ROLLING (AGAIN): SPX JUNE 24TH 2130/2140 SCV TO 2120/2135With a mere 9 DTE to go with this setup, this is probably the last roll I'll do here to capture movement and/or delta balance ... .

Filled for $150 credit ... .

Notes: Actually just noticed that I inadvertently widened the spread by $5, which is probably why I got $150 out of it. Lol.

Ironcondor

TRADE IDEA: RUT/IUX 1075/1085/1190/1200 IRON CONDORStaying with short duration index setups here, so that I can be flexible if any non index premium selling opportunities come along; going with RUT over SPX due to RUT's higher implied volatility ... . (As a smaller, alternative trade, you can look at a similar setup in IWM).

Metrics:

Probability of Profit: 62%

P50: 71%

Max Profit: $340/contract

Max Loss/Buying Power Effect: $660

Delta: -3.51/contract

Theta: 12.26/day/contract

Notes: Naturally, I'm looking at pricing in the off hours, so it may be necessary to tweak the setup a bit in terms of strikes and/or fill price on NY open. I'll look to manage this setup aggressively and take it off at 50% max.

ROLLING SPX JUNE 24TH 2145/2155 SHORT CALL VERT TO 2130/2140Keeping this short-term setup fairly delta neutral here ... .

Rolled the 2145/2155 call side down to 2130/2140 for an additional $105/contract credit, resulting in a 2045/2055/2130/2140 iron condor ... .

Still shooting to take the setup off for the original profit target of about $150/contract.

CLOSED GLD JUNE 17 113/116 SPV; ROLLED CALL SIDEGold just won't give me any breaks. It whips to the put side; it whips to the call side ... . Lol.

With 7 DTE and the put side nearing worthless, I closed it out here for $5 (near max profit). I then rolled the 121/124 short call side out to the July 8th expiry for an $11 debit and sold the 114/117 short put vert in the same expiry for a $50/contract, so that I was net credit on the roll.

I still have a July 1st 111/114/118/121 GLD iron condor on in the July 1st expiry, but the put side there still has some value left in it, so I'll probably just leave it alone for now.

BOUGHT TO CLOSE SPX JUNE 15TH 2055/2065/2120/2130 IRON CONDORFigured I'd take the money and run here ... .

Closed for a $235/contract debit. I got $305/contract in credit for the original setup, rolled up the put side from 2000/2010 to the 2030/2040 for an additional $50 credit, and the rolled it up again to the 2055/2065 for an additional $55 in credit. So, total credits received -- $410; closing it out for $235/contract, yields a net of $175/contract in profit ($410 - $235), which is more than I was shooting for with the original setup ... .

Still have the June 24th SPX 2045/2055/2145/2155 iron condor on, which I'll putz with next week ... .

BOUGHT SPY JUNE 10TH SHORT PUT VERTS TO CLOSEWith 10 DTE left in these June 10th SPY iron condors, I'm closing out the put sides at near worthless, leaving me with short call sides to deal with running into expiration.

One was a 199/202 (sold for $29/contract; covered for a $5 debit) short put vertical; the other, a 198/201 (sold for $46/contract; covered for $4).

With so little time left, I figured I'd just ride out the short call sides (they're close; one has a short strike at 211, the other at 210), rather than adding the put side back in here ... . Naturally, I need a dip to have those call sides work out; otherwise, I'll roll them up and out next week ... .

ROLLING SPX JUNE 24TH 2020/2030 SHORT PUT VERTICAL TO 2045/2055As with my other SPX roll today, I'm rolling up the put side of this iron condor a little bit to on this up move to delta balance, for which I received a $50/contract credit.

Still shooting for the profit target of the original setup, which was about $155/contract or so ... .

ROLLING SPX JUNE 15TH 2030/2040 SPV TO 2055/2065 SPVDoing a little delta balancing here in this short duration SPX iron condor I'm managing fairly aggressively ... .

I initially rolled the short side up to the 2030/2040 for a $50/contract credit, and am doing so again here for an additional $55 credit.

I hope that this aggressiveness doesn't come back to bit me in the ass in the little bit of time we have left in the setup (7 DTE). I don't usually like to roll with this little bit of time, but am doing so on this multi-day meltup were having here ... .

ROLLING SPY JUN 10TH 209/213 SCV TO JUNE 24TH 210/214 SCVRolling my SPY June 10th 209/213 short call vertical out a couple of weeks and up a strike for a little more time and a smidgeon of strike improvement (again ... ).

I got this filled for a $22/contract debit and then sold a 199/203 short put vertical in the same expiration for a $41/contract credit, so I'm net credit on the operation, so I've now got a SPY June 24th 199/203/210/214 iron condor in that expiry.

While I plan on continuing to roll the short call side up and out, if necessary, I'm naturally looking for price to stay between my 203 short put strike and my 210 short call strike toward expiry to exit the trade profitably.

SOLD JUNE 24TH SPX 2020/2030/2145/2155 IRON CONDORKeeping with the short term engagement trade theme here while I wait for some volatility to sell premium in something ... anything ... (currently, there is no fairly liquid underlying with an implied volatility rank of greater than 70 to work).

Metrics:

Probability of Profit: 58%

P50: 77%

Max Profit: $310/contract

Max Loss/Buying Power Effect: $690/contract

Theta: 8.99/contract

Delta: -3.62/contract

Notes: I'll look to take this off at 50% max profit or earlier if something pops to the forefront with decent volatility ... .

TRADE IDEA: SPX JUN 15TH 2000/2010/2120/2130 IRON CONDORWith few "new" premium selling opportunities available, I'm looking to put on a short-term engagement trade that I will bail out of at the first sign of trouble (or, more likely, the first sign of profit).

Metrics:

Probability of Profit: 63%

P50: 68%

Max Profit: $310/contract

Max Loss/Buying Power Effect: $690/contract

Theta: 10.61/contract

Delta: -2.98/contract

Notes: I generally don't like to put on a premium selling setup in a low volatility environment, but I'm collecting nearly 1/3rd the width of the wings here in credit and the theta (10.61) rates as "drop dead gorgeous sexy." Moreover, the "lay" of the strikes here is good from a charting aspect, with the short call slightly above the 2016 high and the short put below that pesky 2040 resistance ... .

Depending on how things go, I may also consider putzing with strategically and repeatedly rolling the short call side out and to the 75% probability out-of-the-money strike and the short put side out to the 85% probability out-of-the-money strike at particular intervals or when it's profitable to do so.

ROLLING SPY MAY 27TH 208/212 TO JUNE 10TH 209/213More housekeeping ... . With 4 DTE and this 30 handle upmove, this is one of those "too close for comfort" rolls. Truth be told, I'll probably end up rolling it again if we don't come off of this 208 level with some vengeance, but only time will tell. In any event, I got a $40/contract credit for the roll ... .

To protect the rolled short call vertical from further upmove, I also sold a June 10th 199/202 short put vertical against it for an additional $27 credit, yielding a June 10th 199/202/209/213 iron condor.

And we'll see how that goes ... .

TRADE IDEA: SPX JULY 8TH "CLASSIC 85/75" IRON CONDORThis particular setup I consider the "classic" delta neutral index IC setup, with the short put at the 85% probability out-of-the-money strike and the short call at the 75% probability out-of-the-money short call. The short call is placed closer in to current price to accommodate skew and on the general assumption that "velocity" of movement is generally greater to the downside than to the upside (which is why puts in these instruments are generally more expensive than similarly distant out-of-the-money calls), as well as to give you a largely "delta neutral" setup.

Additionally, you're receiving approximately 1/3rd the width of the $10 wings in credit for the whole shebang, which is generally what you're ideally shooting for in these ... .

In any event, here are the metrics for the setup:

Probability of Profit: 60%

Max Profit: $335/contract

Max Loss/Buying Power Effect: $665/contract

Theta: 4.94/day/contract

Delta: -2.04/contract

Notes: As usual, look to take the entire setup as a unit at 50% max profit.

As a total side note, as your account size grows, at some point you will need to consider transitioning away from the smaller index instruments like SPY, IWM, and QQQ to the larger SPX, RUT, and NDX. You can naturally continue to scale up your trade size by increasing the number of contracts and/or widening the wings of your setups. However, increasing the number of contracts also increases fees/commissions. Additionally, widening the wings only goes so far, since -- at some juncture -- the long options really get too cheap and can go "no bid" during the life of the trade, causing you headaches with exiting the spread cleanly as a unit (usually, where that occurs, your only choice is to exit the short option of the spread first, and then wait for an opportunity to take off the long when it's bid again or wait until expiry when it will expire worthless).

Naturally, an interim step between trading SPY and the larger SPX using strictly defined risk setups can be to go short strangle ... .

TRADE IDEA: IWM JULY 1ST 100/103/114/117 IRON CONDORLayering on a bit more bread on my butter while VIX>15 ... . This is about as full a boat as I like to have (not <25% in cash), so I may not be posting many new trade ideas here for a bit; most of them will be closing trades. I know ... boring ... .

Metrics:

Probability of Profit: 58%

P50: 65%

Max Profit: $102/contract

Max Loss/Buying Power Effect: $198/contract

Theta: 1.56/contract

Delta: -4.62/contract

Notes: You know the drill ... . Look to take this off at 50% max profit ... .

TRADE IDEA: IWM JUNE 24TH 102.5/106/115.5/119 IRON CONDORCancelled out the July iron condor in IWM (Post below) and looking for something closer in time with this small volatility pop here, so going with the 38 DTE iron condor ... .

Metrics:

Probability of Profit: 61%

P50: 67%

Max Profit: $108/contract

Max Loss/Buying Power Effect: $243/contract

Theta: 1.89/contract

Delta: -4.72/contract

Notes: Looking to take this off at 50% max profit ... .

TRADE IDEA: IWM JULY 15TH 101/104/117/120 IRON CONDORAfter having looked at iron condors in all the index ETF's, IWM presents the best metrics for a nearer in time setup (my ordinary "thang" is to go >90 days out if VIX is <15, as it is here and <45 DTE if VIX >15).

Metrics:

Probability of Profit: 57%

P50: 69%

Max Profit: $93/contract

Max Loss/Buying Power Effect: $207/contract

Theta: 1.07/contract

Delta: -3.56/contract

Notes: I tried to squeeze out 1/3rd the width of the wings in credit, but didn't want to go any narrower here (the short options are at or near the 75% probability out-of-the-money strike). I'll look to take it off at 50% max profit.

ROLLING SPX MAY 20TH 1935/1945 SHORT PUT WING TO 1980/1990I rolled up the put wing of my May 20th SPX iron condor to balance a little delta here on this upmove, receiving a $55 credit/contract to do so. (I originally legged in first to the call wing, and then into the put wing (See Posts Below), and then I widened the strikes from 5 to 10 at some point, but neglected to post it here ... ).

TRADE IDEA: AUG 19TH 188/191/217/220 IRON CONDORAs previously discussed in my post below, there are several things you can do in a "locally" low volatility environment, one of which is to sell premium farther out in time. If you look at SPY's implied volatility in the June, July, and August monthlies, you'll see that there is a natural gravity toward normalization or reversion of implied volatility to a background level of around 20%, with June having an implied volatility of 16.4%; July, 17.6%; and August, 18.6%. It gets more toward 20% in September (19%) and December (21%), but I don't want to go farther out than two cycles (a lot can happen in two options cycles, and I naturally want to keep buying power free in closer-in-time expirations to take advantage).

Here are the metrics for this setup:

Probability of Profit: 51%

P50: 68%

Max Profit: $109/contract

Max Loss/Buying Power Effect: $191/contract

Theta: .64/contract

Delta: -3.32/contract

Notes: Additionally, I foresee pulling off several SPY setups in profit in the next few days, as we are less than two weeks away from May opex where I've got a variety of setups on, and I don't want to get behind the curve with keeping a certain measure of positive theta on here. It ain't sexy, but bread and butter ain't sexy ... .

TRADE IDEA: SPY JUNE 17TH 193/196/212/215 IRON CONDORWith VIX above 15, I'm layering on some additional SPY in the June monthly here ... .

Metrics:

Probability of Profit: 54%

P50: 71% (explained below)

Max Profit: $100/contract

Max Loss/Buying Power Effect: $200/contract

Theta: 1.53/contract

Delta: -3.97

Notes: The overall probability of profit for the setup is quite low. However, the P50 -- the probability that the setup will reach 50% max profit sometime prior to expiry-- is 71%, which I'm more than satisfied with since I'm getting one-third the width of the spreads for the setup. The other thing is that I already have several iron condors on in that expiry, so I can "mix and match" the short call spreads of one iron condor with the short put spreads of another to peel them off should I want to do that at some point ... .

TRADE IDEA: IWM JUNE 17TH 102/105/115/118 IRON CONDORI don't have an IWM setup on at the moment and with the highest implied volatility among the four index exchange traded funds (SPY, IWM, QQQ, and DIA), this is the place to sell broad market premium ... . Moreover, with similar percentage out-of-the-money strikes, I'm getting almost exactly as much bang for my buck as the June 17th SPY iron condor (see Post Below).

Metrics:

Probability of Profit: 55%

P50: 68%

Max Profit: $99/contract

Max Loss/Buying Power Effect: $201/contract

Theta: 1.50/contract

Delta: -4.14/contract

Notes: As with the SPY iron condor, the probability of profit ain't that great. However, I'm getting 1/3rd the width of the wings, and the probability of hitting 50% max at some point during the life of the setup (P50) is 68%. Moreover, I'll look to layer a few of these on over time in the June 17th expiry, assuming VIX >15, and mix and match short call sides with short put sides to take them off in profit ... .

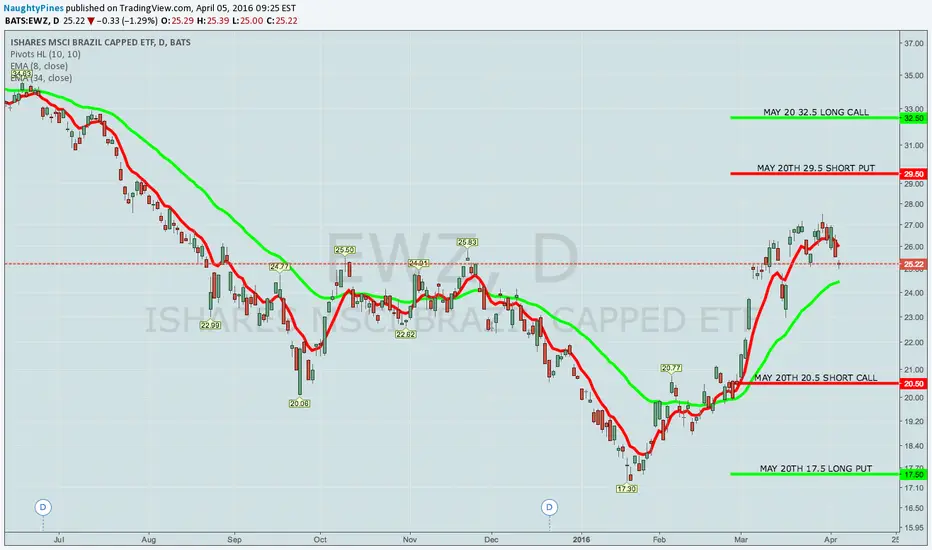

SOLD TO OPEN EWZ MAY 20TH 17.5/20.5/29.5/32.5 IRON CONDORGoing to where the volatility is to sell premium, and that's in EWZ (implied vol rank >70/implied vol is >50). (Plus, I'm kinda ticked that I screwed up closing out that rolled EWZ setup without checking the trade chain ahead of time ... ).

In any event, here are the metrics for the setup:

Probability of Profit: 74%

Max Profit: $66/contract

Buying Power Effect: $234/contract

Notes: I'm continuing to go with small defined risk setups here. EWZ has been "hot" volatility wise, and I may want to layer on additional setups going forward in the instrument, dispersing risk over several expiries. I also want to keep powder dry for broad market premium selling plays and/or additional long volatility setups, depending on which way the market goes ... .

BOUGHT JULY 15TH 180/183/217/220 IRON CONDOR TO CLOSEThis is a "mix and match" of a short put vertical and a short call vertical that were pieces of two separate iron condors I layered on in that expiry during low implied volatility. I'm closing it out for a whopping $40/contract profit here on this down move to reduce some market exposure and free up some buying power for setups nearer in time ... .

VIX >15 MAY WARRANT LOOKING AT ROTATING BACK INTO INDEX ETF'SOrdinarily, when VIX is below 15, I look to get in on long volatility plays, and I piled into them mightily on the sub-13 dip, loading myself up on them, thus spoiling my appetite to partake of earnings in any meaningful fashion.

Now, however, with VIX starting to rotate into +15 territory (today's high was 17.09), I'll turn my attention back to at least looking at index ETF premium selling plays, although -- as always -- higher volatility means higher premium, and VIX at 15.15 isn't actually the index ETF premium selling bonanza we had in mid-December, mid-January, and mid-February.

As of right now, QQQ offers the highest IV out of the four major index ETF's, and my standard, put-skewed iron condor setup (e.g., June 10th 96.5/99.5/110/113; 65% POP; $216 max risk) is offering up $84/contract at the mid price, which isn't horrible (using a four-wide instead will yield $100/contract at the mid price with a $300 max risk). As always, I'll go in small, keeping powder dry for further opportunities to go long VIX/VIX derivatives (if VIX fades here) or other index ETF setups (if VIX continues to rise).