NKE underperforming. At least this is what I'm seeing for NKE, as far as MAs and timeframes are concerned. I doubt the holiday shopping would be beneficial for them either.

NKE

NKE long Some PA supports some Fibo supports, potential Fibo target is 109+, down side risk is limited.

NKE - short from 51.60 or lower to 48 area NKE looks a very good short. It broke the support & going down after retested the support. moneyflow is very deep in negative side.

We think it will be a good short from 51.60 or lower down to 48 area

You can check our detailed analysis on NKE in the trading room/ Executive summary link here-

www.screencast.com

Time Span: 44:20"

Trade Status: Pending

Nike Showing Double BottomLooking for a bounce with NKE now showing a double-bottom from it's June 2016 low. Volume looks to be getting lighter, so I'm looking for volume to increase on the reversal and take it to $55.

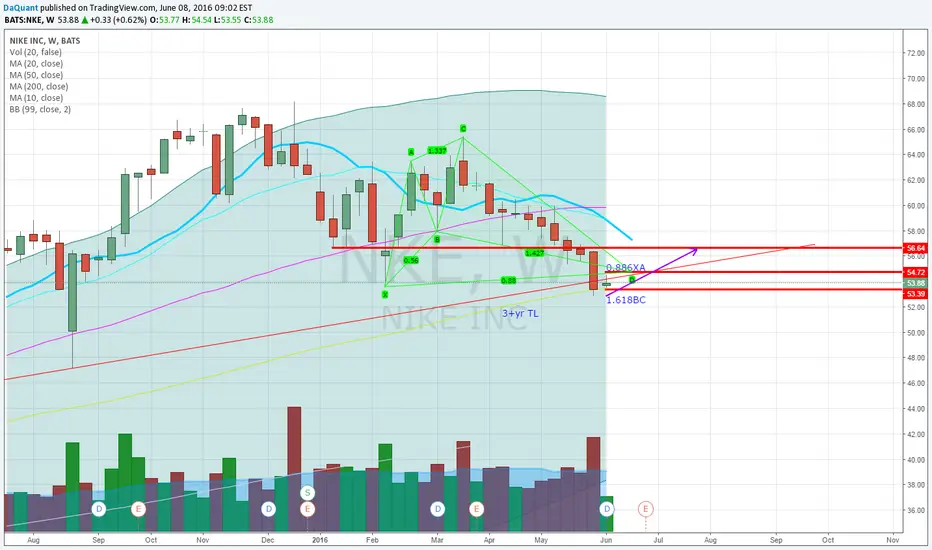

NIKEPossible trend continuation wedge.(ABCDE)

You could do a small short down to $50 then be ready to buy it right back up to $80ish.

Won't be trading this but this looks like a real good setup

$NKE falling wedge on daily$NKE falling wedge on daily.

.618 golden retracement.

Looking for upside move to 200 MA.

NKE - NIKE: ONE MORE WAVE UP BEFORE A POSSIBLE BIG DROP?Nike seems in the middle of a corrective phase. I'm expecting one more wave up before a possible big drop if downward trendline holds. Bullish divergence for the wave up. Buying the breakout seems a good idea.

Watching NKE to see if breaks the trend to reverse back to $58I never liked $NKE above $65 but now that the downward trend has taken it down to $54 it will be interesting to see if it will start a reverse back to $58 or will keep heading south to below $52 and then below $50.

#NKE go long :)Hey! I see nice opportunity to go long on this stock. We have strong support.. and the resistance almost 20% higher. I think that we can try earn some money on log position with nice R:R ratio.

NKE - intermediate top is here.We had a tactical upthrust, followed by a consolidation range which doesn´t look very strong. It could correct further........it very often shows new signs of life before any major worldwide sports event :-)

NIKE is long term bullish.Buy this stock and forget . This is a stock that gives dividend. Important is to enter at a right time.

I see this stock touching 60.24 in near term as it is correcting. But it will pull back from here as there is strong support.

If it break the support of 60.24, then is may be range bound or move down. So watch out and exit in that case.

Strategy: Buy at 60.24. with stop loss of 59.74 which is just below 200 MA

Target : 67 and long term bullish .

BOUGHT NKE APRIL 15TH 56.5/60/69/72.5 IC TO CLOSEClosing out at 50% max profit. Although price moved concerningly close to the short put, the collapse in volatility in the underlying gave the needed assist ... .

SOLD NKE APRIL 15TH 56.5/60/69/72.5 IRON CONDORI had to fiddle a bit with the expiration and the strikes to get what I wanted, but the metrics are basically the same as outlined in the post below..

Got it filled for a 1.03 credit ($103/contract).

Notes: Looking for NKE's implied volatility to contract post-earnings, as well as for price to stay between my short strikes.

Put reverse ratio ahead of earningsI am bullish and want to take advantage of volatility. -4P@65 +1P@71 +3P@65 for March 24