is limited.

GBPJPY ShortHey traders, in the coming week we are monitoring GBPJPY for a selling opportunity around 159.8 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.