NVIDIA. possible another 59.23% gain. 6/June/24NVDA's 1890 (189 after splitting ) is next major resistance where price meet time by end of the year ( right after US election).

Nvidia

Nvidia headed towards completion areaHaving entered the area of a wave (iv), and now exited the box to the upside to challenge the recent ATH, I have to consider the possibility we're headed towards the wave (v) target area to complete this primary wave 3. However, to be clear, below the ATH of $1158.19, we're still in wave (iv). This is visible in the below 1 hour chart.

Nvidia will be embarking on a primary circle wave 4, that could last years. This will not be an event over in a matter of months.

Best to all,

Chris

Nvidia Stock Eyes Apple’s 2nd Spot After Monster 30% Gain in MayChip giant racked up nearly $700 billion in market cap last month and is on track to become the world’s second-largest company.

If you’ve been extremely online and following the headlines for a while, you know how this blog will kick off: Nvidia (ticker: NVDA ) crushed, smashed, and shattered all expectations while reporting record profits and revenue. The artificial intelligence (AI) bonanza is so strong it’s literally no-froth-gains-only out there.

Not that much in the loop? Let’s catch you up. For the fiscal first quarter, Nvidia reported record revenue of $26 billion, up 262% year-over year. Along the way, shares of the AI-focused company soared past $1,000 a pop and the stock is now threatening to overtake iPhone maker Apple (ticker: AAPL ) as the world’s second-largest company .

Blink and You’ll Miss It. You Blinked, Right?

Not that long ago — in March 2019 — Nvidia was a little-known GPU provider with its niche found in the gaming sector and the crypto mining corner. And, worth mentioning, it was chugging along as the 84th company in the world by market cap with shares changing hands at $30 a piece.

Fast-track to nowadays, Nvidia’s market cap hovers near $2.7 trillion after gaining a monster 3,755% from its March 2019 lows. It also swooped in as the third-biggest company globally, replacing Amazon (ticker: AMZN ).

Nvidia’s Big Gains Could Dethrone Apple

The AI mainstay picked up more than $700 billion, or 30%, in valuation over May as its shares hit a record high of $1,160. The big leap positioned the company’s market cap less than 10% shy of Apple’s $2.95 trillion. This said, another $250 billion and Nvidia will become the second-biggest company in the world, trailing Microsoft ( MSFT ), valued at $3.2 trillion. That is, if Apple stays where it is now.

The iPhone maker, on the other end of the spectrum, is having a rough year. The victim of a monopoly lawsuit , Apple is witnessing its shares linger around a 3% gain for the year, compared with Nvidia’s 130% rise.

What’s more, spiraling iPhone sales in China added to the brewing troubles.

Can Nvidia Sustain Its Bonkers Revenue Growth?

Looking forward, Nvidia expects to rack up revenue of $28 billion for the current quarter . Recent quarterly performance shows that this type of guidance is not only being met, but it’s being comfortably exceeded.

That’s what happens when you have big tech companies lining up to be your loyal customers. Nvidia is happily selling its hot hardware to the biggest and baddest out there — Microsoft (ticker: MSFT ), Google (ticker: GOOGL ), Tesla (ticker: TSLA ) and privately-held ChatGPT parent OpenAI are all scrambling to get their hands on the powerful chips made by Nvidia.

These heavyweights usually pre-order the good stuff and sign contracts worth billions and billions of dollars, allowing Nvidia to predict how much revenue it will bring in over a quarter.

Coming for That Margin

Investors poured hundreds of billions into Nvidia as they sought to capture the AI train. What this has done to the industry is to propel a single company to the forefront while leaving a huge gap for the rest of the companies that a) have ample amounts of cash to invest, and b) are looking to get a piece of the AI action.

Here’s Nvidia’s weak point: it boasts a huge profit margin. For the past quarter, Nvidia churned out a net income of $14.88 billion on its $26 billion revenue. That’s a clear invitation for other players in the ecosystem to swoop in and attack that profit margin.

Rivals such as AMD (ticker: AMD ) could be looking to get involved in the battle for margin and launch a product that’s slightly better, slightly faster, and slightly cheaper than what Nvidia is making. The incentive is there — the question is when will a rival roll out a competitive product worthy of attention?

Let’s Hear from You!

What’s your take on Nvidia and the AI race? Do you own Nvidia shares or maybe AMD shares? Join the discussion below.

Nvidia Unveils Rubin AI Platform: New Frontier in Generative AIAt the 2024 Computex trade show in Taipei, Nvidia CEO Jensen Huang sent ripples through the tech world with the announcement of their next-generation AI platform, codenamed Rubin. Scheduled for release in 2026, Rubin promises to be a game-changer, pushing the boundaries of generative AI and accelerating its integration across various industries.

Huang's vision is clear: a new industrial revolution driven by AI. This vision is fueled by the ever-growing demand for high-performance AI hardware, and Nvidia is positioning itself at the forefront of this revolution. By unveiling Rubin alongside the Blackwell Ultra chip slated for 2025, Nvidia is signaling a commitment to annual upgrades in their AI accelerator technology.

This focus on rapid development reflects Nvidia's dominant position in the AI chip market, currently holding an estimated 80% market share. Rubin's arrival in 2026 signifies a significant leap forward in Nvidia's AI hardware capabilities. The platform will encompass not just next-generation GPUs, the workhorses of AI training, but also novel central processing units (CPUs) and networking chips.

While specifics about Rubin's architecture remain under wraps, some key details have emerged. The platform will leverage the next iteration of High-Bandwidth Memory (HBM4), a crucial component for tackling the data bottlenecks that often hinder AI development. Manufacturers like SK Hynix, Micron, and Samsung are expected to be instrumental in supplying this next-gen memory.

Beyond the hardware, Huang emphasized the importance of software and services in democratizing AI. This aligns with Nvidia's recent efforts to expand its software offerings, providing developers with user-friendly tools to harness the power of their AI hardware. It's likely that Rubin will be accompanied by a robust software ecosystem, enabling seamless integration and streamlined workflows for various AI applications.

The potential applications of Rubin are vast. Generative AI, a subfield of AI focused on creating new data, is expected to see a significant boost. This could revolutionize fields like drug discovery, where AI can be used to design new molecules with specific properties.

Additionally, advancements in natural language processing (NLP) facilitated by Rubin could lead to more sophisticated chatbots, capable of carrying on nuanced conversations and even generating creative text formats like poems or code.

However, significant challenges remain. Ethical considerations surrounding bias in AI algorithms and the potential misuse of generative AI capabilities need to be addressed. Additionally, ensuring equitable access to this powerful technology will be crucial to prevent exacerbating existing inequalities.

Despite these challenges, the potential benefits of Rubin are undeniable. Nvidia's commitment to annual advancements in AI hardware, coupled with a focus on user-friendly software, positions Rubin as a catalyst for the widespread adoption of AI across industries. As 2026 approaches, the tech world will be watching with keen interest to see how Rubin ushers in a new era of generative AI and its impact on the global landscape.

$GME 27 AFTER EARNINGS !!NYSE:GME 27 AFTER EARNINGS !!

Improved Net Income and Turnaround Efforts:

GameStop turned a net profit in 2023 for the first time since 2017, indicating a significant improvement in its financial performance. The company's ability to continue generating a net profit and restoring positive free cash flow is crucial for its turnaround and could boost

investor confidence, potentially driving the stock price up.

Revenue per Employee: GameStop is producing the second-most revenue per employee in the Specialty Retail industry among companies with over $1 billion market cap and over 1,000 employees. This high revenue efficiency could be a positive signal for investors, as it suggests the company is effectively utilizing its workforce to generate sales.

Share Buybacks: GameStop's increased EDGAR activity in April 2024 might indicate the company has been actively buying back shares.

Share buybacks can reduce the number of outstanding shares, potentially increasing the value of each remaining share and driving up the stock price.

New Investment Policy: The company's board approved a new investment policy that permits GameStop to invest in equity securities, among other investments. This new policy could lead to new revenue streams or strategic partnerships, which might positively impact the company's stock price.

Market Sentiment: The stock has been volatile in the past, with significant price movements driven by retail investor interest and short squeezes. Positive earnings results could trigger a renewed interest from retail investors, potentially driving up the stock price.

Product Expansion: GameStop is known for its video game-related products. However, tweets mention the company's expansion into other areas such as controllers, wall chargers, keyboards, and headsets. This diversification could attract new customers and increase sales.

Clearance Sales: Encouraging customers to purchase clearance items can help GameStop improve its revenue. This strategy could be part of the company's efforts to manage inventory and boost sales.

$DOCU 60 -70 - 80 AFTER EARNINGS ? NASDAQ:DOCU

60 -70 - 80 AFTER EARNINGS ?

6 REASONS !!

Strong Quarterly Earnings: DocuSign has shown strong financial performance in the recent past, with its stock price rising after reporting strong earnings. This indicates a positive market response to its financial performance, which could lead to a higher stock price in the future.

Increased Price Targets by Analysts: Analysts have increased their price targets for DocuSign, with some predicting a potential rise to $65.

These optimistic forecasts suggest that the market and analysts have confidence in the company's future growth and performance.

Positive Market Sentiment: The market's response to DocuSign's earnings reports has generally been positive, with the stock price rising after strong earnings reports. This suggests that if DocuSign continues to report strong earnings, the market could respond positively, potentially pushing the stock price towards $65.

High Growth Potential: Analysts predict that DocuSign's earnings and revenue will grow significantly over the next 3 years. This high growth potential could attract investors and drive up the stock price.

Market Leadership: DocuSign is a market leader in the e-signature and contract management space. Its strong market position and broad scope of agreement workflows could contribute to its continued growth and success, potentially leading to a higher stock price.

Positive Industry Outlook: The e-signature and contract management industry is expected to continue growing, driven by the increasing need for digital solutions to streamline agreement processes. As a leader in this space, DocuSign is well-positioned to benefit from this industry growth.

$TM 220 - 240 - 25O AFTER EARNINGS ?NYSE:TM 220 - 240 - 25O AFTER EARNINGS ?

6 REASONS !!

Strong Quarterly Earnings: Toyota has shown strong financial performance in the recent past, with its profit in the latest quarter jumping nearly threefold from a year ago as vehicle sales grew globally. This indicates a strong demand for Toyota's vehicles and the company's ability to capitalize on this demand, which could positively impact its stock price.

Increased Net Profit Forecast: Toyota ramped up its annual net profit forecast to $26.1 billion after reporting it more than doubled in the first six months of the year. This indicates the company's confidence in its future performance, which could boost investor confidence and drive up the stock price.

Record High Stock Price: Toyota's shares hit a record high after reporting strong earnings and raising its fiscal-year earnings forecast. This shows that the market responds positively to

Toyota's financial performance, and further strong earnings could lead to a higher stock price.

Year-on-Year Earnings Growth: Despite a recent decline in earnings quarter-on-quarter, Toyota's earnings are up +97% year-on-year. This indicates a strong recovery and growth trajectory, which could lead to a higher stock price in the future.

Positive Market Sentiment: The market's response to Toyota's earnings reports has generally been positive, with the stock price rising after strong earnings reports. This suggests that if Toyota continues to report strong earnings, the market could respond positively, potentially pushing the stock price towards $250.

Dividend Yield: Toyota pays an annual dividend of $5.10 per share and currently has a dividend yield of 2.38%. This could attract investors looking for stable returns, potentially driving up the stock price.

NVIDIA: Very Limited Upside Potential - A ScenarioNote: While predicting the future is impossible, the following game plan is based on an analysis of current events, historical patterns, market bubbles, and the growing public fear of artificial intelligence.

Please bear in mind that I am an extropist who has been dreaming of the Singularity since I was seven years old, with a keen interest in financial and technological privacy.

1. Current Market Capitalization

Unsustainable Levels:

As of May 30th, 2024, Nvidia's market capitalization stands at a staggering $2.82 trillion USD. This valuation reflects extremely high growth expectations and significant optimism about Nvidia's future prospects. However, such a lofty valuation may not be sustainable in the face of potential risks and headwinds.

Valuation Metrics:

Key valuation metrics such as the Price-to-Earnings (P/E) ratio are also at historically high levels, indicating that the stock is priced for perfection. Any deviation from expected growth or profitability could lead to sharp corrections.

2. AI Regulation in 2025

Intensive Regulations:

There are growing concerns that the AI industry, which Nvidia heavily relies on for growth, will face stringent regulations by 2025. Governments worldwide are increasingly wary of the ethical implications, data privacy issues, and potential misuse of AI technologies.

Impact on Growth:

If new regulations impose strict compliance requirements, limit data usage, or introduce hefty fines, Nvidia's AI-driven revenue could be significantly impacted. Compliance costs would rise, innovation might slow down, and the overall profitability could decline, leading to reduced investor confidence and lower stock valuations.

3. Incoming Lawsuits

Patent Infringements and IP Disputes: Nvidia is frequently involved in legal battles over intellectual property and patent infringements. As the company expands its technology portfolio, the risk of lawsuits increases, which can lead to costly settlements or prolonged legal battles.

Class Action Lawsuits: There is also the potential for class action lawsuits from shareholders if Nvidia fails to meet its lofty expectations or if there are any perceived misrepresentations of its business prospects. Legal troubles can drain resources and divert management attention from growth initiatives, negatively impacting stock performance.

4. Geopolitical Risks: China Invading Taiwan / World War 3

Supply Chain Disruption: Taiwan is a critical hub for semiconductor manufacturing, with companies like TSMC (Taiwan Semiconductor Manufacturing Company) playing a crucial role in Nvidia's supply chain. An invasion by China could disrupt this supply chain, leading to shortages, production delays, and increased costs for Nvidia.

Market Sentiment: Geopolitical instability typically spooks investors, leading to market sell-offs. A conflict involving Taiwan would create uncertainty around Nvidia's ability to maintain its production levels and meet market demands. This uncertainty can drive investors to pull out, causing a decline in stock prices.

Trade Restrictions: In the event of a conflict, the US and its allies might impose sanctions or trade restrictions on China, further complicating Nvidia's operations and supply chain. These restrictions could limit Nvidia's access to essential materials or technology, affecting its long-term growth prospects.

5. Social Unrest Due to AI Impact

Mass Riots Over Job Losses: As AI technology advances, millions of jobs are at risk of being automated. This could lead to significant social unrest as people face unemployment and economic hardship. Mass riots and protests against AI-driven job displacement could create a hostile environment for companies like Nvidia, leading to negative public perception and potential backlash.

Intellectual Property Theft Concerns: AI technologies have been criticized for infringing on the intellectual property rights of artists and creators. This could lead to increased legal challenges and a loss of support from the creative community. Public outcry and legal actions from artists claiming that their work is being used without permission could further tarnish Nvidia's reputation and create financial liabilities.

In Conclusion:

While Nvidia has enjoyed a remarkable rise in its stock price, several factors suggest that its current valuation might be unsustainable. The potential for heavy AI regulations, a surge in lawsuits, geopolitical risks related to China and Taiwan, and social unrest due to AI-driven job losses and intellectual property theft present significant headwinds. Coupled with the current market capitalization at an unprecedented $2.82 trillion USD, these factors collectively argue for a more cautious outlook, suggesting that Nvidia's stock may not have much room to rise further and could even face a significant correction.

And as Always: This is NO Financial Advice, Do your own Research.

CYANE

NVDA May 29 Update #NVIDIA #NVDANVDA investors had a fantastic day yesterday, after the Green Gold skyrocketed and hits the 1040. during the night trading sessions the stock touched the 1060, and we are now seeing a major correction at the pre market session.

Investors can secure profits by setting a stop limit order at 1113 or 1084 depend on how aggressive you are.

Target price before the stock splits was estimated to be around 1200 which is very close ahead, and it can be reached by the end of today or by Friday max.

Can we go back to reality?Congratulations NVDA, because you delivered everything you could deliver in terms of good results, however, can we get back to reality?

Will the Black Monday that we experienced in 1987, in the DOW JONES index, be experienced again in 2024, and thanks to NVDA and technology companies?

We know what happened between 1980 and 1985 to the American economy, right?

It is known that in the 1980s and early 1990s, dollars could circulate freely around the world, so much so that we had a global economic miracle, and the world was swimming in booming growth.

But, at the current moment, dollars can no longer circulate freely around the world (FED, China, Russia) and continue contributing to global growth? Therefore, the technological war we are experiencing today (chips and electric cars), diverted dollars to these sectors, further inflating this bubble that is about to burst.

Speaking of electric cars, China is firmly dumping its electric cars around the world at very reasonable prices (as it has no intention of breaking its internal market – control), once and for all destroying the automobile industry in many emerging countries, oh my, no?

Let's go graphics.

Monthly: NVDA has reached the three golden levels of the FIB of the SETUP used, so there is nowhere else to go. So, SPX, get ready.

The red lines are resistance points.

Weekly: With the brilliant financial report recently released, prices are ready to seek the golden region of this chart period.

The red lines are resistance points.

Daily. Prices have reached the region of 100% of the bullish pivot.

The red lines are resistance points.

Do your analysis and good business.

Be aware, if you buy, use stop loss.

See other graphical analyzes below.

A Golden Age for Splits? Nvidia's MoveNvidia's recent announcement of a 10-for-1 stock split sent ripples through the tech industry. Investors cheered the move, with the stock price surging 9% to a record high. But beyond the immediate impact on Nvidia, Bank of America (BofA) suggests this could be the first domino in a wave of tech stock splits. This article explores the implications of Nvidia's split, the factors driving potential future splits, and the historical trends associated with this strategy.

Nvidia's Split: A Catalyst for Change?

Nvidia's stock price, hovering around $1,000 before the announcement, undoubtedly played a significant role in the decision. With a lower share price after the split, the stock becomes more accessible to individual investors, potentially broadening its investor base. This aligns with BofA's observation that Nvidia is already a favorite among retail investors, according to a May 22 Vanda Research report.

BofA analysts see the split as a positive sign, highlighting a trend of "shareholder-friendly policies" within large-cap tech companies. They also point to historical data suggesting that companies undergoing splits tend to experience strong returns in the following year.

A Landscape Ripe for Splits?

BofA's note identifies 36 companies within the S&P 500 with share prices exceeding $500, potentially making them candidates for future splits. This includes tech giants like Microsoft and Meta Platforms, whose stock prices are approaching that threshold.

There are several factors making the current tech landscape ripe for stock splits:

• Soaring Stock Prices: Fueled by technological advancements and strong demand, many tech stocks have experienced phenomenal growth in recent years. This has pushed share prices to record highs, potentially creating a psychological barrier for some retail investors.

• Accessibility and Liquidity: A lower share price can make a stock more attractive to individual investors, increasing overall trading volume and liquidity. This broader investor base can potentially lead to a more stable stock price.

• Psychological Impact: A lower share price can make the stock appear more affordable, even if the underlying value of the company remains unchanged. This can trigger increased buying interest, particularly among retail investors.

Beyond Price: The Strategic Considerations

While share price is a key factor, companies considering a split should also weigh other strategic considerations:

• Signaling Confidence: A stock split can be seen as a sign of management's confidence in the company's future growth potential. This positive signal can improve investor sentiment and potentially attract new investment.

• Maintaining Momentum: A well-timed split can capitalize on a company's positive momentum, further propelling its stock price upwards. However, a poorly timed split during a market downturn might not yield the desired results.

• Cost and Complexity: Implementing a stock split involves administrative costs and logistical complexities that companies need to consider.

Historical Trends and Potential Outcomes

BofA cites historical data showing that stock splits have generally been followed by positive returns. They argue that splits don't dilute the company's value, but rather make it more accessible to a broader investor base. This can lead to increased trading activity and potentially higher valuations.

However, it's important to note that correlation doesn't imply causation. While past trends suggest positive outcomes, future performance remains subject to market conditions and individual company fundamentals.

The Road Ahead: A Spliting Tech Future?

Nvidia's stock split has reignited the conversation around this strategy within the tech industry. With numerous companies sporting high share prices, BofA's prediction of a potential wave of splits holds merit. This trend, if it materializes, could have several implications:

• Increased Retail Investor Participation: Lower share prices could attract more retail investors to the tech sector, potentially boosting overall market activity.

• Enhanced Liquidity: Broader investor participation can lead to higher trading volumes and improved liquidity for these tech stocks.

• Short-Term Volatility: The implementation of splits could lead to short-term market volatility as investors adjust their positions.

Conclusion

Nvidia's stock split may be a harbinger of a larger trend within the tech sector. Companies with high share prices might consider following suit to broaden their investor base and potentially enhance long-term value. However, the decision to split should be a strategic one, carefully evaluating both the potential benefits and the associated costs and complexities. As the market watches Nvidia's post-split performance, it will be interesting to see if this move ushers in a new era of tech stock splits and how it shapes the investment landscape in the coming years.

⭐NVIDIA - 'Best Buy of the Decade?' (2 years later...) 👈🙄Best feature of Tradingview?

That everything stays, nothing can be amended or edited or deleted.

⏰ Jul 15, 2021:

⭐NVIDIA - Best Buy of the Decade? ⭐⭐⭐⭐ :

Some of the comments back then were:

❤️🩹Short it or you will regret it

❤️🩹It was a great buy few years ago. Key word, WAS.

❤️🩹holy f, have you done some valuation analysis? god tier company, the future of mankind. but stock=/=company, insanely overpriced

2 Years later everyone talks about NVIDIA as AI brings near a trillion-dollar valuation.

No further comment other than that i see Major resistance at 449-470$

One Love,

the FXPROFESSOR ⭐🙄

NVIDIA NVDA - Breaking Upward towards $1000?NVIDIA NVDA continues to swing upwards. We are keeping an eye on the $1000 level. Is this a good time for a call Option entry?

Nvidia Shares Soar 8.43% After Stellar EarningsChip stocks soared in out-of-hours trading on Wednesday and Thursday after chipmaker Nvidia ( NASDAQ:NVDA ) smashed Wall Street's expectations with its latest earnings report, continuing a period of extraordinary growth as booming interest in artificial intelligence propels the tech sector to new heights. Shares for Nvidia ( NASDAQ:NVDA ) climbed nearly 8% during after-hours trading on Wednesday, peaking above $1,000 per share for the first time. While these gains have pared a little in the hours since Nvidia’s earnings report, shares for the California-based company were still up by more than 6% at the time of writing on Thursday morning.

Nvidia ( NASDAQ:NVDA ) shares are currently trading at around $1,030, putting the chipmaker on track to surpass the $1,000 milestone and hit an all-time high when markets open on Thursday. Other chipmakers benefiting from intense interest in artificial intelligence include shares for Taiwan Semiconductor Manufacturing Company, Arm Holdings, Dell Technologies, and Super Micro Computer Inc., which were all up between 3% and 6% during pre-market trading.

Nvidia ( NASDAQ:NVDA ) released its hotly anticipated earnings report for the first quarter of 2024 on Wednesday afternoon, which smashed Wall Street’s expectations and marked the company’s most profitable quarter ever. Respectively, profits and sales were up 628% and 268% compared to the same time period last year, Nvidia ( NASDAQ:NVDA ) said, reporting $6.12 earnings per share and $26 billion in sales for the three-month period ending April 30.

The release of OpenAI’s generative AI chatbot ChatGPT in 2022 ignited a global race among tech companies to build and deploy ever more advanced AI systems. The race has spurred stellar demand for the kinds of advanced computer chips required to maintain, run, and develop these AI systems, and Nvidia, formerly known for its gaming hardware, is one of the world’s leading beneficiaries for this demand and has become a bellwether for interest in the sector.

Nvidia's profit soars, underscoring its dominance in chips for artificial intelligence. Its net income rose more than sevenfold compared to a year earlier, jumping to $14.88 billion in its first quarter that ended April 28 from $2.04 billion a year earlier. Revenue more than tripled, rising to $26.04 billion from $7.19 billion in the previous year.

Technical Outlook

Nvidia's (NVDA) stock is up 8.97% in Thursday's market trading riding high with a Relative Strength Index (RSI) of 71.60 placing NASDAQ:NVDA in an overbought territory, hence a trend reversal is along the horizon in the long term.

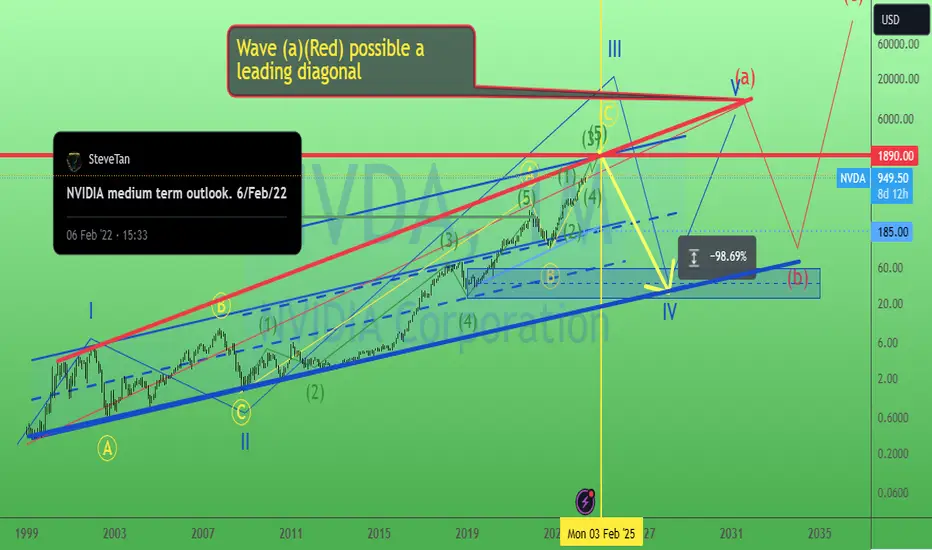

NVIDIA biggest pic. 23/May/24NVDA possible forming a leading diagonal pattern in wave (a)(Red). P/s. It seem like 99% stocks/index chart "showing" year 2025...

NVIDIA. short term swing setup. 23/May/24NVDA just announced a 10-for-1 stock split. So it will be more affordable at $100 +/- than $1000 and "this chart" will be "out of proportion". Support would be @ $900 or 90 +/- (after splitting) if there is a pullback.

Nvidia - Earnings, Channel, $1.000!Hello Traders and Investors, today I will take a look at Nvidia .

--------

Explanation of my video analysis:

If you are objectively looking at the stock chart of Nvidia, you can see that Nvidia is currently trading in a solid rising channel formation. But as we are speaking, Nvidia is retesting the upper resistance and considering that we just saw a rally of +700% without any real correction, it is quite likely that we will see at least a short term bearish rejection from here.

--------

Keep your long term vision,

Philip (BasicTrading)

NVIDIA - ready for the earnings?

Regarding Nvidia, we maintain our view that Wave ((iv)) has concluded, and we are currently on the path to completing the overarching Wave 3. We anticipate this wave to reach between $1032 and $1300, which we consider the maximum potential target range for now.

We observed an accumulation phase from June 2023 to January 2024. This area might become significant again, possibly next year, as a zone for placing new entries. Currently, the market has left a lot of imbalances and shows very little volume on the way up because the price has been consistently surging.

With the earnings report due today, we can expect around 8.7% volatility in either direction, depending on the earnings outcome. It’s common to see even greater fluctuations than anticipated during such events. We will find out this evening after the market closes. For now, everything points towards the continuation of the upward trend.

Zooming in, it's clear that since reaching the 461.8% level, where we perfectly completed Wave ((iii)), we have seen the formation of Waves (i) and (ii) in the current move to complete wave ((v)). We anticipate expanding this upwards within the trend channel. Our tentative expectation is that the upcoming earnings report might outperform expectations, which would align with the chart’s indications.

If earnings exceed expectations, we could see a spike to a new all-time high, followed by a retracement marking Wave (iv) and then an overshooting Wave (v).

The target zones for Wave ((v)) are similar to those of Wave 3, lying between the 50% and 61.8% Fibonacci extensions. Specifically, we are looking at a range between $1123 and $1192.

After reaching these levels, we expect a significant pullback towards the Wave 4. This scenario would align with typical Elliott Wave patterns and provide opportunities for strategic entries and exits.

Nvidia Earnings Poised for Surge as AI Adoption Faces ScrutinySemiconductor giant Nvidia prepares to deliver its first-quarter earnings report on Wednesday, a closely watched event for investors gauging the health of the artificial intelligence (AI) sector.

Market Expectations Point to Explosive Growth

Analysts anticipate a banner performance from Nvidia, fueled by surging demand for its AI chips. Revenue and profits are projected to exhibit exponential growth, with estimates suggesting:

Adjusted earnings per share: $5.65 (400% year-over-year increase).

Revenue: $24.69 billion (200% increase from the prior year).

The Data Center segment, driven by cloud service providers like Amazon and Google, is the primary growth driver. The Gaming segment also contributes positively.

Emerging Challenges in the AI Landscape

Despite positive projections, Nvidia faces potential headwinds:

Transitional Hiccups: The shift from Hopper to Blackwell architecture might cause temporary sales slowdowns as customers wait for the new, more powerful chips.

Competitive Pressures: Tech giants like Amazon developing custom AI chips could threaten Nvidia's market share.

Positive Outlook Prevails Despite Cautious Optimism

Overall sentiment remains optimistic. Nvidia is a leader in the AI chip market, with analysts bullish on its future. The stock price has reflected this confidence with a recent strong performance.

Upcoming Earnings Report: A Critical Barometer

Wednesday's earnings report will be crucial for gauging AI sector momentum and Nvidia's ability to navigate technological changes.

Trading Strategy

Buy at: $975.84

Take Profits at:

T.P_1: $986.77

T.P_2: $1000.00

T.P_3: $1028.34

T.P_4: $1051.81

T.P_5: $1085.00

T.P_6: $1114.86

T.P_7: $1146.96

T.P_8: $1161.76

T.P_9: $1191.66

Stop Loss at: $830.06

ALTSEASON is just about to launch!!!According to the historical relationship between ETH & NVDA

The caveat obviously this relationship was far stronger when ETH was validated using GPU's

... but we still have to take note of this relationship in my opinion!

We know a vast majority of the altcoins are still in fact ERC20's ... including all the various L2's like

Arbitrum, Base, Pulsechain and the other various EVM's

A strong eth has a multiplier effect on those S coin prices. As we have already seen this cycle on Solana.

The ETH etf is on the docket to be approved .. it is actually a political necessity now.

like I've been saying we are due are GENERAL altcoin season any day now... not just new coins, or new narratives..

I think all boats will rise in this next ramp up.

? do we get a double bubble like in 2017? or a short 6 months -9 months and end the 4 year cycle early?

NAS100 Hits Record Ahead of NVIDIA but RSI DivergesThe tech-heavy index runs its best month of the year, extending the advance to new record highs. After last week’s CPI moderation, markets strengthened their bets for two rate cuts by the Fed this year, beginning in June. NAS100 now eyes the psychological 19K mark.

On the other hand, the disinflation process has slowed this year and Fed officials have turned cautious around a pivot, adopting a higher-for-longer narrative, while the hawkish commentary continued this week from various policymakers. On the technical side, the RSI did not follow prices higher, in a divergence that creates risk for a pullback towards the EMA200 (black line). Daily closes below it, would pause the bullish bias, but that would need strong catalyst.

Even if a pullback ensues, the path of least resistance is higher. NAS100 has looked past the Fed’s cautious shift, largely due to the generative AI boom and investors now await Wednesday’s results by NVIDIA, its enabler and main beneficiary. After February’s last report, the stock had jumped more than 12% and had lifted NAS100 with it, so there is potential for volatility.

NVIDIA expects new record revenues due to AI demand and growth to the tune of 235% y/y. This would mark a small slowdown in pace and markets will want to see if it can continue to post eyewatering numbers, or if cracks will begin to appear.

Stratos Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd (trading as “FXCM” or “FXCM EU”), previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Trading Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763). Please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this video are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed via FXCM`s website:

Stratos Markets Limited clients please see: www.fxcm.com

Stratos Europe Ltd clients please see: www.fxcm.com

Stratos Trading Pty. Limited clients please see: www.fxcm.com

Stratos Global LLC clients please see: www.fxcm.com

Past Performance is not an indicator of future results.

NVIDIA Earnings May 21 - Will Crypto AI Narrative AGIX Heat Up?Back in Feb 22, 2024 NVIDIA AI chipmaker reported Q4 2023 earnings per share of $5.16 with a posted revenue of $22.1 billion higher than expected. Biggest crypto AI narratives AGIX gained 37%.

Now the biggest question is: "Will AGIX token will lead the crypto market as NVIDIA is going to report earnings of Q1, 2024?"

YES , there is HIGH probability of greater reporting earnings by NVIDIA for Q1, 2024. The fact that Taiwan Semiconductor (TSMC) AI chipmaker Q1 earnings came in higher ($7.3 billion) suggests Nvidia’s could reveal the same.

Trade Setups with TP, SL and Entry is shown in the chart.

Good Luck!!!

NVIDIA Earnings May 21 - Will Crypto AI RNDR Heat Up?Back in Feb 22, 2024 NVIDIA AI chipmaker reported Q4 2023 earnings per share of $5.16 with a posted revenue of $22.1 billion higher than expected. Biggest crypto AI narratives RNDR rose upto 20%. .

Now the biggest question is: "Will RNDR token will lead the crypto market as NVIDIA is going to report earnings of Q1, 2024?"

YES , there is HIGH probability of greater reporting earnings by NVIDIA for Q1, 2024. The fact that Taiwan Semiconductor (TSMC) AI chipmaker Q1 earnings came in higher ($7.3 billion) suggests Nvidia’s could reveal the same.

Trade Setups with TP, SL and Entry is shown in the chart.

Good Luck!!!