So... What is next? Shortest recession in play?Stock market - Against all odds, S&P index has risen almost 32% since hitting a low for the year on March 23. The fact that it happened after a ferocious plunge of 35% between Feb. 20 and March 23, the most devastating sell-off since the great depression, made the feat even more remarkable.

As a matter of fact, the market posted its best quarter since 1998, with Nasdaq leading the way by soaring 30.6% for the quarter, the most since 1999.

Some speculated that the fast recovery was due to the big outflow of money from the fixed-income market into the stock market as emerging market fails to meet its debt obligation.

Others credited young investors (medium age of 31) on Robinhood (3 millions user added 2020, 13 millions total) with stock market's spectacular rally.

I personally doubt that the combined purchasing power of all Robinhood users is strong enough to sway the stock market.

Nonetheless, the stock market performance is not representative of the entire economy as there are more than 30 millions small & mid-sized company not listed on major U.S stock exchanges

GDP - What is even more incredible about the stock market's recovery is that it all happened after various sources estimated the GDP contraction to be around 30% to 50% in second quarter

Recently, Fed and policymakers projected the economy to shrink 6.5% (medium projection) in 2020 and the unemployment rate to be 9.3% at the end of the year

Corporate earning - According to data from S&P Capital IQ, 40 percent of the S&P 500, about 200 companies, have withdrawn their guidance and declined to make EPS estimate in 2020.

This lack of guidance has caused a lot of problem for the prediction of corporate earning.

A recent analysis by CNBC earnings editor Robert Hum showed enormous differences at historical level between the high and low estimates for the largest stocks in the S&P 500.

According to numbers compiled by the data provider FactSet, second-quarter profits will fall more than 40 percent.

Refinitiv is projecting about a 43% drop in second-quarter earnings.

Expect to get a more clear picture of corporate earnings around mid-July as banks release their corporate earnings.

Even though the stock market is reflecting more of future sentiment than current economic condition, the speed of its recovery seems to indicate that most investors believe that not only will the market erase all the losses in 2020, but also it will quickly resume the long-term growth trend equals that of 2019, which seems highly unlikely to me.

Again, it is hard not to notice the massive distortion between the stock market's performance and corporate earning.

Unemployment - Initially, the hope is that most temporary layoffs would not turn into permanent job loss. However, as lockdown extends, many furloughed employees are at the risk of becoming unemployed as more and more small businesses going out of the business.

Roughly 20 million Americans are currently receiving unemployment benefits and the insured unemployment rate is still high at 13.4%.

BLS said that discrepancy in unemployment # due to "misclassification" has been adjusted accordingly. An alternative measure of unemployment that includes discouraged workers and the underemployed fell to 18% from 21.2%.

Overall, better than expected unemployment # and steadily declining initial claim and continuous claim # have painted a much better picture for the labor market.

However, unemployment remains at historic levels. Output and employment remain far below their pre-pandemic levels, according to Federal Reserve Chair Jerome Powell

Pandemic - WHO reported around 180,000 new coronavirus cases last Sunday, the single-largest increase since the pandemic began, with two thirds of new cases coming from the Americas. Around half of the 50 U.S. states were also reporting a rise in new coronavirus cases, most notable in southern states that were previously spared from the Covid-19 ravage.

On Tuesday, United States recorded the biggest single-day rise in new cases since the pandemic began.

According to Bloomberg report, most experts believe a vaccine won’t be ready until next year.

Other factors -

Trade war with China and upcoming election...

#1. Median existing-home price last month was $284,600, up 2.3% from May 2019.

#2. The 30-year fixed-rate mortgage averaged 3.13% for the week ending June 18. Mortgage rates have drop to another record low.

#3. The number of Americans applying for home mortgages has hit an 11-year high.

#4. An index measuring homes in contract to sell, or pending sales, jumped by a record 44% in May.

#5. A record spike in U.S. retail sales, though the recovery happened after a huge dive of retail sales a month earlier.

#6. PMI has surged sharply after a huge plunge since the pandemic started. It is possible that the # is skewed by the lack of small business participation and the effect of China re-opened its economy ahead of other major economy.

I believe most current home buyers are not heavily impacted during this economic downturn and their purchase decisions are probably not indicative of the economic recovery.

Shortest recession is made possible because this economic crash was driven by the uncertainty of pandemic rather than economic fundamentals? I don't know. But if you only look at real estate and stock market, it surely seems so.

GDP

S&P 500 U Shape Recovery 2020-2022The impossible "V-shaped"

The year 2020, a bad memory quickly forgotten? No, warn more and more economists, alarmed by the violence of the shock in the first half. They expect a slow recovery, provided that a second wave of the new coronavirus does not strike.

The IMF has also made it clear that, despite the expected rebound, world GDP in 2021 would come out cut by 6.5% compared to what was expected before the pandemic.

Some sectors are affected for a long time, especially in services. Perfect example: tourism and travel. No catching up possible for empty rooms, meals never served, planes nailed to the ground. Did IATA, the international air transport association, not warn that it did not expect to return to normal before ... 2023?

In industry, factories face many health restrictions. Farmers all over the world are struggling due to the lack of foreign workers.

Exit therefore, the "V" scenario that some people were still hoping for in February. Rather, it is a "U-shaped" scenario that emerges at best, with several months of recession before the economy recovers. See a "W" with alternating rebounds and relapses. Or, worse yet, an "L" with depressed activity for a very long time.

Let's Compare Some Recent Bubbles..Some that claim that markets are forward looking and see better things ahead. These markets saw nothing coming and ran right into disaster and now they’re simply jumping on the Fed liquidity train again, the very train that got them trapped in the first place. No lesson has been learned. How do we know that? Because the very same mistakes are again repeated and driven to new and even more historic extremes.

This proves that this is a market driven by a handful of large cap stocks. This means that we are in the midst of a very much distorted and disoriented marketplace. This is the best market a trillion in central bank intervention can buy. A distorted overvalued market completely disconnected from the fundamental picture.

21:53:03 ( UTC )

Fri Jun 12, 2020

Watching for possible blow-off top, then shorting into JulyAs my followers know, I've been mostly sitting in cash and silver waiting for sanity to return to this market. Y'all bought stocks, and all I bought was popcorn, and it turns out the joke's on me.

Here's how big the gap between price and fundamentals has gotten. On June 1, GDPNow reduced its Q2 GDP forecast to -52.8%. This is down over 10% in the last week. As stocks approach all-time highs, the US Congressional Budget Office forecasted a couple days ago that GDP over the next ten years will be about $7.9 trillion lower than previously forecast, and it may take 10 years for employment to return to pre-pandemic levels.

In corporate earnings, FactSet notes that the consensus estimate for 2020 SPX earnings per share has declined by 28.0% while $SPX price has decreased by only 6.2% since December 31. We are finally seeing a slowdown in downward estimate revisions, but it remains to be seen whether estimates have actually reached a bottom.

The forward 12-month P/E ratio for $SPX of 21.5 is at its highest level since January 2002, even as the risks are rising. We've added over $4 trillion in global corporate debt this year, even as credit rating agencies downgrade existing debt at an unprecedented pace. S&P Global has downgraded 247 issues in the last month and now has 1,287 on its potential downgrade list, surpassing the previous record of 1,028 from April 2009.

So what's driving the indexes upward? Three things: unprecedented speculation from zero-commission retail traders, Fed liquidity, and the hope of more stimulus from Congress. I definitely expect the disconnect between price and fundamentals to go away eventually, but the question is when it will happen and what the catalyst will be.

The combination of nationwide riots and technical resistance might cause at least a short-term pullback. We're now approaching some important resistance levels in both SPY and Nasdaq. SPY is approaching its top from March, and QQQ is approaching all-time highs. Generally I would expect a technical pullback from these levels and possibly the beginning of a big correction, and it seems like a lot of other traders are thinking along the same lines. We're currently seeing the largest futures net short position in SPY since 9/2015.

However, I've decided not to play this particular resistance level, because IMO the massive short interest creates the possibility of shorts getting crushed in a short squeeze. We've also entered a clearance area on the volume profile, which means there's not much resistance until we hit about 322. The 9/2015 high in short interest led to an 8% gain the following month. Only in the four months after that did SPY finally sell off 14%. It also seems possible that we'll get another Congressional stimulus package in the next month, including either another round of stimulus checks, or an infrastructure bill, or both.

Personally I am looking for the correction to start in late June or early July. In the last decade or two, June has been the last month of the bull market season, followed by seasonal weakness in July-September. June tends to be an especially strong month for tech stocks, and we're likely to see that pattern repeat this year. Waiting till July gives stimulus optimism and economic reopening optimism the opportunity to play themselves out, perhaps climaxing in a blow-off top as shorts get squeezed up to 322 ahead of the correction. Any parabolic move in SPY would be the signal to start shorting this market as we head into seasonal weakness in the summer.

GDP. Unemployment. China. PMI. All good for TVIX?There is undeniable toxicity in the economy. Fear sent the TVIX to an over 800% bullrun followed by market calming. So, is it over? Can we expect another run from TVIX? The answer: Yes!

One only has to look at the economics to see what is coming and already here. Today, we are looking at some of the worst numbers in economic history. I've always said that the stock market is a lagging indicator and investors will see the truth.

I've said it before.. we are coming up on the 2nd leg down of this market. We're at the Return to Normal phase of the asset bubble chart. Look at the hard economic data:

GDP - Lowest on record.

Unemployment - Highest on record.

Debt - Surpassing records monthly.

Deficit - Growing, even though there is a slowdown.

Chicago PMI collapsed to 32.2 vs estimated 40!

UMich Consumer Sentiment fell to 7-Year low.

Bankruptcies numbers are growing

4.75 million homeowners are in forbearance.

This is just a portion of whats going on. The amount of foreclosures and bankruptcies from average people and small businesses is growing at a faster rate than 2008. Just look at the hard data and stop buying into the false CNBC euphoric message of "the economy is recovering fast" nonsense because these were the same people who said "there is no housing crisis in late 2007".

TVIX Price Target(s):

1st - $200

2nd - $400

3rd - $700

4th - $1,100

Week ahead: GDP and InflationWeek ahead: GDP and Inflation

It is a busy week ahead for the markets as the Coronavirus is still front and center. Oil is up 75% in the past month while tensions between the United States and China escelates. Traders and investors should take caution when entering into the markets this week..

As of today, the Coronavirus death toll stands at 343,116 as the United States edges towards the grim milestone of 100,000 deaths.

All dates are in NZDT.

Mexico’s GDP Growth rate – Tuesday, May 26th

Mexico has recorded 7,179 deaths implying a near 11% fatality rate. With over 50 million residents being in relative poverty in a population of 130 million, their Coronavirus “curve” is unlikely to flatten in the short term. Furthermore, the IMF predicts negative GDP growth of -7.1%, down from -.5%.

This is on the back of President Andres Obrador, stating that they will implement a “Happiness Index” alongside their GDP releases.

Currencies to look out for: USD/MXN

US CB Consumer Confidence, GDP Growth Rate and Core PCE Price index – May 27th, 29th and 30th

As the United States edges towards 100,00 deaths due to the Coronavirus, President Donald Trump insists on getting the economy going again. Analysts regard this as gambling on the lives of American Citizens. However, with stimulus checks and working from home be prevalent in the past couple of weeks, the US consumer is predicted to splurge once physical retail opens. A drop from 118.8 to 86.9 last month, analysts predict a slight jump to 88 this month. Alongside this, results on the GDP quarter over quarter is expected to drop 6.9% from 2.1% to -4.8%, with the core PCE Price Index expected to drop to 1.1% from 1.7%. The Core Personal Consumption Price Index is the Feds preferred inflation measure.

Currencies to look out for USD/NZD, USD/AUD

Friday, 29th May – Euro Core Inflation Rate

With the Majority of Europe slowly flattening the curve, plans of a $545 Billion recovery fund backed by debt from the majority of the richer countries in the European Union has come into fruition. Therefore, Europe will be able to “raise money and transfer directly to the countries, regions, and industries most in need, without further impairing their economic situation by increasing their debt,” Euroasia’s Mujtaba Rahman stated to the New York Times. Even alongside the ECB ramping up their Asset purchasing program, demand for goods and services due to the Coronavirus is expected to have a net decline. Inflation is expected to drop this week ahead to 0.8%, from 0.9%

Currencies to look out for: EUR/USD, EUR/GBP

Sunday, 31st May – China’s NBS Manufacturing PMI

With their recent move to take control of Hong Kong to defend itself from attacks regarding the origins of the Coronavirus, China has been center stage in the Coronavirus and Scrutiny. With Li Keqiang announcing that they will abandon setting their annual target for GDP, their focus shifts to employment with a $500B stimulus package ensuring employees can keep their jobs. This is on top of the myriad government stimulus provided, ensuring liquidity within the financial markets and providing loans to small to medium businesses. A large chunk of the stimulus is predicted to go to infrastructure projects, like that in 2008. With a drop to 20.8 from 52 in April, a boost in government stimulus may see the PMI increase.

Currencies to look out for: AUD/USD

With tensions between different political parties rise alongside election season being in full swing amongst many countries, investors and traders this week ahead should prepare for an increase in volatility as statements for influential figures may cause key currencies and indices to swing violently.

USDCAD => Weekly Forecast CAD With OIL Inventories What Expectedwe appreciate your coming for taking the time to read our idea please do not forget to hit the like it's our only reward🙌

If one of our idea can help one other person , then to me, that is success. Strive to be authentic, not perfect. Share your Ideas in Comments – that’s what enables Traders to connect. And know that there is always someone listening –

=>

if You Need Trading guide, any Notes, any information about trading Feel free to message us through Trading view.

Check today analysis

Fundamentals

CAD GDP DATA expected Low Short USDCAD

If Oil Inventories Recover Long USDCAD Expected]

Crude Oil Inventories Data Release =>11:00 am Thursday, Eastern Time (ET)

CAD GDP DATA => 8:30 am Friday, Eastern Time (ET)

Stay safe everyone

_____________________________________________________________________________

Before trading our ideas make your own analysis and research properly.

Forex Trading are leveraged product & can result in the loss of your entire capital.

Please ensure you fully understand the Risks involved.

>>

I’d like to close with a big thank you. Thank you for reading and for helping us to grow. But most of all thank you for being a part of our journey…

With love,

Trading Fleet Team

Japan is advancing regardless pandemic environment T1 was crossed back in US session on Friday, but analysis and forecast is still same. Short can be more powerful.

I think technical analysis is simple and complete, no more focus on fundamentals. Q/Q GDP of Japan of quite positive today regardless pandemic issues.

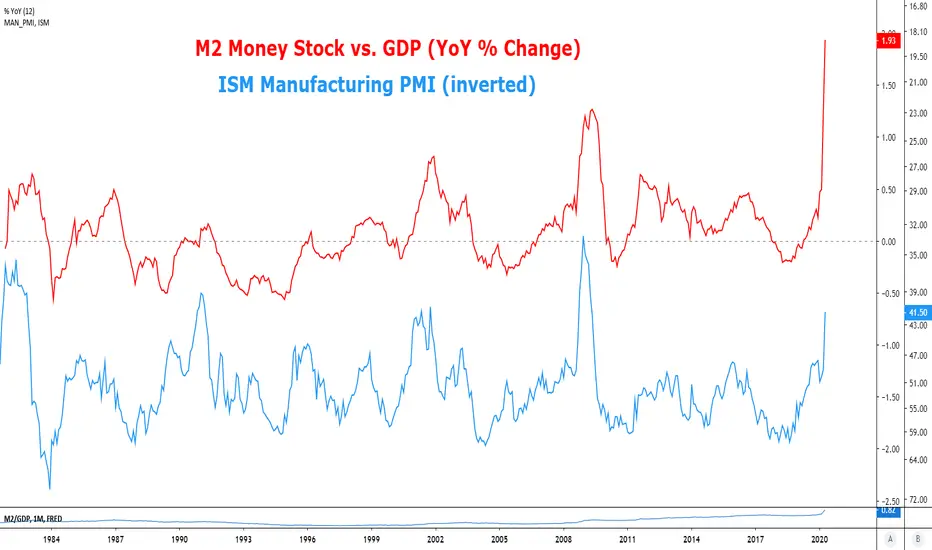

M2/GDP RatioThis ratio is indicating more pain to come from macro indicators such as the ISM Manufacturing PMI..

Covid-19: EU and NA countries have the hugest death ratesLooking at how many people got infected and how many died, seems like countries that used cheap drugs to treat this cold have slowed the spread most and also have much less deaths.

Countries with really lots of deaths have went full lockdown and GDP took a huge hit, like -15% projections.

15% of GDP... could buy a WHOLE lot of drugs with this...

Right now, governments of the countries with the most authoritarian measures and the most deaths, due to slow and incompetent bureaucrats, have their approval ratings gone sky high. The bureaucrats are pretty happy about it due to their ignorance. A whole lot of average people are strongly defending their "heroes", approval ratings have gone up 5-40% (of total, not of how much they had before)

This is of course due to the population limitless ignorance, combined to hilarously low intelligence. Fear makes them more stupid also, create more herd mentality.

"Standard deviation becomes lower the larger a group gets" I just made up this quote btw. I'm certain it is true: The larger a group gets, the dumber it gets and opinions vary less! Plenty of reasons for that.

In gambling timing is everything: Filth tier MBS were absolute crap in 2005 yet the price kept going up.

The mistake made is as soon as they realized the things were absolute trash tier and overpriced they rushed in they FOMO'd like Bitcoin dogs, Michael Burry went all in and held the bag for years with his clients losing their minds. Don't get me wrong these guys are smart, maybe even genius tier (depends on the definition if above 130 then the odds are high if above 160 the prob not lol), and they are money smart, still FOMO'd like noobs the second they saw the mispricing.

So here, first GDPs are getting decimated, at that point I'm even going to go long the SEK probably even thought I kept saying it would go to zero :p. It will go to zero but europe and the usa will go to zero faster!

And then this approval spike... Won't last long. So depends when elections are. If (probably) and when the information reaches the brain, is when people will get pissed and everything. Plus they are going to understand very fast the great depression when it breaks their jaws. Pain is an understanding accelerator.

Predicting in advance, understanding what others don't is essential, but then it is necessary to know that the market and the world isn't a reflection of the truth, it moves when info reaches people brain. Something obvious for years will have no effect and then the second, literally second, the information reaches the herd brain they will rush (for the exits?) at lightspeed (why in such a hurry? The info was available and obvious for years).

People are going to be pissed at certain pharma companies possibly? People will be pissed at governments? Dumb people don't think alot but they get angry alot. Expecting rioting. Well no point speculating too much there is plenty of time. Took me a few minutes to figure it all out, so should take the herd a couple of years.

Some countries numbers:

I tried comparing countries with similar climate and similar populations or confirmed cases if possible.

Israel got 2.4 million doses of experimental coronavirus drug (chloroquine) and more:

www.jpost.com

Japan has been using an antiviral:

www.theguardian.com

Russia since march has been producing and using an anti-malaria drug (Mefloquine)

www.aa.com.tr

Europe and North America have been fighting treatments and promoting expensive patented drugs that don't work.

They have thought drugs that work for what? Protecting idiots that self medicate?

And what a surprise, they have the biggest death rates. Poor countries are doing much better than rich ones except sea ones.

Weird since french army stockpiled chloroquine "in case it does work".

Making sure they have something to offer to an invading country to help negotiate surrender.

Business owners have imported chloroquine to give to their workers and got in trouble (stupid people that self medicated have died).

There all sorts of treatments, here is something "A single treatment able to effect ~5000-fold reduction in virus at 48 h in cell culture."

www.sciencedirect.com

In france our main ID expert in the spotlight said

"We have with my team made some of the greatest virology discoveries of the XXI century"

"Scientists are not equal just like Lebron James isn't equal to amateur players" (something like that)

"I am one of the greatest experts in the world but I avoid herd meetings" (avoiding the herd like Tesla)

"Avoid at all costs consensus and political correctness"

And my favorites

"People criticizing me are children!"

"I don't care about their critics/opinions. I refuse to debate with people that have a too low level of knowledge"

A little too polite. I prefer the Dan Pena style.

And from now on I refuse to argue with the typical Bitcoin & Tesla bulls.

Warren Buffet in March said he wouldn't sell any more airline company but he dumped everything (on retail bottom chasers btw).

The perma bull white knight of the USA stock market ran for the exit, and he has the biggest cash position ever seen.

But sure don't worry, every thing will be alright.

I hope the USA will go for Stalin rather than Hitler, kill his own people rather than start a huge war and kill others. The USA are "terrified" of "the far right", and there's lots of marxists there. Excellent. BurgerLand will become a godforsaken hellhole, they'll kill each other, and the stock market will go to zero, while I'll be chilling. Don't want far right guys like Trump that threaten foreign nations and do trade wars (Trump+ does more than trade wars). Gogo democrat socialism.

Burgerland is in dire need of socialism and more antifa. Please god, please let them kill each other and ignore us and not nuke anyone.

"Buuut you are wishing ill on the usa" ... actually no I'm not going to lower myself to explain.

Ahem * clears throat *

DOWN DOWN DOWN DOWN! EVERYTHING WILL CRASH! DOWNTREND FOR YEARS! ONLY DOWN! ECONOMIES WILL NEVER RECOVER!

EVERYONE WILL LOSE MONEY EXCEPT BEARS! MASSIVE UNEMPLOYEMENT AND POVERTY! HUGE EXTREMISM! US STOCKS ARE DOOMED THEY WILL NEVER GO UP AGAIN!

DXY is exhausted momentallyThis week we might see slight pullback from the purple support zone I marked on the chart(around 99.00 and 98.80)

Those zones are buy signals and it can go to the next monthly resistance around 99.78 before thursday

In the next days we having consumer prices (news) which are mostly positive( we people always consume and also during corona times)

But i would look out on thursday because we have the jobless claims. so take your profit and go in dependant on the news.

On friday we have the GDP news from Europe which is also interesting to watch what will happen(in my opinion negative news so selling EURUSD)

From now on it only can be better, bcause countries are opening back from the lockdown in europe.

Take your risk reward and have a nice week

QQQ Getting a *Little* ExpensiveIf we completely ignore the news, the graph of QQQ seems to be recovering quite nicely. For a technical trader it's extremely optimistic. Then, if you look at any sort of news, this trading at Jan 2020 levels seems absolutely insane. Both sides have good cases, but I am going to choose to ignore each of them. The indexes are beyond unpredictable right now (see GDP -4.8%, IXIC +3%) that my options trading is pivoting towards almost exclusively to singular companies - as opposed to my typical index/ETF trades. I hate to sit on the fence here, but anyone who says they know where this is going is ignoring half the data on either side. Good luck to all!

Ominous Rising Wedge Suggests X=X 1,000 Point CollapseAccording to technical analysis theory the rising wedge points in the opposite direction to the breakout.

In this hourly chart of the coronacrash we can clearly see the rising wedge pattern formation.

This pattern also predicts that the length of the move into the wedge “X” is the same distance as the length of the break-out “X”.

Therefore X = X.

The downtrend into the wedge was a drop of 1,000 points, ergo the breakout will be a 1,000 point drop.

Caveat.

I have back-tested stock chart patterns and they are not 100% true, but in general, they are better than 60%.

That’s not saying much.

Mostly the direction will be set by the news, especially today with 2 big news items.

1. GDP Advance Announcement – Productivity in the Economy

2. GDP Spending – very important for the economy and sentiment, spending drives the economy

I expect both of these to be bad numbers, but will it be the start of the resumption of the much-needed downturn in the market?

Not necessarily.

The “Trump Pump” will be in full effect I am sure with a new announcement of stimulus designed to boost spending and therefore save the stock market.

It will be interesting to see if the technical analysis Rising Wedge is predictive in this case, or will ultimately fail because of government intervention.

I believe the monetary policy is now to encourage healthy inflation above 2% and keep interest rates at close to zero for the next decade, to ensure the debt burden is reduced over time. As Ray Dalio calls it a “Beautiful Deleveraging”.

An interesting day ahead, and be sure, the only thing that can save Trump’s re-election campaign is to ensure the stock market does not collapse, and he will do everything to save it.

Stay safe and like and follow if you want more.

Barry

$SPY : Rejected at resistance at first test$SPY opened higher than resistant but reversed and closed lower. No damage done to the intermediate term trend which remains positive and above 20 EMA.

$ES Futures are pointing to a green open about 0.8% higher. GDP number and FED minutes today can influence and whipsaw the markets today.

Total Fed Balance Sheet and GDPSince 2003 the USA's GDP has grown about ~100% (roughly)

Since 2003 the USA Federal Reserve's Total Assets on Balance Sheet has grown ~800% (Roughly)

Interesting... What are your thoughts? Does this matter in the new 'debt' economy we live in?

If people own your debt as treasury bonds / securitized debt, don't they have a bias to see you succeed long enough to pay back that debt?

Much Love

xoxo

snoop

Dr. Copper ... we're in trouble The historical up-trend has been broken ... Copper is a big indicator for economy health, and it really has bad view!

GDP, FRED, RUSSEL 3000, GBTC Bitcoin Trustnothing to see here, move along, just a coming financial crisis and short term recession, not that bad...

wait for evertything to tank more begining of summer, buy with both hands before OCT2020

NIO- Long-term bargain price is within the grasp. Don't miss it!Please click like and follow me if enjoy my posts! :)

Due to the whole market meltdown, NIO has retraced back to Fib 0.786 lvl early this week. However, it has since then rebounded strongly and is currently fighting the resistance lvl.

Barring the continuing worsened market condition, I believe NIO's distribution cycle is nearly over. The current bargain price is hard to pass up despite the unfavorable external environment. The prudent approach would be to determine the total amount you want to put in, then use the pyramid method to scale in slowly as the price moves down lower.

I would grab my cheap shares of NIO if the price falls inside the buy zone and set the tight stop loss if the price falls below the buy zone.

*Dow, Nasdaq100, S&P500 and S&P400 are all still below SMA 200. SPX 50SMA/200SMA crossover seems imminent.

*Futures market seems indecisive. Dow and S&P500 are up while Nasdaq is down.

*GDP final and initial claim filing figures will come out tomorrow. Both reports may have the negative impact on the stock market tomorrow.

*Manufacturing related economic indictors may have the impact on NIO so it is worth to pay attention to them as they come out.

*COVID-19 growth factor slows down for the first time since Mar.11. Yesterday's growth factor was 0.86 (Below one means the exponential growth slows down)

DYOR! Not an investment advice.

The bottom is in... ?Technically it is interesting that this recent selloff has come down to test the 2018 lows and has so far held. The level also matches with an inflection point back in 2017. Is this the bottom though?

Let's ask a different question. Is everything priced in? The stock market is a gauge of perception about the economy going forward and the accepted metric for the economy is Gross Domestic Product (GDP). Going on at least one opinion (because that's what it is) Goldman Sachs released the estimates of their economists that Q1 2020 GDP will expand 0% followed by Q2 contracting -5% because of the economic drawdown from Coronavirus. These will be followed by a rebounds in the 3rd and 4th Quarter to bring the year's GDP growth to just 1%. Estimating growth at all is a rather bullish outlook when you consider it.

Let's just go with Goldman's estimates for what this next quarter will do to the economy. The prior years' GDP growths of 2018 and 2019 were 2.86% and 2.3% respectively. So with a sudden 5% contraction we can roughly say that the US economy is puking up 2 years of economic growth. That would theoretically put us back at a valuation from 2 years ago where the SPCFD:SPX was trading around 2750; a 9.6% difference from as of writing. Somewhere in the range of unknowns it is possible that the losses the economy will actually sustain are now priced in at up to 10% below the theoretical fallout.

A trader has to make a bet and so long as any new shocks do not enter the market I think we've seen the end of the selloff and now it is a matter of returning to the mean.

I've had a few spirited debates with highly intelligent people that seem convinced that "this is it" and all the Fed's money printer going 'brrrrrrrr' is coming home to roost. I'm just don't think "this is it." What we have here is a unique and critically impacting Black Swan event but nothing fundamentally about the monetary system or real world assets has been put in jeopardy. A pandemic, while dangerous, is not particularly deadly among most demographic and does not impact financial system liquidity. Businesses may lay off workers due to reduced economic activity but the buildings are still standing and inventoried goods will eventually be sold. In fact this unique mass hysteria has actually caused a great deal of excess consumption as people stock up for "the apocalypse that is nigh."

So stay well, wash your hands, make sure to design at home workouts to stay fit, and trade while keeping your head!

Potential growth of USDTRY as waging war agains Syria1. Wait for breaking parallel channel or resistance line then take long

2. Wait till lower band of parallel channel and then take long

Turkey officially declare war against Syria. it could bring chaos to middle east. Russia also is defending Syria. Turkey threatened NATO to support otherwise it would open its borders and free Syrian refugee to flee to EU countries.Turkey did it and refugees had faced a very bad conflict with police of Bulgaria and Greece (EU Gate). Turkey is drowning as more than 45% of GDP made by external loan from international institution like IMF as an example. How could a country be independent while it has 433 Billion USD external load more than 45% of GDP!? President of Turkey Erdugan said we would not get any dollar from IMF as it would violate our foreign independence. After some months it appears Erdugan could not resist foreign pressure and wage war. If both sides of conflict could not reach an agreement that would be death and destruction. Erdugan could not rescue Turkey economy by doing this and corona virus could damage tourism earning so much so bye bye Lira! bye bye foreign real estate investors!

USA will use Turkey like a tissue and then throw it away.

History will repeat itself.

GBPUSD: Market Outlook, Plan and Probabilities Future Price MoveU.K.’s first GDP reading, which is expected at 0.0% after a 0.4% reading in Q3 2019.

If weak expectations then we could see GBP/USD drop below its 1.2875 weekly lows (weekly pivot s1 level) and maybe even make a run for the lower s2 or beyond. This is still possible given Cable’s daily ATR and its move so far today.

If today’s data dump allows the BOE to avoid the dove camp for a while longer, then Cable could revisit its 1.2970 broken support before submitting to other economic catalysts.

Speaking of, Fed’s Powell will talk economy in D.C. during the U.S. session. He will likely repeat the Fed’s growth optimism and concerns over low inflation but traders will also want to hear about the impact of Coronavirus and maybe his reaction to Trump’s latest calls for lower interest rates.