Gold corrective leg down?$gdx $gdxj $nugt $jnug $jdst $dust $slv $gld I'm bullish on hard assets- watching for possible leg down. A higher high will invalidate this.

GDXJ

GOLD (XAUUSD) preparing for MAJOR SELLOFF before true breakout!!Cycles analysis indicates one more major deflationary move to occur. A selloff approaching for XAUUSD down to support levels near 1380, as well as a retest lower for gold miners. To be followed by a longer term major buy setup for gold. Let's remain objective and not get too excited just yet!!

Gold Quarterly Closes Above 61.8% Fib Retracement Gold saw a strong quarter with an opening price of $1,521 in January and a closing price today of $1,637 for a +7.6% gain in the first three months of 2020. This comes after price broke above the 38.2% Fibonacci retracement level in the second quarter of 2019 which was a level that acted as resistance during the 6-year bear market after price peaked at an all-time high of $1,923 in the summer of 2011. 2019 saw price break above the critical 50% retracement level which put gold back in a bullish trend, and this past quarter saw the trend confirmed with a push above the 61.8% golden retracement level as well.

The Relative Strength Index(RSI) is indicating bullish momentum behind price with the green RSI line rising above its purple signal line, as well as both lines being above the centerline at the 50 level. An RSI reading above 50 indicates a healthy RSI reading and bullish momentum.

The Price Percent Oscillator(PPO) is indicating bullish momentum as well with the green PPO line above its purple signal line, and both lines rising above the centerline at the 0 level. Neither the PPO line or signal line crossed below the centerline during the 6-year bear market which indicated that no bear trend in momentum ever took hold, and that a bullish pullback instead was taking place.

Current short-term and long-term views on gold remain bullish, especially with the amount of money being printed by central banks across the globe as they continue to fight the economic slowdown caused by the coronavirus. The more they print, the more they’ll devalue their respective currencies, the better gold will perform. It’s still my opinion that gold remains on track to test its all-time high sometime this year with the potential to create a new all-time high.

GDX and GDXJ to the toiletAMEX:GDX AMEX:GDXJ are headed down to the toilet. Symmetrical triangle is a continuation of the previous trend, which is downward. Target is down around $5 or less.

Gold is a lot different from the gold miners.

Gold Miners Likely Topped and should get Obliterated furtherGDXJ failed to close above a key resistance level of $30.70 on Friday and it is highly likely that for the month of April, the miners (and Gold and Silver) have topped. At this point if you follow my ideas, Gold will sell for liquidity in the near-term for the second wave of the downfall of equities.

Investors should remain totally on the side-lines for the miners for much of the month of April.

Come towards the end of April and into early May we can start to look for key bottom opportunities. However, in the near-term, the miners will be decimated.

Note: When we start to get quarterly re-balancing near the end of March (i.e. next week), we can expect more sharp sell-offs not only in the commodity of Gold and Silver, but the mining stocks themselves (and equities).

- zSplit

Daily Market Review | Gold to $1,886 | Money is Moving Into GoldThanks for watching. Please support my work by sharing this video with other investors and traders.

Don't forget to smash that like button here and drop a follow.

See you guys tomorrow.

Take it easy.

~Bo

THE WEEK AHEAD: A PREMIUM RICH MARKETOPTIONS LIQUID EARNINGS ANNOUNCEMENTS:

MU (77/112)

NKE (74/103)

EXCHANGE-TRADED FUNDS ORDERED BY IMPLIED VOLATILITY RANK:

EWZ (91/132)

USO (89/210)

XLU (84/76)

GDXJ (82/141)

XLE (77/109)

EWW (76/105)

SMH (73/105)

TLT (71/47)

XOP (63/154)

SLV (73/79)

GLD (63/37)

FXI (61/63)

GDX (57/106)

BROAD MARKET ORDERED BY IMPLIED VOLATILITY RANK:

IWM (76/71)

EEM (74/73)

SPY (73/66)

QQQ (73/60)

EFA (54/53)

VIX/VIX DERIVATIVES

VIX: 66.04

/VX APRIL: 62.00

/VX MAY: 56.95

/VX JUNE: 49.95

MUSINGS:

On Margin:

As you can see by the chart showing the top five or so exchange-traded funds having the highest implied volatility ranks, this is largely a closely correlated sell-off. Because of this, I'm somewhat hesitant to pile into a bunch of nondirectional stuff simultaneously, if at all. If we get relief from the selling, these very same instruments could whip back to the call side in closely correlated fashion, leaving me with a bunch of tested call side; whereas now I'm just put side tested (and how). Naturally, this means I have to put up with being far more directional than I would ordinarily be, but these things happen and being patient and mechanical with how you manage current positions will be more productive in the long-term than going bonkers here and bailing out of everything in panic.

Unfortunately, this likely means that I will be taking on far more shares of stock than I ordinarily like to hold on margin and then reducing cost basis over time via covered call. I'm always prepared for that, but being in stock on margin isn't buying power efficient, although you always have to plan somewhat for that possibility and go with the flow if taking on shares is really the best way to work yourself out of the trade.

In The IRA:

As pure luck would have it, leaving my SPY position monied throughout this nonsense (as well as erecting some additional call diagonals at market highs as delta cutters) has served me well. This wasn't particularly prescient or a stroke of genius; I was just doing what I felt I had to do to protect the largest element of my retirement portfolio at a point at which it made the most sense to do that and nothing else. Anyone else who did that and got lucky isn't a guru. No one saw this crap coming, and if they're saying they're a genius, well, I say you're free to call bullshit.

Is this an opportunity to pick up things on your shopping list? Maybe. I've taken this opportunity to ladder some out-of-the-money short puts out in a few things that I've had on that list for ages -- XLU, IYR, EFA, and HYG; all dividend generators which have been just far too pricey to deploy the frustratingly large bit of dry powder I've had sitting on the sidelines for ages as the market inexplicably ground up to more and more ridiculous valuations. Will I get in at the best possible prices? The jury's out. I will be getting in far lower than at the market highs we saw just a few weeks ago (assuming price stays below the rungs of my ladders) and won't let anyone talk me out of the proposition that lower is always better in your retirement account even if I don't hit the lows perfectly.

The basic strategy here, after all, isn't largely about share price; it's about assembling a portfolio that will pay out dividends regardless of growth and in which you can reduce cost basis over time via short call. It's three-legged: dividends, short call premium, and (if it happens) growth. If the grand arc of time has taught us anything, it's that growth may be an "average given" over the entire life of the market, but may not be over shorter time frames.

GDX just got my attentionI believe the miners are undervalued and stand to do well moving forward. Gold and silver have shown their stability through history and remain solid in my opinion. I see a lot of potential in the miners.

(renko blocks are not playable so I'l have to post updates below)

Looks legit, anyone still in $DUST ? - $GLD $NUGT $GDX $GDXJ Gold miners are clearly worthless now that gold is down 10% from the high.

Does anyone know who planned this event?

Gold About to Test Key Level#Gold is now retesting the rising trend line from the Aug '18 low. A break here would target the major horizontal breakout area ~$1530-$1540. That will be the last gasp to preserve a bullish regime. Below that level could send gold down towards a 1370 retest. #GLD #GDX $GDXJ

Money for nothin' and your chicks for freeLooks as though the Gold to Silver Ratio has peaked just over 100 and the popular pairs trade of Long Gold and Short Silver has run its course..

Back Up We Go... See Chart for Details and Target Price. Should Bernie Sanders upset Biden tonight, it would justify a more explosive move to the upside.

AMEX:JNUG AMEX:GDXJ AMEX:NUGT AMEX:GDX TVC:SILVER CURRENCYCOM:SILVER FX_IDC:XAGUSD AMEX:SLV NASDAQ:PAAS NYSE:AG

THE WEEK AHEAD: ADBE, ORCL EARNINGS; GDX/GDXJ, USO/XOP/XLE, EWZEARNINGS:

ADBE (89/65) and ORCL (77/60) both announce earnings on Thursday after market close and have the metrics I look for in earnings-related volatility contraction plays (>70% rank; >50% 30-day implied).

Pictured here: a short strangle paying 11.65 at the mid price camped out around the 16 delta. Its defined risk counterpart: the 265/275/395/405 ten-wide iron condor pays 2.46. Off hours markets are showing wide, so look to price setups out during the regular session.

The delta neutral ORCL April 17th 40/55 short strangle pays 1.45.

EXCHANGE-TRADED FUNDS WITH EXPIRY IN WHICH THE AT-THE-MONEY SHORT STRADDLE PAYS >10% OF THE STOCK PRICE:

GDX (99/51), April

USO (97/66), April

GDXJ (96/58), April

XLE (97/75), April

EWZ (92/52), April

XOP (92/51), April

TLT (91/41), May

EWW (91/48), April

XLU (90/43), June

SMH (84/56), April

FXI (65/33), June

BROAD MARKET WITH EXPIRY IN WHICH THE AT-THE-MONEY SHORT STRADDLE PAYS >10% OF THE STOCK PRICE:

EFA (87/37), June

QQQ (83/43), April

IWM (82/46), May

SPY (78/41), May

EEM (70/37), June

FUTURES:

/CL (97/65)

/GC (84/25)

/SI (70/30)

/NG (65/48)

/ZS (30/19)

/ZC (21/22)

/ZW (13/27)

VIX/VIX DERIVATIVES:

VIX finished the week at 41.94, so it has been a rough ride for shorters who were in plays before this volatility expansion (points to self). The basic watch word is "patience"; volatility will abate at some point in time ... .

I like the miners and the things they mineminers have re-entered my "I'm interested" zone. I think 2020-2021 has very good things ahead for the miners and the things they mine exciting $nugt $dust $gdx $gdxj $jnug $jdst sorry for the ugly chart

THE WEEK AHEAD: SQ EARNINGS; SMH, XOP, GDX, GDXJEARNINGS:

SQ (77/59) announces Wednesday after market close and has the volatility metrics I'm looking for out an earnings-related volatility contraction play -- implied in the 70th percentile or greater over the past 52-weeks and 30-day at or greater than 50%.

Pictured here is an SQ April 17th 72.5/100 short strangle camped out around the 20 delta paying 3.55 on a buying power effect of 8.37 (42.4%) and delta/theta metrics of .66/7.78. For those high on defined, consider the 65/70/95/100, paying 1.58 (46.2% credit received as a function of buying power effect).

EXCHANGE-TRADED FUNDS ORDERED BY RANK/30-DAY IMPLIED AND SHOWING THE EXPIRY IN WHICH THE AT-THE-MONEY SHORT STRADDLE IS PAYING >10% OF STOCK PRICE:

SMH (73/30), May

XLE (63/23), July

USO (51/37), April

XBI (48/30), June

XOP (45/37), May

FXI (40/23), August

GDX (40/29), May

GDXJ (38/33), May

EWZ (26/27), June

I didn't get an opportunity to do a ton last week beyond take off a few setups in profit, so this is probably an opportunity to build up theta pile in stuff that I don't have plays in currently and to add to stuff via delta under hedge that has experienced an up tick in volatility over the past several days.

BROAD-MARKET ORDERED BY RANK/30-DAY IMPLIED AND SHOWING THE EXPIRY IN WHICH THE AT-THE-MONEY SHORT STRADDLE IS PAYING >10% OF STOCK PRICE:

QQQ (59/23), September

SPY (43/17), November

IWM (42/19), September

EEM (37/19), September

In spite of the expansion of volatility over the last several days, broad market isn't paying fabulously in shorter duration, so if you're going to play, look to start out small, add small over time, and take profit somewhat aggressively.

FUTURES:

/GC (70/15)

/CL (51/36)

/NG (47/39)

/ZS (43/19)

/ES (42/17)

/SI (33/89)

/ZW (24/24)

/ZC (23/13)

VIX/VIX DERIVATIVES:

VIX finished the week at 17.08 with the March, April, and May /VX futures contracts trading at 17.05, 17.33, and 17.09 respectively. It's tough to divine what /VX futures traders' thought processes are here, but it looks like they may be focused on the exogenous event of the year -- the expiry around the general elections, where there is a huge term structure "hump" from September (currently trading at 17.75) to October (20.55), with the remainder of the preceding structure being fairly flat in the interim. There is a mere .70 differential between the March contract price and the September one which I regard as unusually flat, which doesn't make for good term structure trades. Naturally, at some point, the term structure may adjust to a more "standard look," but in the mean time, look to add short to VIX derivatives (VXX, UVXY) on pops to VIX > 20% via short call vertical or long put vertical with a break even at or above where the underlying is currently trading and shooting for one-third the width in credit (if a credit spread; don't pay more than 2/3rds the width if a debit spread).

Gold Miners in a dual pattern breakout - Rally Alert!Just building up, the GDX Gold Miners, which were lagging Gold prices for a while, is now on the verge of a breakout... from a tilted Cup & Handle Pattern, as well as a Triangle.

MACD and OBV are bullishly supportive, and momentum is strong.

A breakout sets an upside target of 32.50.

Enjoy the ride!

GDXJ Gold Juniors Poised for run to $52?$GDXJ Gold Junior Miners finally breaking out of resistance above $43. Next stop $52. $GDX $GLD #gold

#gold consolidates in $1630s miners lag min 10% $GDX $NUGT $DUSTIt is uncharacteristic for the miners to lag in this way, usually, it goes the other way around.

The explanation is simply that the S&P is near all-time highs and has signaled repeatedly to short the gold mining companies and ETFs.

GDX resistance in the $31 region is not likely to hold this time. Gold miners are seeing all-time record profits due to gold reaching new all-time highs in every currency but the US dollar ( XAUUSD ) and Swiss Franc ( XAUCHF .) Most mining costs are incurred in other currencies where gold has been hitting all-time highs repeatedly for many months.

Shorting of the miners are will be bad for business as these levels are pierced.

Gold Rally UnderwayIf you look at the previous gold rally from 2001 to 2011 you'll see a similar pattern of the 50DMA crossing below the 100DMA and then a few days/weeks later rising above it again and rallying to new highs. I believe this is what we're seeing right now. Gold is going to touch $1700 in the next rally, or get VERY close before correcting. Let's see how it plays out...

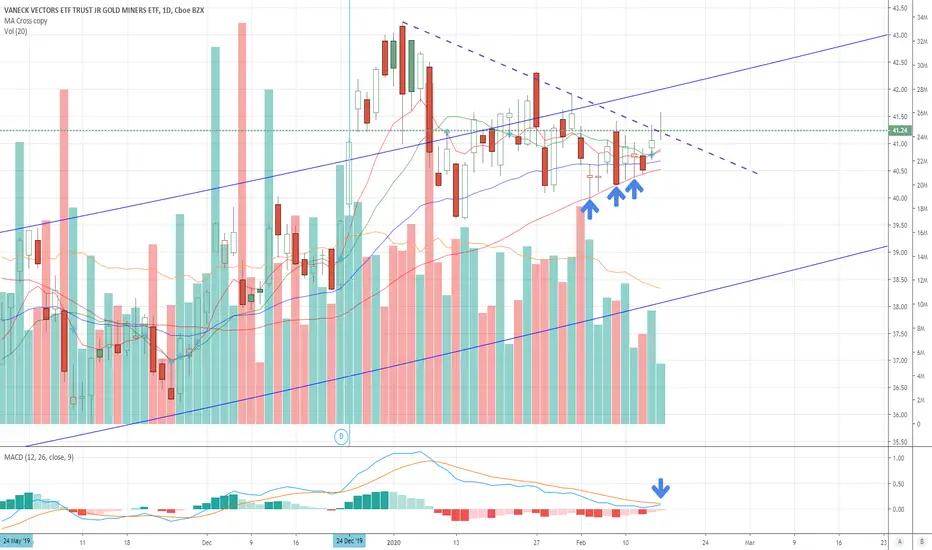

GDXJ long ideaTo me I am finally getting a buy signal on miners. GDXJ has been supported by the 50 sma and is getting a move higher. The upper trend line was crossed, BUT we didn't close above it yet. I do see a cross of the 8sma and 13ema which is a buy signal. I had a buy signal on AXU yesterday. Pretty close to lift off.

THE WEEK AHEAD: DBX, TECK EARNINGS; USO, GDXJ; VIX, VXX, UVXYEARNINGS:

The earnings that are best metrically for earnings-related volatility contraction plays are DISH (87/59), TECK (87/52), and DBX (82/57). Unfortunately, strike availability in DISH is limited to two-and-a-half wides, making it an unattractive play given its stock price (39.97 as of Friday close).

Pictured here is a DBX (82/57) skinny short strangle in the March cycle paying 1.98 on a buying power effect of about 3.25 (60.9%), break evens wide of the expected move, and delta/theta of 3.32/-7.44. Given its near-straddle narrowness, I would look to take profit at 25% max. Announcing on Thursday after market close, look to put on something in the waning hours of Thursday's session.

The other one of interest is also small: TECK (87/52), which finished the week at 13.46. A play similar to that in DBX -- a March 20th 13/14 skinny short strangle -- pays 1.15 at the mid price on a buying power effect of about 2.25 (51.1%) with break evens greater than the expected move and delta/theta metrics of -4.21/2.17. As with the DBX skinny, look to take profit at 25% max.

EXCHANGE-TRADED FUNDS WITH EXPIRY IN WHICH AT-THE-MONEY SHORT STRADDLE IS PAYING GREATER THAN 10% OF STOCK PRICE:

XLE (46/20), July

USO (42/35), April

FXI (35/21), August

XOP (34/34), June

XBI (34/27), June

SMH (30/25), June

EWZ (14/25), June

GDXJ (5/28), May

GDX (4/23), June

The paying plays of shortest duration are in USO (April) and GDXJ (May). Take your pick in June between XOP, XBI, SMH, and EWZ.

BROAD MARKET FUNDS WITH EXPIRY IN WHICH THE AT-THE-MONEY SHORT STRADDLE IS PAYING GREATER THAN 10% OF STOCK PRICE:

EEM (38/12), December

QQQ (26/18), September

EEM (23/18), September

IWM (19/16), October

SPY (16/13), November

FUTURES (EXCLUDING CURRENCY/TREASURIES):

/NG (52/39)

/CL (41/35)

/GC (26/11)

/ZS (23/17)

/ZW (20/21)

/ZC (16/14)

/ES (16/14)

/SI (5/24)

VIX/VIX DERIVATIVES:

VIX finished the week at 13.68, so there are probably some happy campers out there who shorted the January-end volatility pop to nearly 20. The March, April, and May /VX contracts are trading at 15.40, 16.11, and 16.30, respectively. I could see going small with an April term structure trade if you haven't already got one on, but May isn't going for a ginormous premium over April, so there probably isn't much benefit to going out farther in time: the April 16/18 is paying .60 at the mid with a break even of 16.60 versus the /VX contract of 16.11; the May 16/20, virtually the same price.

With the VXX short call verticals I already have on, I'm basically looking for a VIX low (it was around 12) to consider pulling some units off in profit. On the other end of the stick, I'm waiting for another pop in VIX to potentially add. VIX at 20 is a nice place to look to do that ... .