UBER 80 Afrer earnings ? NYSE:UBER

Uber Technologies Inc. Stock Surges to $75-$80 Range Following Strong Earnings Report

Uber Technologies Inc. (NYSE: UBER) has seen a significant boost in its stock price, reaching the $75-$80 range after the release of its latest earnings report. The ride-sharing giant reported impressive financial results for Q2 2024, with total revenue hitting $10.13 billion. This marks a notable year-over-year growth of 15%, showcasing Uber’s ability to expand its market presence and drive revenue despite challenging economic conditions.

The company’s strong performance was driven by increased demand for its ride-sharing and delivery services, as well as strategic investments in new technologies and markets. Uber’s net loss widened to $654 million, but the market responded positively to the revenue growth and future potential1. This optimism among investors has propelled the stock to new heights, reinforcing confidence in Uber’s long-term growth strategy.

As Uber continues to innovate and expand its service offerings, the future looks bright for this industry leader. Investors and market watchers will be closely monitoring how Uber leverages its current momentum to drive further growth and shareholder value.

CAFE CITY STUDIO & NY RUNS GLOBAL INC. NYC

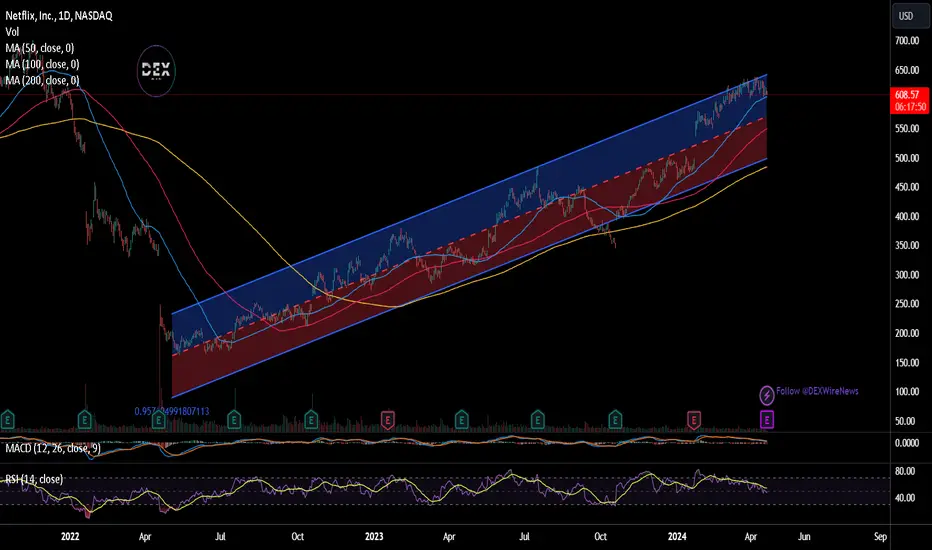

Netflix

$NFLX it was fun wall it lastedNASDAQ:NFLX while it's been a nice 300% gain over the last year 2 years, I think the trend is starting to reverse.

If you look at the chart, you'll see that we've formed a double top. You'll also see the price has held the trend line fairly well on the way up. Now we've rejected it twice and I think that price is heading much lower from here.

I think we're likely to see new lows by end of year. We've seen 3 touches on the support at $163, which leads me to believe that if price can retest that level, we'll break it and see new lows.

I think the lower supports $88-124 are likely.

I've taken these positions to express the view:

10 NFLX 08/16/2024 550.00 P

60 NFLX 01/17/2025 200.00 P

Let's see how it plays out

Netflix (NFLX) - Preparing for the Next Upward MoveBack in March, we anticipated the target zone for Netflix to be between the 38.2% and 61.8% Fibonacci levels. This zone was reached in April, marking the end for Wave 4 perfectly.

Since then, the overarching Wave (1) has likely been completed. We expect a significant correction before another upward move, with the anticipated pullback range between 35% to 50%. Despite the expected correction, we maintain a bullish outlook for Netflix, anticipating higher prices in the longer term.

Once we confirm the pullback and identify precise entry and exit points, we will issue a detailed market report.

🐲 The Roaring FAANG. Five Big Tech Stocks That Move The MarketFAANG is an acronym that stands for five major, highly successful U.S. tech companies: Meta (formerly Facebook), Amazon, Apple, Netflix, and Google.

FAANG stocks' performance has a substantial effect on the overall market and comprises 15% of the S&P500 Index SP:SPX .

If you follow the financial or business news, you may have seen or heard the term FAANG thrown around. No, it's not a misspelling or an animal's roar. It's an acronym that stands for five big companies — some might say the big companies — in the high-tech industry.

The FAANG quintet consists of Meta (formerly Facebook), Amazon , Apple, Netflix and Google (Alphabet as an official corporate name).

These corporations — all American, but with a global presence — are not only household names, they're financial behemoths. Their combined market capitalization is over $4 trillion. The blue-chip stocks of the tech sector, they collectively make up 15% of the Standard & Poor's 500 SP:SPX (an index of the largest public companies in the US). So they represent not only one of the US' most significant industries, but a sizable chunk of the US stock market itself.

The origins of FAANG

FAANG actually began as FANG. The origin of the acronym has been attributed to Jim Cramer, the financial TV host and co-founder of TheStreet.com. Known for his slangy abbreviations and catchy phrases, Cramer coined the term in 2013 to represent four tech stocks with outsized market appreciation. Cramer believed that these companies belonged together because they are all high-growth stocks that share the common threads of digitization and the web.

Cramer's original term was just FANG — it didn't initially include Apple. The company joined the ranks in 2017, reflecting the growth of internet services (iCloud, Apple Music, Apple Pay) to its revenues.

So the acronym became FAANG, and it's remained so.

The five stocks of FAANG

They need no introduction: The five stocks of FAANG are all familiar brands, whose products and services permeate our lives daily. They are also American corporate success stories — each has seen its stock shares experience triple-digit growth since 2015, and year-to-year as well.

👉 Meta ( NASDAQ:META ) is the social media maestro, owner of Instagram, WhatsApp, and its Facebook website. It has returned more than 190% over the past 12 months, and it is a # 1 over all S&P500 Index components with that amazing result.

👉 Apple ( NASDAQ:AAPL ), the sole product manufacturer of the group, with more than 36% yearly performance.

👉 Amazon ( NASDAQ:AMZN ), the world's largest e-store, has returned more than 65% over the past 12 months.

👉 Netflix ( NASDAQ:NFLX ), the superpower of streaming, has returned 44% TTM.

👉 Google — parent company Alphabet ( NASDAQ:GOOG , NASDAQ:GOOGL ) — has a name synonymous with internet searches and services. Its GOOG shares have increased by more than 43% in 12 months.

Just to put these numbers in context: the S&P 500 has grown 17% over the past 12 months. So FAANG stocks have been at the forefront , significantly outperforming the broad market.

Twelve months performance of FX:FAANG components vs S&P500 Index

The bottom line

The main technical graph (3-day chart for FX:FAANG stock basket, introduced by @FXCM provider, with 20% inception weight for every single component) illustrates perhaps right there happens the major breakout of 52-week highs, with further projected/ targeted upside price action.

Netflix - Gap fill? NFLX would have to 3X to return to Highs?Netflix - NFLX - Can it regain its previous stock price? Will its ads subscription model make it more competitive? Will its content win more viewers over? Who knows? What we do know is that price is filling the gaps from the previous decline. I am not counting NTFLX out. Patience pays off.

Netflix is goin up to $764 with the trend traders favourite toolRegression Channel (Trend traders)

This is a channel that picks up the support and resistance of any trend.

Clearly the trend is up, and the contination trend's momentum is strong.

We can expect Netflix to rally further.

Nature: High Probability

Price>20

Price>200

Target $764.80

Double Top for Earnings 15x Put Option Insurance Play InsideI think Netflix will show how bad the consumer is and it'll capsize with the markets after earnings forming a double top. This stock will rebound off red or orange support.

Buy the 550 August 16th, it could return up to 1500% return. NFA!

Netflix Descending Triangle BreakoutThank you everybody for dropping in on this trade idea setup in Netflix. Bullish descending triangle continuation pattern developing here looking like it's about to burst for next week or maybe this Friday as long as the market keeps going up. I want to make sure that I'm getting into these mega cap stocks because that seems to be the only thing that's really on an uptrend and making plays that are multi day uptrends. Another stock I'm looking at is Amazon because it seems to be basing out but I want to wait a little bit until after I get into Netflix before I jump into any other trades since I have a good amount of position size already allocated in my entire portfolio.

NFLX - Netflix / Idea INetflix

12M: → Bullish close but truely bullish above 701

→ the grey zone being at → 633 – 585 (Fib ext.)

→ in case of a breakout 744 is target

3M: slightly less progress because of 701 Ath close by – traders will think about double top from here on

→ 701 showdown likely

Monthly: Bullish close but yet a bit hesitation going on here. Probably some profit taking going on.

3D: Ascending Triangle in play like in many other stocks – waiting game until a break occurs

thanks for reading, feedbacks appreciated

NETFLIX Retesting All-Time-High! Sell!

Hello,Traders!

NETFLIX is trading in a

Strong uptrend but the

Stocks is now retesting

An all-time-high horizontal

Resistance level around 700$

From where we will be

Expecting a local bearish

Correction because the

Stocks is locally overbought

Sell!

Like, comment and subscribe to help us grow!

Check out other forecasts below too!

NFLX - Bullish NetflixNetflix is within this expanding structure looking to continue climbing

I expect a retest of the dashed white support line and then continuation up towards the top of this structure where I have point price labels.

Bars pattern is just an example of how this could occur.

Daily chart for NFLX

NVIDIA 176% YTD GAINS 2024 NASDAQ:NVDA 🚀 NVIDIA’s Stellar Ascent: A 176% YTD Surge! 🚀

In the high-stakes world of tech stocks, NVIDIA has emerged as the year’s undisputed champion, boasting a jaw-dropping 176% increase in its stock price year-to-date. Here’s a snapshot of why NVIDIA is the talk of Wall Street:

Market Cap Milestone: NVIDIA has not only skyrocketed in stock value but also achieved a monumental market cap of $3.335 trillion, surpassing tech giants like Microsoft to become the most valued company in the world.

Stock Split Magic: The company’s recent 10-for-1 stock split has made its shares more accessible to a broader range of investors, fueling the fire of its already impressive rally.

Generative AI Gold Rush: NVIDIA sits at the forefront of the generative AI revolution, with its GPUs being the powerhouse behind the scenes. This sector is projected to reach a staggering $967.6 billion by 2032, and NVIDIA’s leading-edge technology is poised to reap the benefits.

ETF Rebalance: A leading tech ETF has shifted its balance, significantly increasing its stake in NVIDIA. This strategic move involves a massive $23 billion stake exchange, highlighting the confidence investors have in NVIDIA’s future.

Wall Street’s Vote of Confidence: Analysts are bullish, with predictions that NVIDIA’s stock could soar to $200. The consensus is clear: NVIDIA is expected to dominate the computing market for the next decade.

NFLX ContinuationNFLX is starting to flag and tighten above previous highs. Basic resistance turned support flip, plus our premium indicator is printing bullish continuation.

#NETFLIX Could rip faces in a Reactionary RALLYAfter getting destroyed and dropping like a #Crypto

The chart has showed relative strength

and formed a Bullish CUP & HANDLE

Some stocks will probably not survive these market conditions in the next couple years, which is healthy

So look for signs of strength vs the broader market

NFLXPair : NFLX - Netflix

Description :

Completed " 12345 " Impulsive Waves

Break of Structure

RSI - Divergence

Bullish Channel as an Corrective Pattern in Short Time Frame

Resistance Level

NFLXPair : Netflix - NFLX

Description :

RSI - Divergence

Demand Zone

Rising Wedge as an Corrective Pattern in Short Time Frame with the Breakout of the Lower Trend Line and Retracement

Break of Structure

Completed " 12345 " Impulsive Waves

NETFLIX Bullish break-out eyeing $725.00Netflix (NFLX) has established trading above the 1D MA50 (blue trend-line), turning it into a Support following the rebound since May 01. With the long-term pattern since June 14 2022 being a Channel Up, similar bullish break-outs above the 1D MA50 (blue circles) have been the start of Bullish Legs.

Even the 1D RSI has been very consistent at identifying bottoms. The last two Bullish Legs topped after the price hit the 1.786 Fibonacci extension level. As a result, we remain bullish on NFLX, targeting $725.0 (the 1.786 Fibonacci).

Flashback to our previous idea:

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

NFLXPair : NFLX - Netflix

Description :

Double Top

Resistance Level

Completed " 12345 " Impulsive Waves

Impulse Corrective

Break of Structure

CHoCH

The Best Months of The Year to Invest in US Stock to Make Money This video will show you the best months of the year you should be investing in US stock market.

In the video, I showed proof that this method works almost every time.

But if you feel you need me to guide you further on how to manage your investment portfolio, feel free to send me a DM now.

If you find this video helpful, give it a like, drop comments, and share it with your friends.

NFLX is setting up for another gap down open next weekNFLX is setting up for another gap down open next week

Quite bearish action here, no longs for me until Jan gap close is closed

NFLX: Bullish dip?Friday was nasty for big tech. 10% drops in NFLX and NVDA got some people to fear for the worst. Is the market going to crash 90% now? Maybe not yet. Right now the price only retraced to 0.764 fib. I would expect a little more weakness next week and then a relief rally. Price should come down to about .618 fib retracement area where there is also some market structure support and take off from there. Weekly RSI is showing some bullish divergence, but not confirmed yet. As long as price doesn't fall through market structure supports and below $344, bull case is still on track to 2026 top. Good thing is that NFLX falls fast and recovers fast. Bad news is it is kinds difficult to time the short for this stock because it falls so quickly. So, I am not planning on shorting and also not worried yet on the long bag. Actually planning to add to the bag maybe another $30 below this level. We'll see how things go.

NFLX Netflix Options Ahead of EarningsIf you haven't entered NFLX in the buying zone:

Then analyzing the options chain and the chart patterns of NFLX Netflix prior to the earnings report this week,

I would consider purchasing the 607.50usd strike price at the money Calls with

an expiration date of 2024-4-19,

for a premium of approximately $26.50.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Netflix Faces Subscriber Growth Challenge Netflix has consistently set benchmarks and pushed boundaries. However, as the company gears up to report its earnings, a closer look reveals a nuanced landscape where subscriber growth is no longer a foregone conclusion. The once-lauded crackdown on password sharing, while initially boosting numbers, now presents a plateauing challenge. With the fervor of the pandemic waning, Netflix must navigate through shifting tides to sustain its momentum.

The Password-Sharing Conundrum

Netflix's recent surge in subscriber numbers was partly fueled by its global crackdown on password sharing. Yet, analysts warn that the euphoria from this initiative might be waning, especially in mature markets like the United States. While the crackdown may still yield results in burgeoning markets like India, it's evident that Netflix needs more than a singular strategy to fuel growth.

Diversification Beyond Traditional Models

In a bid to diversify revenue streams and cater to a wider audience, Netflix ( NASDAQ:NFLX ) has ventured into an ad-supported tier. With over 23 million monthly subscribers already onboard, this move marks a significant shift in its business model. Analysts predict that the ad-supported tier could play a pivotal role in mitigating churn and bolstering revenue in the years to come. Moreover, recent price hikes in premium plans could further incentivize users to opt for the ad-supported model, driving up average revenue per user.

Strategic Content Investment

Netflix's commitment to content remains unwavering, with projected investments reaching as high as $17 billion this year. Unlike its competitors, who are trimming content budgets to achieve profitability, Netflix ( NASDAQ:NFLX ) is doubling down on its content strategy. By retaining a flat spending trajectory, Netflix has managed to attract subscribers while securing rights to coveted content. The recent trend of competitors selling exclusive content to Netflix not only reduces churn but also underscores the company's dominance in the streaming arena.

Sports Entertainment: A New Frontier

In a strategic move to diversify its content portfolio, Netflix ( NASDAQ:NFLX ) has entered the realm of sports entertainment. The recent deal with World Wrestling Entertainment (WWE) signals Netflix's intent to tap into the lucrative sports entertainment market without bearing the exorbitant costs associated with traditional sports rights. By acquiring WWE's flagship program, "Raw," Netflix aims to leverage the inherent stickiness of sports content while aligning with its ethos of entertainment-centric programming.

Conclusion:

As Netflix ( NASDAQ:NFLX ) prepares to unveil its earnings report, the spotlight shines on its ability to innovate and adapt in a rapidly evolving landscape. While challenges loom, from plateauing subscriber growth to intensifying competition, Netflix's strategic diversification and unwavering commitment to content position it as a formidable force in the streaming industry. By embracing change, seizing opportunities, and staying true to its vision, Netflix ( NASDAQ:NFLX ) charts a course towards sustained growth and continued relevance in the ever-expanding world of streaming.