Growthstocks

Shell company positioning wellLooking at UUV tonight after some large volumes over the past week.

In terms of context, the company wrapped up all previous business in the US last November 2020. Winton Willesee was appointed Chairman in October 2020 to push this through. For those unfamiliar, he has a history of leading RTOs (xTV to NZS) and growing small-cap companies such as CPH and NC6.

Seemingly off the back of this hype, UUV has been pushing through some impressive volumes of late.

The 50 day EMA has crossed the 100 day EMA and is heading toward the 200 day EMA. We could even have a golden cross if the splurge contains and the 100 day EMA follows the 50.

Volume profile (since November 2020) suggests that support exists at $0.003 and with the buying frenzy this is unlikely to drop below $0.002/$0.003.

Finally, the MACD shows a positive trend, which after a slight dip was reconfirmed after today's trading.

In terms of the future, it is extremely uncertain and will hinge on how UUV reposition. There have been links to AR9 and the cyber security sector, and any further tidbits of information coupled with the low share/options price will likely spur short-term growth.

Looking for a nice bounce of the EMA to long Amazon.1.6 Trillion dollar company here.

Amazon is a near and dear company to my heart. Not only do I use their services regularly I find they deliver an exceptional client experience and have been doing that consistently for a long time. I wish nothing but good things for Bezos and his new venture and hope he finds great success being more hands on with blue origins.

This company is a growth machine. They have brilliantly mastered the flywheel effect, you can read more about that from Jim Collins latest book, and I think they have a lot more room for growth despite the gigantic size they already are.

Fundamentals for the company are stunning:

P/E 78.71 (For Amazon this is shockingly not too bad)

Employees 1,298,000 - WOW

P/FCF 63.21 (Yes very high)

Debt/Eq 0.55 (Very low)

Long Term Debt/Eq 0.53 (again very low, and its good to see them take advantage of low rates)

-Obviously in reading that, no one is buying Amazon as a value play. The opportunity here is in growth, and It think it is time to plan our entry as an aggressive growth play due to the following:

EPS this Y +81%

EPS past 5Y 101.8%!

Sales Past 5Y +29.3%

Sales Growth Q/Q +43%

EPS Q/Q +117.5%

ROE 27.1%

Equity Ownership

Insiders Own 10.6%

Insider Transactions over past 3 Months -1.9%

Institutions Own 58.7%

Institution Transactions -0.03%

2/10/21 ZenMode Price Target $4,000

2/3/21 UBS Price Target $4,150

2/3/21 Susquehanna Price Target $5,200

2/3/21 Stifel Price Target $4,000

2/3/21 J P Morgan Price Target $4,400

2/3/21 Goldman Price Target $4,500

2/3/21 Deutsche Bank Price Target $4,250

2/3/21 Barclays Price Target $3,860

If you found this content helpful gentleman please be sure to give it a like and a share. If you think I missed something important in the analysis please be sure to share it with me and the community to aid us in learning more!

$TRIP $TRUFF A nice Cup and Handle forming as we make it towards the end of the week. Perfect timing with the upcoming news release.

Red Light Holland has already made it known that they want to be the forefront in Psychedelics. To date, i've noticed a strong campaign regarding branding and increasing company exposure/ psychedelic acceptance. I do like that Bruce Linton is also the Chairman of Advisory Board

To note: Red Light Holland making an APP to share personal stories of Microdosing?.. Along with a Job-Contest coming up for Feb 8th?..

I do not see this staying at these levels much longer. GLTA

- Pocketfeeder

HelloFresh: profitable growth stock with a reasonable valuationHelloFresh is a multinational German company that delivers home, packaged in a box, the fresh ingredients of its recipes selected online

by the customer to cook them in their kitchen in half an hour.

HelloFresh operates in Germany, USA, Australia, Austria, Belgium, Canada, the Netherlands, Switzerland, and the United Kingdom.

Its anyway strong growth accelerated in 2020 due to CORONAVIRUS. Regarding its profitability, we do not just hope that the company

will likely become profitable sometime, it is already profitable, and its valuation is very reasonable given its growth.

Below are presented the mid- and short-term trend charts of HelloFresh.

Disclaimer

The writer of this text is not an investment advisor. The preceding content is intended to be used for informational and educational purposes only. It is not an advice or inducement for the purchase or sale of the products mentioned. Before making any investment based on your own personal circumstances, it is very important to do your own research and analysis and also take independent financial advice from a professional to verify any information provided here.

LONG MSFT BREAKOUT, STRONG SUPPORT, SWING TRADE, TOP TECH PICK

The fundamental are really strong for this MSFT. With the recent announcement of partnering with GM and investing $2B on the cruise from GM. EV market is now getting attention from big tech companies likes apple who have plan to get into. Microsoft investing in cruise which is ahead of tesla in certain tech feature and automation. Based on its current prices it just broke resistance levels and if it continues which seems highly probable going into earrings it will gap up to $230+ easily.

Forecast:

Using the Bloomberg terminal the average one year target price for MSFT is $242. This will yield a 8%+ return from its current price. Its high target price is at $278 and it's low target price is at $200. Considering the stock price is already at $224 the down side is only -$24 or (-10.71%). It leaves an upside of +$54 or (24.11%). Clearly there is more upside in this investment then downside.

In terms of the Industry Analysis; the technology sector is outperforming every other industry. MSFT is classified under software sub industry which is one of the best performing sub industries. The company has essential products especially like TEAM which is fairly need but is already competing with other companies like Slack. It's Azure cloud program is doing great in terms of growth. It's revenue growth rate is 48% over the last quarter. Microsoft’s current and future revenue. Office Commercial and consumer products are both growing – unsurprising in the work-from-home era. Additionally, Microsoft Teams has reached 115 million daily active users, up from 75 million in April.

Overall, the current price makes this company undervalued. It broke a resistance level and will continue to gap due to sub industry analysis, price target, technical analysis, fundamental analysis. This company will continue to growth due to covid stay at home work. Its products and remote service on top of having Azure positions its in great spot to increase in value.

Growht vs. Value in small capsThe Russell 1000 growth/value ratio has formed a head and shoulders pattern, indicating growth stocks may be in trouble and value may be on its way back

STMP over 225.73One of my favorite patterns, rounding bottoms tapping up against a descending trendline. Should yield a big move. Good for a swing, better with commons as options can be spready.

Stocks To Watch This WeekThe Bull Market is strong, the end of 2020 saw many growth names pull in or consolidate which gives a better reward to risk entry. Some of these charts still need to confirm their price action. This video is my watchlist. Most of these names are at or near all time highs or multi year highs. There are 30 total stocks on this list. I add an additional 3 stocks that are on my potential short squeeze watch list. Many of these have IPO'd in the last few years and still have a growth story ahead of them. Know your time frame and risk tolerance, grab a pencil and paper and jot down the names that look interesting to you and then make the trade your own. Good Luck!

BYND over 147.25A few things to note here. First, the .5 fib is from a set from all time low to high, so its a big level for price to base over. Second, the way the Bollinger Bands are pinching down means there's decreased volatility meaning 1. Cheaper contracts 2. Decreased periods of volatility precede high volatility, more indication a big move is coming. Third, Ichimoku clouds are a tool I’m still studying. But the confluence of the fib and cloud at the 155.38 mean it will be a stiff resistance level. Once over the cloud will be a bullish signal and can see higher.

Brent OIL; Hard Way But will Grow!Corona vaccination.

Biden.

Increase shipping.

And etc that you now better.

ROOT - Root helps Global 2000 companies around the world with strategic change management and digital transformation to solve critical organizational challenges. It is also a parent company of the millennial

As long as $14 hold, I am playing it. Looks like could be a replay of Upwork chart. Great company, great story - shitty price action. I like it. Not enough data to "analyze" it but looks good enough. I like the inverted head and shoulders on RSI and double bottom (as long as its not breached, otherwise there is no floor). Good luck out there!

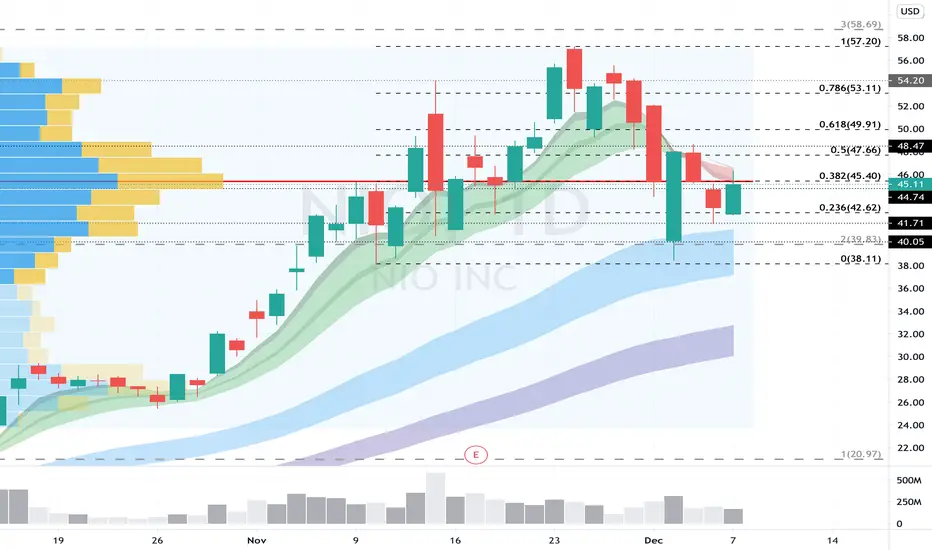

NIO over 48.47The earlier frenzy has worn off a bit and more importantly this has cooled down. Some consolidation and chop which may clear up over 48.47.

Chargepoint (SBE): Potential Exponential Growth AnalysisChargePoint, an electric vehicle charging network, has struck a deal to merge with a SPAC (Special Purpose Acquisition Company), Switchback Energy Acquisition Corporation (SBE), with a market valuation of $2.4 billion.

In this analysis, I'll be going over the company's business model and financials, as well as technical analysis of the very short price action history we have available.

What is Chargepoint?

- Founded in 2007, ChargePoint has built one of the world’s leading electric vehicle (EV) charging networks

- The company delivers a fully integrated EV charging solution, with a comprehensive portfolio of hardware, software and services

- It recently received an enterprise value of $2.4b.

- Essentially, while companies like Tesla (TSLA) and Nio (NIO) compete for dominance in the EV market share, Chargepoint (SBE) offers the infrastructure necessary for all EVs.

Market Outlook

- EVs are projected to consist 9.9% of all new vehicles sold in 2025 and 29.2% in 2030 in the U.S. and Europe.

- The trend is definitely green, especially with Biden essentially having been elected as president recently.

- In the market of Network L2 Charging, Chargepoint takes up 73% of the market share, 7x more than its closest competitor.

- I always emphasize the importance of choosing the number 1 stock in the industry or field, and Checkpoint qualifies.

Financials

- Chargepoint demonstrated good revenue growth until this year

- It did $66m in 2017, $92m in 2018, and $147m in 2019.

- However, due to the Corona virus pandemic (Covid-19), the expected revenue for this year is at $135m.

- Nonetheless, the company has very bold goals as it seeks to reach a $2b revenue target by 2026.

- This would indicate a 40% compound growth rate per year over the next 6 years.

- While they are still at a net loss, Chargepoint is currently sitting on $648m of cash, so their cumulative net loss of $347m can easily be covered.

- By 2026, which is when the $2b revenue target is hit, we could see the company reach net profit

- Their gross margins have been deteriorating due to massive expansion and scalability of infrastructure around the world.

- However, it's important to understand that these are one time costs, and we could expect Chargepoint's gross margin to grow from 13% in 2019, to 42% by 2026.

Technical Analysis

- Because Chargepoint was listed through a SPAC recently, it does not have much price action data to be analyzed.

- Based on the hourly chart, we can see that prices are ranging in a slow uptrend, forming higher lows and higher highs

- It's trading within an ascending parallel channel, in an extremely choppy range

- There are currently three key levels of support on the hourly, formed through gaps

Summary

This company's fundamentals for the long term appears extremely solid. It has high growth potential, dominant market share, and is part of a megatrend industry of EV infrastructures. We would have to see whether the company delivers, according to their IR deck, but the overall outlook remains very bullish.

If you like this analysis, please make sure to like the post, and follow for more quality content!

I would also appreciate it if you could leave a comment below with some original insight.