Chart of the Day: $HYG under pressure$85.50 is the key neckline support for $HYG as it bounces off the top boundary of wedge pattern. The neckline can be seen with multiple previous SSR levels. The downward bias is reinforced by the current SSR level for which price action is firmly pinned under.

With an earnings recession in progress and oil demand in question, it is inevitable to see some stress emerging in the junk bond segment which has a fairly high representation of US shale players.

HYG

BKLN vs. HYG | Leveraged Loans Underperforming High YieldEarlier this year I pointed out how leveraged loans are increasingly in a precarious position as underlying economic fundamentals deteriorate around the world. Another way of measuring the risk premium is to observe the performance spread between the leverage loan bonds (orange line) and high yield bonds (candles). Both are in logarithmic scale.

High yield corp. bondsbig wedge forming over last two decades. no where near ATH's, unless MMT works. $SPY

$HYG - High Yield Bonds Sending a Sign?As can be seen on its weekly chart, the $HYG appears to be sending a warning signal. On a technical basis, a "Shooting Star" pattern has emerged, coupled with negative divergence in the SMI and RSI indicators.

To us, it appears that high yield bonds are sending a signal that its rallying may be getting a little stretched.

We would caution investors to tread carefully and take some money off the table if in this space.

TRADE IDEA (IRA): HYG SEPT 20TH 82 SHORT PUTMetrics:

Max Profit: $173/contract

Buying Power Effect (Cash Secured): $8026

Break Even: 80.26/share

Delta: 31.71

Theta: .67

Notes/Comments: Up to this point, I haven't posted many of my IRA trade ideas, primarily because they are way longer-dated setups than people are generally interested in, and I've also been an infrequent buyer of the underlyings that make up my portfolio -- a fairly mundane mix primarily made up of SPY, EFA, TLT, and IYR covered calls where setup management consists of looking at the short calls from time to time and rolling them out for duration, credit, and further cost basis reduction. It isn't very exciting, and I may not have to do much for weeks, if not months, in certain cases.

Naturally, this trade is not going to be attractive to everyone; you are, after all, going to be tying up $8k of buying power for a very long time with a return on capital of about 2.16% if you do nothing and the short put expires worthless. For me personally, I have idle cash sitting in the IRA earning virtually nothing, and I don't anticipate adding to my core positions in short order given my cost basis, where these underlyings are in the grand arc of time, and my proximity to retirement. Moreover, one of my basic IRA rules is not to undertake single name risk, so my basic options are (a) do nothing; or (b) stick something out there and get paid to wait for the price at which I want to acquire.

Here, I'm interested in acquiring HYG with its attractive 5.46% yield, but at a price discounted substantially over where it's currently trading; otherwise, I simply don't want the shares. I can either wait until price gets there or sell puts that will result in a cost basis at or below what I'd like to get in at if I'm assigned. Here, I'm opting for the latter ... .

Post fill, I'll periodically look to roll for duration and credit to reduce cost basis further.

Head n Shoulder - High Yield Junk Bonds!! SHORTLong Term setup here - you know what to do.

Targets Marked on chart.

Small Caps Lead Broader Markets $IWMSmall caps are often used as a gauge for domestic growth because they are more sensitive to changes in economic conditions, such as input costs, wages, financial stress...

Many were caught off guard by the equity rollover in early October, but few were paying attention to what was occurring. In late September, financial conditions began to tighten and credit spreads began to roll higher. I wrote about this several times for my subscribers. There is a strong correlation between dollar strength and rising credit spreads.

twitter.com

The correlation between small caps (IWM) and credit is rather significant. The 30-week correlation between junk (HYG) is .92 and investment grade (LQD) .85. It's also important to understand that over half of all Russell 2000 companies make no money, which is detrimental when margin compression occurs.

There is no reason to doubt why the Russell rolled over, leading broader U.S. equities, just as financial conditions began to tighten.

The Curve Is Falling, The Curve Is Falling $TLT God bless the legacy financial media because their uselessness is a blessing.

Headline to headline is no way to live through live whether you trade oil or bitcoin. The click du jour is how the 2s/5s yield curve is now inverting, and the 10s/2s are at a mere 11 bps.

I have been one of the largest flat curve-ers out there. Why? Because my process shows why the decelerating in rate in change in both growth and inflation will sink the back-end and the front steepening eases.

On Sept. 6, I wrote in "Cognitive Dissonance: What the Yield Curve Is Saying:"

"A lot of headlines have fluttered across the wires on the 10s/2s yield curve on a continuous path to inversion. Neckties on legacy media continue to say a flat or inverted curve doesn't mean much.

I reckon, given the directional trajectory of both the curve and MVR inflation matrix that the curve is signaling market's expectations on inflation.

Generally, this would make sense given that the steepening from a curve inversion is triggered by the fed's policy stance on interest rates during the end of the cycle."

The concerns about increasing U.S. supply in paper is valid, but the concerns of too much debt issuance over demand becomes "where do I put my money" concerns.

That's likely treasuries, increasingly so as investment and junk credit continue to breakdown.

Strong #Dollar Themes ContinueOn October 30, I published "Stronger Dollar Themes To Continue" for my subscribers, which gave a unique approach to why the dollar is rallying even tho traders foresee Fed policy getting dovish: credit spreads.

"Now, when comparing credit spreads to the financial crisis it doesn't seem to be "that big." Combine record U.S. corporate debt, a highly distorted high-yield market and slowing economy, and you got the makings of a credit crisis. The move this year is not only noticeable, but inflects from the previous couple years of lower-lows."

"The rate of change in spreads is remarkable, actually. Just look at the move in spreads and the monthly close of the trade-weighted dollar index (major FX)."

As credit conditions breakdown and high-yield/investment grade spreads widen, the dollar continues to march higher as a representation of the dollar shortage.

Take a look of what the HYG+LQD basket (inverted scale) does when the dollar strengthens:

Now take a broader look:

Near-term quantitative ranges are dotted, while longer-term levels are solid. By Q1-19, the DXY will likely be triple digits if not sooner.

Short HYG (High yield bond) How can you bullish equities?HYG clear clear cannot be more clear cup and handle. How can you be long equities now, super risky.

Yes, Still Bearish on $EURUSDParity in play? Think so.

Here's a small snippet from tonight's subscriber note:

"Typically, U.S. corporations push dollars into Europe at the end of the month, and that is likely not going to happen. Stress will remain.

I still believe the DXY could reach triple digits and EURUSD will retest 1.05. Potentially, I foresee a test of parity by mid-2019 unless current trends change course dramatically."

SPY vs. HYG convergence / divergenceCurrent convergence is Bullish to Neutral. Will the Bullish convergence hold?

UPDATE: High Yield credit supports long EURUSD s/t tgt 1.203Hi guys, thank you for the support! I will have this analysis out each weekend as well as daily updates throughout the week, if you guys like what I'm doing hit the "follow" button and you will get a notification each time I post a video or chart!

Have a great day everyone!

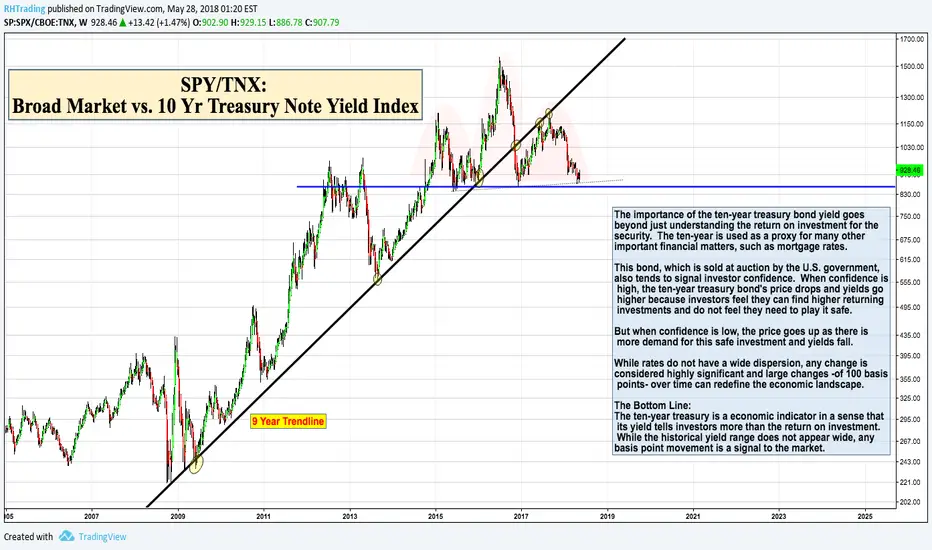

Charts That Make You Go Hmmm... (SPY/TNX)Thank you to all my followers that take the time to read this with me.

Some historical background on the importance of the 10 year Treasury Note Yield Index. (Hey, we all need to brush up on it from time to time)

This is a ratio chart of SPY/TNX with a 9 year trend. As is the case with most charts related to interest rates, it's pretty technically perfect.

I've always found this interesting because this is a market that is almost 100% Fundamentally driven, yet produces the cleanest technicals, but I digress.

I just stumbled across this ratio chart, as interest rates are increasingly on my radar. I think the chart is self-explanatory for the technicians out there.

Lastly, let's play 'Guess-That-Pattern' on the weekly 9-Year chart. Good luck to all.

Are stocks crashing? Watch the junk credit spread.With the increased volatility this year after such a long period without any significant declines has got some wondering if the market has peaked, or even about to crash. To get a better idea of what’s going on ‘under the hood’, we can study the high yield ‘junk credit’ market. High yield is also known as ‘junk credit’ for its higher risk of default and being rated below investment grade. This heightened risk means greater sensitivity to market conditions, and can serve as a 'canary in the coal mine'.

The Merrill Lynch High Yield index has a yield of 6.36% at the moment. This is close to the 6% combined ‘yield’ of the S&P500 trailing earnings and dividend. When junk bond market is under stress and fear of default is rising, the yields ‘blow out’ or spike quickly. (We’re seeing this happen right now with concerns over TSLA credit).

The chart shows how yields 'blew out' during times of stress. The orange line is the additional yield offered by the high yield index after subtracting the ‘risk free’ treasury rate. This ‘spread’ gives us a better idea of the risk premium demanded by junk credit investors. Currently the spread remains lower in around the range under 3.6%.

The S&P500 index in blue is compared to the Merrill Lynch B grade corporate yield spread. At each of the previous peaks before the stock market crashed, there was a sudden spike in the credit spread. We even saw this spike in 2011 and 2015 when default fears increased. At the moment we’ve yet to see a similar jump in the high yield spread. Which would suggest that currently investors are not sensing any increasing risk of default (at least for now). A spread approaching the long term median or average range of 5% would give cause for alarm.

The Merrill Lynch high yield spread chart is updated daily here:

fred.stlouisfed.org

The WSJ updates bond benchmarks daily here:

www.wsj.com

HYG Breaking DOWNImportant to note the High Yield Bonds broke the closing low from the Feb lows. This is very bad. Market down side continuation is almost assured. Considerable down side risk in these bonds.

Rolling OverHi guys. It appears that HYG has lost its positive momentum and we're observing a possible roll over on the weekly chart. I'm not an expert and just want to share some observations. It's my understanding that HYG is almost like an index. I wish everyone good trading.

Credit - HYG & BIZD- BIZD looks like a descending triangle and HYG is in down channel

- a bounce is possible but the long term pattern is not bullish

HYG BIZD bearish trend - BIZD leads HYG and divergence gives confirmation of pattern

- BIZD currently in down channel

- Longer time frame, H&S pattern in formation

- bigger move if H&S pattern play out and take times for the formation

HYG correlation with SPY/QQQ/IWM-30D correlation turns -ve for SPY/QQQ/IWM

- since 2009 only 4 cases

- the first sample occurred at low and market turn higher later

- other 3 cases show bumpy road ahead. Pullback when HYG hit lower

$XLF Is the Financial Pullback Something More? (includes video)U.S. financial stocks have been in pullback mode this week despite the SPX moving higher. Considering that financial stocks had been a big boost to market gains over the last several months, this could be concerning.

The XLF is down about 3% - and regional banks KRE down 6% - since the recent top. Let's put this move into context, shall we?

As MacroView as posted before, financial stocks really began to rally in early Sept just as the 10s/fed funds curve bottoms around 90 basis points. The correlation has been rather strong between .65 to .93.

In our view, the curve and financials rallied on two things: markets were trying to price higher inflation (we saw this as the long-end steepened) vis-a-vie higher commodity prices. Then, markets were anticipating Pres. Trump nominating John Taylor as the next fed chair, who would be uber hawkish.

We were happy to take the other side of that bet. Powell is dovish. In turn, we saw yields and copper, particularly, head lower.

The 10s/fed funds rate topped out at 131 basis points and began to trade lower on the above events. Price action in XLF and KRE weakened and the pullback ensued.

Click the here to listen to where support may be found and whether or not financials and the curve will rebound.

Check us out on twitter @macro_view