MARCH 11TH SPY IRON CONDORI'm continuing to layer on setups both over expirations and in the March 18th expiry.

Here's one for the March 11th:

SPY 175/178/200/203

Probability of Profit %: 63%

Max Profit: .98/$98/contract

Buying Power Effect: $202/contract

This will be the last setup I put on in SPY between here and the March 18th expiry, except for minor tweaks here and there to balance delta and to keep the body of setups -- as a unit -- fairly neutral. (See Options Tip: Managing Multiple, Single Instrument Setups).

Ironcondor

FB EARNINGS PLAYSFB announces earnings tomorrow after market close, so look to put on any play in the final hours of the NY session.

Here are the two possible plays that may naturally require strike adjustment in light of any movement the underlying experiences during the trading day:

FB Feb 5th 81.5/87.5/107/113 $500 BP Iron Condor

Probability of Profit %: 69%

Max Profit: $101/contract

Buying Power Effect: $499/contract

Break Evens: 86.49/108.01

FB Feb 5th 87.5/107 Short Strangle

Probability of Profit %: 71%

Max Profit: $150/contract

Buying Power Effect: Undefined Risk

Break Evens: 86/108.5

Notes: Look to take off the entire setup at 50% max profit and redeploy the buying power elsewhere; one side or the other when it reaches near worthless (<.05/$5); and be prepared to roll on the break of a side prior to expiration out for duration, selling an oppositional side against for a credit that exceeds the cost to roll the tested side.

SPY FEB 26TH IRON CONDORLayering on a bit more Feb SPY action on before this volatility bleeds out of the market (it inevitably does). As usual, it is skewed to the put side due to vol skew on the call side with the short call strike at the edge of the expected move for the expiration (about 75% probability OTM) and the the short put at about the 84% probability OTM strike (the 1 standard deviation line).

SPY Feb 26th 171/175/196/200 iron condor

Probability of Profit %: 66%

Max Profit: $114/contract

Buying Power Effect: $286/contract

Break Evens: 173.86/197.14

Notes: Look to take off the entire setup for 50% max profit or one side at a time if that side approaches worthless (<.05. or $5.00). If a side is tested, roll that side out for duration and sell an oppositional side against it for a credit that exceeds the cost of the roll of the tested side by some reasonable measure (I usually shoot for a .50 credit in excess of the debit it cost to roll the tested side).

TLT MARCH 11TH IRON CONDORTruth be told, TLT doesn't really meet my premium selling criteria here: its implied vol rank is 28 over the past 52 weeks, 40 over the past six months, 67 over the past 60 days, and 50 over the past 30. Its implied volatility is under 14. In sum, it's not a good premium selling play. Nevertheless, my tendency is to always have a bit of treasuries on, since they enjoy a somewhat inverse relationship to the broader indices, provide bit of balance to broader index movement, and don't suffer from nearly the degree of vol skew the broader index ETF's do ... .

March 11th 119/121.5/132.5/135

Probability of Profit %: 70%

Max Profit: .62/$62/contract

Buying Power Effect: $188/contract

Break Evens: 120.88/133.12

SPY -- "OLD SCHOOL" IRON CONDORAs I may have previously mentioned, it's my habit to stick with broad index ETF, SPX, or RUT plays when there is sufficient volatility there and to pass over plays in individual underlyings. These SPY plays aren't sexy, unfortunately, and they aren't the kind of "boom, kapow!" plays that earnings are ... . Nevertheless, bread and butter is bread and butter.

Here's my standard SPY iron condor with the call side set up at the edge of the expected move for the expiration and the put side setup around the 1 SD line (84% Probability Out of the Money):

Feb 26th 173/176/201/204 SPY iron condor

Probability of Profit: 62%

Max Profit: $100/contract

Buying Power Effect: ~$200

Break Evens: 175/202

Notes: Unlike some of the longer-dated "dynamic" iron condors where I roll the put/call sides toward current price when it's profitable to do so, I'll look to take this entire setup off as a unit at 50% profit and then redeploy the buying power .... .

SPX "AGRESSIVE SHORTIE" 10 DTE IRON CONDORI generally don't do setups that are 10 DTE or less unless they involve earnings plays, but figured I'd use one of these short duration iron condors instead of scalping /ES, which tends to involve a lot of screen time.

Here's the setup I put on today at NY open:

SPX Feb 5th 1785/1795/1930/1940 Iron Condor

Probability of Profit: 60%

Max Profit: $385/contract

It's a very nearly delta neutral setup with the short call strike at the expected move for the expiration and the short put strike at the 84% probability/1 standard deviation line.

I will take the whole setup off at 50% max profit and/or wings off separately at near worthless.

As with all setups, I am prepared to roll a tested side out if that occurs (ordinarily for a debit) and sell an oppositional side against for a credit such that I receive a net credit for the sold oppositional side minus the debit for the roll of the tested side. In that case, I'll look to work that rolled out setup to scratch and/or profit ... .

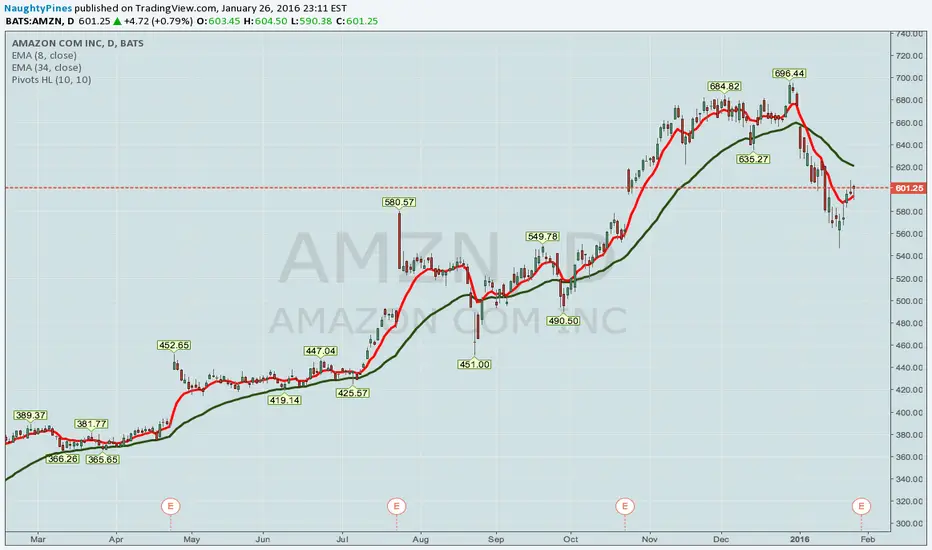

AMZN -- DON'T BE SCARED OF TRADING THE BIGGIES WITH DEFINED RISKPeople frequently remark that they don't like to trade underlyings like AMZN, GOOG, or NDX merely because the price of the underlying is "huge." However, unlike trading these underlyings directly -- a totally unworkable if not inadvisable trade for most people, using defined risk options strategies such as iron condors offer a method to trade these behemoths without putting a lot of risk on the line.

Here's an example:

Feb 5th 525/530/672.5/677.5 AMZN iron condor

Probability of Profit: 69%

Max Profit: $151/contract

Buying Power Effect: $349/contract

Naturally, should you be more risk tolerant, you can merely widen the wings of this setup to increase its max profit potential (which will, in turn, increase the buying power effect); "scaling" the iron condor in this way by either widening or narrowing the width of the wings should make underlyings like AMZN more approachable for the vast majority of traders. ( See the "Scaling" Post, below.)

BABA EARNINGS PLAYBABA announces earnings on Thursday before market open, so look to put on any play in the final hours of the NY session on Tuesday.

Here is one possible play that may naturally require strike adjustment in light of any movement the underlying experiences during the trading day:

BABA Feb 5th 61.5/78 Short Strangle

Probability of Profit %: 70%

Max Profit: $115/contract

Buying Power Effect: Undefined Risk

Break Evens: 60.35/79.15

Notes: I looked at an iron condor setup in off hours, but it may not provide enough juice to be worthwhile. Right now the Feb 5th 56/61.5/78/83.5, a $470 buying power setup, looks like it could get you a .80 credit ($80/contract max profit), but the long call at the 83.5 strike is nearing "no bid" (bid .01/ask .10). Of course, it certainly wouldn't hurt to try during market hours to see if you could get a fill if a defined risk setup is more to your liking.

Look to take off the entire setup at 50% max profit and redeploy the buying power elsewhere; one side or the other when it reaches near worthless (<.05/$5); and be prepared to roll on the break of a side prior to expiration out for duration, selling an oppositional side against for a credit that exceeds the cost to roll the tested side if you have to pay a debit to roll.

AAPL EARNINGS PLAYAAPL announces earnings tomorrow after market close, so look to put on a play before the end of NY trading.

Here are two possibles:

AAPL Feb 5th 84/89.5/110/116 iron condor

Probability of Profit %: 66%

Max Profit: $93/contract

Buying Power Effect: ~$507

Break Evens: 88.57/110.93

AAPL Feb 5th 89.5/110 short strangle

Probability of Profit %: 68%

Max Profit: $142/contract

Buying Power Effect: ~$1600

Break Evens: 88.08/111.42

Notes: With the iron condor, I'm mixing things up a bit with wing widths in order to produce a $500 buying power effect setup; for a person with a $10k account, that setup would represent a 5% BPE for the trade ... .

As usual, strikes may require some tweaking between now and NY close depending on price movement of the underlying.

As with all earnings plays, look to take the entire setup off at 50% max profit and redeploy the buying power elsewhere.

UPDATE: YUM BROKEN IRON CONDORThese earnings plays gone awry usually involve long stories, since it frequently takes a bit of time with rolling, massaging strikes, and such to get the thing into a state where you can exit for at least a scratch.

On October 6th, I played earnings via a 2 contract 72/75/90/93 iron condor, for which I received a .94 credit. Price proceeded to breach the short side, but I closed out the call side for a .16 debit, and then proceeded to roll out the 72/75 short put wing to the Nov 27th expiry for a 1.25 debit, which I matched with an opposition call side slightly above the short put side (same expiry; 73/76) for a 1.74 credit. On Nov 24th, I closed out the call side for .64 debit, rolled out the short put side to the Dec 31st expiry for a 1.78 debit, and again matched it with an oppositional call side (Dec 31 75/78 for 1.66 credit) (so for the last two rolls I've basically been treading water, with debit received for the short put side roll about equal to that for the credit spread ). Truth be told, I had an opportunity to improve the short put side in early December when price broke 76, but wasn't paying attention ... .

In any event, with 10 DTE, I'm looking to close out the short call side here while I can for a profit, as I don't really want to be short call YUM at 75, since I'm generally bullish on the underlying, given the fact that it's their intent to spin off the Chinese business which, last earnings, was a drag on price ... . I'll then proceed to deal with the short put side of the setup as we get closer to expiration ... .

THE "UBER" BREAD AND BUTTER -- SPX IRON CONDORAs mentioned in the post below, there are several different ways to scale up the size of your trades: widening the spreads of your iron condor wings, increasing the number of contracts used, and well as "going naked" via short strangle.

There are also other instruments that can offer you scale for trading the S&P in lieu of SPY -- SPX options and /ES (E-Mini S&P futures or futures options). Basically, 1 SPX = 10 SPY, and 1 /ES futures contract = 5 SPY. Each of these products offers various advantages and disadvantages over one another, including fees/commissions incurred, liquidity, and issues associated with ex-dividends. For purposes of this post, however, I'm only going to be talking about using SPX over SPY as way to scale up the size of your trades instead of either (1) going completely "naked" (which may not be desirable or permissible for some, depending on risk tolerance and the nature of the account involved) or (2) simply increasing the number of SPY contracts utilized, which will naturally increases the fees/commissions paid for those setups with brokers that charge fee that is a multiple of the contracts traded in addition to a commission for the trade.

Here's an example:

SPX 1700/1705/1980/1985 iron condor

POP%: 57%

Max Profit: $180/contract

Buying Power Effect: ~$320

As with the SPY iron condors, you can also scale SPX up in terms of buying power effect by widening the wings. The advantage here is that instead of paying fees/commissions for the equivalent number of SPY contracts (10), I'm only paying fees/commissions associated with a single contract of SPX ... .

NFLX EARNINGS PLAYNFLX announces earnings on Tuesday 1/19 after market, so look to put on any premium selling play shortly before NY close.

Here are two possible setups, which may have to be tweaked, depending on price movement in the underlying:

Jan 29 80/128 short strangle

Probability of Profit %: 77%

Max Profit: $246/contract

Buying Power Effect: ~$1041

Break Evens: $77.54/$130.46

Feb 5th 75/80/127/132 iron condor

Probability of Profit %: 73%

Max Profit: $103/contract

Buying Power Effect: ~$397

Break Evens: $78.97/$128.03

Notes: I went out a little longer than I usually like with the iron condor, as I had difficulty on the put side getting the strikes (and credit) I wanted for the setup with the Jan 29 expiry. The Jan 29th short strangle is also a little wider than I usually like to go, as there is some "funkiness" with the strikes on the put side (they open up to five bucks apart at the 1 standard deviation line, unfortunately). Look to take these setups off at 50% max profit and redeploy the buying power elsewhere.

GS EARNINGS PLAYGS announces earnings on Wednesday before open, so look to put on this play before Tuesday market close.

Here are the plays:

Jan 29 142/170 short strangle

Probability of Profit %: 76%

Max Profit: $180/contract

Buying Power Effect: ~$1749

Break Evens: 140.20/171.80

Jan 29 138/143/167.5/172.5 iron condor

Probability of Profit %: 69%

Max Profit: $136/contract

Buying Power Effect: ~$364

Break Evens: $141.64/$168.86

Notes: As with all these earnings plays, look to cover at 50% max profit for the setup and redeploy the buying power elsewhere.

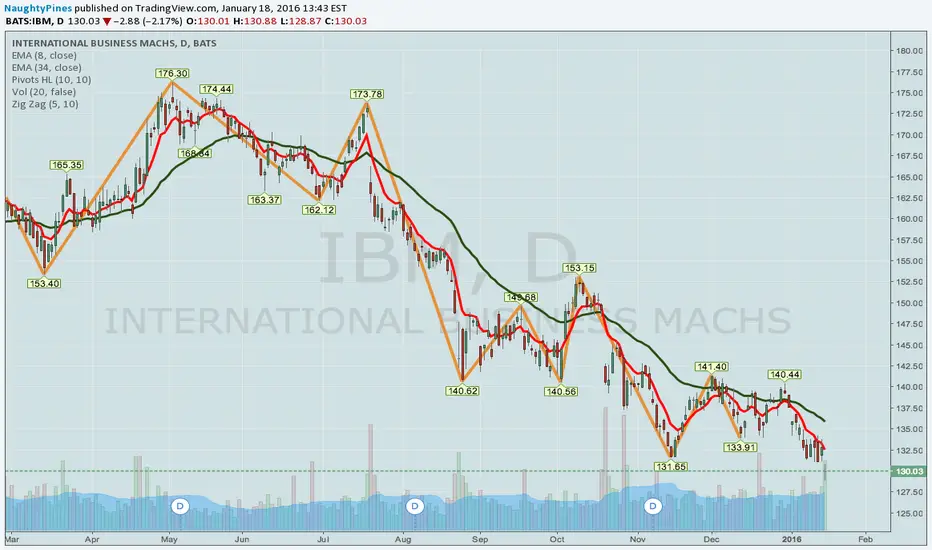

IBM EARNINGS PLAYIBM announces earnings tomorrow after market, so look to put on a play before market close.

Here are two possible plays, but I'm looking at these in off hours, so I'm doubtful that the potential credit to be received is accurate, although the strikes, probability of profit, and break even metrics should be fairly accurate (as usual, they may require a strike of two of tweaking after market open):

Jan 29 119/142 short strangle

Probability of Profit %: 74%

Max Profit: $147/contract (tentative)

Buying Power Effect: ~$1493

Break Evens: 117.53/143.47

Jan 29 116/119/141/144 iron condor

Probability of Profit %: 68%

Max Profit: $21/contract (tentative; if it's ultimately the case that this setup will yield <1.00, I would pass on it or look at widening the wings to yield additional credit, assuming that's consistent with your risk tolerance)

Buying Power Effect: ~$279

Break Evens: 118.79/141.21

Notes: I'm already in an IBM trade left over from last earnings that I'm working on, so I won't be playing this one .... .

NEXT WEEK'S EARNINGS PLAYS -- NFLX, IBM, GS, SBUX, AND OTHERSNext week is literally hopping with potential earnings announcement plays.

I've tried to pick out the ones that (1) have > 70% implied volatility rank; (2) offer greater than a 1.00 credit ($100) for the "classic" one standard deviation short strangle setup; (3) have fairly good liquidity with options prices; and (4) offer weeklies, but there are also a few >.50/<1.00 credit plays that I might nevertheless play (e.g., CREE, SBUX), although I think I can afford to be picky here given the selection ... .

PLAYS TO PUT ON TUESDAY

CREE -- Tuesday, after market close. High implied vol rank/high implied vol, but <1.00 credit for a 1 standard deviation short strangle.

IBM -- Tuesday, after market close.

NFLX -- Tuesday, after market close.

GS -- Wednesday, before market open.

PLAYS TO PUT ON WEDNESDAY

SBUX -- Wednesday, after market close. High implied vol/but implied vol <50% and <1.00 credit.

PLAYS TO PUT ON THURSDAY

SLB -- Thursday, after market close. I don't think I've every played this underlying. It's a tech company that provides support to oil and gas, and I've got plenty of petro plays on.

Notes: There are also a couple of earnings plays that might be interesting to play via other methods. One of these that comes to mind is KMI. It's got a high implied volatility rank, high implied volatility, and liquidity. The problem is that the price of the underlying is currently $13.00, so you just can't get enough premium out of it via short strangle or iron condor to bother with it using one of those strategies ... .

LEG into an IRON CONDOR on IBM Moving sideways, i have an JAN 16 order for a bear call spread 141/142

Everything looks to confirm sideways movements especially the bearish engulfing candle on 12/30

FB IRON CONDOR 2nd legI have placed order for .10 limit of this bear spread on FB.

Five trading days left, high probability, Everything confirms neutral.

IBM IRON CONDOR (UPDATE ON BROKEN EARNINGS SETUP)This is becoming somewhat of an epic, post-earnings work-off setup.

Without boring you with all the details (which are outlined in the post below), my post-earnings setup, after rolling and such is currently a Dec 7 140/143/140/143 iron condor. The 140/143 is the put wing and, yes, the 140/143 is the call wing (so it's basically inverted, with the call wing below the put wing; in short, it's an f'd-up setup).

In any event, the 143 long call of that setup is nearly worthless, has done its job, so I'm going to take it off here for a .05 credit. The short call I will take off for as much I can get for it.

Thereafter, I will have to roll the put side, most likely no later than Tuesday of next week, since I don't see IBM pounding above 143 (my short put strike) in short order. What I'm going to do is look to roll it out 45 DTE, but I'm going to first see what I can get for a 1 SD short call vertical at that expiry (it will be some kind of credit). Once I know what that credit is, I will look to see how much I can improve the short put side in terms of its strikes, because I don't want to pay more to roll/improve the short put side that I can receive in credit for the short call side.

The unfortunate thing is that a 45 DTE will most likely be beyond IBM's next earnings announcement, so I will have to watch to see if I can take advantage of price movement/volatility around that event in order to improve the put strikes further ... .

EARNINGS PLAYS THIS COMING WEEK -- FDX, ORCLOnly two earnings plays stick out to me this coming week -- FDX and ORCL, both of which announce earnings on 12/16 (Wednesday) after market close, so look to put on setups before NY close on Wednesday.

Currently, FDX's 52 week IVR is at 54 (IV 34), which isn't stellar, but it's at 92 for the past six months. Moreover, there is pretty good credit to be had whether you go short strangle or iron condor, so I imagine I'll play that one way or another if the IV sticks in there.

ORCL (IVR 75/IV 35) isn't looking all that hot, frankly, because I can't get 1.00 in credit with either a short strangle or iron condor (a Dec 24 34.5/39.5 short strangle will only get you a .61 credit at the mid price right now, which isn't anything to go crazy over; a same expiry iron condor just isn't worth it). Nevertheless, we could see a greater volatility pop toward earnings that makes it a little bit more worthwhile such that I'll play just because there isn't that much else worthwhile to do ... .

(Of course, there is that all FOMC thing next week, too).

ROLLING TESTED IRON CONDORS -- SOME TIPS (PART I)If you've got a few index ETF (SPY, IWM, DIA, or QQQ) iron condor trades on like I do, well, sadly, it is likely that your short call sides have been breached by this recent up move.

So, what do you do?

1. Don't panic. These were defined risk trades when you put them on, and they remain defined risk, which means that your max loss is limited on the call side even if SPY keeps shooting to the moon.

2. Take off the untested side when it no longer provides any meaningful protection to the set up or roll it in the direction of the tested side. In this particular case (where the call side has been tested), look at your short put wing side. If it is now worth less than .20 ($20), consider locking in profit here and covering it or rolling it up toward the tested side, keeping the expiry the same, assuming there is sufficient time for the rolled up spread to work, and you can get sufficient credit to make it worthwhile. I generally will roll in the same expiry if the untested side is worth <.20 and there are 25 days or more until the expiration of the tested side. If you are at or near expiry (3-5 DTE), consider saving yourself some cash in commissions and fees and letting the untested side expire worthless.

3. Near expiry of the tested side (3-5 DTE), attempt to roll the tested side for duration and credit. If you can get a credit that is at least the cost of the roll and you can improve your strike prices, fantastic. Proceed to do that and sell an oppositional wing set up at or near the 1 SD. I generally like to go another 45 DTE or so with a roll or as close as possible to that to allow the trade additional time to work out.

4. If you cannot roll for duration and credit, it isn't ideal, but all is not lost. You can do one of several things: (1) close it out and take the loss; or (2) attempt to work the tested side back to scratch or profit. I generally choose the latter.

I have done quite a bit of reading and video watching regarding traders' various approaches to breached iron condor setups where you cannot roll the tested side for duration and credit (i.e., generally where the tested side is not "on the dance floor"). The best idea I have found comes courtesy of TastyTrade, which advises you to roll out the tested side for duration without changing the strikes and then proceeding to sell the oppositional side against the tested side such that the end result is an iron butterfly or "iron fly." I will post an example of that separately.

WITH VIX/VXX CREEPING UP, PASSING ON AMZN/GOOG PLAYSAs anybody who has read my posts probably knows, I am not a big fan of earnings plays. As I have pointed out, they either go great (instant gratification) or terribly (several cycles of rolls to mitigate loss that tie up buying power). Me, I'm a bread-and-butter guy with a penchant for mechanical index ETF and TLT trades that supply a fairly constant level of theta (and so theta decay). They're awfully boring, but I don't require exciting to be successful.

Consequently, I'm going to go with "boring" and passing on AMZN and GOOG earnings. Both of these juicy monsters could easily move the markets (depending on the outcome of earnings), and I simply want to keep my powder dry in the event of a volatility pop in the broader indices so that I can devote the buying power to putting on an index ETF play or two instead without risking the tie-up of buying power that an earnings play could entail.

That being said, if you're going to play these, look to put on an earnings play some time tomorrow during the NY session. Due to the price of the underlying, the only way I would probably play these is via iron condor, so look to put on the short strikes of the setups at or near the 1 SD line, with your long strikes 2-3 strikes out from the shorts and take them off at 50% max profit.

Naturally, both of these remain troublingly near their 52-week highs, so you might think about skewing the setups slightly bearish or making the setups "chicken wide" (wider than the 1 SD line) to avoid potential explosions/implosions that are far greater than the expected move. Good luck!

YUM 10/6 EARNINGS PLAYYUM announces earnings on 10/6 after market close, so if you're going to play this via an options setup, look at getting a fill for whatever you put on prior to the 10/6 New York close.

Ordinarily, I trade these using a short strangle or iron condor, with the short call/put legs at or around the 1 standard deviation line for the chosen expiry, which will either be the Friday immediately after the earnings announcement or the Friday thereafter if the earnings announcement is too late in the week to manage the trade post-announcement if necessary.

SHORT STRANGLE:

A short strangle is an undefined risk strategy that consists of selling a put and a call with the assumption that price will remain between the strikes of the put and call for the duration of the contract.

Oct 16th Expiry 74.5 Short Put/89 Short Call Short Strangle

74% Probability of Profit

Maximum Profit: $121/contract

Buying Power Effect: Undefined

Break-Evens: 73.29/90.21

IRON CONDOR:

An iron condor is a defined risk strategy that consists of a long put, a short put, a short call, and long call with the assumption that price will remain between the strikes of the short put and short call for the duration of the contract.

Oct 16th Expiry 72 Long Put/74.5 Short Put/89 Short Call/91.5 Long Call Iron Condor

70% Probability of Profit

Maximum Profit: $57/contract

Buying Power Effect: $193/contract

Break-Evens: 73.93/89.57

Look to take both of these trades off at 50% max profit ... . Should price breach one side or the other of your setup, look to roll that side out to a later option expiry for credit and, if possible, for an improvement of your strike prices.

EARNINGS PLAYS I WILL BITE ON -- NFLX, GOOG & GS I have a love-hate relationship with earnings plays. When they work out, I'm happier than a clam; when they don't, I swear off them, use expletives to describe them, and say that they're a total *?! waste of time.

That being said, there are some I just can't pass up, usually because the premium is just too good. In the next couple of weeks, these will be NFLX, GOOG, and GS, so I am keeping a little bit of powder dry to do those.

Tips:

1. Look to put on a short strangle or iron condor prior to the close of the New York session before which the earnings announcement will occur. As a general rule, I play these nondirectionally, assuming no directional bias for the underlying and generally set up the sides at or around the 1 standard deviation line for both the call and put side.

2. Use expiries that are either the weekly options expiry immediately after the announcement or, if that provides too short a time frame in which to potentially manage the trade post-announcement, the Friday expiration thereafter. I generally prefer the weekly expiries for these setups, since they sometimes give you strikes in .50 increments, which allow you a little more precision with your strikes.

3. For both the short strangle and iron condor setups, I look to take the entire setup off at 50% max profit as volatility contracts post-announcement.

4. In the event of a test of a side of the setup, look to roll that tested side out to a later expiry for at least a credit equal to the cost of putting the trade on (fees/commissions) two to three days prior to expiry and close out the untested side or allow it to expire worthless.

Additionally, attempt to improve the strike prices for the rolled out side if possible.

Lastly, after rolling out the tested side, match it with an oppositional trade in the same expiration as the rolled out side (for example, if the put side is tested, roll it out to a later duration and set up a call side for that same expiry, ordinarily at or around the 1 standard deviation line for that expiry). My general rule is to roll out to the expiry that is of the shortest days until expiration that provides me with an opportunity to both roll for no additional cost in fees and commissions and that allows me to improve my strike price. If a particular expiry doesn't afford you that opportunity, try a later expiry for the roll.

I'll post examples of setups in these and any other "too good to pass up" high volatility, premium selling earnings plays as we get closer to the announcements .... .