Macys

THE WEEK AHEAD: M EARNINGS, TWTR, X, EWZThe only volatility contraction earnings play I'm looking at for this coming week is in Macy's, which announces earnings on Wednesday before market open, since it has the implied volatility rank and 30-day metrics I'm looking for (76/56).

Here are some Macy's preliminary setups, with the short strangles set up around the 20 delta strikes:

August 17th 36/44 short strangle, 1.21 credit at the mid, break evens at 34.79/45.21.

September 21st 35/46 short strangle, 1.60 credit at the mid, 33.40/47.60 break evens. (The reason why I'd go with this one over the August is that there isn't much time to manage the August setup if it goes awry).

September 21st 40 short straddle, 5.42 credit at the mid, 34.58/45.42 break evens

Other underlyings with earnings in the rear view/exchange-traded funds:

TSLA (rank 61/30-day 66). I am unsure of whether I will touch this underlying any longer given private equity discussions. These can ruin an options trade if they go through, as well as ruin one if they don't. (See, RAD, like, more than once ... ).

TWTR. The rank isn't great, but there is still some background implied to mine there (41.7%). The Sept 21st 29/36 short strangle is paying 1.06, which isn't shabby for a 32 clam underlying.

X. With a 30-day at 41.4%, the September 21st 27/34's paying .87, the 30 short straddle, 3.06.

EWZ. I've been short straddling this high implied exchange-traded fund, but the 30/38's paying .82 in the Sept cycle if you just can't stand the kind of skewing out the short straddle enjoys every other day with this one ... .

Other Major Food Groups:

TLT: Waiting for 122.50-ish for another bearish assumption setup.

M - 08/12Waiting on Earnings (08/15), has been an awesome Dividend play if you picked it up lower down.

M daily short - weekly longM on daily appears to be overextended based on high RSI (70.5) however we recently have seen it as high as 79 - weekly actually paints a strong bullish picture so possibly light retracement or just accumulation - will post follow up weekly chart

I would be a tough buyer on Macys, but...I would be a very tough buyer on Macy's, but around 24.07, not before nor after.

Have a Good Trading Week,

Learn how to beat the market as Professional Trader with an ex-insider!

Cream Live Trading, Best Regards!

THE WEEK AHEAD: M, BBY, OIH, VIXEARNINGS ANNOUNCEMENT/VOL CONTRACTION PLAYS:

M announces earnings on 2/27 before market open. Preliminarily, the March 24/30 short strangle is paying .84 at the mid, which isn't very juicy. Given the size of the underlying, it may be more amenable to a short straddle or iron fly, with the March 9th 27 short straddle paying 2.95 and the 23/27/27/31 iron fly paying 2.13 with the longs camped out around the 16 delta strikes. I would shoot for 25% max profit or .74 in the case of the short straddle; .54 for the fly.

BBY announces on the 1st of March before market open. The March 9th 20-delta 66.5/81 short strangle is paying 2.05 at the mid, with the defined risk variant 63.5/66.5/81/84 iron condor paying just a smidge short of one-third the width of the wings -- .92/contract.

HIGH IMPLIED VOLATILITY EXCHANGE-TRADED FUNDS:

The exchange-traded funds screened for percentile greater than 70% and ranked by percentile are IYR (background 20%); XLI (background 20%); FXI (background 26%); EEM (background 22%); and XLU (background 18%). Ranked by background implied: GDXJ (33%; 33rd percentile); XOP (32%; 64th percentile); OIH (32%; 80th percentile); GDX (28%; 42nd percentile); and EWZ (28%; 19th percentile). Generally speaking, I like to pull the trigger on a premium selling trade when the percentile is greater than 70% and the background implied is greater than 35%, so I would pull the trigger on an OIH setup here, even though it's slightly short of that 35% background metric.

Here are a couple of possible plays:

Neutral Assumption/Undefined:

OIH April 20th 25 short straddle

Probability of Profit: 54%

Max Profit: $224/contract

Max Loss: Undefined

Break Evens: 22.76/27.24

Notes: Look to take profit at 25% max or .25 x 2.24 or .56/contract. Intratrade defenses: roll of untested side toward current price, delta hedging.

Neutral Assumption/Defined:

OIH April 20th 22/25/25/28 iron fly

Probability of Profit: 44%

Max Profit: $176/contract

Max Loss: $122/contract

Break Evens: 23.22/26.78

Notes: As with the short straddle, look to take profit at 25% max or .25 x 1.76 or .44/contract. Intratrade defenses: Delta hedging.

THE VIX

After this recent pop, I'm still watching the VIX and VIX futures term structure to return to its ordinary "contango look." While the structure has returned to contango if you look at the March, April, and May expiries, May is in backwardation relative to June, June in contango relative to July, July in backwardation relative to August, with the remainder of the structure in contango.

Trade Idea Of The Week MACYS INC (M)Forgot to post this yesterday, but we have been in this trade since Friday with some puts trying to ride this market during this large pullback. I am still going to post this because even with this bounce today I still think it has more room to fall.

Last week there was a huge turning point in momentum and the selling volume started to pick up. With the signs of the overall market weakening we decided to go bearish. We will ride this trade until the short term trend is broken on the 15minute/30minute candles.

Best of luck!

THE WEEK AHEAD: SEAS, CTL, SQ, M EARNINGS; TEVA (NON)SEAS announces earnings on 11/7 before market open, with an implied volatility of 71%, which is at the upper end of its range over the previous 52 week period. The November 17th 11 short straddle is paying 1.37 at the mid with a comparable iron fly probably not paying enough to make it worthwhile (less than 1/4 the width of the longs).

CTL (implied volatility of 62%; at the top of its 52 week range) announces on 11/8 after market close. The quasi-short straddle or tight short strangle 16/17 in the November 17th expiry pays 1.27 with break evens slightly wide of expected move. As with SEAS, the iron fly doesn't pay enough to be worthwhile ... .

SQ also announces on 11/8 after market close. With an implied volatility of 55, it's in the top quarter of its annual range. The November 17th 33/42 short strangle camped out at around the 20 delta strikes yields 1.03 in credit, implying that a defined risk play like an iron condor won't pay one-third the width of the wings, although it may be worth pricing it out closer to earnings.

M announces on 11/9 before market open (implied volatility 55, top quarter of range). The November 17th 18/19 tight short strangle/near short straddle pays 1.43 at the mid, with break evens wide of the expected. The November 17th 14/18/19/23 comparable defined risk iron condor/fly play pays 1.86, which is close to 1/4 of the width of the longs, so worth a check shortly before the announcement.

TEVA's earnings are in the rear view mirror, but its implied volatility remains elevated here at 65 -- at the upper end of its 52 week range. The December 15th 30 delta strike at 10 pays .30 as a potential short put/acquire/cover play with a cost basis of 9.70 in any acquired shares. For the patient and/or fearful of the possibility that this company's another VRX, going monied covered call out of the box with a share purchase here at 11.40 and a sale of the March 16th 10 call would cost 9.06 to put with a max profit of .94.

Time to think about Macy's

1) the aim of deep correction is completed

2) bullish divergence,

3) oversold by RSI

such kind of signal were at 2008-11-03.

Currently we can see the 1 growth wave is completed at 73.77$. I confident that it was the first wave because it was started from historical min price 5.07$

I think for starting to buy near 19.69$, since gap should be closed. Probably it can be the bottom and I do not expect significant going down of price. Actually I've started form a position near 20.78$ - about 20% of plan.

I will buy more when bearish signal will be worked out, I guess it should happened near 19.69$. Where I will buy additional 20% of plan.

If the double top (fig.3) will be realized the target of going down is 15$.

If you are do not tolerant to risky, additional buy could be done by 10% of plan after 7%-10% of going down the price. But this going down of price will be in negative scenario only. Also you can wait for confirmation for reversal of down trend.

Target price of 3th growth wave is above 73.61$. For achieving that price several years can be required. The growth of the first global wave is being during about 6.5 years.

THE WEEK AHEAD: DIS, M, NVDA, VIX, GLDWith VIX continuing to rattle around at sub-11 levels (it finished Friday's session at 10.03), the place to sell premium remains in earnings, although even there the pickings are slim, as broad market low volatility bleeds through the entire market.

The decently liquid underlyings on tap for earnings next week: DIS, M, and NVDA, with DIS announcing Tuesday after market close, M on Thursday before market open, and NVDA, Thursday after market close. From a pure metrics standpoint, only NVDA is offering the kind of metrics I look for in these plays (>70 implied volatility rank/>50% implied volatility). I'll price out setups, both undefined and defined, as earnings get closer, as price is likely to jostle around between now and then.

With respect to sector and/or broad index exchange traded funds (where I look for >70 implied volatility rank/>35% implied volatility) in which to sell premium, there are a paucity of high implied volatility rank/high implied volatility plays to be had (what's new?), with XOP coming in at the top of the list with a rank of 35 and a background of 31, QQQ -- at 31/15. My general test for those (aside from the rank/background implied volatility metrics) is seeing whether a 45 DTE 20-delta three-wide iron condor will pay one-third the width of the widest wing (i.e., 1.00). They won't here, so putting on one of those plays is likely to be less than productive, since the limited volatility in these instruments doesn't have much to contract to.

Flipping the implied volatility screen to look for extremely low volatility underlyings where low volatility strategies (diagonals and calendars) might bear more fruit yields a fairly abundant list of underlyings, with TLT coming in at 10.3, DIA at 11.10, GLD at 11.15, and SPY at 11.17. I'm in a TLT long-dated put diagonal, so may consider putting something on in the DIAmonds or GLD (e.g., a Sept 15th/Dec 15th 118 put calendar; 1.51 db at the mid; theta .57; delta -7.54; back month at 40 delta; front at same strike as back).

trade on Macys rebound.bought it on Friday morning when the market had a big dip. currently up 2.14%.

Expect M to bounce backi think M is oversold now, expect to bounce back, I am prepared to open a trade, stop loss around 22.00

Contrary To Some Analysts; Gains Ahead For Macy'sMacy's has been in a bearish downtrend since late 2015. Although the overall trend is down, the stock does cycle up and down throughout the trend. On May 19, the stock bounced off support and should slightly cycle up over the course of the next month and a half. This is the first indicator the stock should move up. With mixed earnings from retail out of the way for now, the following points will highlight why the stock should move upward.

When we take a look at other technical indicators, the relative strength index (RSI) is at 27.2540. RSI tends to determine trends, overbought and oversold levels as well as likelihood of price swings. I personally use anything above 75 as overbought and anything under 25 as oversold. Currently the RSI is overbought and due to drop. This indicator has recently exited oversold territory. The stock is due to slowly move, or move up over the next few weeks. This is the second indicator of potential upward movement.

The true strength index (TSI) is currently -35.5789. The TSI determines overbought/oversold levels and/or current trend. I solely use this as an indicator of trend as overbought and oversold levels vary. The TSI is double smoothed in its calculation and is a great indicator of upward and downward movement. The current movement has the stock moving down.

The positive vortex indicator (VI) is at 0.7106 and the negative is at 1.2909. When the positive level is higher than 1 and higher than the negative indicator, the overall price action is moving upward. When the negative level is higher than 1 and higher than the positive indicator, the overall price action is moving downward. Currently both indicators are at extreme levels which typically lead to a reversal of the stock. The positive indicator should begin to move upward while the negative indicator heads down. This is the third indicator the stock should begin moving up.

The stochastic oscillator K value is 11.4677 and D value is 7.5284. This is a cyclical oscillator that is highly accurate and can be used to identify overbought/oversold levels as well as pending reversals and short-term activity. I personally use anything above 80 as overbought and below 20 as oversold. When the K value is higher than the D value, the stock is trending up. When the D value is higher that the K value the stock is trending down. The stochastic is oversold and the K has finally moved above the D. This is the fourth indication of pending near-term upward movement.

Considering the RSI, TSI, VI and stochastic levels, the overall direction favors a move to the upside. Based on historical movement compared to current levels and the current position, the stock could gain at least 5% over the next 31 trading days if not sooner.

Macys (M) might be a long, volatility is tellingFirst off, RISKY. Secondly, obviously in a downwards spiral. But it seems that earnings seem to be overstated (and the time in between). So this begs the question. Will this go up before earnings or on earnings? Id think yes. So I might be looking to open an order up after I check the right trade to get into. it MUST be a small position. Because this is obviously going down in the long run. BUT missing earnings doesn't seem to be the factor that decides if this gains or loses. (luckily) Check 11/10/16 missed earnings for any proof.

THE WEEK AHEAD: FXE OR /E6, P, NVDA, AND MWith the French elections now in the rear-view mirror, the Euro is at 1.10-ish at Asian open, and I'm looking to watch and short /E6 or FXE after seeing how far the spot forex pair goes here. Typically, the currency doesn't move all that much in the Asian session, so I kind of want to see what the European market does with the news before committing to a short position, which is likely to be a straightforward short call vertical, although some tweaking to the strikes being used will be necessary now that it's at 1.10-ish. (See Post Below).

Aside from that, we've got some quality earnings plays coming up this week, a few with the metrics that meet or almost meet my "smell test" (>70% implied volatility rank, >50% implied volatility).

P (80/68) -- announces on Monday after market close, so look to put on a play before the NY market shutters. Due to the size of the underlying, only a short straddle or defined risk iron fly makes any sense here for a nondirectional play.

NVDA (72/50) -- announces on Tuesday after market close. Short strangle or iron condor are the suggested plays with potential tweaks aimed toward limiting downside risk (e.g., Reverse Jade Lizard) so you don't get AMD'd if that's the way this cookie crumbles.

M (85/45) -- announces on Thursday before market open. At $29/share, this one's a kind of "in-betweener" -- you can go short strangle/iron condor if it pays enough or agress with a short straddle/iron fly if you want the allure of more credit at the door and the option to take profit at a lower max profit percentage. Of course, it's brick and mortar retail, which as a sector has seen individual name mixed results over the past several earnings cycles (being generous here), so my tendency would be to keep setup POP% high as a trade off against bringing in more in credit to give you greater flexibility dealing with a broken setup post earnings than a short straddle or iron fly would.

I'll post more concrete setups should I decide to dip my toe into one or more of these ... .

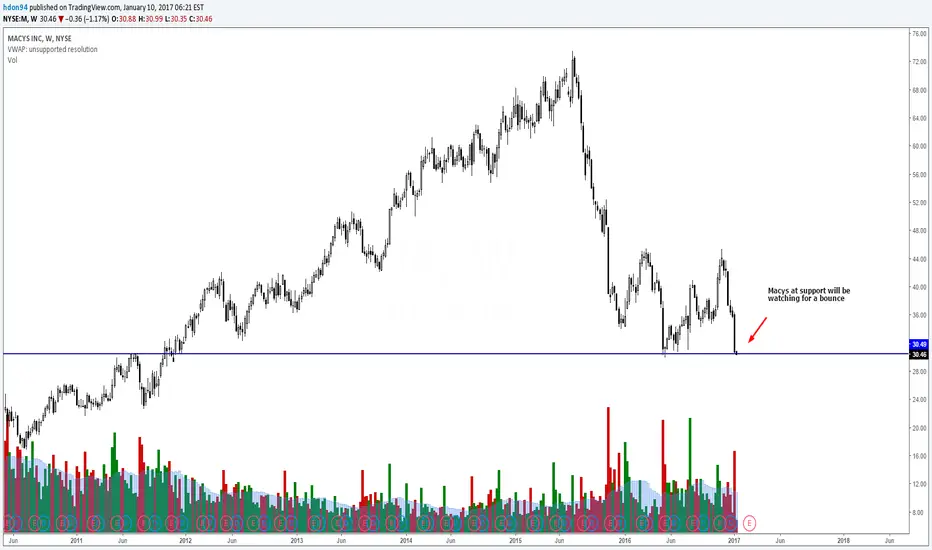

Macys - Possible LongMacys at a support level, will be watching closely for a bounce to go long (shares or calls).

$M - Golden retracement on weekly - falling wedge$M showing a golden retracement at the .618 w/ a sharp falling wedge w/ positive divergences. Looking for move north.