GBP/USD ShortFundamental Analysis:- The USD is still the stronger of the two currencies with the FED looking at continuing their gradual rate raises over the near term. Even raising rates a little more than expected to stop Inflation jumping over their target. On the GBP side of the currency pair; Teressa May comes under pressure to resign as 40 of her MP's announce a vote of no confidence. This will add pressure to the outcome of Brexit and weigh further on the GBP. These two fundamentals make the GBP weak and the USD strong giving this currency pair downward pressure.

Technical Analysis:- You can see from the 4 hour chart that the price closed on a previous support and resistance zone and their was a significant push down after the pull back to 13100. Each high spike since the end of September has been lower than the previous showing downward pressure. The current price looks good for entry although after the vote of no confidence over the weekend the market might open lower. A stop loss above the high spike of 13100 is a good spot and looking for a return to 12900 in the first instance will give a reward of 3:1

enter 13060

stop loss 13110

take profit 12900

Longusd

USDJPY LONGThis is a long trade which we are going to trade on the other hand there is a ascending channel the the USD/JPY just broke on the chart giving signals or selling but with this we will stick with long

Technically, however, the Yen appears to have something of an advantage now. USD/JPY has slipped quite dramatically below the strong, newish uptrend channel that had previously bounded trade since September 7.

Bond Buying Rotation EURUSD ShortGreat technical and fundamental tailwinds for this trade.

The top indicator is a BB% with the 30MA as its source

The bottom indicator is Labu Bear's 'Wave Trend" indicator

Usd/Nok we have a Bottom.I think the pair found the medium term bottom and we are heading up for a nice ride. We have a perfect double bottom. Expecting a retest and buy buy buy.

EURUSD Play-By-Play for SHORTSHere is my step by step analysis for the EURUSD short I am calling. I have published my short reasoning on another chart which I have linked below.

I predict a daily chart EURUSD retrace

Here is the EXACT snipe entry to enter possible shorts. We shall see how this bold prediction plays out.

USD CAD looking to continue pattern and go longlong term item of USD CAD to go long and continue on the pattern

keep an eye out as ikt could also break the channel which will result in a nice short

good luck

XAUUSD 2618 trade setupsl 1227

short limit order 1206.5

t1 1184

t2 1166

2618 trade setup - short (double top, .618 retracement to enter short trade)

US Dollar index (DXY) could possibly find support around 99 to 100.5 for another bullish wave

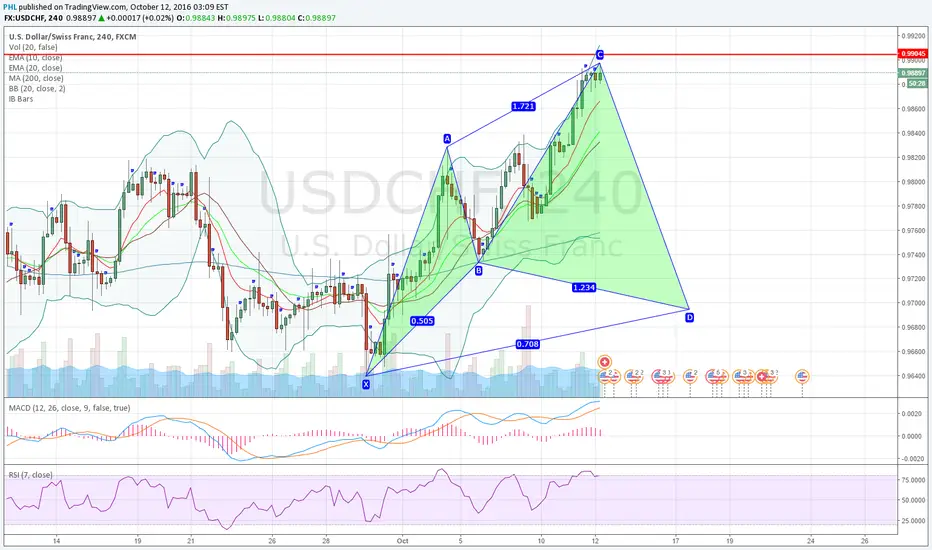

USDCHF potential bullish cypher pattern forming on 4H chartbuy @ 0.96949

it might be a bit early to look at this since C is still forming at the moment but markets can turn upside-down in a matter of seconds so better be prepared!

USDCHF potential bullish bat pattern on hourly chartlong @ 0.96531

We have seen repeated rejection of the 0.9650ish area on the higher 4H timeframe which supports the expectation that we bounce off again after completion of this bat.

USD STIR RALLY PUTS USD BACK ON BID: FED ROSENGREN SPEECHFed Funds Rallied up from 18% to 33% on the day with Fed rosengrens hawkish comments the only likely impetus.

Imo DXY here at 95 mid has an easy 50bps of topside left in it if rates can hold here at 33%, UST also seen higher across the board with the bench mark 10y yield breaking pre-brexit levels.

Long DXY, and shorting $yen on rallies is the way I intend on playing this, yen from a risk-off perspective imo is still cheap whilst USD been heavily offer for the past week.. rates need to hold up though so this is tactical positioning rather than a structural 21st Sept Fed bet. SPX likely to remain underpressure too whilst rates trade here so short positioning is paying off though i still like SPX lower to 2000s and will be holding for this.

Fed Rosengren Speech Highlights:

Fed's Rosengren: Gradual Interest Rate Increases 'Appropriate'

Rosengren: U.S. Economy Resilient Despite Drag From Overseas

Rosengren: Could Reach or Exceed Full Employment 'Over the Course of the Next Year'

Rosengren: 'Reasonable Case' for Gradual Interest Rate Increases

Rosengren: Weakness in Recent GDP Readings Reflects Inventory Adjustments

Rosengren: Expects Growth to Exceed 2% Next Two Quarters

Rosengren: 80,000 to 100,000 Jobs a Month Needed to Keep Unemployment Rate Constant

Rosengren: Stock Prices, Volatility Gauge Show U.S. Resilience

Rosengren: Commercial Real Estate Prices Have Risen Rapidly

Rosengren: Risks to Forecast 'Increasingly Two-Sided'

Rosengren: Waiting Too Long to Raise Rates Could Lead to 'More Pronounced' Slowdown in Growth

BUY USD DIPS VS GBP/ NZD: DOVISH FED W. DUDLEY SPEECH HIGHLIGHTSFed Dudley was speaking At A joint New York Fed, Indonesian Central Bank Seminar On Sunday evening when he left a mixed impression for the markets to digest - saying "it is premature to rule out an interest-rate increase this year" but then on the contrary saying "Raising Rates Prematurely Would Be Riskier Than Moving Slightly Too Late" and following up that sentiment with "Investor Expectations For Flatter Path Of U.S. Interest Rates Seems 'Broadly Appropriate'" and pointing out the medium-term risks are seen skewed to the downside - all of which somewhat contradictory expecting a 2016 rate hike.

IMO these comments are more less positive news for the greenback, given the hawkish July Minutes should take precedent (despite the market weirdly selling the september hike being officially put on the table) and after the DXY lost every day last week I think it will struggle to continue this trend into this week as the drop in rate hike expectations/ fed funds rates should flatten out - Likely seeing the bulk of the dovish expectations price last week - september 25bps hike expectations fell from 25% at the beginning of the week to 12% on Friday following the miss GDP report - will likely bottom out around here to 8%min.

That said, given the BOJ's miss we could easily see further pressure on US rates this week as imo the failed big stimulus hopes are likely to fade the risk-on environment of late, and move us back into the safe haven trend that has dominated 2016 - so dont be surprised to see some more risk-off rate expectation USD selling/ bond buying - look out for consecutive moves higher in UST or moves lower in tnx.

In the medium term this still hasnt changed my view of bullish USD and at present IMO this selling wave has opened up the opp for some good USD buying entry points e.g. kiwi above 0.72, stelring at 1.33, and eur at 1.115 - kiwi and sterling the best trades as we move into RBA, BOE and RBNZ within the next 10 days which should realise considerable downside for kiwi and cable (and for those trading aussie too, tho i prefer the kiwi proxy).

Fed Dudley Speech Highlights:

-Fed's Dudley Warns It Is Premature To Rule Out an Interest-Rate Increase This Year

-Dudley Says Fed-Funds Futures Prices Seem 'Too Complacent'

-Dudley Says There Is 'Room For Improvement' in Fed Communications, But They Are Growing More Transparent

-Dudley Says His Baseline Outlook For U.S. Growth, Inflation 'Has Not Changed Much In Recent Months'

-Dudley Expects 2% Annualized U.S. Growth Over Next 18 Months

-Fed's Dudley Says Medium-Term Risks To Economy Are 'Somewhat Skewed To The Down Side'

-Dudley Says Brexit Impact Has Been Short Lived, But Longer Term Potential Fallout 'Hard To Gauge'

-Dudley Says Fed Takes Dollar Appreciation Into Consideration, But Not Targeting Any Set Exchange Value

-Dudley Says Evidence Accumulating The Crisis-Era Headwinds 'Are Likely To Prove More Persistent'

-Fed's Dudley Warns it is Premature to Rule out an Interest-Rate Increase This Year

-Dudley: Investor Expectations For Flatter Path Of U.S. Interest Rates Seems 'Broadly Appropriate'

-Dudley Says Raising Rates Prematurely Would Be Riskier Than Moving Slightly Too Late

LONG DXY / USD: HAWKISH FOMC RATE STATEMENT - SEPTEMBER HIKE?The FOMC rate statement was largely in line with expectations and to the hawkish side - with a september hike hinted at. Much of which followed the rhetoric of FOMC members in the past few weeks (see previous posts) and data (disregarding the poor -4% durable goods mom print). Perhaps the most hawkish/ promising statement made for a Sept rate hike was the fact Fed George Preferred to Raise Rates to Range Between 0.50% and 0.75% - hinting hikes are now being considered. And "Fed Could Raise Rates Later This Year, Possibly As Early As September". Though on balance the Fed did repeat the dovish phrases "low/soft" several times when regarding various measures of inflation and business investment.

This FOMC Statement holds in line with my medium run long $ view (hike based) - especially against Yen, GBP, EUR, AUD and NZD who are expected to ease and thus policy diverge.

In terms of market pricing, the Fed Funds Future Option implied probabilities of a rate cut have continued their steepening this week - following the 3wk trend with Sept/Nov now pricing a 25.9/ 26.8% probability of a hike (up from 9% 2wks ago) - Dec now has a probability of 41.8% and is showing some stability here, with a 50bps hike implied at 9.9% and rising steadily. From this the implied probability of one rate hike in 2016 is at nearly 70% (Nov+Dec) - which imo is in line, or slightly below my qualitative probability of 90%. With the probability of 2 hikes at 12.5% which is about what i would expect.

Nonetheless eyes are now focused on BOJ - which is expected to be a year changing meeting.

September FOMC Rate Decision Statement - 0.50% unchanged:

--Fed Leaves Policy Rate Unchanged, Says Near Term Economic Risks Have Diminished

-Fed Offers More Upbeat Assessment of Labor, Economic Conditions

-Fed Could Raise Rates Later This Year, Possibly As Early As September

-Federal Reserve Keeps Fed Funds Range Unchanged at 0.25% to 0.50%

-FOMC: Voted 9-1 For Fed Funds Rate Action

-Fed Leaves Discount Rate Unchanged at 1.00%

-Fed: Economic Activity Expanding At A 'Moderate' Rate

-Fed: Labor Market Strengthened, Job Gains 'Strong' in June

-Fed: Payrolls, Other Indicators Point to 'Some Increase' in Labor Utilization in Recent Months

-Fed: Market-Based Inflation Compensation Measures 'Remain Low'

-Fed: Survey-Based Inflation Expectations Measures 'Little Changed'

-Fed: Inflation Expected to Remain Low in Near Term

-Fed: Inflation Expected to Rise to 2% Over Medium Term As Transitory Effects Fade

-Fed: Household Spending Has Been 'Growing Strongly'

-Fed: Business Fixed Investment Has Been 'Soft'

-Fed Continues to Expect 'Only Gradual Increases' In Fed Funds Rate

-Kansas City Fed's George Dissents On Fed Policy Action

-George Preferred to Raise Rates to Range Between 0.50% and 0.75%

SHORT AUDUSD: EYEING CPI PRINT - SELL 1.0%YOY, 0.3%Q; RBA EASINGAM 2:30GMT Ausssie Inflation prints are released these are key for determining their August Policy Decision

1. IMO a 1.0%yoy CPI print shows a further 0.3% contraction in their yearly CPI, this should be sufficient to push the RBA to cutting their OCR by 25bps, similarly a 0.3%qoq CPI will be needed in conjunction to show that inflation is growing at a slow pace.

2. RBA Minutes that support this view of low CPI leading to a cut from July said -

- On the margin RBA remained in line with previous meetings, adding little but still keeping it on the dovish side imo. Once again, as in previous minutes (and from several other central banks) RBA continued to communicate the necessity of "watching key data" to drive future policy decisions. Interestingly though, they also mentioned the negative impact of a strong AUD which in turn supports RBA doves out there as a cut is the remedy to stop a deflationairy currency in its tracks. Further, RBA notably were under no illusions regarding their inflation situation stating " inflation set to stay low for some time" - another encouraging stimulus for doves given inflation's important position/ weight for setting future policy.

- As per the attached post, i remain dovish/ bearsh on aussie$, and i continue to expect a cut to 1.50% (25bps) this year given i expect their inflation to remain stagnant. Clear targets are 0.73 when probability of a cut is higher - though i would enter shorts regardless if AUD$ could find its way to its 12m highs at 0.78, though unlikely.

- I like USD strength in the medium term too hence supporting the short Aussie dollar view

RBA Minutes Highlights:

RBA MINUTES: BOARD TO WATCH KEY DATA, WILL MAKE ADJUSTMENT TO RATES IF NEEDED; REVIEW OF FORECASTS IN AUG WILL HELP STEER POLICY

- Inflation set to stay low for some time, employment mixed, retail sales look set to pick up

- Stronger AUD would complicate economic rebalancing

- Economic transition is now well advanced

USDJPY: BOJ - FINAL THOUGHTS; FUNDAMENTAL/ TECHNICAL ANALYSISAt market price:

1. At 104 $yen offers an attractive buy and sell side - from the position of not knowing what the BOJ will do..

- I dont think that this pull-back to 104 is a material shift in risk-sentiment, rather i think this is a technical sell-off where the 107 pivot was hit (as highlighted) at which point BOJ/ UJ bulls lost confidence on their long positions which in turn caused a cascade of $Yen selling on profit taking - right into the 104 pivot. Also as you can see the price traded to 50% retracement of the risk-rally price (currently at 40%) after 4days - i dont consider this a fundamental risk-shift, such a shift would cause much more aggressive selling in fewer days e.g. 50% in 1-2 days, rather than 4 - this just looks like a technical pull-back and i wouldnt be surprised to see use move into the 105mids again. However, A break below 104 and I would agree that this is a BOJ market expectations move/ shift in risk sentiment to risk-off.

2. Most of you will know that I have been a $yen bull for some time citing policy divergence and future policy divergence as the reasoning.

- So this in mind, going into BOJ/ Fiscal stimulus, where policy divergence is likely to increase, how does this affect my bullish $yen view?

Bullish $Yen arguments:

1. The base case remains approximately 10bps to the depo rate, 10bps to the LSP, yen10trn to JGB and some 50-100% increase to the annual ETF from 3.3trn + the median expectation of stimulus is Yen15trn.

- So from a bulls perspective i wonder, how much of this move is already priced in, given the 5-6% move from 100/101 certainly wasn't for free - I think at the 106/7 level pretty much all of the base view is priced e.g. 10bps depo, 10bps LSP, yen10trn JGB increase and yen10-15trn of fiscal stimulus..

- Thus to make a position worth while imo the BOJ/ Fiscal Stimulus is going to have to outperform the median expectation. Imo in order to see 111 and for $yen to trade at such levels as an average for the next 3-6, we would have to see the base case almost doubled; e.g. 20bps to the depo, 20bps to the LSP, yen20trn JGB and perhaps yen20-30trn fiscal stimulus (which has been mentioned).

The case for BOJ beating expectations:

- I think the market is somewhat underestimating the BOJ/ Govt at only 6bps given the BOJ is seeing an already -0.4% deflationary environment (-0.5% in Tokyo) when - 1) Yen is up 20-30% in 2016 vs most ccys - which is even more deflationary, they need a big package to reduce this; 2) 9 consecutive months of exports falling aggressively - deflationary and a function of strengthening Yen - needs to be combated by aggressive easing policy to devalue the yen for sustained period; 3) No policy change since January - so they have had 6 months of policy transmission, where the situation has worsened, to see now something drastic is needed; 4) Brexit/ Fed hike/ US Election/ China/ other risk-off factors likely to drive yen further up in the future - thus preemptive action needs to be taken now; 5) Great Pressure from JPY Govt/ public given -0.4%CPI is the rate they had back in 2014 when they started the massive QEE programme - basically hasnt changed in 2yrs - BOJ underpressure for results; 6) BOJ knows markets are ready to sell any "average" easing - so they know they need to be aggressive to beat/ get infront of the marker; 7) BOJ knows its perhaps the last and best time to reclaim any market trust/ confidence - anything less than extraordinary and market will continue selling any future BOJ policy as they are already inclined to do - Since BOJ/ Kuroda confidence is low as they have failed to deliver on several previous big occasions e.g. April.

- If the above materialises I advise buying $Yen at market price, with a 109-111TP.

DXY/ USD: FOMC - GS 65% 2016 RATE HIKE; RABO ONE 2016 RATE HIKEGoldman Sachs on July FOMC Decision :

- The run of positive economic news in recent weeks has coincided with generally dovish comments from Fed offcials. Policymakers have indicated that they are not âbehind the curveâ, and have expressed increased uncertainty about the neutral level of interest rates. We would treat recent comments with caution, however, as we have not heard formal remarks from the Fed''s leadership.

- Taken together, we see recent economic data and the public comments from Fed ofï¬cials as consistent with only modest changes to the FOMC statement. We think the committee will upgrade its discussion of the labour market and measures of inï¬ation expectations, but change little else. The period between the July and September meetings will include a number of important data releases as well as the annual Jackson Hole conference. Therefore, policymakers will have an incentive to keep their options open, and plenty of opportunities to guide market expectations, should they need to.

- We continue to see a 25% chance that the committee will raise the funds rate in September and a 40% chance that it will do so in December - implying a roughly two thirds probability of at least one rate increase this year.

RaboBank on July FOMC Decision:

-While the Fed is in a wait-and-see mode to assess the threats to the global outlook and the strength of domestic momentum, recent US data have boosted the Fed;s confidence. We expect the Fed to squeeze in one rate hike before the end of the year, most likely in December.

NZDUSD: TECHNICAL ANALYSIS - 0.70 RES, MA, STDEV, IV=HV & RR NZD$ Technical analysis - Remain bearish below 0.70 - 0.69tp1 0.68tp2 on a rate cut (Aug 10th):

Key level close:

1. On the daily and weekly we closed at the strongest pivot point of recent times at 0.70 - this is very bearish as historically this is the strongest level (lower than post brexit).

MA:

1. We trade below the 4wk and 3m MA - this is a bearish indication + we are finding some support at the 3m moving average where price currently sits, though NZD$ looks to try and push lower with daily candles skewing their spikes to the downside. We have been above the 6m MA since June which sits at 0.69 and likely offers our next bearish support once we break the 3m MA.

IV/ HV:

1. Realised Vols have also unsurprisingly aggressively come off in recent days, likely a function of the RBNZ rhetoric fading. Plus Implied vols are seen steeper in the 1wk and flatter in the 2wk-1m - with 1wk, 2wk and 1m Implied vols trade at 13.12%, 12.66%, 13.09% vs HV 1wk 2wk 1m at 10.90%, 15.60%, 14.58% - this mixture between HV and IV shows there has been considerable volatility drivers in the past/ future which are causing the curves to converge and diverge in no particular direction e.g. brexit, RBNZ hawkish/ dovish comments, future rate expectations - which all distort the interaction between HV and IV.

Deviation Channels/ Support levels:

1. We Trade near to the bottom of the 6m deviation channel at 0.69 as NZD economic assessment asserts downside pressure on the pair, nonetheless but we could see support here as 0.69 is also a price action support level. Looking at the 12m SD channel, we are trading just below the average price at 0.703 - hence there is definitely more room for downside and we have just crossed the middle regression line implying we are entering some downside deviation now, with the 12m -2SD resistance level at 0.675 which is in line with the price support level at 0.68 which is where i think we will head after the RBNZ announces a 25bps cut..

Risk-Reversals

1. 25 delta Risk reversals trade marginally bearish for NZD$, with current at -0.2, 1wks at -0.3 and 2wks at -0.6 and 1m at -0.95 - this suggest the NZD$ has a slight downside bias which concurs with the RBNZ's dovish stance and committment to cutting rates that was made clear in the July economic assesment (see attached).

- 3m risk reversals trade with a similar downside bias to the 1m at -1 which shows the market expects extended NZD$ downside, likely a function of further rate cut expectations from the RBNZ.

*Check the attached posts for indepth fundamentals*

GBPUSD SHORT: BOE/ FOMC POLICY EXPECTATIONS INCREASINGLY BEARISHFollowing today's Service/ Manufacturing PMI miss (worst contraction in 88 months - since 2009) the Sterling market has come under significant pressure as BOE rate cut expectations increase with OIS rates markets pricing a 94% chance of a 4th Aug cut vs 85% before the PMI's were released.

Further, the PMI misses has attracted attention from UK Politicians e.g. Chancellor Hammond - which puts further qualitative pressure on the BOE to cut, rather than just quantitative data prints - Political pressure combined with data pressure is the best us GBP sellers can ask for when looking for a BOE rate cut.

I have to say this is a breath of fresh air for GBPUSD shorts that i am holding (cable trades down to 1.30xx) - given that the start of the week was the complete opposite, with strong CPI/ Employment and Hawkish comments from MPC members Weale and Forbes; all of which reducing the pressure on the BOE to cut and thus the sterling market.

Below also, following the PMIs we see Aug 4th BOE expectations from BoAML/ JPM - which call for a 25bps cut and 50bn addition to QE (with increased near-term pressure to do so/ act post-PMI) - in which imo will send GBP$ to 1.25, if not through - these expectations are encouraging for shorts thougb it should be remembered the cut was expected in July also but didnt materialise (though the minutes from the meeting did state "most members expect to ease in August". Further we see fresh recession concerns emerge as from Barclays below - once again putting downside pressure on GBP through poor GDP and increased BOE cut likihoods.

Further, on the USD side of the trade, in this risk recovery we continue to view FOMC rate hike expectations rising - aiding dollar topside (and gbp$ downside) - as Fed Funds Futures Opt Implied probs now trade at 19.5% for Sept, 20.8% Nov and 40% for Dec, up from yesterday at 18.8, 20 an 39.8 - the risk-on bias already started today will likely see these probabilities continue to strengthen through the end of the day.

Trading Strategy:

1. So from here after holding shorts at 1.3400 average, given this fresh and extreme impetus for downside - I will continue to hold my cable lower to the 1.285 target (unload 50%) and save 25-50% (depending if i unload 25% at the 1.305 level) for the Aug meeting itself where 1.25 is likely - where before today holding cable seemed more risky as the risks looked skewed to a hawkish BOE, which now has flipped. Unlikely, but any rallies to 1.33-35 level i will be reshorting - cable downside is a function of time imo.

- I like holding short because BOJ are likely to ease, whilst the FOMC stay neutral/ Hawkish, this in turn puts more pressure on the BOE to ease/ GBP - in order to prevent GBP appreciating vs JPY (disinflationairy) BOE must ease too & hawkish FED stance puts pressure on GBPUSD lower.

- Risks to the view continue to be if 1) New/ Weale/ Forbes continue to reiterate their hawkish/ no easing stance and perhaps less impactful; 2) Next weeks UK GDP reading - will not contain much Post brexit data so any upside is unlikely to give GBP strength, though downside is welcomed and could cause further selling (Low pre-Brexit GDP gives BOE more reason to cut)

GBP OIS PRICING A 94% CHANCE OF A 25BPS CUT FROM THE BOE IN AUGUST (85% PRE PMI)

- UK CHANCELLOR HAMMOND: Must restore uncertainty after July PMI

- UK CHANCELLOR HAMMOND: BOE will use monetary policy tools at its disposal

- UK CHANCELLOR HAMMOND: BOE have tools to respond to market turbulence in the short-term

BoAML ON BOE:

- We look for the BoE to cut rates 25bp and increase QE by £50bn in August, split between Gilts and private sector assets.

- BoE inaction so far and heightened policy uncertainty leaves risk-reward unattractive in the front end in our view.

- We prefer to position for potential BoE Gilt purchases, reiterating our 5s20s Gilt flattener as attractive in a QE-scenario.

JP MORGAN ON BOE:

- Current market pricing of a 25bps rate

SHORT NZDUSD: GOLDMAN SACHS FORECASTS 0.68, 0.64, 0.62 GOLDMAN SACHS EXPECT 3 RBNZ RATE CUTS OF 25BP APIECE IN AUG, NOV AND MAR.

In a scheduled "Economic Update" published on Thursday, the RBNZ signalled a significant strengthening in its easing bias, and dovish shift across its views on domestic inflation and domestic/global growth. At the heart of many of these changes is renewed concern about the elevated NZD. In our view, these changes make clear that the RBNZ is positioning for a deeper easing cycle, notwithstanding ongoing risks to financial stability from rising house prices.

NZDUSD Targets:

- 3 Month: 0.68

- 6 Month: 0.64

- 12 Month 0.62

This is largely inline with my previous posts/ reaffirms my short view of NZD$ - especially with the possibility of 50bps of cuts increasing for this year (GS citing two cuts); Plus I also see increased USD strength over the medium term as rate hike expectations/ implied probabilities ever grow - Fed Funds Futures Opt Implied probs now trade at 19.5% for Sept, 20.8% Nove and 40% for Dec, up from yesterday at 18.8, 20 an 39.8 - the firsk-on bias already started today will likely see these probabilities continue to strengthen until the end of the day.

The Probability of 2 hikes this year is also becoming an ever stronger possibility with 2 hikes pricing at 7.5% in Dec - and with July Pricing a hike for the first time since Brexit at 2.4%

GBPUSD SHORT: DOVISH BOE M. CARNEY SPEECH HIGHLIGHTS - AUG CUTIMO Mark Carney was very dovish on the margin, certainly reinforcing their/ my view of an August cut being 90% on the table. The most supportive statements were "MonPol Important In Cushioning Effects Of Any Relapse In Recovery In Months & Quarters Ahead", "The MPC Does Not Have The ''Luxury '' and "More Should Be Done To Cushion The Effects Of Negative Shocks" - all of which infer that an August cut is very much on the cards - especially given that the BOE has been relatively neutral as yet, whilst they have increased the offering of interbank funding by a few £100bn, apart from that the BOE is yet to make any moves in conventional policy tools, which member/ market expects the BOE to do e.g. a Bank Rate cut and/or formal QE.

I personally am short GBP$ at these levels (see attached posts), and these comments from today have certainly reinforced my position given their dovishness, even more so when combined with yesterdays minutes which said "most MPC members expect to loosen policy in August" and "detailed analysis of all available policy tools is required" - both of which go hand as 1) they want to make sure they analyse the economy properly, which takes time (July too soon) yet all members expect August to be enough time to conclude/ act upon such analysis.

Not to mention, given bank forecast a median GBP$ price of somewhere near 1.225, being short in the 1.30+ imo is certainly probabilistically favourable, especially if you are able to execute close to the Post-brexit highs of 1.35 which has held as solid resistance and imo should do for the foreseeable future given we traded to lows of 1.38 before brexit so 1.35 is very expensive post brexit. Further, the median bank forecast was for a 25bps cut in the bank rate in July (with some calling for 40-50bps), so if that was the case in July, given BOE didnt deliver, this only increases the chances of a cut in August which imo will take GBP$ to 1.25xx.

USD demand increasing - Federal Funds Rate Implied PDF prices:

Also, on the USD side, demand is increasing which compounds the GBP$ short support, as the Fed Funds Rate implied hike probabilities are continuing to steepen. For example, since yesterday, the implied probability of a September/ November hike has increased from 12%/12% to 19.5%/20.8% - with, for the first time, a 50bps hike being priced at 0.4%/0.8% respectively; Decemeber's probability also steepened to its highest level post brexit to 40% from 33.7%, 50bps at 7.5% from 3.4% and 75bps for the first time at 0.3%.

This aggressive steepening in the rate/ probability curve is likely a function of the risk-on market we are in (SPX 4 new highs in a row), with 10y rates rallying TNX, averaging +4% every day this week. Further, I think the FOMC speakers comments which have 80% been hawkish this week has also increased confidence.

Gov Mark Carney Speech Highlights

- Monetary Policy Cannot Do Everything To Counter The Impact Of The Referendum

- MonPol Important In Cushioning Effects Of Any Relapse In Recovery In Months & Quarters Ahead

- BoE July Minutes, ''Broadly Consistent With My Personal View.''

- The MPC Does Not Have The ''Luxury ''

- Far Too Early To Draw Strong Conclusions On Precise Path Of The UK Economy

- UK Economy Is Unlikely To Crash, It Is Likely To Slow

- A Sharp Fall In Currency Rate Will Provide A Shot In The Arm To The UKâs Net Exports

- More Should Be Done To Cushion The Effects Of Negative Shocks

- Past Few Weeks Have Generated Considerable Uncertainty Around UK Economy, Policy & Politics

- Monetary Policy Should Stand Ready To Move In Either Direction

- Brexit Has Increased Materially The Degree Of Uncertainty

- Some Of This Uncertainty May Dissipate, But A Good Chunk Is Likely To Linger Over Next 2-Yrs

- Uncertainty To Weigh On Domestic Spending By Both Companies & Households For Foreseeable Future

- The Amount Of Slack In The UK Economy Is Likely To Steadily Rise