NETFLIX Will the stream giant correct after the Earnings?Netflix (NFLX) is reporting Earnings today and what we see from the past 4 weeks that has been unable to make new Highs, it might be pricing a peak. That peak might be a technical Higher High formation on the 1.5 year Channel Up, which is the Earnings disappoint, can initiate a medium-term correction towards the 1W MA200 (orange trend-line) and 1W MA50 (blue trend-line) Support Zone.

The technical confirmation for a sell will most likely be a 1W candle closing below the 1D MA50 (red trend-line), which has been the standard support of uptrends within the Channel Up. In addition to that, we will be expecting to see the 1W MACD form a Bearish Cross. On that signal, we will target 425.00.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Netflix

Decide: Buy or Sell - Netflix vs. Tesla EarningsSome analysts anticipate that Netflix's stock could reach a new 52-week high above $500 per share following the release of its fourth-quarter earnings report this Tuesday. The $506 mark is considered a target, representing the price it fell to at the beginning of 2022.

Positive sentiment towards Netflix has grown as profit estimates have been revised upward 17 times since the last earnings report. The company's revenue is expected to increase by 11% annually to $8.71 billion, driven by the introduction of a new, lower-cost, ad-supported basic subscription tier and efforts to combat illegal password-sharing.

If the forecasted revenue materializes, it will mark the highest quarterly sales total in Netflix's 17-year history, representing an 11% increase from the previous period to $8.7 billion.

However, this quarter's earnings might not live up to the company’s last earnings call, which generated a ~15% bump.

Meanwhile, Tesla's fourth-quarter update, scheduled for release on Wednesday after the close, may have a different trajectory. Tesla shares declined by 4.4% after the last earnings report, experiencing their third consecutive earnings-reaction-day selloff.

A fourth occurrence is possible, although it's also possible that the bottom is in. It will likely come down to whether investors are disappointed in their forward guidance for the first quarter of 2024

Tesla's margins are expected to face pressure due to its ongoing price-slashing strategy in recent quarters. However, this might already be factored into the current stock price.

TSLA has shown a pattern of lower highs and lower lows since the peak in July 2023, and it remains to be seen if support will materialize at its support levels of $200 and $194.

NFLX / 1H / TECHNICAL ANALYSIS NASDAQ:NFLX I expect a bullish movement towards the 518 level if the resistance zone at the 503 level is breached and there are candlestick closures. Our support level is at 461.

Like and comment if you find value in our analysis.

Feel free to post your ideas and questions at the comments section.

Good luck

A Traders’ Week Ahead Playbook: living in interesting times We reflect on the week that was and where the US equity markets stole the show, with new highs in the S&P500, and the NAS100 outperforming all major equity markets. A.I names went on a tear on Friday, where notably Nvidia, Broadcom and AMD felt the love. With 16% of the S&P500 market cap reporting this week, earnings and corporate outlooks will play a greater role in the price action – it is hard to be short these markets given the upbeat flow but it’s hard to chase as well.

Tesla and Netflix will be the trader favourites this week, with the options markets implying moves (on the day of reporting) of -/+ 5.4% and 7.5% respectively. Tesla needs to pull something out of the bag to turn sentiment around and we see price having lost 20% in the past 14 days. Netflix comes off the back of a 16.1% rally on the day of reporting Q323 numbers, so longs will be hoping for something similar, to take price above $500. A daily close below the 50-day MA and I’d be exiting longs.

Conversely, the HK50 and CHINAH were savaged by over 5% and shorts continue to be the play, although a surprise cut to the 1 & 5-year Prime Rate would cause a decent reversal higher.

Pushback from several central bankers on the start point and extent of rate cuts (priced into swaps markets) caused front-end bond yields to move higher last week, with the market reevaluating whether March is indeed the start date for many central banks to start a cutting cycle. In the case of the Fed, the implied probability has fallen to 50%, and this pricing should hold firm until we see core PCE print later in the week – The USD holds a fair relationship with the evolving implied pricing for a March Fed cut, where rate cut probability falls the USD rallies (and vice versa).

The USD was the best performing G10 currency last week but with the ECB meeting in play this week, there are reasons to think EURUSD could push back into the 1.0950/70 area. The NZD gets close attention given the Q4 CPI print due and we’re seeing signs of diverging paths between the RBA and RBNZ in market pricing – looking for NZDUSD shorts on a momentum move through 0.6100 and AUDNZD longs at current spot levels, adding on a close through the 200-day MA.

The flow and set-up in gold is a little messy and the price is chopping about – no real directional bias in the near term and would look at selling rallies on the week into $2055 and buying dips into $2000.

While Nat Gas is getting good attention given price is in freefall, Crude is also on the radar with rallies recently sold into $75.20 and dips bought at $70 – A break on either side of that range could be meaningful.

Politics also comes into focus with the New Hampshire REP primary held on Tuesday – it won’t be a market event but could pull Trump one step closer to becoming the REP nominee, a fate most fully expect.

Good luck to all.

Marquee economic data for traders to navigate:

• China 1 & 5-year Loan Prime Rate – After the PBoC surprised and left the Medium-Lending Facility (MLF) rate unchanged last week the market now assumes the PBoC will also leave the 1 & 5-year prime rate unchanged at 4.2% & 3.45% respectively. The CHINAH was the weakest major equity market last week (-6.5% wow) and could revisit the October 2023 lows unless we see something far more definitive from the Chinese authorities.

• BoJ meeting (23 Jan no set time) – this should be a low vol affair, where expectations for policy change at this meeting are incredibly low, and one would be highly surprised if the BoJ lift rates out of negative territory. Consider the BoJ will provide new CPI and GDP forecasts at this meeting, and they could be very telling of the future need to move away from a negative rate setting.

• NZ Q4 CPI (24 Jan 08:45 AEDT) – the market sees Q4 CPI running at 0.5% QoQ / 4.7% YoY (from 5.6%. This is a clear risk for NZD exposures, where the outcome could see the market questioning if the RBNZ cut before/later than current pricing (in swaps) to start easing in May with 91bp of cuts priced by year-end. I like AUDNZD upside on growing central bank policy divergence.

• EU HCOB manufacturing and services PMI (24 Jan 20:00 AEDT) – the market sees both surveys modestly improving at 44.8 (from 44.4) and 49.0 (48.8) respectively. A services PMI read above 50 would likely promote EUR buying.

• UK S&P manufacturing and services PMI (24 Jan 20:30 AEDT) – The consensus is that we see the manufacturing diffusion index improving a touch to 46.7 (from 46.2), while services should grow at a slower pace at 53.0 (53.4). GBPUSD is carving out a range of 1.2800 to 1.2600 and I’m happy to lean into these levels for now.

• US S&P global manufacturing and services PMI (25 Jan 01:45 AEDT) – the market looks for the manufacturing index to come in at 47.5 (from 47.9) and services at 51.0 (51.4). A services PMI print below 50 could cause some gyrations in the USD and equity.

• Norges Bank meeting (25 Jan 20:00 AEDT) – The Norwegian central bank will almost certainly leave interest rates will stay unchanged at 4.5%. The market prices the first cut from the Norges Bank in June, with 107bp of cuts priced this year.

• Bank of Canada meeting (25 Jan 01:45 AEDT) – the market prices no chance of action at this meeting. The first cut from the BoC is priced in April with 101bp of cuts priced this year, so USDCAD (and the CAD crosses) tone of the statement.

• Japan Tokyo CPI (26 Jan 10:30 AEDT) – the market looks for headlines CPI to come in at 2% (from 2.4%), and super core at 3.4% (3.5%). The JP CPI print would need to miss/beat by some margin to cause a move in the JPY given the print is seen so soon after the BoJ meeting.

• ECB meeting (26 Jan 00:15 AEDT) – the market ascribes no chance of a cut at this meeting, but the ECB will provide new growth and inflation forecasts. Recent communication from multiple ECB members suggests a growing consensus for a cut in June, although EU swaps pencil in the first cut in April (priced at 82%), with 136bp of cuts priced by December.

• US core PCE inflation (27 Jan 00:30 AEDT) – the median estimate is for headline PCE to come in at 0.2% QoQ / 2.6% (unchanged) and core at 0.2% QoQ / 3% YoY (from 3.2%). US swaps put the probability of a cut in the March FOMC at 50%, so the PCE inflation data could influence that pricing and by extension the USD.

New Hampshire (NH) REP Primary (23 Jan) – Donald Trump is leading Nikki Haley in the polls by 15ppt in NH, with Trump picking up votes with Vivek Ramaswamy recently exiting the race, while Nikki Haley is benefiting from Chris Christie’s recent departure. Haley must win here or come very close, or her chances of becoming the REP nominee drop sharply. There is talk that Haley may drop out after NH if she doesn’t come close to gaining the most votes in NH, although she may still run in the South Carolina Primary (24 Feb) given it’s her home state – either way, the race for the REP nominee could essentially be over depending on the outcome of the NH primary. Polls close at 8pm EST, so we should know the outcome shortly after that.

US earnings – GE, Procter & Gamble, IBM (24 Jan after-market), Netflix (24 Jan 08:00 AEDT), Tesla (24 Jan after-market), Visa, Amex, Intel

NFLX _ Volume AnalysisNetflix was being accumulated well prior to the POP> Check out how Unusual Market Volume Detector Identified the BUYING after Price divergence on the 12th OCT.

Selling resumed Today in NFLX/ NetflixIt is profit booking for sure, there is clearly a Red TrapZone and Red UMVD in place for now. So only shorts are active now for Netflix.

TrapZone and UMV combined together are complete automated technical analysis indicator package. You get to clearly see in Realtime the market trend strength and volume confirmation.

Netflix's Legal Triumph and Ad-Driven Ascension

In a recent legal showdown, streaming giant Netflix emerged victorious in a California federal court, successfully defeating a shareholder lawsuit that accused the company of concealing the impact of account-sharing on its growth trajectory. The lawsuit, filed by a Texas-based investment trust in May 2022, sought damages for investors who purchased Netflix shares between January 2021 and April 2022. Despite the significant blow to the stock value and a subsequent drop in subscribers, U.S. District Judge Jon Tigar ruled that the plaintiffs failed to provide evidence supporting their claims.

Legal Victory and Investor Response:

The judge's decision, delivered on Friday, underscores the importance of substantiated claims in legal battles. While Netflix shares initially faced a downturn, losing a third of their value, the ruling has provided a reprieve for the streaming giant. The door, however, remains open for the investors to refile the lawsuit if they can bolster their claims with additional facts.

Netflix's Stock Rollercoaster:

The legal victory is just one chapter in Netflix's rollercoaster journey in the stock market. Between January and April 2022, the company's shares experienced a drastic decline of around 50%. The drop was triggered by revelations that account-sharing and increased competition had hindered new subscriptions. Former CEO Reed Hastings attributed some of the challenges to the complexities of interpreting subscription trends amid the ongoing COVID-19 pandemic.

Ad-Supported Triumph:

Amidst the stock market turbulence, Netflix is finding success in an unexpected corner—the ad-supported realm. Recent reports indicate that Netflix's ad-based plan has surged, surpassing 23 million global monthly active users. This substantial growth, revealed by President of Advertising Amy Reinhard at the Variety Entertainment Summit at CES 2024, marks a notable increase from the reported 15 million users just over two months ago.

Engaging the Audience:

Reinhard emphasized the robust engagement levels among users on ad-supported plans, with a staggering 85% streaming on the platform for more than two hours daily. This data suggests that the ad-supported model is resonating well with Netflix's audience, providing a fresh perspective on the evolving dynamics of streaming preferences.

Pricing Strategy and Market Penetration:

Netflix's pricing strategy for its ad-supported plan is noteworthy, with the Basic With Ads plan priced at $6.99 per month in the United States—less than half the cost of the Standard plan at $15.49 per month. This strategic pricing could be a key factor in attracting a broader audience to the ad-supported tier, as ad-tier subscriptions reportedly account for approximately 30% of all new signups in the 12 countries where the platform has been launched.

Microsoft Partnership and Technological Advancements:

Netflix's success in the ad-supported arena is further amplified by its ad-tech deal with Microsoft. The partnership designates Microsoft as Netflix's global advertising technology and sales partner, playing a pivotal role in the triumph of Netflix's advertising strategy and technology infrastructure.

Conclusion:

As Netflix navigates legal challenges and charts a new course in the ad-supported landscape, the streaming giant continues to demonstrate resilience and innovation. The legal victory provides a foundation for future endeavors, while the surge in ad-supported subscriptions showcases Netflix's adaptability in meeting evolving consumer demands. The company's strategic pricing, coupled with a robust technological infrastructure, positions it for continued success in an ever-changing streaming landscape.

NETFLIX: This rebound isn't a buy opportunity.NFLX is staging a rebound on the 1D MA50 on a marginally bullish 1D technical outlook (RSI = 56.295, MACD = 4.710, ADX = 36.125). We don't consider this a buy opportunity as even if a slightly HH is made, the 1D RSI is showing a Bearish Divergence on a Channel Down, the same kind of bearish pattern that started the bearish waves in the two HH prior. Consequeantly we expect a pullback to at least the bottom of the Channel Up (dashed) or the HL trendline (which will be -25.25% from the top) depending on when the 1D RSI crosses under the 30.000 level (oversold), which was the buy trigger on the last two bottom opportunities. We have a long term TP = 550.00.

See how our prior idea has worked:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

APPLE BACK TO 182 SOLID POSITION Long Position:

Key Points:

Strong Fundamentals: Apple has a history of solid financial performance, driven by its diverse product ecosystem, including iPhones, iPads, Macs, wearables, and services. The company's consistent revenue and earnings growth make it an attractive option for long-term investors.

Services Segment Growth: Apple's services segment, including the App Store, Apple Music, and Apple TV+, has been a significant contributor to revenue. Continued expansion and growth in the services sector can provide a more stable revenue stream for the company.

Innovation and Product Pipeline: Apple's commitment to innovation, evidenced by new product releases and technological advancements, keeps the brand at the forefront of consumer technology. Anticipated releases and advancements in products like the iPhone and wearables can drive excitement and demand.

Share Buybacks and Dividends: Apple has a history of returning value to shareholders through share buybacks and dividends. Share repurchases can contribute to stock price appreciation, and dividends provide income to investors.

ADOBE LONG 620 LONG 620 TP

Long Position:

Adobe has consistently demonstrated strong financial performance, driven by its leading position in the creative software and digital experience markets. The company's subscription-based model provides a reliable revenue stream, and its innovative product portfolio continues to attract a wide user base.

Key Points:

Earnings Growth: Adobe has shown impressive earnings growth in recent quarters, fueled by increasing demand for its creative cloud services. Positive trends in earnings can drive stock appreciation.

Subscription Model: Adobe's shift to a subscription-based model ensures a steady stream of recurring revenue. This stability may appeal to long-term investors seeking a reliable growth story.

Digital Transformation: Adobe is well-positioned to benefit from the ongoing digital transformation across industries. As businesses and individuals increasingly rely on digital tools for creativity and marketing, Adobe's products remain essential.

Innovation: Adobe consistently invests in research and development, ensuring a pipeline of new and improved products. The company's commitment to innovation may drive future revenue growth and market share expansion.

Netflix in large Cup and Handle PatternNetflix appears to me to be completing a large cup and handle pattern. The initial peak of the cup appears at a price level of about $485 while the base appears to be at a low of $345. This price difference is $140, so I suggest the possibility that a new price target for NFLX should be at $625.

The handle has just been broken in the upward price direction and I am trading this to that price target unless invalidation occurs. I am watching for the stock price to hold the $485 support that was once previously a resistance to confirm the trend and avoid invalidating the technical formation.

NFLXNetflix, Inc. is an entertainment services company.

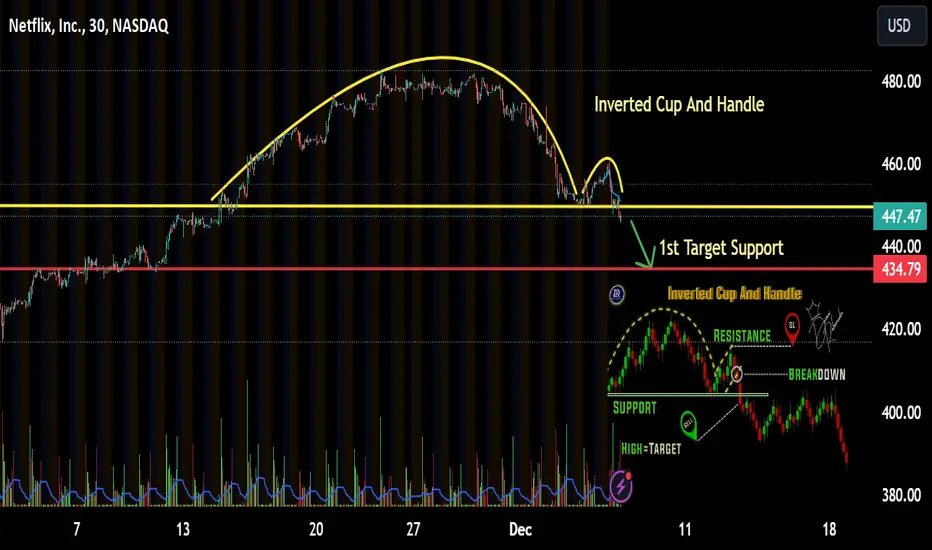

Good point to start correction.

tp1 442

tp2 404

$NFLX Inverted Cup And Handle NASDAQ:NFLX I Found a Cup And Handle for you. My 1st target for next week would be 434ish area. Also tomorrows NASDAQ:AVGO ER should have an adverse effect on the market tomorrow along with eco data. It will be an interesting Thurs and Fri

NETFLIX Expect this rally to be extended.Almost a month ago (October 31) we gave a strong buy signal (chart below) on Netflix (NFLX) with the price reacting immediately having entered a non-stop rise:

Due to the sheer aggression of the current bullish leg of the Megaphone as compared to its previous ones though, we have to downgrade our medium-term target to $580, which will make a perfect +69.30% rise from the bottom as the July 18 High. Their RSI patterns are quite similar, though obvious that the current is more aggressive, hence will correct equally aggressively at some point, probably early-mid January 2024.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Short $NFLX hereNASDAQ:NFLX looks like a great short here. Took some puts Nov 24 $437.5 and $435.

I'm expecting a retracement down to at least $413 or $396, however lower targets also possible (hence why I added the to the chart).

SELL NVIDIA AFTER EARNINGS 350 TP Market sentiment Sell OFF

Sell Nvidia from 500 - 510

Stop Loss 550

all the way back to 450 TP - TP SELL OFF 350 FINAL

be patient until December 2023 - January 2024

CAFE CITY STUDIO

Put your Stop Loss Because thats your Insurance !!!

NETFLiX: $230 | Key Levelsfolks at $1.30 and $0.35 cents should be getting ready to upsize ..

and for those who sold at $10 and $20 ..

maybe an opportunity to get back on board Gamblers and Clueless folks at $700 and $600

hang in there and meet you halfway at $300

NFLX ~ Snapshot TA (Daily / Nov 2023)NASDAQ:NFLX chart mapping/analysis.

Bullish recovery back into ascending parallel channel (green).

Bull target(s)

Breakout descending parallel channel (white) + descending trend-line confluence resistance

Overhead gap fills (~470 / ~506.93 / ~566.88)

Golden Pocket Fib + gap fill (~506.93) confluence resistance zone

Bear target(s)

Underlying gap fills (~412.52 / ~354.79 / ~341.38)

Ascending trend-line support (light blue dotted)

38.2% Fib

23.6% Fib

SPX BACK TO 4100 BY DECEMBER 2023 - JANUARY 2024 Be patient

This Trade can take 1 Month or 2 Months

SET IT AND FORGET IT !!

Do not overtrade

Do not Overleverage

PUT ONE TRADE AND WAIT !!

SOME TIMES IS HARD BUT PAYS OFF !!

CAFE CITY STUDIO 2024

Netflix Surges 28% Since Q3 EarningsNetflix's stock in 2021 has been a rollercoaster, starting with a strong 62% rise by July, nearing the $500 mark, before experiencing a sharp downturn. The stock fell below the crucial 200-day moving average to around $370, marking a significant 28% drop, but found some support at the weekly 50-day average near $350.

The Q3 earnings report was a turning point, with actual earnings of $3.73 surpassing the estimated $3.49. This led to a positive market reaction, with the stock opening 16% higher post-announcement and climbing 28% since then. The surge in earnings was primarily due to robust subscriber growth, a key indicator of the company's future financial health and stock potential.

Looking ahead, Netflix faces major resistance levels, first at the $500 psychological mark, and then at last year's high of $609. Overcoming these barriers could signal further bullish trends. As of November, the stock is showing strong performance with an 8% increase, adding to the positive outlook among investors.

If you enjoyed this post, make sure to like, and follow for more quality content!

If you have any questions or comments, comment below. We reply to every comment!

See below for more information on our trading techniques.

As always, keep it simple, keep it Sublime.

netflix approaching a big jumping pointHoly smokes, this is lining up for one huge final pump. If she holds 365, there is potential to rocket all the way up to 436. It won't be in 1 night, you'll have time to buy and sell, but it won't be a lot of time. You'll likely start seeing big AH movements, and a bunch of solid green days in a row as it climbs.

There is a chance it breaks down to 333, but again, there should be time to exit and reset your trade before it gets all the way down there. I would favor the upside pretty heavily on this trade, however, WAIT until it bounces off trend. If it hits the red trend, enter short on the rejection. If it climbs down and hits the green, go long on the support bounce.

Apple - Sick Fundamentals Mean a New All Time HighI have recent calls on the SPX

SPX ES - Welcome To The Fourth Quarter Rodeo

The Nasdaq

Nasdaq Futes - You Wanted a Dip For That 'Santa Rally,' Aye?

SPY

SPY - Did We Bottom, Or Is Manipulation Coming?

And Tesla

Tesla - Remember, The Ponzi Always Continues

Which generally have a bullish-into-year-end thesis accompanying them, but caution that an October bottom for the second year in a row and a mega three day rally to start November may be something of a trap.

When it comes to Apple, we have reservations that we topped under $200, for really obvious reasons, especially considering that on the monthly, the last three months of bearish price action haven't been that bearish.

Yet, because the weekly shows us that there are two bars under $150 and $140 from last year that never printed a low, that those areas are probably protected until Apple starts to seriously deflate and enter an end-of-life cycle bear market.

If Apple is going to enter an end of life cycle bear market, the MMs will 100% take out the $200 range and sell everything there first.

So, fundamentally, why would Apple be at the end of its life? The answer is simple: the company, all these years, wed itself to the Chinese Communist Party, which is the scourge of humanity, The Beast, and the benefactor to Babylon (Shanghai).

There's lots of really horrific data involving Apple numbers and the Chinese market right now, and the CCP under Xi Jinping is also rushing to replace other phone companies with domestic product, like the notorious Huawei.

The elephant in the room when it comes to cellular and computer purchases in China is that they're down because there are less people in China as a result of the enormous damage the novel pneumonia pandemic that originated in Wuhan City has caused.

SARS 1 in 2003 was covered up by the Party. The CCP made it seem like only a few thousand people died, when in reality, some accounts have stated that several million people died.

Today, the Party still claims that less than 122,000 people died from COVID-19, despite China being the epicentre of the disease.

You don't need an expert, or even a calculator, to figure out what's really going on and why the Chinese economy is in trouble.

What's at stake for Xi and his faction is the 24-year-long organ harvesting genocide and persecution against Falun Dafa's 100 million practitioners.

Although Xi has not participated in the persecution, and has, to the contrary, been killing via his Anti-corruption Campaign the Jiang Zemin faction who started and maintained the persecution all these years, the problem is that Xi is the head of the Party.

When you kill a dragon, you decapitate it. But first, you start with its tail. And it's telling that former Premier Li Keqiang died a few weeks ago, merely in his 60s, at the hands of "an heart attack."

So the fundamentals on Apple are bad because of China. So, with great faith in the principle of reversed logic, we actually look for longs with the chance to sell over $200.

But the charts, as they stand, are not giving us a long signal.

Everything, including Apple, bounced so hard in the first three days of November, and for Apple this came on the back of an earnings report, that we have to view the situation with major reservations, expecting that the candle painting of the low for the monthly bar has not yet been completed.

Last October, Apple pretended to bottom, pretended to double bottom in November, and then gave it all back and set the low of the year at the end of 2022, and all of this happened while the indexes had properly bottomed in October.

There was none of that "Magnificent 7" talk back then.

So, how to trade this? I think it's wiser to go long on a breakout over $183 in a size that allows you to take partials at $198, $205, and $215 than it is to have bought in the last three days.

And if we do dump, where we're looking for reversal patterns is at or below the April of 2022 low at $159.80~.

But if we're about to moon for manipulation, we're actually likely to see a sweep just below the current November low of $167.90.

So long as you can buy there without getting expired worthless on some short dated options, you'll have the best chance to ride the manipulation wave.

But be careful. When it's time for the CCP to fall, all the bigger dominoes go with it, because they're all really lesser dominoes.

Gap down overnight because of the time difference between Beijing and Manhattan means margin calls that scale in brutality, because Wall Street won't be in the mood to go risk on anything ever again.

Nor will it have the money or the breath to.

The Netflix: Streaming The Stock's PotentialKEY POINTS

a. Netflix now has 15 million subscribers in its ad-supported tier.

b. The company is also rolling out new ad products.

c. The success of the new subscription tier is just one of the reasons the stock has surged this year.

The leading streamer just hit a key milestone with its ad business.

Netflix (NFLX 1.80%) was one of the best-performing stocks of the 2010s, but for much of the current decade, the once-meteoric growth stock has struggled to achieve liftoff.

The company got a temporary boost from the pandemic, only to give it all back and then some when the economy reopened in 2022, and it lost subscribers two quarters in a row. Since then, the streaming leader has regrouped, launching initiatives that some investors had long asked for, such as adding an ad-supported tier and cracking down on password sharing.

The results of those moves have been overwhelmingly successful with the stock up 47% year to date, even as many of its streaming peers like Disney and Warner Bros. Discovery are trading near 52-week lows.

With the help of paid sharing, Netflix has added nearly 15 million new subscribers over the last two quarters, beating its total additions from the previous five quarters. The stock jumped following the third-quarter earnings report in October on strong subscriber growth as well.

Building on this recent momentum, Netflix provided an update Wednesday that shows its new ad-based strategy is paying off.

A key milestone

It's been one year since the company launched its ad-supported tier in a handful of its biggest markets, and the company said the new service has now signed up 15 million subscribers, up from just 5 million in May. That news should not only tamp down concerns that growth from this tier has been weaker than expected but also show that the ad-supported option is clearly resonating with subscribers. Additionally, it's impressive to see those gains coming at a time when much of the digital advertising industry is struggling.

That figure represents more than half of net subscriber additions over the last year, though some of the ad-tier subscribers likely traded down from the more expensive ad-free tiers, especially after Netflix just raised prices on some of its plans in the U.S., U.K., and France.

Netflix has also refined its advertising product since launch and now offers five different ad lengths, ranging from 10 seconds to 60 seconds. It also offers targeting to mobile devices as well as options like more genres, time of day, and new audience demographics. Downloads are expected to be available by the end of the week, making Netflix the only ad-supported streamer to offer downloads.

The company has more new features planned for next year, including a binge-watching bonus that gives ad-tier subscribers an ad-free episode after they've watched three episodes in a row. It will also begin offering QR codes in ads and is expanding its partnerships program globally, allowing advertisers to sponsor certain shows.

Netflix's ad-supported tier may cannibalize some ad-free subscribers, but that's part of the company's strategy. Offering ads gives it cover to raise prices on ad-free tiers, as it just did, allowing the company to make more money from the ad-free side of the business (with the idea that the ad-supported tier should be revenue-neutral compared to the ad-free subscription, as it has been for Hulu).

The ad-tier option also capitalizes on massive existing demand from advertisers. As former CEO Reed Hastings noted in an Oct. 2022 earnings call, advertisers have been left behind by the transition to streaming and are anxious to follow the eyeballs that have already gravitated over to streaming services.

With more than 200 million subscribers globally, intimate knowledge of their viewing habits, and the ability to perform precise targeting, Netflix can offer advertisers much more than a traditional linear TV platform.

Why it's a buy

A little more than a year ago, investors seemed to think the growth story at Netflix was over. However, the recent rebound and strength from paid sharing and advertising shows the streamer's second act is well underway.

The company forecast subscriber additions of around 9 million in the current quarter, showing the recent momentum should continue, and its subscription business model means that incremental revenue flows through to the bottom line. Indeed, management sees operating margin improving from 20% this year to 22% to 23% in 2024.

If Netflix can continue to deliver subscriber growth, there's room for profits to go significantly higher. The success of the ad-supported tier will only make that easier.