BOUGHT TO COVER SPX AUG 12TH 2100/2115 SHORT PUT VERTWith 4 DTE left in this troubled post-Brexit setup and the short put side nearing worthless, I bought to cover it for a .15 ($15)/contract debit, rolled out the short call side from the Aug 12th 2145/2160 to the Aug 26th 2155/2175 for a .55 ($55)/contract credit, and sold a 83% probability of profit short put vert against in the same expiry for an additional 1.05 ($105)/contract in credit, leaving me net credit on the roll and with an Aug 26th 2120/2130/2155/2175 iron condor.

Still looking to exit this for scratch or better, but have to pour through the chain to calculate my scratch point ... .

Ironcondor

NEW TRADE: SOLD RUT/IUX AUG 19 1110/1120/1230/1240 IRON CONDOR... for a $323/contract credit.

This is my standard 85/75 iron condor setup for skewed instruments like SPY, IWM, QQQ, RUT, SPX, etc. (i.e., short call at the 75% probability out of the money strike; short put at the 85% ... or as close as I can get to those).

As usual, will look to take off the entire setup as a unit at 50% max profit.

BOUGHT TO COVER GLD AUG 12TH 117/121 SHORT PUT VERTWith the short put wing of this Brexit wracked setup approaching worthless, I closed it today for a .04 ($4)/contract debit.

I then rolled the short call side out to the August 19th expiry to the 121/126 for a .50 ($50)/contract credit and (inadvertently) sold an overlapping short put spread against it for a .25 ($25)/contract credit. (This is what happens when you're busy and do stuff on the phone app ... ). Hopefully, price doesn't whip back into the put side, and I can fix the overlap with the next roll ... .

CLOSING: SPX JULY 29 2085/2095 SHORT PUT VERTThis is one of a trio of post-Brexit trades in RUT, NDX, and SPX that I put on post-Brexit and that moved, well, a little more than I'd like ... .

Today (with 2 DTE to go), I closed out the put side for a .15 debit, and then rolled the call side from 2115/2125 to the 2145/2160 for a .30 credit and then sold the Aug 12th 2100/2115 for a 1.50 credit (giving me the pictured setup). As with my GLD and RUT trades (and soon, my NDX iron condor if price doesn't peel off substantially from the highs), I'm looking to lather, rinse, repeat with net credit rolls (i.e., credit received exceeds any debit paid for rolling) until I'm able to exit the setup for scratch or better ... .

Notes: Some people choose to allow the side approaching worthless to expire that way if there is a "high likelihood" that will occur (there was here with the put side). I generally choose to close it out "just in case" something unexpected occurs ... . It's just not worth the extra $5-$15 you'll make, Weird stuff has been known to happen.

CLOSING: GLD JULY 29TH 118.5/121.5 SHORT PUT VERTThis was my only "Bremain" bet trade, and it's taking its sweet time coming off the highs ... .

The trade started out as a directional spread -- a short call vertical, that was soon breached post-Brexit. My recollection is that I proceeded to sell a short put vert against the call side (completing an iron condor) to protect the call side from further upmove. Here, I'm closing out that protection at near worthless, rolling out the short call side from 119/122 to 120/124 for a .18 credit and then selling a short put vert against the call side for an additional .28 credit.

The resulting setup is basically an iron fly, albeit with the short put above the short call. The perfect outcome would be for the underlying to move right to 120.5 or so at expiry, which is unlikely to occur. Rather, the notion here is to lather, rinse, repeat with the net credit rolling while keeping track of my scratch point to eventually exit the position at scratch or better ... .

EARNINGS PLAY: NFLX JULY 29TH 85.5/111 SHORT STRANGLEUnfortunately, the only underlying announcing earnings next week that has sufficient implied volatility to consider selling premium in is NFLX, with an implied volatility of 52%.

It announces earnings on Monday after market close, so look to put on a play some time on Monday, preferably right before the NY close.

Preliminarily (I'm checking this crap in off hours, so it's rarely spot on), here are the metrics for the two setups I would consider doing:

NFLX July 29th 85.5/111 short strangle

Probability of Profit: 74%

Max Profit: $215/contract

Max Loss: Undefined

Break Evens: 83.35/113.15

NFLX July 29th 81.5/85.5/111/115 iron condor

Probability of Profit: 70%

Max Profit: $99/contract

Max Loss: $301/contract

Break Evens: 84.51/111.99

Naturally, strikes may need to be tweaked slighly depending on price movement on Monday.

SOLD IUX/RUT JULY 29TH 1000/1010/1160/1170 IRON CONDORBecause I have virtually nothing on from having gone almost entirely flat pre-Brexit, I slapped this bugger on in the NY morning session ... . It's basically a "classic" skewed instrument iron condor, with the short call at the 75% probability out-of-the-money strike for the expiry; the short put at the 85%.

Filled for a $325/contract credit ... .

ROLLING: NDX/IUXX AUG 5TH 4350/4375 SPV TO 4400/4425Rolling up the put side yet again (I've basically rolled the thing into an "iron butterfly" (filled for a .90 credit ($90)) to defend the call side.

I generally don't like to "invert" condors (here, roll the put side beyond the call side), so I'll probably just leave the setup alone running into expiry, but keep an eye on the setup's net delta and make a decision as to whether I want to erect a separate delta hedge (in this case, most likely another short put vertical set up in a separate expiration) to protect the position from further upside and/or mitigate call side loss.

Otherwise, I'll just do my usual close out the worthless side, roll out the tested side for minimal strike improvement, and sell a put side against for a credit that exceeds the price to roll the tested side.

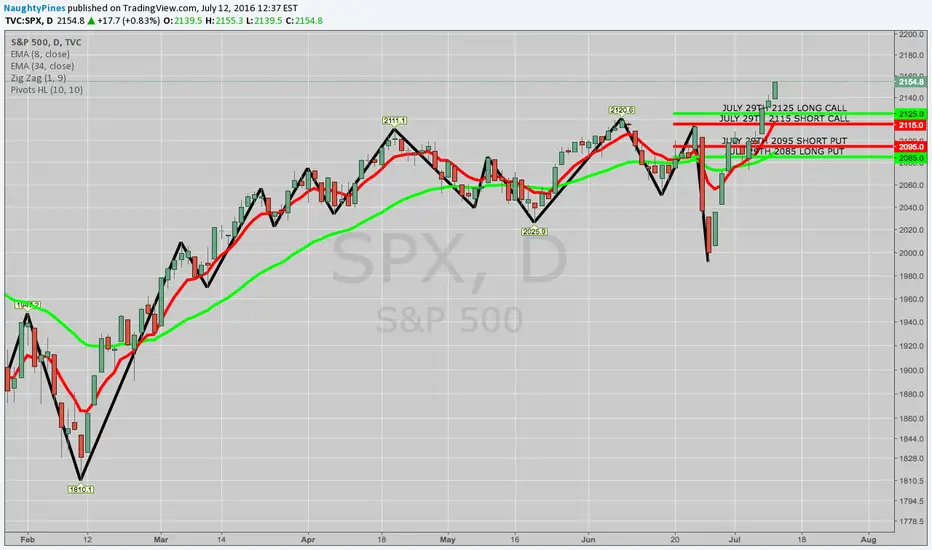

BOUGHT SPX JULY 22ND SPV TO CLOSE, ROLLED CALL SIDE FOR DURATION1. Closed the July 22nd 2020/2030 short put vertical for a .15 debit, as it's near worthless and done its job.

2. Rolled the July 22nd 2110/2120 call side out a week to the July 29th 2115/2125 and slight strike improvement for a .75 debit. The improvement isn't much, but I like to do these improvements small and over time until I get the required movement to exit the entire setup.

3. Sold the July 29th 2085/2095 short put vert to finance the call side roll for a 1.05 credit.

As with my NDX setup, what I need now is some movement back toward the call side to exit the entire setup at or above my "scratch point."

ROLLED NDX AUG 5TH 4250/4275 SHORT PUT VERT TO 4350/4375... for a $137 credit to defend my breached call side.

This thing is starting to morph into an "iron fly" ... . I will naturally need price to move significantly back toward my call side strikes before expiry to not have to roll the call side out for duration/strike improvement. Nature of the beast ....

NOTABLE HIGH IV STOCKS WITH IV > 50%1. P, 79%

2. FCX, 76%

3. X, 75%

4. TWTR, 67%

5. STX, 57%

6. ABX, 56%

7. NFLX, 56%

8 GG, 53%

9. SLW, 52%

Naturally, we are coming into earnings season here, so there's a reason that some of these have high IV here (e.g., NFLX announces in a week and a half). Ordinarily, I like IV to be >50% and IVR (current IV's level relative to where it's been for the past 52 weeks to be high, too), but I may not find a great deal of 70%+ IVR plays here with broad market volatility so low (VIX finished the week below 15).

Neverthless, it may be worthwhile to churn through this small list for premium selling plays (iron condors, short strangles, short straddes), assuming there's sufficient time before earnings to sneak a play in. Otherwise, it's probably best just to wait to do the standard volatility contraction play surrounding earnings ... .

IWM/RUT "CLEARLY SUPERIOR" FOR AUG PREMIUM SELLING TO SPY/SPXIWM/RUT's respective IV's for Aug expiry are 19.0/19.6%; SPY/SPX's are 14.3/13.9%.

With a RUT Aug 19 neutral iron condor setup currently offering nearly 1/3rd the width of the wings in credit, that's the way I'm probably going to go this coming week with my weekly broad index premium selling play ... . I'll post a setup once we get there (I usually do these on Tuesdays).

TRADE IDEA: RUT/IUX AUG 19TH 1060/1070/1200/1210 IRON CONDORI'm not going to take this particular trade (as I've already got a RUT IC on at the moment), but figured I'd post one anyhoo while I wait for earnings.

Metrics:

Probability of Profit: (Software's being glitchy here in off hours; should be between 55 and 65%)

Max Profit: $331/contract (nearly 1/3rd the width of the wings, which is what you're shooting for generally in these)

Max Loss/Buying Power Effect: $669/contract

Break Evens: 1067/1203

Theta: 5.15

Delta: -2.61

Notes: Naturally, these are off hours quotes, so you may have to fiddle with strikes and fill price at open. Look to take this off at 50% max profit.

ROLLING SPX AUG 19TH SHORT PUT VERT TO 2015/2025As with my NDX/IUXX iron condor, playing defense here, and rolling up the put side for an additional $45/contract credit.

Still shooting for 50% max of the original setup ... .

ROLLING NDX/IUXX AUG 5TH SHORT PUT VERT TO 4250/4275What's new? Playing defense of the call side here on this up move.

Rolled for an $85/contract credit ... .

Still shooting for 50% profit of the credit received for the original setup, but will need a little assistance to the downside to get there.

TRADE IDEA: SPX AUG 19TH 1955/1965/2155/2165 IRON CONDORA bread and butter trade offering about just about 1/3rd the width of the wings ... .

Metrics:

POP%: 58%

P50: 74%

Max Profit: $330/Contract

Max Loss/Buying Power Effect: $670/contract

Theta: 5.26

Delta: -2.52

Notes: As usual, may have to piddle with a fill. Price will dance across the mid by .10-.20. Look to take it off at 50% max profit.

WBA EARNINGS PLAYSWBA announces earnings tomorrow before market open, so look to put on a play before today's NY close.

Here are the metrics for defined/undefined risk setups:

WBA July 15th 76.5/90 short strangle

POP%: 76%

Max Profit: $106/contract

Max Loss/Buying Power Effect: Undefined/$1031/contract

WBA July 15th 74/78/89/93 iron condor

POP%: 67%

Max Profit: $104/contract

Max Loss/Buying Power Effect: $296/contract

Notes: Shoot to take these off at 50% max profit and move on. For the short strangle, the buying power effect metric is quite "ugly." For the iron condor, I had to bring the wings in to squeeze $100+ out of the setup, which lowers the probability of profit (POP) of the setup heftily. There are always trade offs between max profit potential, buying power effect (defined vs. undefined), and probability of profit ... . To gain with one metric, you inevitably give up ground on another ... .

PREMIUM SELLING CANDIDATES FOR TUESDAY -- CY, HOG, POTWith broader market volatility bleeding out of the markets, I'm on the hunt for non-index premium-selling plays, and there are a few that have popped up on my radar. That being said, earnings season is nigh, so it might be best to be particularly selective as to individual underlying plays, keeping powder dry for the actual earnings, rather than pulling the trigger here such that you have to guide the setup around the actual earnings announcement. In any event, here are a few to look at:

Individual Underlyings

CY: implied volatility rank 100, implied volatility 78. The unfortunate thing about Cypress Semiconductor from a premium selling standpoint is its price, which limits the profitability of iron condor/short strangle setups. Where this is the case, the go-to is a short straddle. Preliminarily (looking at off hours quotes here), an August 19th 10 short straddle will bring in $228 in credit with break evens at 7.72 and 12.28, which would fit in nicely with CY price action. However, if you're looking to take the straddle off at 25% max profit (the usual goal for straddles), you're not looking at a tremendously great play here, even though these little "grounders" add up over time ... .

HOG: implied volatility rank 100, implied volatility 63. Preliminarily, an August 19th 42.5/65 short strangle would bring in $168/contract, the drawback being that the underlying only offers monthly expirations ... .

POT: implied volatility rank 70, implied volatility 51. Like CY, you won't be able to get much out of a play if you go short strangle or iron condor, leaving you with a short straddle as the go-to setup. The August 19th 17 short strangle will bring in $227/contract credit with break evens of 14.73 on the lowside, 19.27 on the topside which is not a bad fit for what POT is doing on its chart (essentially, sideways chop between 15 and 20).

Exchange-Traded Funds

The ETF space is not looking particularly attractive here, with the vast majority of them sub-50 in implied volatility rank. The one standout is SLV (coming in at 70), but you won't be able to get much premium out of an SLV play due to fairly low implied volatility (currently 34, which is fairly high for SLV), although it looks enticing for some kind of directional play (bearish assumption).

TRADE IDEA: NDX/IUXX AUG 5TH 3825/3850/4425/4450 IRON CONDORMetrics:

Probability of Profit: 63%

P50: 74%

Max Profit: $830/contract

Max Loss/Buying Power Effect: $1670/contract

Theta: $16/contract

Delta: -1.69/contract

Notes: $820/contract was the mid price pre-market; as usual with these large instruments, you have to do a little "price discovery." Will look to take it off at 50% max ... .

ROLLING SPX JULY 22ND 2140/2150 SCV TO 2110/2120Rolling the call side of my July 22nd SPX iron condor down a few strikes to delta balance here ... . (I basically rolled it to the 75% probability out-of-the-money short call strike).

Filled for an $80/contract credit.

Scratch Point: The original setup was put on for a $280/contract credit, and I brought in an additional $80/contract for this roll, so my current scratch/break even point for the trade is $360 per contract (exclusive of fees/commissions). Because I'm still shooting for 50% max of the original setup (or $140 per contract), I'll look to take this off for the scratch point ($360) minus the original profit goal ($140) or for about a $220 debit ... .

SOLD TO OPEN: SPX JULY 22ND 1920/1930/2140/2150 IRON CONDOROut of one SPX iron condor ... into another. Did this from my phone, so I don't have the exact metrics on this little fella, but it was supposed to be a "classic" skewed instrument iron condor, with the short call strike at the 75% probability out-of-the-money strike and the short put at the 85% probability out-of-the-money strike for the expiry.

I usually like to shoot for getting a fill at 1/3rd the width of the wings (i.e., 1/3rd of $10 or about $3.33). Since I was doing it from my phone (not ideal, lemme tell ya), I wasn't as surgical as I usually am with these setups, and settled for a $280 credit fill ... .

As usual, I'll look to take this off at 50% max profit or about $140/contract ... . Next week, I'll probably look at similar setup in RUT, since it is likely to have higher implied volatility than SPX and therefore juicier premium to be had.

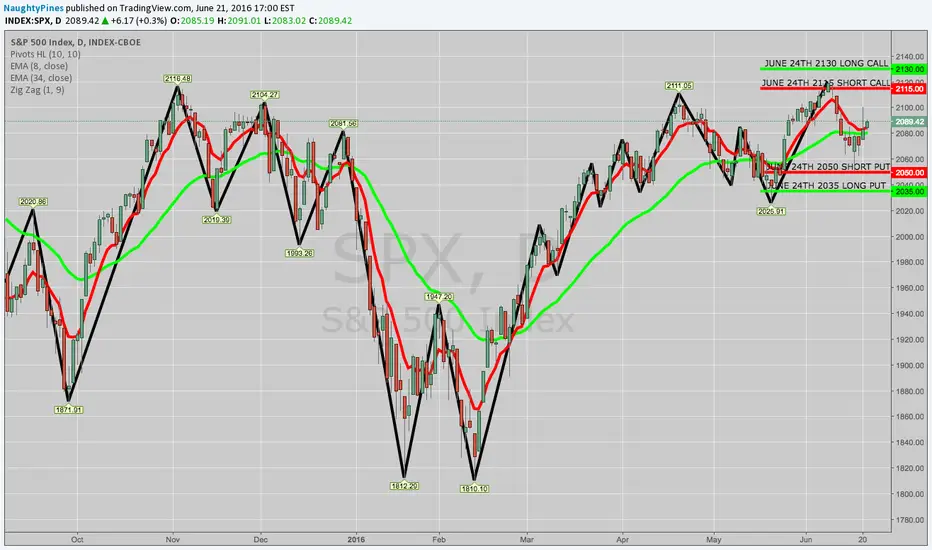

ROLLING SPX JUNE 24TH 2105/2120 SHORT CALL VERT TO JULY 8THNot every trade works out ... . The original notion of this iron condor was that, pre-Brexit, we'd pin at 2085 or so as traders basically sidelined themselves waiting for the outcome. No such luck with late polling showing a Remain lead. At market open, I closed out the short put side and then rolled out the call side (for a $35/contract credit; this was before price broke 2105) for a couple of more weeks to let the market digest the vote and then go from there. Since it looks like we're going to see more upside, I also sold a put side against for an additional $80 credit (I just noticed that I did a $10 wide; I'll widen it to $15 if there is continued movement to the upside and I can sensibly roll the put side in).

Currently, my scratch point is $750/contract (excluding fees/commissions). (The scratch point is calculated by taking the total of the credits received for the original setup, plus any rolls, and subtracting the total of the debits, fees, and commissions paid). The original setup was put on for about a $300/contract credit, at which time I was shooting for 50% max profit or about $150/contract. Consequently, I'll look to take this off at the scratch point ($750) minus that $150 target or about $600/contract.

SPX OPTIONS AND BREXIT -- KNOW WHAT YOU'VE GOT, PLAN ACCORDINGLYThe vast majority of SPX options I play are Friday a.m. settled. Ordinarily, this isn't a horribly big deal, but the fact that these are Friday a.m. settled makes it a "horribly big deal" this week. This is because after NY close on Thursday, I won't be able to do anything with them. They will essentially be "locked" and "settled up" on the basis of Friday a.m. prices, taking into account what the market has done overnight. Naturally, this could be a major bummer because Brexit results are likely to be known when NY is closed and futures will move in the overnight hours. What to do?

First, know whether the options you have are Friday a.m. or p.m. settled. There are some SPX options that do settle on Friday p.m. (The same goes with RUT and NDX; know your settlement date and time ).

Secondly, attempt to avoid taking the setup "down to the wire." Ideally, you should be attempting to either close options setups out in profit with 4-10 DTE or look to roll a tested side or a side that is "too close for comfort" out for duration in this time frame. (In this particular case, I'm waiting to take this iron condor off until the last minute because I think price is going to be pinned here around 2090 running into Brexit).

Third, if you're absolutely set on taking the setup down to the wire, know your "drop dead" day and time and plan accordingly (I know I'm basically repeating myself here). For me, Thursday NY close is my "drop dead" date and time. I either have to shut the whole show down or roll something out before then ... . I won't be able to do it on Friday.

Good luck around Brexit, everyone!